AYX - Alteryx: After Massive Q4 This Stock Is Ready To Rally

Summary

- Alteryx surged 7% after reporting incredibly strong Q4 results that featured ~30% y/y growth in ARR and ~70% y/y growth in revenue.

- Revenue comps will get tougher as Alteryx laps the maturing of its SaaS transition last year, but profitability will continue to shine as the company is posting double-digit operating margins.

- Continued high net expansion rates on Alteryx's growing ARR base, plus the company's high gross margins, will continue to feed scalable growth for years to come.

- Trading at just 6x forward revenue, Alteryx is still quite cheap for its fundamental profile.

With this year's rampant rally in tech stocks, the common question that many investors are asking is if it's already too late to dive into the rally. My answer is of course it's not: but stock selection is key here. We're looking for stocks with decent value that are also posting strong results, have meaningful profits or at least a trajectory to breakeven, and won't be overly impacted by tightening macro conditions.

Alteryx (AYX) fits the bill perfectly here. This data-integration software company has just reported blazing Q4 results, taking its year-to-date recovery to ~30%. Despite the generous rebound so far, I think Alteryx (still below half of its 2020 all-time highs) has plenty of steam left for a continued rally.

After parsing through Alteryx's latest results, I am even more bullish on the stock now and am keen to add more to my position as Alteryx builds strength. Now, Alteryx of course is not immune to macro headwinds. Backend IT projects like Alteryx, for many companies, are "nice to haves" in the current economy rather than mission-critical, and Alteryx has reported that especially in the fourth quarter rising scrutiny on deals has elongated sales cycles and delayed closings.

That being said, when we look to the long term, we continue to see companies elevating the importance of data-driven decision making and using technology to drive as much efficiency as possible. Now largely a SaaS play rather than an expensive license product, Alteryx is perfectly positioned to capture this growing market.

Here is my full bull thesis for Alteryx:

- Digital transformation is already underway - Companies want to use data to drive decisions. Unfortunately, data is sometimes locked in different formats and takes hours of manual work to untangle. Alteryx's technology helps with that process and automates one of the most labor-intensive pieces of adopting a "big data" strategy in the C-suite. Investing in technology like Alteryx may not have been a top priority during the pandemic, but it will become a much hotter-button topic as we look ahead.

- $113 billion 2025 TAM - Alteryx's current ~$1 billion annual revenue run rate is only a fraction of its estimated current $65 billion TAM, leaving plenty of room for growth. Alteryx additionally expects its TAM to expand to $113 billion by 2025.

- Truly horizontal software serving a wide variety of use cases across many industries - Alteryx's software is broadly applicable to clients in virtually any industry. An illustrative cross-section of Alteryx's customer base: Netflix ( NFLX ), Walgreens ( WBA ), Abbott Laboratories ( ABT ), Chevron ( CVX ), Wells Fargo ( WFC ), Visa ( V ), Marriott Hotels ( MAR ), and Facebook ( META ) are all among Alteryx's anchor clients, spanning every industry.

- Best-in-class gross margins of ~90% are among the highest in the software industry - Virtually every dollar of revenue for Alteryx flows through to the bottom line, justifying the efforts that Alteryx makes on the initial sale.

- Plans for significant profitability - Already, Alteryx has hit significant pro forma operating profits. Over the long run, it plans to generate pro forma operating margins in the 25-30% range, primarily by achieving economies of scale on sales and marketing. When a company like Alteryx has huge recurring revenue, over time the cost of sales support for that revenue base will eventually dwindle.

A quick checkup on Alteryx's valuation: at current share prices near $64, Alteryx trades at a market cap of $4.44 billion. After we net off the $432.0 million of cash and $877.5 million of convertible debt on Alteryx's most recent balance sheet, Alteryx's resulting enterprise value is $4.89 billion.

