AYX - Alteryx: Buy The Crash

2023-04-30 04:09:10 ET

Summary

- Shares of Alteryx plunged more than 15% after the company reported Q1 results.

- Management is indicating that growth will decelerate to roughly flat in Q2, a sign of the tough macroeconomic environment.

- To prepare for the slowdown, Alteryx is cutting 11% of its workforce, primarily in sales and marketing.

- Given the company still expects high-teens full year growth, as well as Alteryx's huge TAM, it's a great time to buy into Alteryx while it's weak.

Market volatility seems to have no end. Stocks continue to react dramatically to every piece of incremental news, most recently First Republic Bank's ( FRC ) fallout as well as reports of persistent inflation. Yet amid the chaos, investors who can keep their heads down and focus on stock-picking excellent names at cheap prices will win once we get to the other side of this recession.

Surprisingly, the tech sector has become a haven for value investors as many small and mid-cap names have cratered due to investors' lowered appetite for risk taking. Alteryx ( AYX ), a big data analytics platform that helps companies stitch together data from different sources, recently sank more than 15% after indicating that growth would decelerate owing to macroeconomic hardships, taking away all of its year-to-date gains.

In my view, the market is being quite short-sighted on Alteryx. Of course the company will see a huge slowdown in the current environment - it's an expensive software product that addresses long-term transformation needs, and can clearly be cut when corporate IT budgets are pinched. But longer-term, the company is still addressing a massive $113 billion TAM. In simpler terms: Alteryx may see a few quarters of retrenchment, but it will be more than fine in the long run.

For investors who are newer to this name, here is my full bull case on Alteryx:

- Digital transformation is already underway - Companies want to use data to drive decisions. Unfortunately, data is sometimes locked in different formats and takes hours of manual work to untangle. Alteryx's technology helps with that process and automates one of the most labor-intensive pieces of adopting a "big data" strategy in the C-suite. Investing in technology like Alteryx may not have been a top priority during the pandemic, but it will become a much hotter-button topic as we look ahead.

- $113 billion 2025 TAM - Alteryx's current ~$1 billion annual revenue run rate is only a fraction of its estimated current $65 billion TAM, leaving plenty of room for growth. Alteryx additionally expects its TAM to expand to $113 billion by 2025.

- Truly horizontal software serving a wide variety of use cases across many industries - Alteryx's software is broadly applicable to clients in virtually any industry. An illustrative cross-section of Alteryx's customer base: Netflix ( NFLX ), Walgreens ( WBA ), Abbott Laboratories ( ABT ), Chevron ( CVX ), Wells Fargo ( WFC ), Visa ( V ), Marriott Hotels ( MAR ), and Facebook ( META ) are all among Alteryx's anchor clients, spanning every industry.

- Best-in-class gross margins of ~90% are among the highest in the software industry - Virtually every dollar of revenue for Alteryx flows through to the bottom line, justifying the efforts that Alteryx makes on the initial sale.

- Plans for significant profitability - Already, Alteryx has hit significant pro forma operating profits. Over the long run, it plans to generate pro forma operating margins in the 25-30% range, primarily by achieving economies of scale on sales and marketing. When a company like Alteryx has huge recurring revenue, over time the cost of sales support for that revenue base will eventually dwindle.

Stay long here and buy the dip.

