AYX - Alteryx: Sales-Driven Growth Rebound

Summary

- Strong growth in recent quarters has been driven by large investments in sales and marketing.

- Alteryx needs to demonstrate that they can maintain growth while moderating investments.

- The stock is relatively inexpensive, but it is not clear what the catalyst for a rerating would be.

Alteryx (AYX) provides low-code / no-code analytics software that is targeted at knowledge workers. In recent years the company has switched focused to penetrating larger organizations and building out a platform which covers the entire data science lifecycle. The sales initiative has reinvigorated growth, but has come at a significant cost to margins. Alteryx now need to demonstrate they can generate efficient growth, and prove the viability of their cloud transformation.

Analytics software is not immune to the same macro headwinds that other segments are facing, but companies continue to implement digital transformation projects to improve decision making and automation. Over 70% of organizations plan on spending more on analytics relative to other software investments in the next 12-18 months. It is also estimated that enterprises have deployed solutions in less than half of the departments that actually need them and less than half of knowledge workers are actively using analytics software.

There is a secular opportunity in analytics software, but it is unclear who will be able to capitalize on this, and the near term could be volatile if declining profits force organizations to delay investments. Analytics encompasses a large number of use cases, and as a result the vendor landscape is extremely fragmented. There are a number of companies attempting to develop end-to-end platforms, but there is no one solution that is dominating the market.

Alteryx are trying to develop their own universal analytics solution, and hope to be the automation and orchestration layer within the analytics stack of their customers. In support of this, there have been a number of acquisitions and significant internal development over the past few years. These efforts are yet to really impact the business though, as integrations and product releases are still ongoing.

Alteryx acquired Trifacta early in 2022, to form the foundation of their cloud infrastructure, and the integration is reportedly going well. Alteryx also acquired Hyper Anna, which is now Alteryx Auto Insights. The integration of this with Alteryx and the Trifacta is also going smoothly.

Alteryx auto machine learning is another development, which allows Alteryx general knowledge workers to leverage machine learning models. Alteryx Machine Learning has also now been integrated into the Alteryx Analytics Cloud platform. While these products could provide upside going forward, the vast majority of Alteryx's revenue still comes from their on-premise products (designer and server).

Even when Alteryx's cloud solution begins to mature, it is still expected to be incremental to their existing products and customers. This may be disappointing to some investors, but Alteryx have always maintained that their product strategy is dictated by their customers and where their data is.

Newer offerings include:

- Metrics Store - allows customers to create, share and manage metrics

- App Builder - enables customers to build applications on a cloud-native platform and connect them to Alteryx workflows

- Location Intelligence

Early feedback has been positive and Alteryx expect these solutions to be available in 2023.

Sales Driven Rebound

Alteryx's recent turnaround appears to be almost solely driven by a shift in sales strategy. In the past, Alteryx focused on selling to users, like business analysts. Over the past 18 months they have transitioned to more of a top-down sales motion, where they are targeting executives and selling the software based on ROI and the ability to drive business transformation. As a result, Alteryx is now also more focused on larger organizations, where they can drive significant expansion after developing a close relationship with the customer.

Alteryx are also ramping up their partner business, both with organizations like PwC and KPMG and technology partners like Snowflake ( SNOW ), Databricks, Google ( GOOG ) BigQuery and AWS ( AMZN ). This should help to drive adoption and expansion within larger organizations and improve the productivity of Alteryx's sales organization.

Evolving Data Infrastructure

Alteryx's poor share price performance over the past few years was driven by a combination of weak financial performance and concern over the company's competitive positioning, as the preferred data infrastructure architecture has continued to evolve.

Data science platforms are facing changes related to how data is stored and accessed and how analytics can be scaled to massive data sets in an efficient manner. Extract, Transform and Load (ETL) refers to the process of copying data into a destination system which represents the data differently from the source and has been around since the 1970s. ETL almost exclusively uses relational databases and is best for structured data and small to medium amounts of data. Extract, Load and Transform ((ELT)) is a process where raw data is loaded into the data warehouse and transformations occur on the stored data. ELT is useful for processing large data sets and is better suited to unstructured data. The choice between ETL and ELT largely comes down to the type and volume of data being handled and the type of analysis being performed. ETL is more likely to be used in business intelligence type applications whereas ELT is more likely to be used in more advanced machine learning applications. Alteryx is often used as part of ETL workflows and as ELT becomes more common, it may weaken Alteryx's value proposition.

