ALTG - Alta Equipment Looks Cheap: Proven Model M&A And Online Efforts

2023-07-27 16:11:49 ET

Summary

- Alta Equipment Group increased its expectations for 2023, which could drive stock price growth.

- The company has exclusive commercial agreements with large manufacturers and is expanding its technician headcount.

- Online rental and purchase options could lead to free cash flow and revenue growth.

Alta Equipment Group Inc. ( ALTG ) delivered an increase in its expectations for 2023, and management continues to make acquisitions. With a proven business model, exclusive commercial agreements with large manufacturers, growing technician headcount, and new options for customers to rent and purchase online, Alta Equipment could see growth in its FCF. I did identify several risks from the total amount of debt, new sale of shares, or lack of new agreements with manufacturers, however, I believe that there is an upside potential in the stock price.

Alta Equipment Group And The Recent Guidance Increase For 2023

Alta Equipment Group maintains a network of specialized equipment dealers with a presence throughout the United States and operations that extend to Canada. The company sells, rents, and provides parts and technical support for products such as forklifts, earthmoving equipment, environmental processing equipment, and construction services. The company's activities can be divided into sales of new equipment, sales of used equipment, sales of parts or pieces, repair and maintenance services, and rental of equipment.

Presentation To Investors

Within the territories where it works, Alta Equipment is the official distributor of some well-known original manufacturers such as Volvo (VLVLY), JCB, Kubota (KUBTY), and Hyster-Yale (HY) among others. The company has recently reached a commercial agreement to officially distribute Nikola Corporation (NKLA) electric vehicles in New York and Pennsylvania. The variety of origins and activities of its clients include companies from the industrial or construction field as well as the food and medical sectors. None of these clients represented more than 1% of the company's revenue by 2022, while the top ten customers of the company account for 5% of its annual revenue.

The business is organized into two operating segments: materials handling and construction. Construction represents a higher percentage in the company's financial figures. Both segments evolve in parallel and allow Alta a diversified business profile.

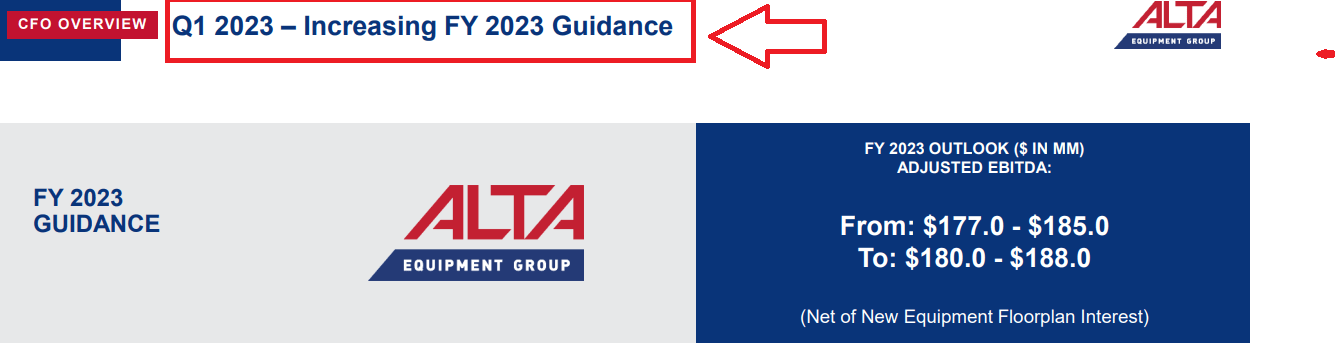

With that about the business model, I believe that the most interesting about Alta Equipment is its recent guidance increase for the year 2023. From adjusted EBITDA close to $177-$185 million, the company raised its expectations to about $180-$188 million.

{kind=link}

Other analysts are expecting net sales growth close to 7%-5% in 2024 and 2025 along with EBITDA growth and net income growth. 2025 EBITDA would stand at close to $214 million, and 2025 FCF would be close to $40 million with an FCF/Sales of 1.9%.

