AYX - Alteryx: I'm Not Buying Due To High Uncertainty

2023-06-14 10:45:02 ET

Summary

- Alteryx has a solid revenue growth profile, but the company still did not achieve sustainably positive free cash flow.

- The stock looks attractively valued, but the level of uncertainty regarding underlying assumptions is very high.

- I add the stock to my short-list, but before I invest, I want to examine how the next few quarters will develop.

Investment thesis

Alteryx's (AYX) stock price is now about four times lower than the all-time high of 2020. Indeed, my valuation analysis, where I discount future cash flows suggests that the stock is significantly undervalued. At the same time, there is no stable trend in the company's profitability metrics. I believe this is the main factor that made many investors sell this stock. I want to examine how the next few quarters will unfold before investing. Therefore, the stock is a "Hold" at the moment.

Company information

Alteryx is a software company specializing in analytics automation. The company's flagship platform is called Alteryx Analytics Automation. According to the latest 10-K report , the platform democratizes access to data-driven insights by making sophisticated analytics capabilities available to all users, ranging from IT administrators and business analysts to data engineers and trained data scientists

The company's fiscal year ends on December 31. The business operates as a single reportable segment. In FY 2022, about 70% of Alteryx's revenue was generated in the U.S.

{kind=link}

Financials

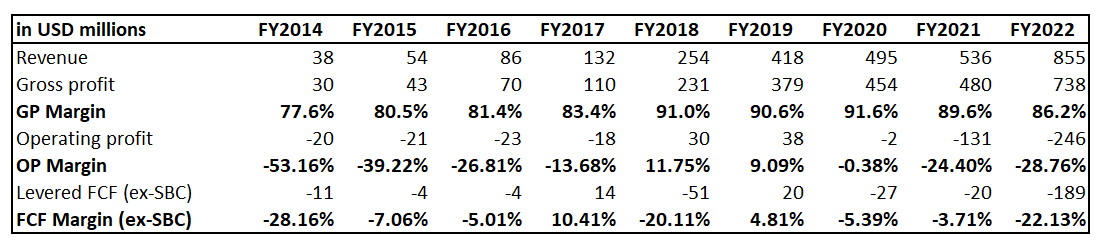

Over the past nine years, AYX demonstrated a staggering 47% revenue CAGR. Though, comps are very low, with revenues below $100 million until FY 2016. I like the company's gross margin, which danced around 90% over the past five years. AYXs figures are not yet sustainably positive from the operating profit and free cash flow [FCF] perspective.

{kind=link}

SG&A represents a substantial part of the company's sales. I am usually bearish when the company needs to demonstrate a declining SG&A to revenue ratio as the business scales up. It means that revenue growth heavily depends on marketing and might look like growth just for the sake of growth. Therefore, there needs to be more certainty about how will the revenue dynamic unfold if the company decides to cut SG&A. On the other hand, I like that the company is committed to innovation which I can see from the stable above 20% R&D to revenue ratio. For me, this is an indicator that the management has a long-term view on delivering shareholders value.

Now let's narrow the financial analysis down to the quarterly performance to understand the strength of the growth momentum. The good sign is that the topline outpaced expenses growth in the latest reported quarter, meaning margins improved YoY. Revenue growth YoY demonstrated a solid +26%, though this is a significant deceleration compared to FY 2022 quarterly dynamics. If we look sequentially, margins slipped, but this is due to the seasonality, where the December quarter is usually much stronger than the one ending in March. It is also a good sign that the company generated a positive about 9% FCF margin in Q1, even if we deduct stock-based compensation [SBC]. It is a significant YoY improvement since last year, and the FCF margin ex-SBC was just slightly above zero.

{kind=link}

Positive free cash flow is a bullish sign. But we need to see it over multiple quarters to be sure the company switched from the cash burn mode to cash generating. Therefore, let's assess the health of the company's financial position. The company is in a net debt position, and the leverage ratio is elevated. On the other hand, short-term liquidity is in good shape with an above two-quick ratio. I would have called the balance sheet a red flag if the company still burned quarterly cash. I want to look through the upcoming quarters to understand whether the company achieved sustainably positive FCF.