Software is also increasingly moving from on-premise deployments to cloud hosted SaaS, which can be advantageous in terms of cost, accessibility, scalability and performance. Although for some customers it may simply come down to a choice based on where the data currently resides. These changes are part of the reason that Alteryx has developed a cloud hosted solution and built an end-to-end analytics platform. A cloud hosted solution allows Alteryx to maintain relevance as data migrates to the cloud and the more use cases Alteryx can address, the less dependent it is on the ETL paradigm.

Despite this, there are still reasons to question the strength of Alteryx's competitive position in the long run. Snowflake has so far been focused on adding functionality to its platform which can attract new workloads. In the future Snowflake may choose to offer their analytics tools, rather than relying on third-party vendors. Snowflake is introducing Snowpark and Snowpark optimized warehouses, which allow users to deploy code directly in Snowflake and increases compute efficiency for machine learning workloads. It would be a small step from there to offering analytics solutions on top of the database directly.

Confluent ( CFLT ) has also introduced Stream Designer, a simple UI for building pipelines using Confluent's data streaming platform. Stream Designer is a drag-and-drop tool that allows less technical users to rapidly build and deploy streaming pipelines. Stream Designer is free, rather than generating revenue directly it aims to accelerate usage of ksql and Kafka, and so far adoption has been strong. Stream Designer may be more targeted at different users and use cases, but at the margin it may impact the use of tools like Alteryx for building data pipelines.

The Microsoft Threat

Alteryx could also become a victim of Microsoft's ( MSFT ) massive distribution at some point in time. Microsoft is able crush superior products by bundling software and rolling it out to their massive user base, as seen with Slack and Teams. This is a problem that UiPath ( PATH ) are also facing. Alteryx's focus on knowledge workers and analytics places it an area where Microsoft likely has the ability and inclination to successfully launch a competing product. Whether this threat eventuates remains to be seen, but analytics software could easily become a feature of a business productivity suite rather than a standalone product in the future.

Financial Analysis

Alteryx has demonstrated extremely strong revenue growth in 2022, but this has not really been reflected in the share price, indicating that investors are still not buying into the Alteryx story. Similar to other software companies, Alteryx is seeing an elongation of sales cycles, as deals have been receiving more scrutiny. Their salesforce is focused on demonstrating value upfront to keep deals progressing in this environment.

Approximately 20% of Alteryx's ARR is denominated in foreign currency, meaning the strong USD has presented a significant direct drag on the business in recent quarters. This headwind is likely to ease going forward.

In the fourth quarter of 2022 Alteryx expect ARR growth to be 29% YoY and revenue growth to be 59-62% YoY. It should be kept in mind that Alteryx has benefited from an increase in the amount of revenue being recognized upfront in 2022 versus 2021 (50% compared to 40%). This, along with acquisitions, has boosted growth somewhat, meaning that growth is likely to normalize in 2023.