Q1 results and the guidance fiasco

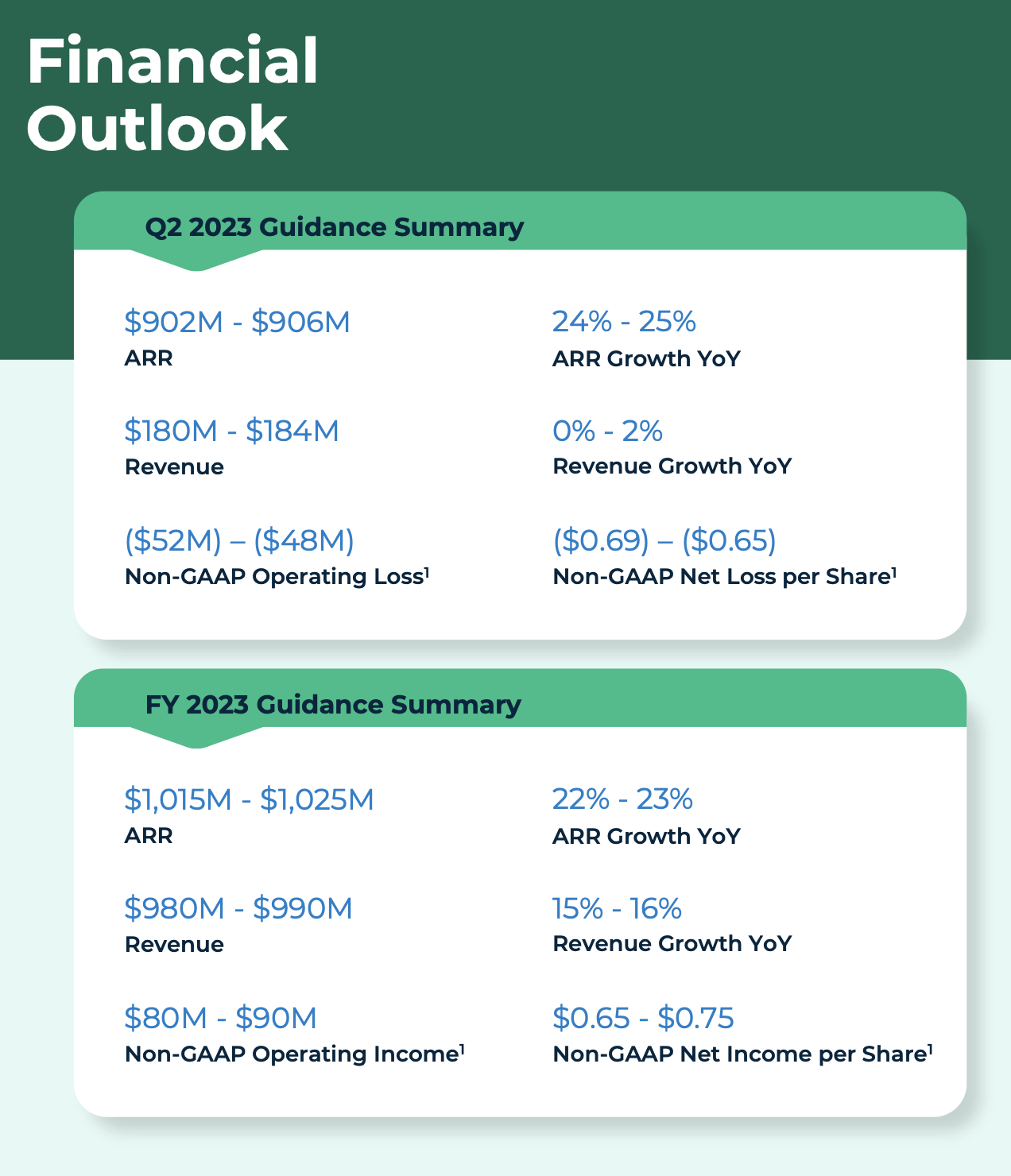

Let's start with the elephant in the room: what exactly spooked investors out so much about Alteryx's most recent earnings print? It wasn't the Q1 results themselves, but Alteryx's outlook for Q2, which called for a sharp deceleration to 0-2% y/y growth:

{kind=link}

This being said, Alteryx is still expecting 15-16% y/y growth in the full year: implying a relatively short trough and re-acceleration in the back half of the year.