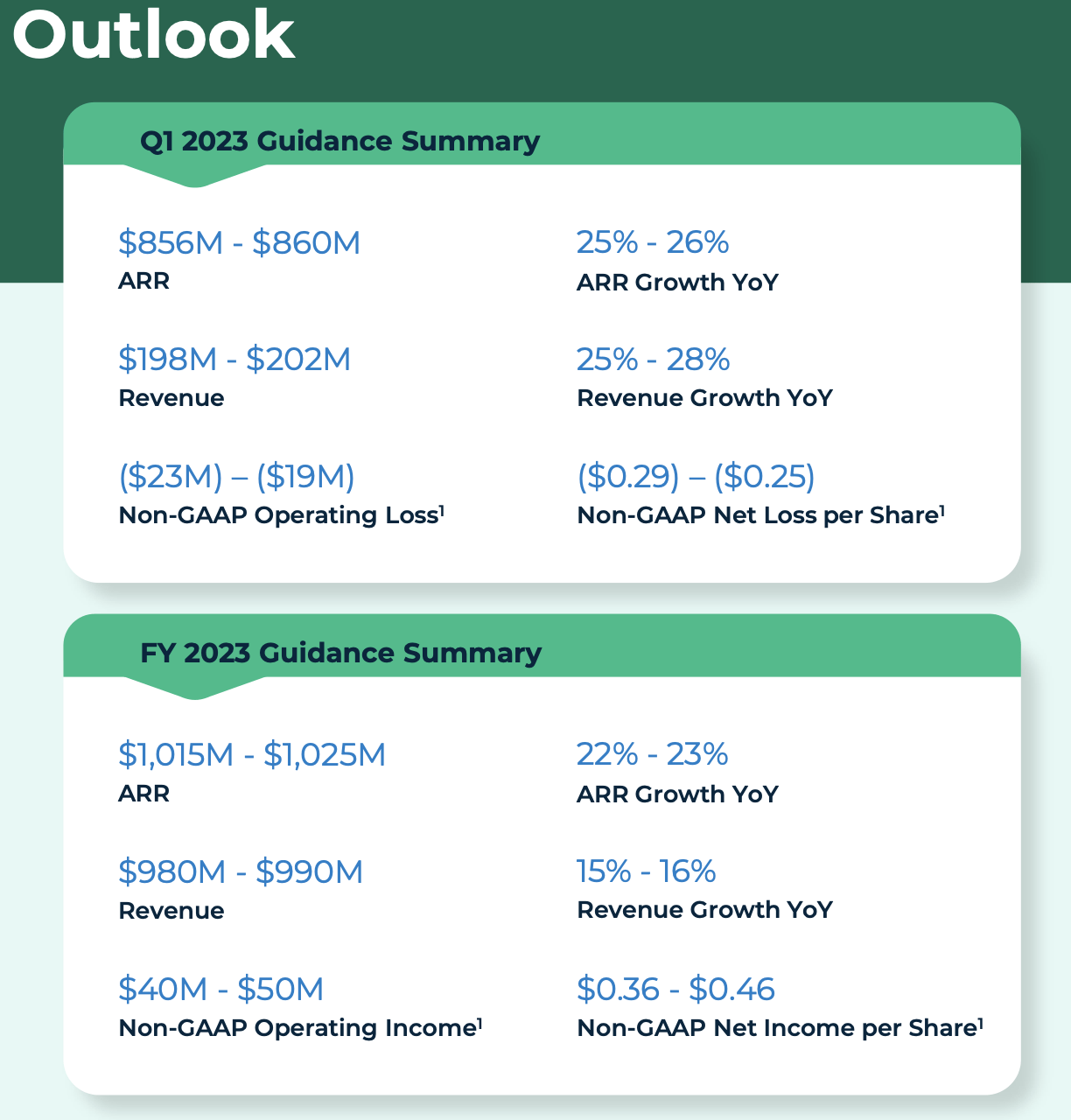

Meanwhile, for the current fiscal year FY23, Alteryx has guided to $980-$990 million in revenue, representing 15-16% y/y growth. Note that Alteryx is coming off a Q1 in which revenue grew >70% y/y. Notably, comps will get tougher in the prior-year period as Alteryx laps the maturation of its SaaS transition (recall that in the early days of switching over from a license to a subscription model, software companies will take a hit to revenue due to deferring over time what used to be large upfront revenue streams). That being said, there is still likely some conservatism in this outlook.