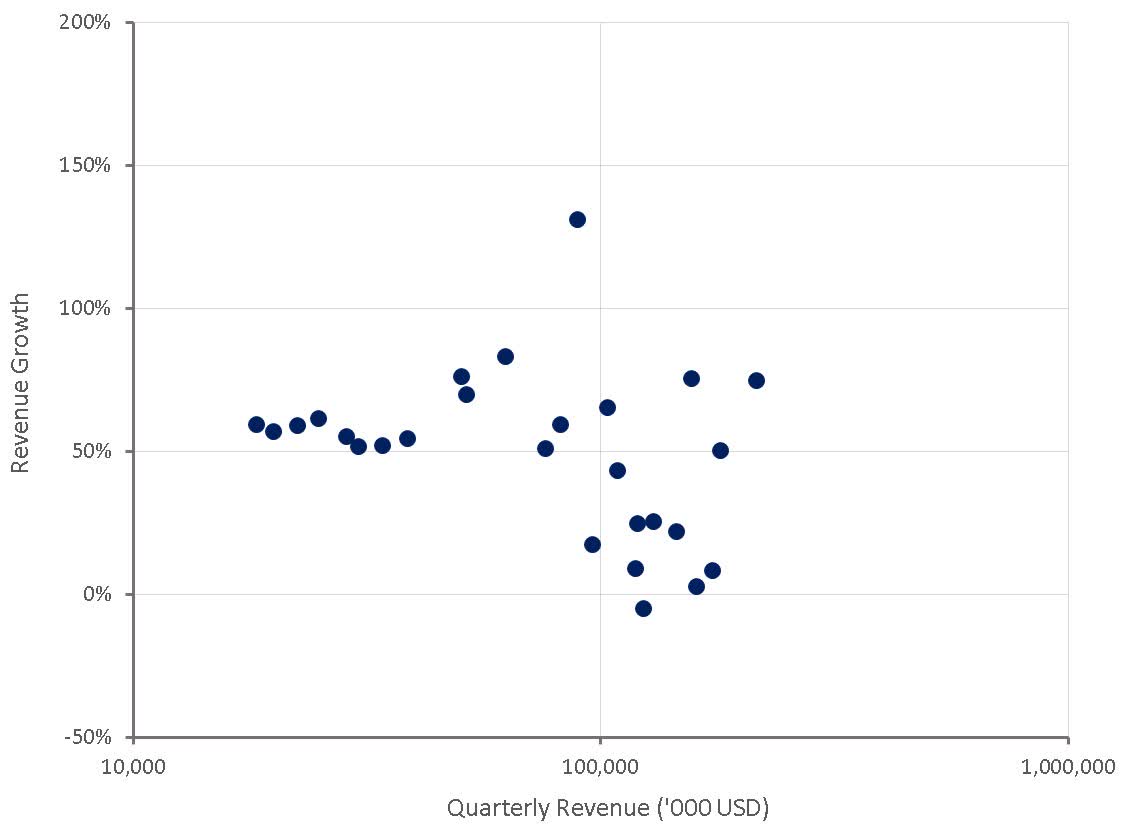

Figure 1: Alteryx Revenue Growth (source: Created by author using data from Alteryx)