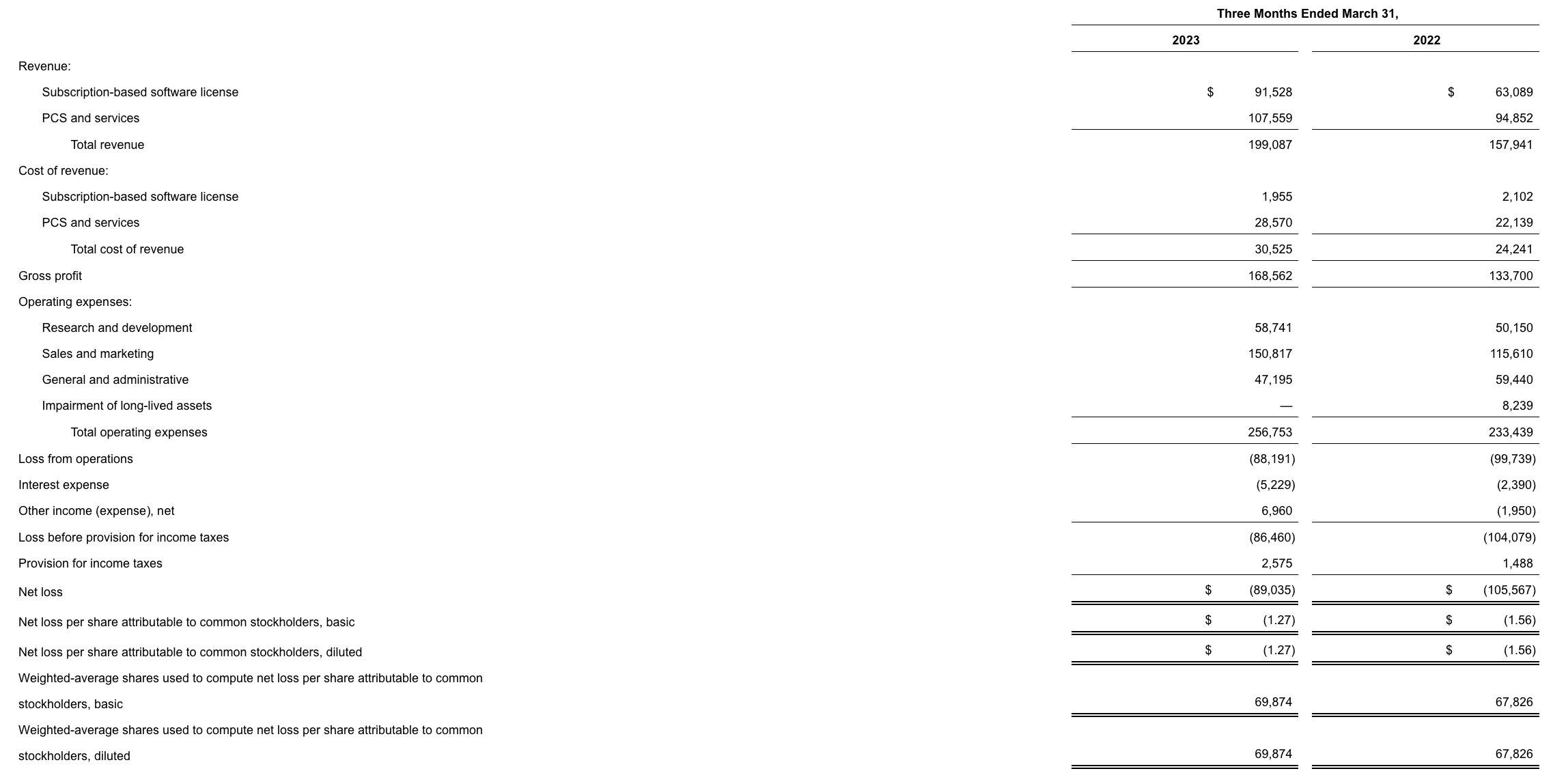

Q1 results weren't terrible, either. Take a look at the earnings summary below:

{kind=link}

Alteryx's revenue grew 26% y/y to $199.1 million in the quarter, far above the flat growth that it's expecting in Q2 (though this did decelerate sharply from 73% y/ growth in Q1, as Alteryx starts to lap the easier comps it had in the prior year as it was transitioning to a subscription business model).

The company noted that buying behavior changed late in the quarter as more scrutiny was applied on deals - similar commentary that has resonated throughout the enterprise software sector. Per CEO Mark Anderson's remarks on the Q1 earnings call:

Our financial results demonstrate the value that our innovation delivers to customers everywhere, even when facing some continued tightening of the broader IT spend environment.