Marketscreener.com

Balance Sheet

In the quarter ended March 31, 2023, Alta Equipment reported an optimistic increase in the total amount of assets driven by increases in inventories, property, plant, and equipment, and goodwill. I believe that increases in inventories and properties will be appreciated by investors. In my view, it may mean that management expects to sell more in the short term future.

More in particular, management noted cash worth $1.7 million, accounts receivable of $228.3 million, inventories close to $469.1 million, prepaid expenses and other current assets worth $30.4 million, and total current assets of $729.5 million. Total current assets are larger than the total amount of current liabilities, so I believe that liquidity does not seem an issue for Alta Equipment.

Long-term assets include property and equipment worth $398.9 million, operating lease right-of-use assets of $111.4 million, goodwill close to $70.5 million, and total assets of $1.376 billion .

10-Q

The total amount of liabilities increased due to increases in the line of credit and increases in floor plan accounts payable. The debt to equity ratio stands at close to 6x, and the financial debt to EBITDA is equal to 4x.

YCharts

In my view, some investors may be a bit concerned about the total amount of debt. If the company reduces its total amount of leverage, the EV/EBITDA would most likely trend up. The current EV/EBITDA of close to 6.5x appears quite low for Alta Equipment.

Presentation To Investors

The ratio of assets/liabilities stands at more than 1x, so I believe that the balance sheet appears quite stable. With that, it is worth having a look at the debt and obligations of Alta because they are not small.

First, floor plan payable for new equipment stands at $252.5 million. The company also reported a current portion of long-term debt close to $4.7 million, accounts payable worth $88.1 million, and current deferred revenue worth $12.6 million.

Long-term debt net of the current portion stood at $311.3 million, with finance lease obligations of close to $17.7 million and long-term operating lease liabilities worth $100 million. Finally, with deferred tax liability of $6.3 million, total liabilities were $1.238 billion.

10-Q

DCF Model

From the recent information about the guidance for 2023, I assumed that Alta Equipment will likely continue to enjoy end-market demand and a beneficial pricing environment in the coming years.

Presentation To Investors

Besides, I believe that growing technician headcount and strong rental utilization will most likely have a good impact on future earnings. Considering previous headcount growth, I do not see why hiring of personnel would slow down.

YCharts

I would also expect further commercial exclusivity agreements to distribute parts from original manufacturers in new territories. This does not only include access to the sale of equipment, but also access to manufacturers' software that allows solving and correctly maintaining the needs of their customers. As a result, I believe that we may see further net sales growth.

I believe that the placement of a high number of products in these markets will most likely lead to increases in the income given by technical and repair services. Besides, in my view, the increase in the purchase and sale cycles and the rental offer will have a beneficial increase in the demand for this type of service.

Customers seem to prefer online rentals, which may go against the classic business models offered by Alta. With this in mind, the company has carried out adaptation processes in its sales channels to include online options, which, in my view, will have a beneficial impact in the coming years. More transactions online will most likely lead to larger FCF margins and growing FCF.

Lastly, Alta has successfully made a significant number of acquisitions in the regions where it already has a significant position in the markets and the areas of future expansion, such as some areas of Canada or the East coast of the United States. Under this DCF model, I assumed that new acquisitions will be successful. As a result, I would also expect further economies of scale and larger EBITDA margins.

Presentation To Investors

Those who believe that the current debt level may not allow new acquisitions may need to have a look at the recent acquisitions executed by Alta Equipment. For instance, in 2023, the company acquired M&G, a privately held Yale dealer. I believe that banks appreciate quite a bit the business model of Alta, and will most likely finance new transactions in the coming future.