{kind=link}

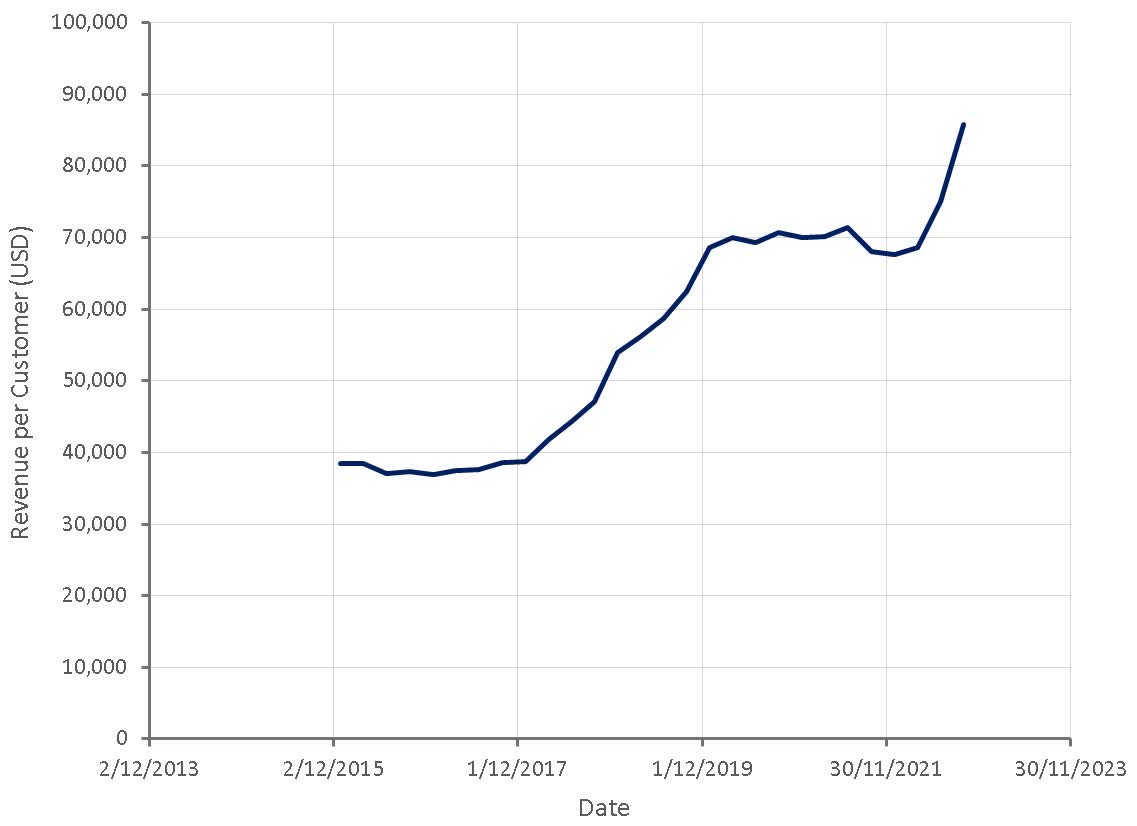

Alteryx's focus on large customers has led to a rapid increase in revenue per customer and improving expansion rates. Alteryx's renewal rates are holding near multi-year highs, and their net expansion rate was 121% in the third quarter . Alteryx are seeing the strongest ARR growth within their 1 million-plus USD ARR customer cohort, and for Alteryx's large customer cohort, the net expansion rate is 129%. Average deal size increased over 30% YoY with both new logo and expansion wins.

Some of this strength may be due to Alteryx's Enterprise Licensing Agreements. These ELAs give customers the ability to burst upwards of 50% more licenses and of the early adopters, over 40% of are already in their burst capacity.

Figure 2: Alteryx Revenue per Customer (source: Created by author using data from Alteryx)

{kind=link}

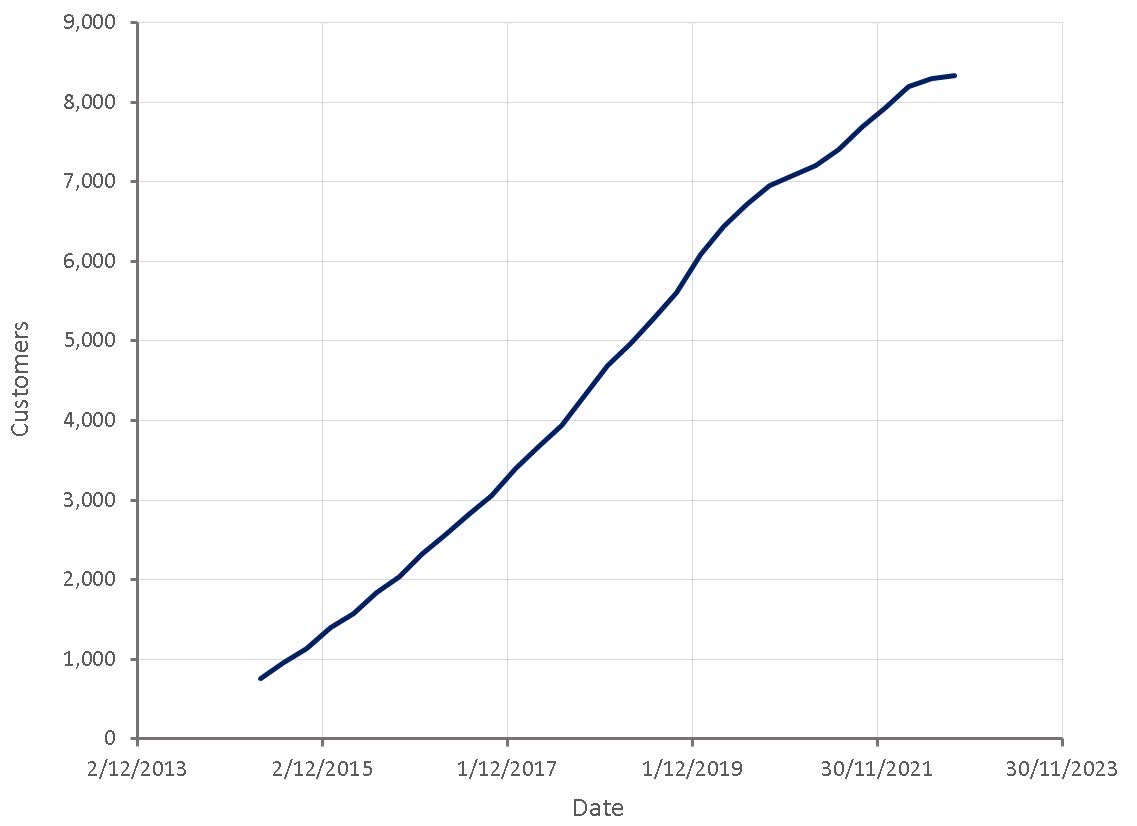

Customer additions have slowed significantly in recent quarter, although this is somewhat offset by large customer growth. Alteryx increased their penetration of the Global 2,000 to 46% in the third quarter , up 7% YoY. The slowdown in customer growth is one of main signs of weakness in Alteryx's business at the moment.