More specifically, we saw changes in customer buying behavior late in the quarter. Customers are applying more scrutiny on deals, which has continued to lengthen our overall sales cycles. This in turn led to some deals that we would have expected to close in a more stable economic backdrop slipping out of the quarter. Despite continued macroeconomic uncertainty we have not seen any material shift in the competitive dynamics something we track closely."

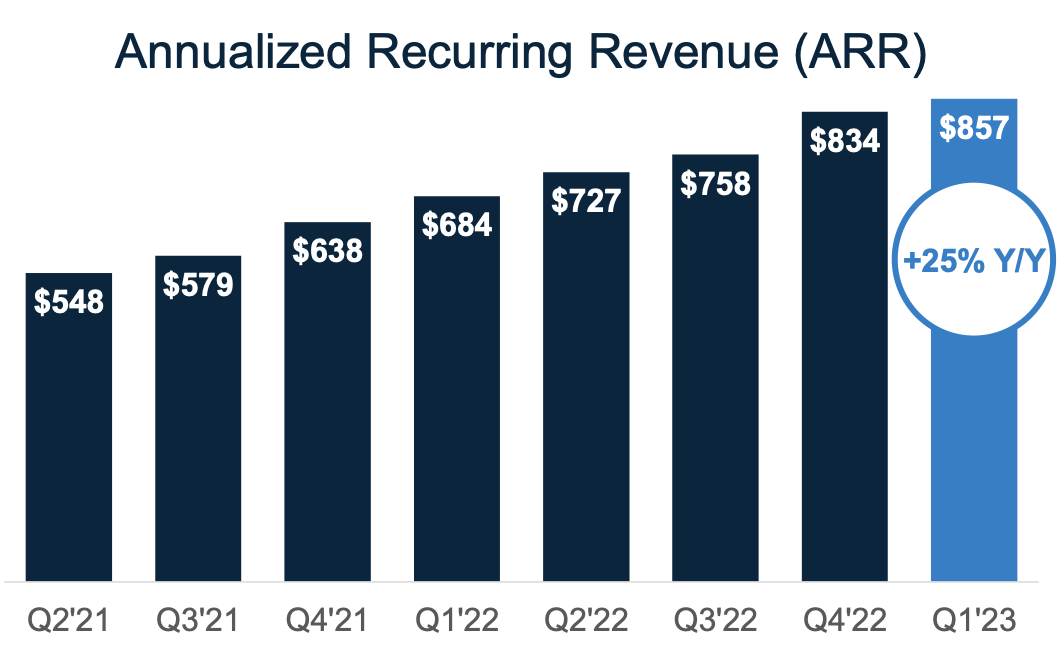

Where I take comfort, however, is Alteryx's large ARR base, which still grew 25% y/y to $857 million in Q1.

{kind=link}

Alteryx's ARR has expanded significantly as it shifted to a subscription model during the COVID years, and it's this base of sticky recurring revenue that will prevent the company from having overly lumpy revenue trends amid macro hardships.

Note as well that Alteryx is cutting roughly 11% of its global workforce, primarily in sales and marketing. Cuts to sales forces often indicate a slowdown is incoming (as sales hiring is the first and most important lever that tech companies have to grow) - but in my view, this expense discipline will give Alteryx the opportunity to boost its operating leverage once it exits the downturn. It's important to note that Alteryx is still expecting strong 9% pro forma operating margins on the year.

Valuation and key takeaways

At current share prices near $41, Alteryx trades at a market cap of $2.86 billion. After we net off the $885 million of cash and $1.32 billion of convertible debt on Alteryx's most recent balance sheet, the company's resulting enterprise value is $3.20 billion.

This puts Alteryx's valuation at just 3.2x EV/FY23 revenue against the $980-$990 million midpoint of the company's guidance range for the year. To me, that valuation provides quite a reasonable safety net for investing in Alteryx while it's re-evaluating its sales model and preparing for a temporary downturn.

For further details see:

Alteryx: Buy The Crash