AYX - Alteryx: The Rebound Rally Is Here

- Shares of Alteryx jumped nearly 20% after reporting a blowout second quarter and substantially raising guidance for the year.

- The company noted that sales cycles are improving and that it's entering Q3 with its strongest pipeline in history.

- With pro forma gross margins near 90%, Alteryx is one of the most scalable software companies in the market.

- Trading at just ~6x current-year revenue, Alteryx still remains a bargain stock.

The clouds are lifting for the growth sector. Risk-taking is back in vogue as concerns about inflation and rising rates have muted, and in recent weeks tech stocks have started reclaiming some of this year's heavy losses.

There are few rebound opportunities, in my opinion, that are as appealing as Alteryx ( AYX ). This big data stock, which focuses on data integration tools that allow companies to pull in data streams from various sources and bypass manual data-fitting work, had been in a steady decline since mid-2020. Yet now with a subscription transition well underway and a very strong Q2 print under its belt, Alteryx is coming back roaring.

Post-Q2 earnings, shares of Alteryx jumped nearly 20%, bringing its year-to-date performance to nearly flat (far better than many other tech stocks). And considering that Alteryx still remains quite undervalued, I think there's plenty of rebound potential left to go.

The bullish thesis remains vibrant, especially with guidance boost

I remain bullish on Alteryx, and I think this post-earnings rally is just the beginning of a long-deserved upward correction in this stock. The big data market remains vast - and Alteryx has proven itself to be a mission-critical wedge tool in helping businesses wring value from their own data. And now, with Alteryx shifting away from pricey one-time licenses (that were once notoriously known as among the most expensive software offerings on the market) to recurring-revenue deals, the company has also lowered the barriers to adoption while also creating a more predictable lifetime revenue stream.

As a reminder for investors who are newer to Alteryx, here's a rundown on the key bullish drivers for the name:

- Digital transformation is already underway. Companies want to use data to drive decisions. Unfortunately, data is sometimes locked in different formats and takes hours of manual work to untangle. Alteryx's technology helps with that process and automates one of the most labor-intensive pieces of adopting a "big data" strategy in the C-suite. Investing in technology like Alteryx may not have been a top priority during the pandemic, but it will become a much hotter-button topic as we look ahead.

- $65 billion TAM- Alteryx's current ~$730 million annual revenue run rate is only a fraction of its estimated $65 billion TAM, leaving plenty of room for growth. Alteryx's acquisition of Trifacta will also immediately kick in with $20 million of ARR contribution in 2022.

- Truly horizontal software serving a wide variety of use cases across many industries- Alteryx's software is broadly applicable to clients in virtually any industry. An illustrative cross-section of Alteryx's customer base: Netflix ( NFLX ), Walgreens ( WBA ), Abbott Laboratories ( ABT ), Chevron ( CVX ), Wells Fargo ( WFC ), Visa ( V ), Marriott Hotels ( MAR ), and Facebook (META) are all among Alteryx's anchor clients, spanning every trade.

- Best-in-class gross margins of ~90% are among the highest in the software industry- Virtually every dollar of revenue for Alteryx flows through to the bottom line, justifying the efforts that Alteryx makes on the initial sale.

- Plans for significant profitability- At present, Alteryx is breakeven on a pro forma operating margin perspective (already better than many SaaS peers). Over the long run, it plans to generate pro forma operating margins in the 25-30% range, primarily by achieving economies of scale on sales and marketing. When a company like Alteryx has huge recurring revenue, over time the cost of sales support for that revenue base will eventually dwindle.

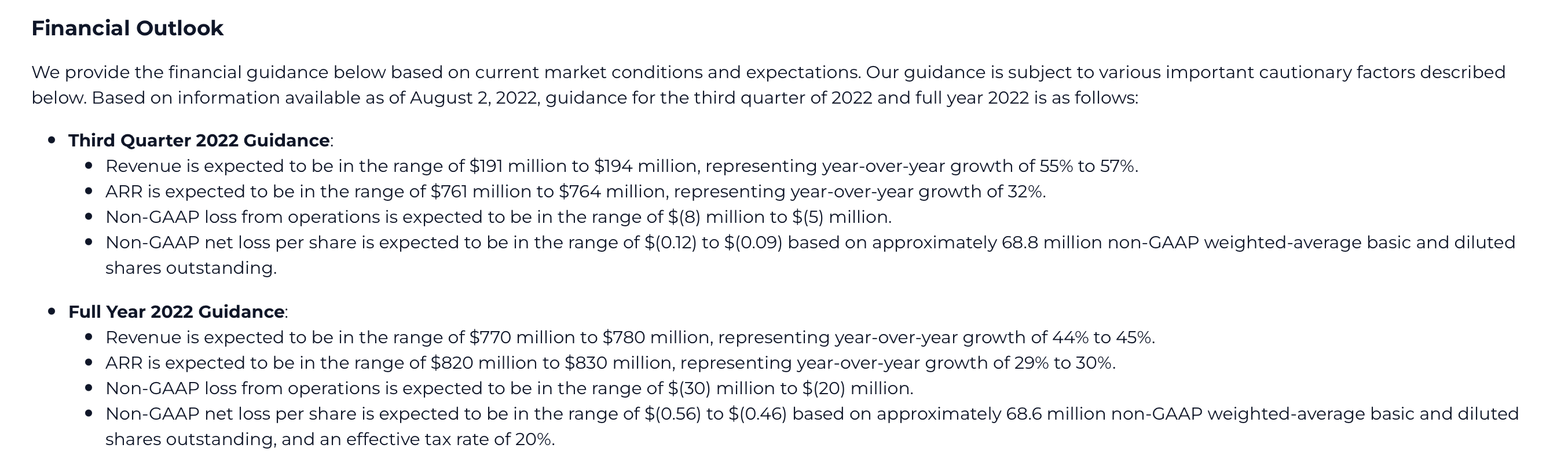

We'll note as well that Alteryx just significantly boosted its guidance outlook for the current year. It's now pointing to $770-$780 million in revenue for the year, up 44-45% y/y - up from a prior guidance outlook of just $730-$740 million, or 32-35% y/y growth - needless to say, quite a big jump.