Figure 3: Alteryx Customers (source: Created by author using data from Alteryx)

{kind=link}

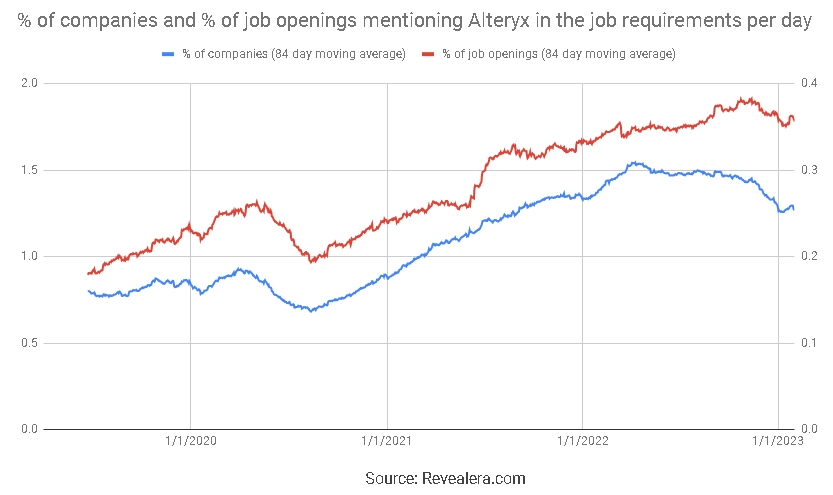

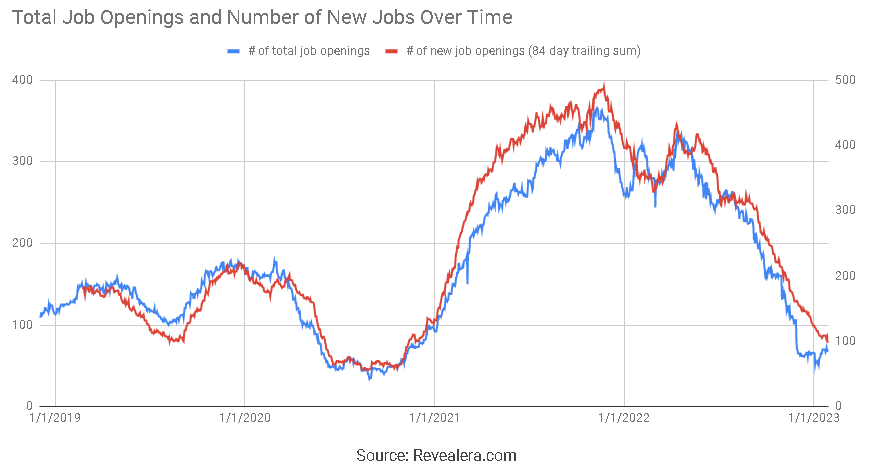

The number of job openings mentioning Alteryx in the job requirements has begun to fall in the past few months, after steadily increasing since the early days of the pandemic. Growth in the number of openings is outpacing growth in the number of hiring organizations, another indication of Alteryx's increased focus on penetrating larger organizations.

Figure 4: Job Openings Mentioning Alteryx in the Job Requirements (source: Revealera.com)