{kind=link}

Pro forma operating income guidance, which implies a 4.5% margin at the midpoint, is likely substantially undercalled (the company generated a mid-20s margin in Q4). This is also less likely to be impacted by tougher y/y comps.

Even taking this projection at face value, Alteryx trades at a valuation of just 5.0x EV/FY23 revenue.

The bottom line here: for a company with so much room to scale profitably owing to its huge margins, and with positive tailwinds from its transition to a subscription-based business model with huge ARR growth rates, Alteryx is poised for a further recovery.

Q4 download

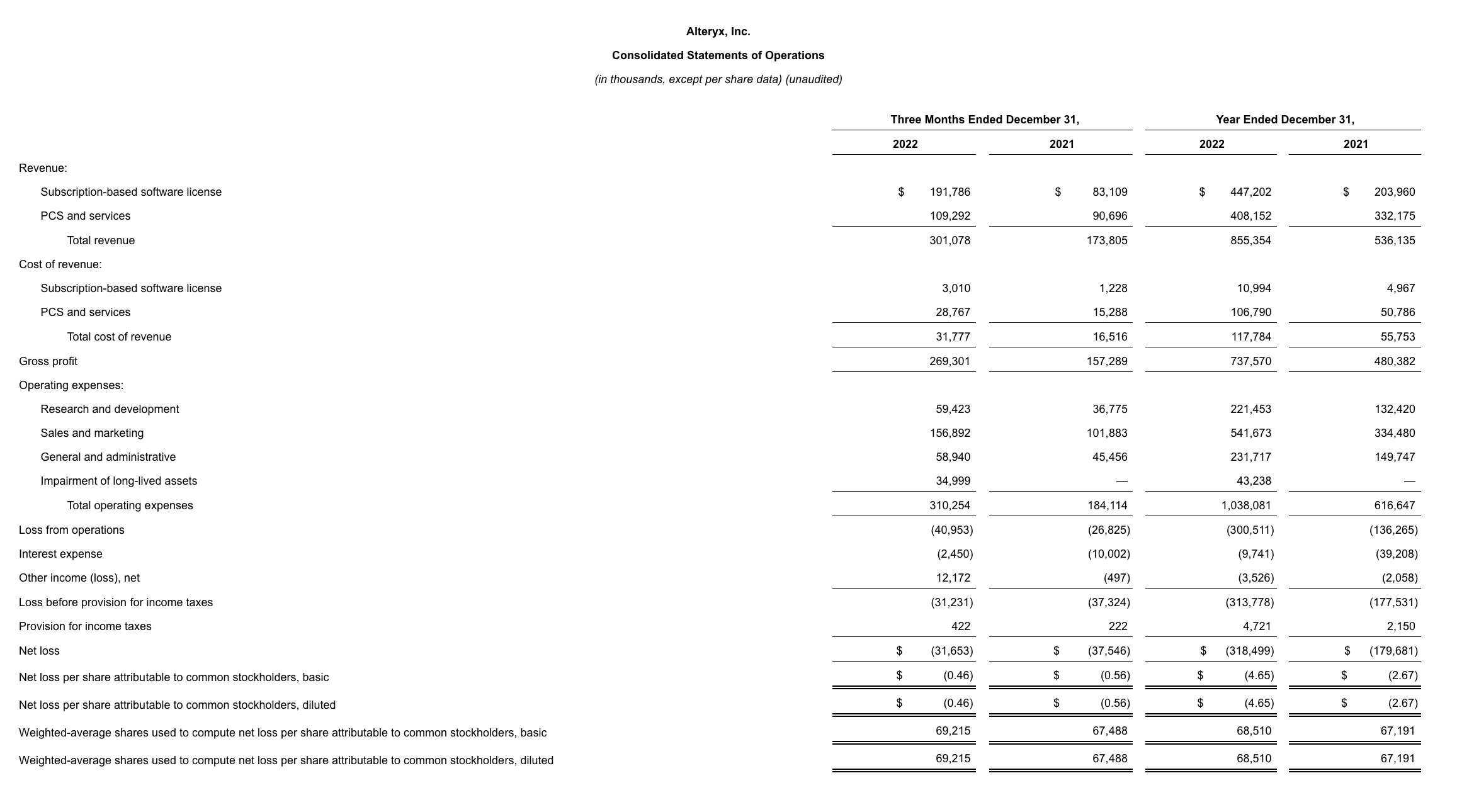

Let's now go through Alteryx's latest Q4 results in greater detail. The Q4 earnings summary is shown below:

{kind=link}

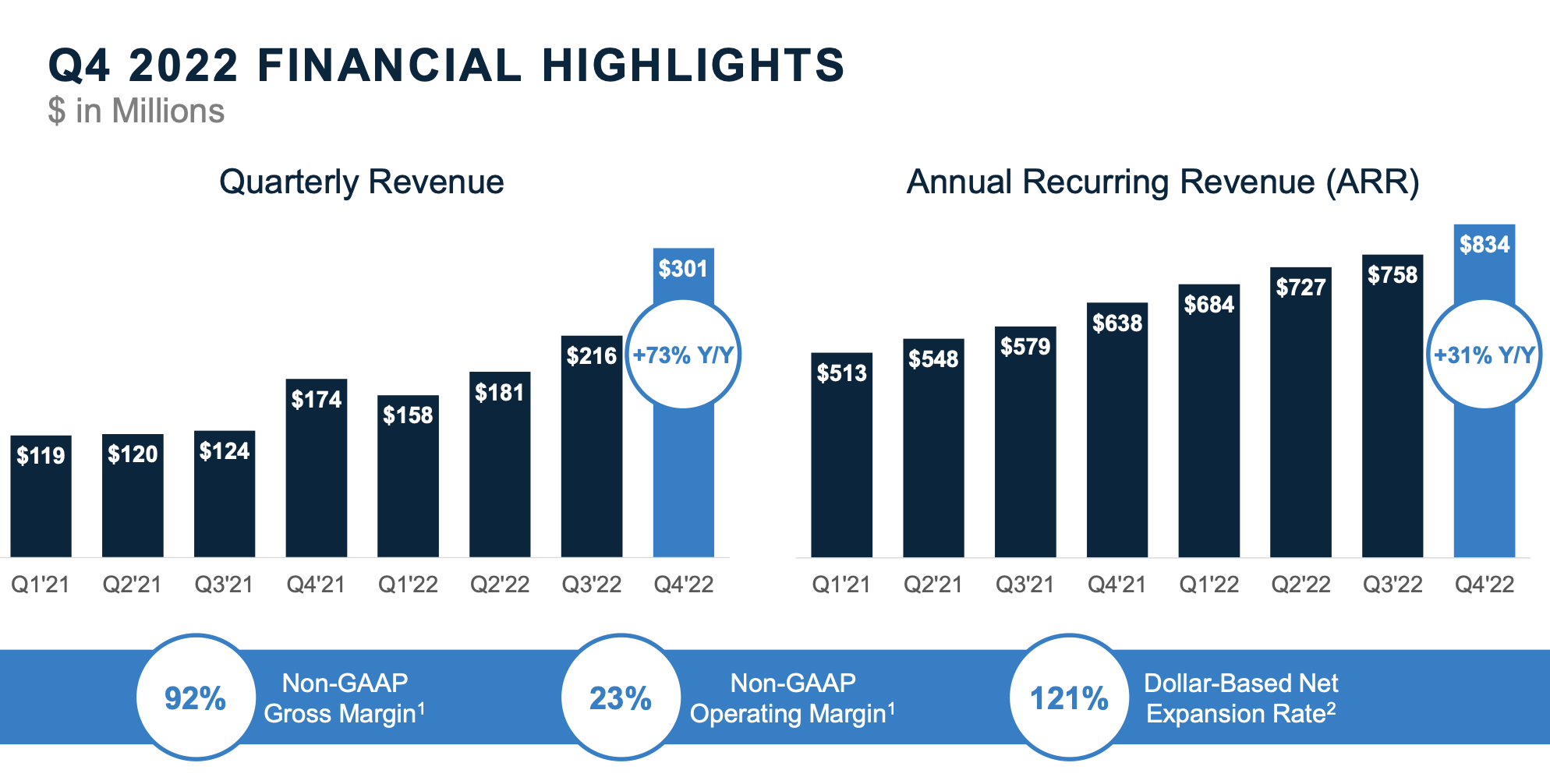

Alteryx's revenue grew at a blazing 73% y/y pace to $301.1 million in revenue, beating Wall Street's expectations of $279.3 million (+63% y/y) by a huge ten-point margin. Revenue growth also largely kept pace with last quarter's 75% y/y growth, though we note that this will likely be the last quarter of "hyper growth" - as can be seen in the chart below, last-year revenue started to climb in a meaningful way in Q2 after the dust settled on Alteryx's SaaS transition. Alteryx also typically has a seasonal Q4 to Q1 drop-off; Q1 guidance this year calls for $198-$202 million in revenue, translating to 25-26% y/y growth (again, I think there is conservatism here).

{kind=link}

And as seen as well in the chart above, Alteryx achieved significant ARR expansion this quarter, up $76 million on a sequential basis and growing 31% y/y. Alteryx expects year-end ARR to clock in at $1.015-$1.025 billion, higher than its revenue forecast for the year.

Management noted that in spite of macro headwinds that caused elongation of sales cycles, Alteryx managed to offset that by leveraging higher sales tenure and boosted sales productivity. Per CFO Kevin Rubin's remarks on the Q4 earnings call :

We benefited from early productivity improvements in the sales force in 2022 versus 2021 in terms of new ACV per sales rep. As we enter 2023 with a higher mix of ramped reps, more comprehensive sales enablement capabilities and an expanded product portfolio, we expect these tailwinds to persist and help us navigate this dynamic macro environment. And we improved Q4 non-GAAP G&A expense as a percentage of revenue by 3 points year-over-year, driven primarily by efficiencies of scale [...]

Expansion is a key growth driver for our business with the vast majority of our new ACV in any given quarter continuing to come from existing customers, and now as the opportunities become bigger, we are seeing consistent growth in the average expansion deal size. To help us streamline this enterprise adoption, we introduced ELA bundles in mid-2021. ELAs come in tiered bundles that vary in size and burst capacity. This allows for progressive upselling and we are already seeing success with the 2021 ELA cohort."

Management also noted on the expansion/renewal front that 2023 benefits from a very large renewal base, helping to illustrate the notion that FY23 guidance may be on the light side:

That said, we have several incremental growth drivers to layer on in the coming year that we expect will contribute to our growth and profitability momentum. First, we have a meaningfully larger renewal base relative to 2022, which supports revenue growth and creates upsell opportunities.

Second, we have a growing book of ELAs where burst explorations create additional upsell opportunities with a high level of visibility. Third, we expect to sell significantly more ELAs in 2023 driven by growing traction with large enterprise customers."