Our growth strategy is predicated on making strategic acquisitions that expand our geographic reach, broaden our capabilities and service offerings and diversify our customer and supplier bases. We believe these acquisitions, both immediately and over the long-term will be accretive to our financial performance. To that end, on March 1, 2023 the Company purchased the assets of M&G, a privately held Yale dealer with a presence in Rhode Island. With the acquisition, the Company now offers material handling customers in Rhode Island both Hyster and Yale branded products. Source: 10-Q

My DCF model included 2033 net sales worth $3.075 billion, 2033 net income close to $217 million, and depreciation and amortization of about $311 million. Besides, with gain on sale of rental equipment assumed to be close to -$134 million, provision for inventory obsolescence worth $4 million, and changes in deferred income taxes of about $14 million, I included changes in accounts receivable of -$175 million.

If we also include changes in inventories worth -$1.116 billion, proceeds from sale of rental equipment worth $324 million, changes in manufacturers' floor plans payable worth $647 million, and accounts payable close to $69 million, 2033 CFO would be $236 million. Finally, with 2033 expenditures for property and equipment worth -$60 million, 2033 FCF would be about $177 million.

My DCF Model

My results also included an enterprise value worth $1.358 billion. Besides, with cash of about $1 million, and subtracting the current portion of long-term debt worth $4 million, line of credit of $256 million, long-term debt, net of current portion of $311 million, and finance lease obligations of $17 million, the implied equity is $770 million. Finally, the implied price would stand at $23.8 per share.

My DCF Model

A Lot Of Small Competitors

There are a large number of participants in the area of ??the sale, loan, and distribution of specific pieces, generating a highly competitive environment that has not fully consolidated. This fragmentation is given by small companies that operate at the regional level through exclusive commercial agreements and others that, like Alta, have a distribution network at the national level. Competition is also given by distributors that offer other brands of products. Smaller competitors will most likely benefit from the company's inorganic strategy.

On the other hand, when it comes to exclusive distribution agreements, Alta has no competition in these territories, either in terms of original parts or repair parts. This factor is accompanied by the maintenance services that arise and are added to the company's own commercial activity.

Risks

Alta Equipment is directly dependent on the activities of the original manufacturers to fulfill its sales cycle. This dependency deepens if we think about the industry sectors that make the most purchases from the company, such as construction and material handling. In any case, the company has managed to maintain a highly diversified client portfolio that allows it to avoid complications in the event of the cessation of activity of any of these. However, this diversification is not manifested in what concerns its suppliers, since almost 50% of the parts that the company sells come from the few companies that I named above.

Another comment in an operational sense is that the contracts that Alta maintains with the manufacturers do not have renewal obligations. In the same way, the variations in the prices of original parts and the ability to market the products with a favorable margin as well as the ability to pay in the event of an increase are daily risk factors for its activities.

In another sense, Alta reports considerable debts that could deny it access to the capital and liquidity flows necessary to maintain activities as well as to meet its clients' deadlines. Along with this, the implementation of its business strategy is also endangered by this factor, in case of not achieving success in future acquisitions or the integration of these into its business model.

Considering the total amount of debt and the M&A expectations, I believe that Alta could sell equity in the coming months to finance its operations. Very recently, the company announced the sale of 2,200,000 shares. I believe that certain shareholders may dislike the increase in the share count, which may lower the demand for the stock, which may represent a risk.

Alta Equipment Group Inc. announced the pricing of an upsized underwritten secondary offering of 2,200,000 shares of its common stock, par value $0.0001 per share at a price to the public of $16.25 per share. Source: Alta Equipment Group Inc. - Alta Equipment Group Inc. Announces Pricing of Upsized Secondary Offering of Common Stock

Conclusion

Alta Equipment recently delivered an increase in its 2023 EBITDA expectations, which may accelerate the demand for the stock in the coming months. In my view, the introduction of online options for customers, M&A, growing technician headcount, and commercial exclusivity agreements with new large manufacturers would serve as a revenue catalyst. Additionally, I believe that expansion into new territories and new products from new manufacturers may also accelerate economies of scale, which could push the FCF up. Even considering risks from the lack of new exclusive commercial agreements, sales of equity, or risks from the total amount of debt, Alta could trade at more than its current EV/EBITDA level. I do believe that there is certain undervaluation.

For further details see:

Alta Equipment Looks Cheap: Proven Model, M&A, And Online Efforts