{kind=link}

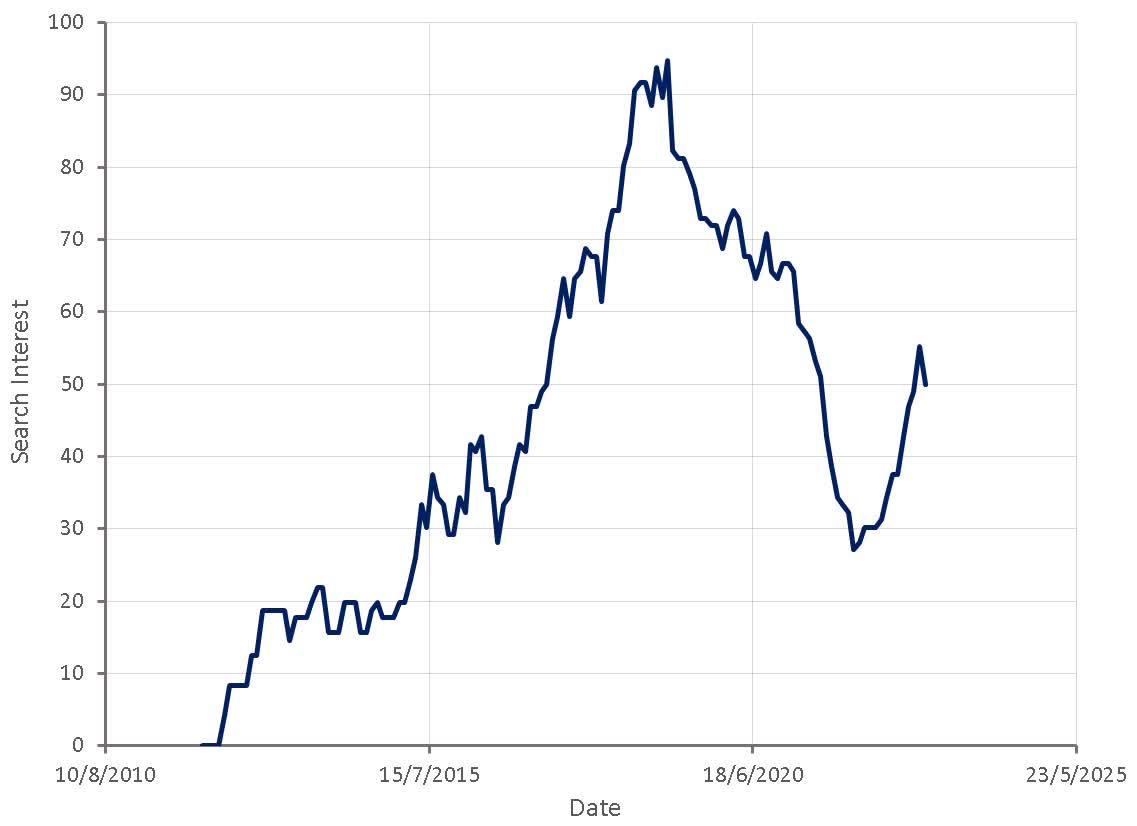

Search interest for Alteryx pricing remains relatively weak, although it is not clear if this means there is no longer broad based interest in Alteryx's platform.

Figure 5: "Alteryx Pricing" Search Interest (source: Created by author using data from Google Trends)