Valuation

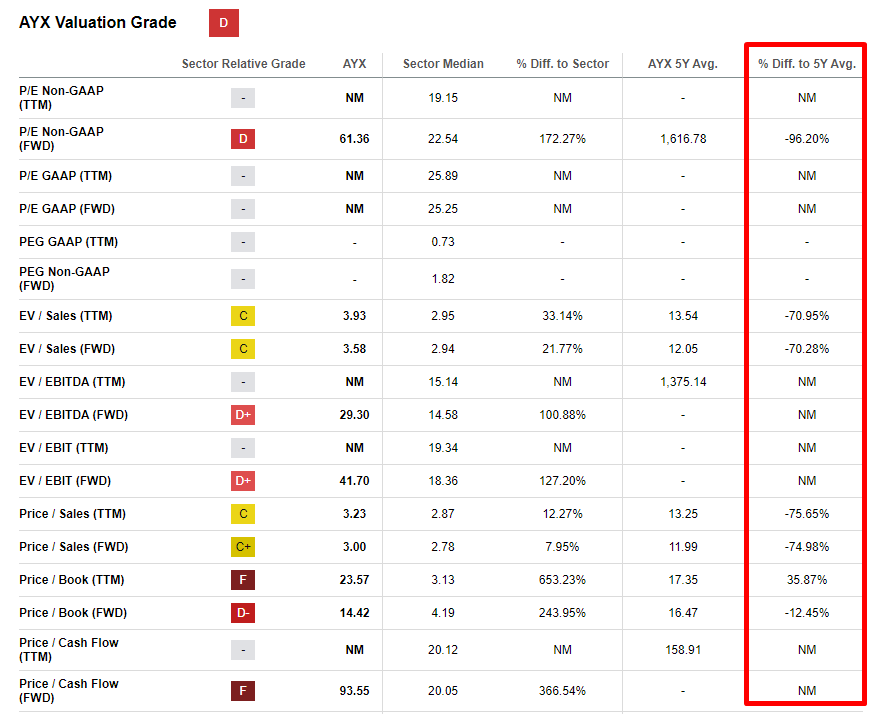

AYX stock price declined about 12% year-to-date, significantly underperforming the broad market. Seeking Alpha Quant suggests that AYX's stock valuation with a "D" grade is unattractive. Based on the multiples, I agree that some are too high. For example, a forward price-to-sales ratio is almost 12. On the other hand, the company's multiples are much lower than 5-year averages across the board.

{kind=link}

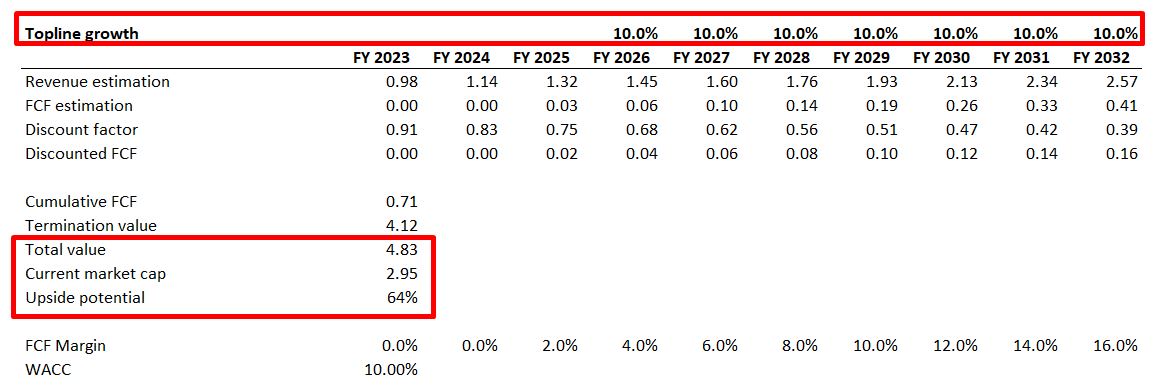

Since AYX is a growth company, I will use discounted cash flow [DCF] analysis for valuation. Valueinvesting.io suggests that the company's WACC is about 10%. I use it as a discount rate for the DCF. We have consensus revenue estimates up to FY 2025, so I would like to simulate a few scenarios with different revenue growth estimations. I expect the FCF margin to be zero in FY 2023-2024 and then expand by two percentage points. I implement a 10% revenue CAGR for the first base case scenario for the years beyond FY 2025. Under a 10% revenue growth assumption, you can see that the upside potential is massive.