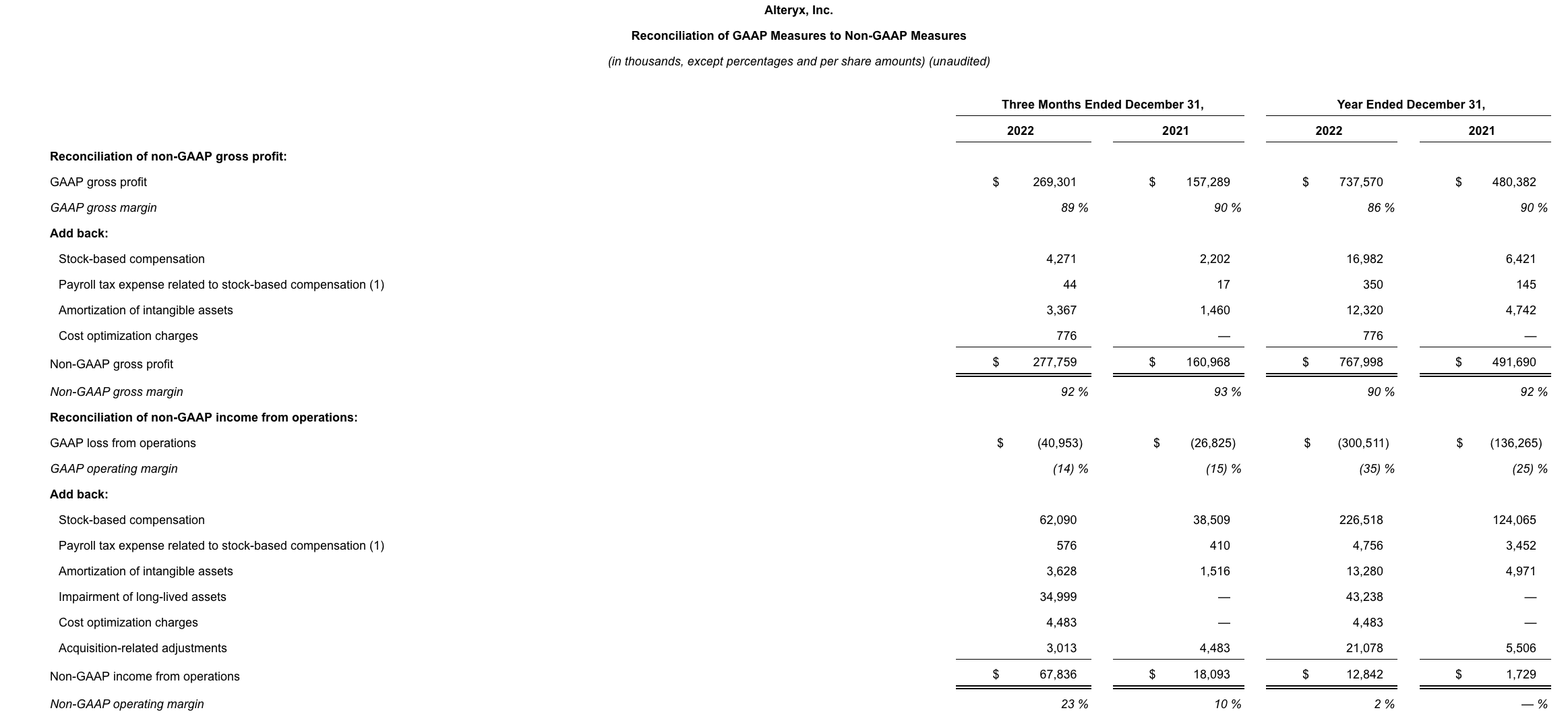

Alteryx also excelled on bottom-line performance. Q4, which tends to be Alteryx's most profitable quarter, saw pro forma operating margins jump to 23%, up from 10% in the prior-year quarter: driven economies of scale on opex, which is easily achieved on Alteryx's 90%+ gross margins.

{kind=link}

Key takeaways

With the benefit of rich margins, a continued buildup in ARR, and a large rental base that will feed growth in 2023, I see no reason for Alteryx's recovery rally to give up steam. Stay long here.

For further details see:

Alteryx: After Massive Q4, This Stock Is Ready To Rally