{kind=link}

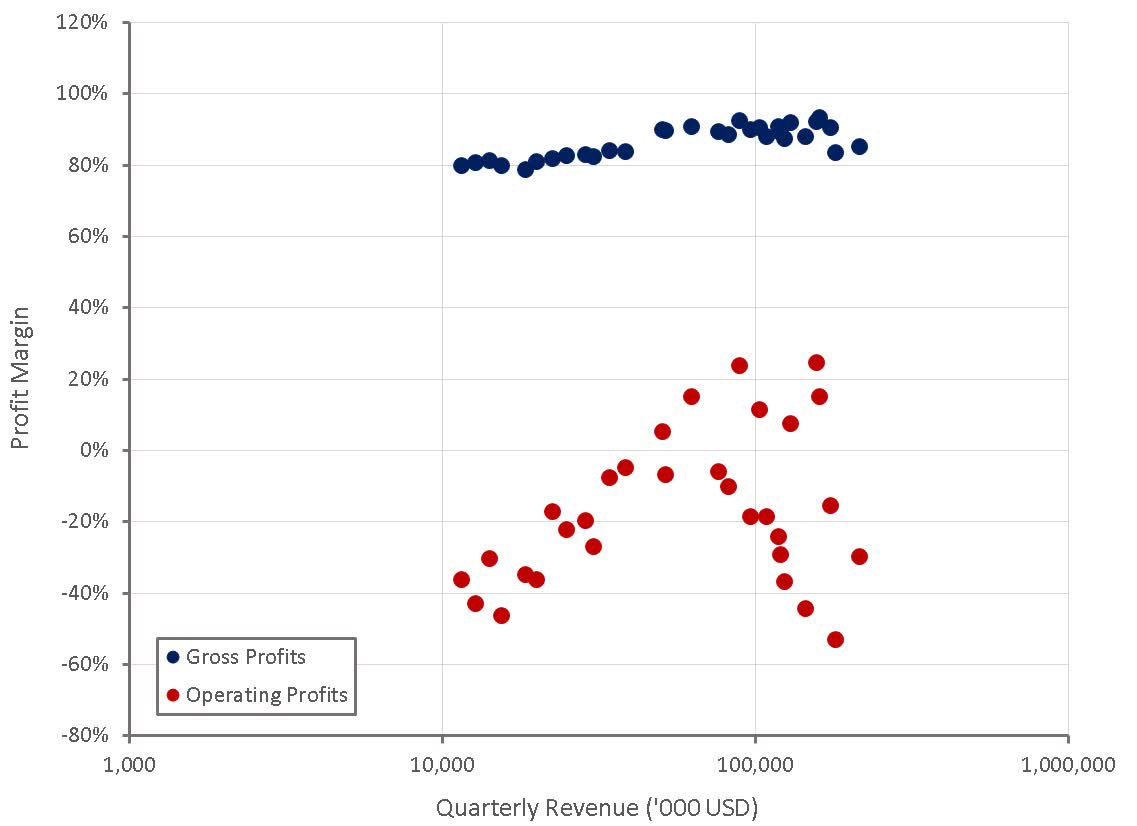

Alteryx's gross margins remain strong, but are likely to come under pressure if their cloud products begin to gain traction. Operating margins have deteriorated significantly over the past few years as the company has invested in product development and sales and marketing. Alteryx now need to demonstrate that the returns on these investments are sufficient, and that the company is able to generate efficient growth.

Figure 6: Alteryx Profit Margins (source: Created by author using data from Alteryx)

{kind=link}

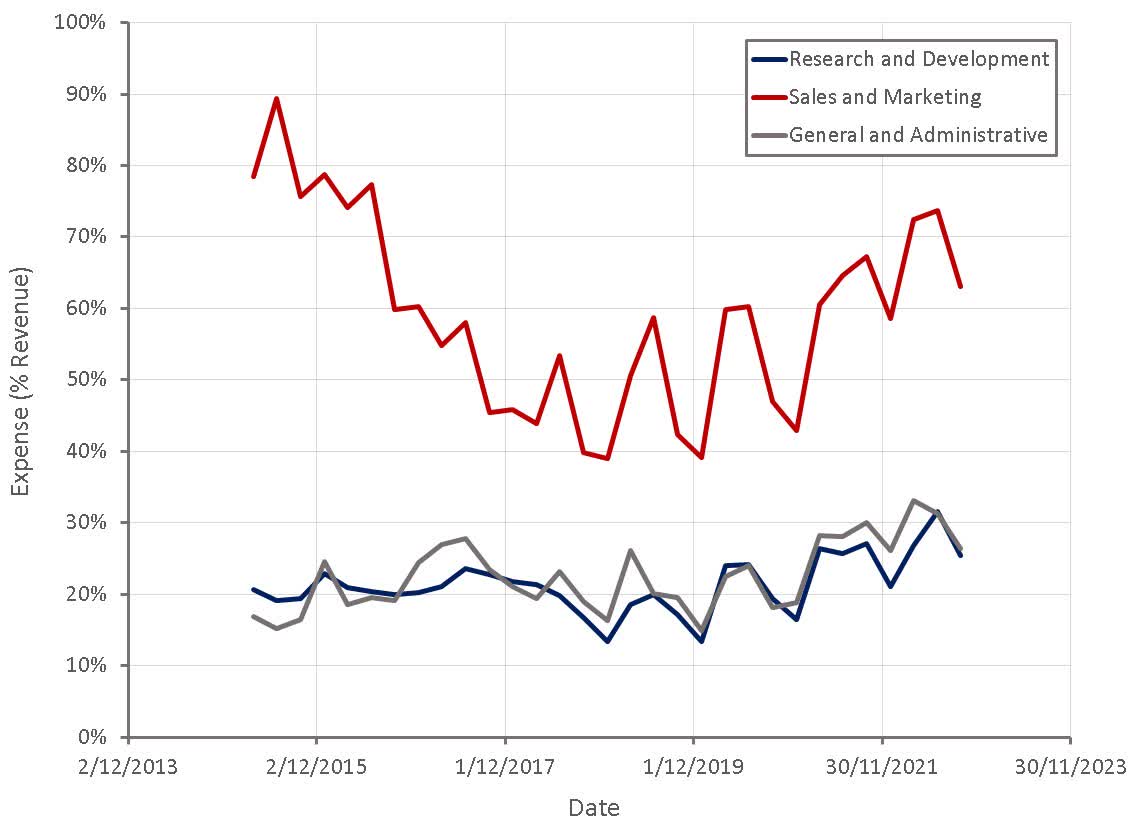

Alteryx's customer success organization has more than quadrupled in the last two years, and while this supports renewal rates and expansion, it has added to Alteryx's costs significantly.