{kind=link}

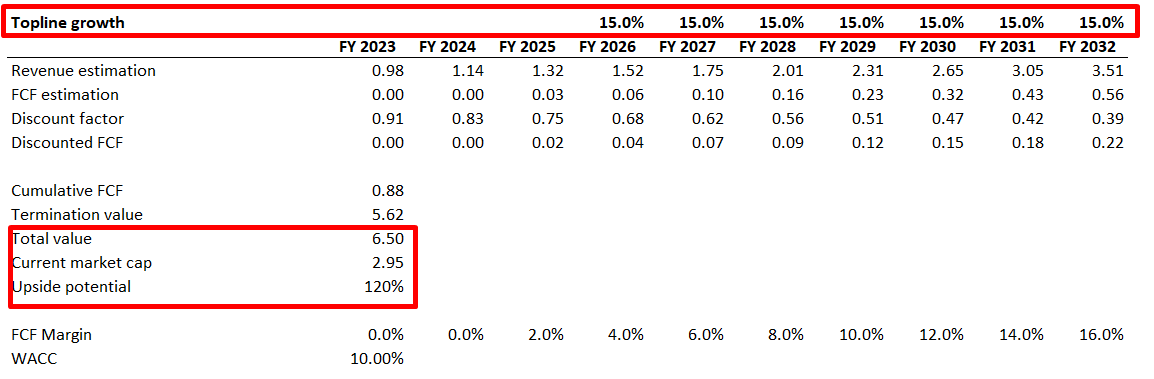

Now let me simulate the optimistic scenario with a 15% revenue CAGR for the years beyond FY 2025. Other input data is unchanged. Under this aggressive revenue growth assumption, we can see that the business's fair value is about $6.5 billion, which is more than two times higher than the current market capitalization.

{kind=link}

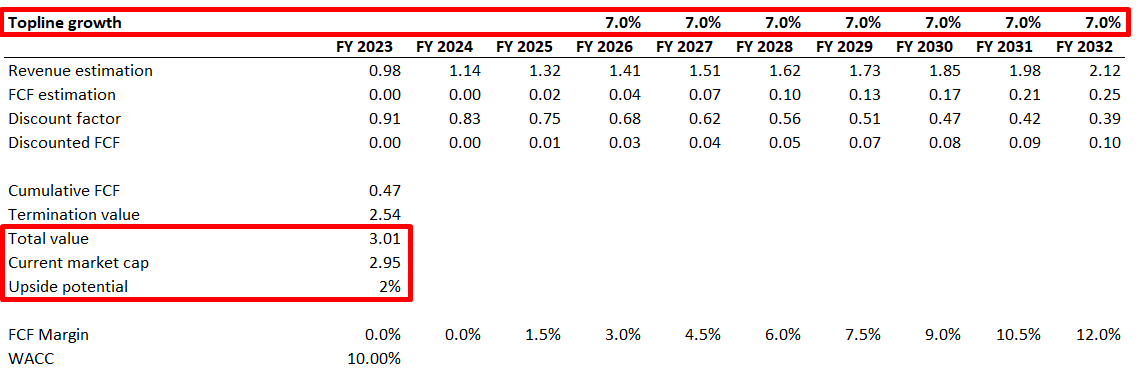

Finally, let me now simulate a pessimistic scenario. I implement a 7% revenue CAGR and FCF margin expanding by 150 basis points yearly. With these pessimistic assumptions, the fair business value is about $3 billion. It is very close to the current market cap, meaning the stock is fairly valued under tight assumptions.

{kind=link}

Risks to consider

As a growth company, Alteryx stock's intrinsic value faces the risk that the company will not be able to deliver expected revenue growth and margin expansion. As we saw in the "Valuation" section, most of the company's fair value comprises termination value for the cash flows from years beyond FY 2032. Therefore, the level of uncertainty regarding the underlying assumptions for the DCF model is very high.

Alteryx is an innovative company that faces the risk of a rapidly evolving technological landscape. There is fierce competition in the technology sector, both direct and indirect. For example, technological giants might not be direct competitors of AYX at the moment. On the other hand, these companies possess vast resources and recruit the best engineers. Therefore, the probability that a giant like Microsoft ( MSFT ) or Google ( GOOG ) at one point will decide to enter AYX's market is not equal to zero. Therefore, the company should innovate and diversify its offerings to sustain long-term growth.

Bottom line

Alteryx stock looks very attractive from a valuation perspective. On the other hand, the level of uncertainty regarding the underlying assumptions is very high. A company with unstable FCFs, like AYX, should have a stronger balance sheet. The stock is a "Hold" since I want to wait on the sidelines and look at how will next few quarters unfold before I invest. I will look at the revenue growth momentum and the FCF dynamics.

For further details see:

Alteryx: I'm Not Buying Due To High Uncertainty