Alteryx is moderating its pace of hiring, and also plans on executing a real estate rationalization initiative in Q4. Provided that growth remains robust, this should lead to improved margins in time.

Figure 7: Alteryx Operating Expenses (source: Created by author using data from Alteryx) Figure 8: Alteryx Job Openings (source: Revealera.com)

{kind=link}

{kind=link}

Valuation

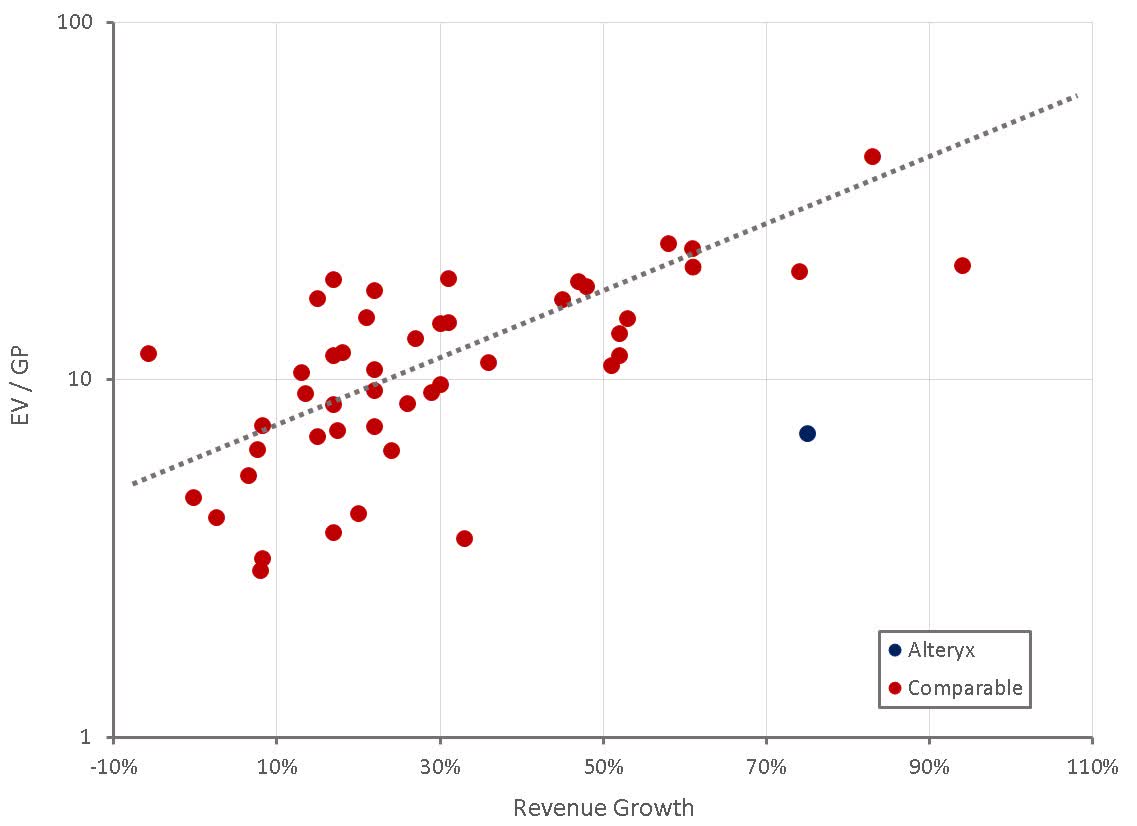

Alteryx appears inexpensive relative to peers given its current growth rate and gross margins. Some of this may be due to the fact that sustainable growth is viewed as being more like 30%, but even then, Alteryx would appear cheap. This could prove to be an opportunity if Alteryx is able to reduce the burden of operating expenses while maintaining growth, but Alteryx may continue to trade at a discount if analytics software continues to be viewed as relatively indefensible.

Figure 9: Alteryx Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Alteryx: Sales-Driven Growth Rebound