{kind=link}

Alteryx's valuation is also quite well-positioned against this outlook. At current share prices near $61, Alteryx trades at a market cap of $4.16 billion. After we net off the $511.7 million of cash and $875.8 million of debt on the company's most recent balance sheet, the company's resulting enterprise value is $4.52 billion.

This puts Alteryx's valuation at 5.8x EV/FY22 revenue, versus the midpoint of Alteryx's updated guidance range - quite a bargain for a stock that is currently growing revenue at a ~50% y/y pace, and with near-90% gross margins to boot.

The bottom line here: Alteryx's years-long losing streak is seeming to come to an end, and its rebound rally is just beginning. This is a high-caliber software company that is well-positioned to capture a huge $65 billion market opportunity and scale profitably. Don't miss the chance to buy this stock while it's still cheap.

Q2 download

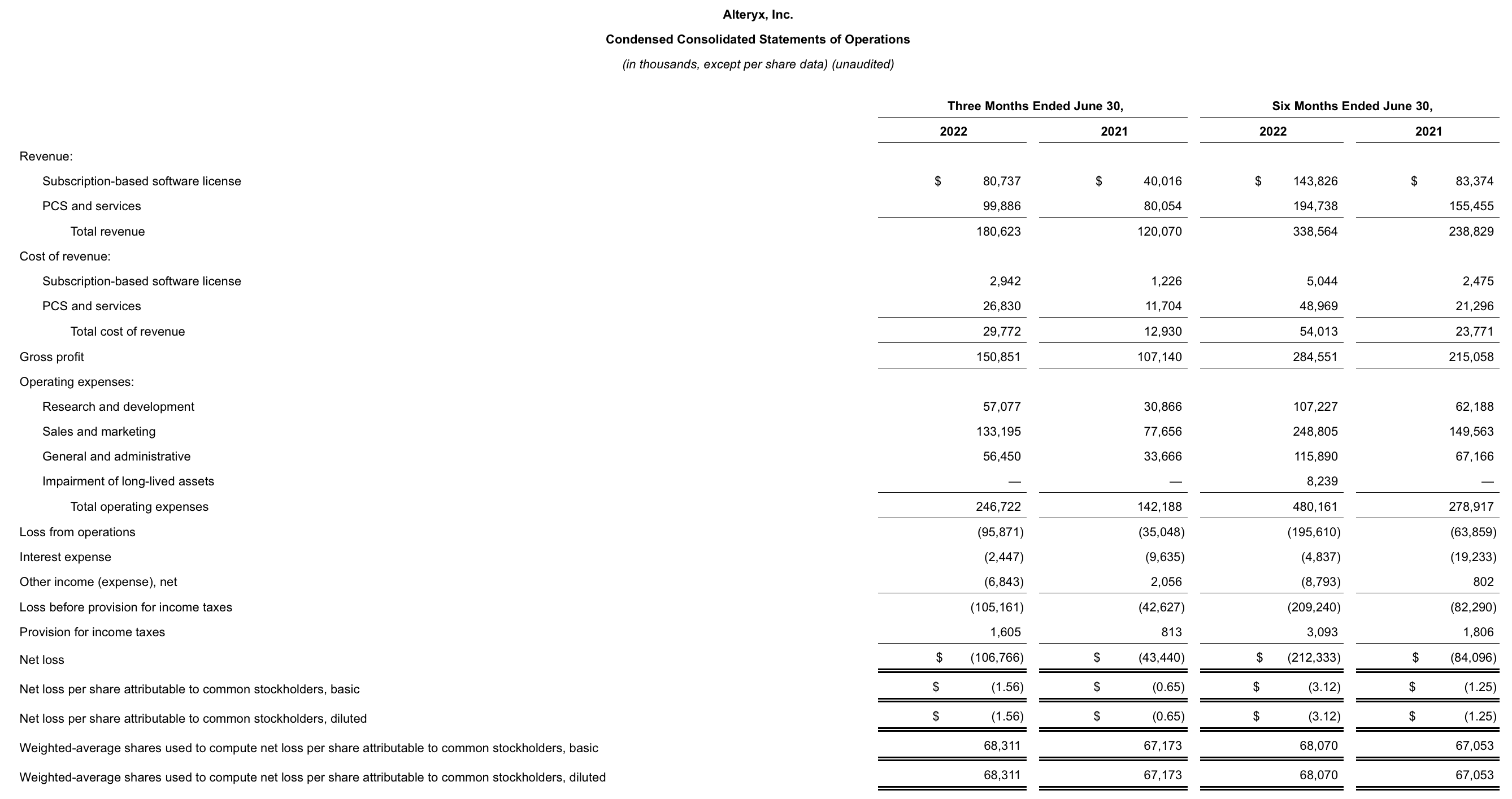

Let's now go through Alteryx's latest Q2 results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Revenue grew at a stunning 50% y/y pace to $180.6 million, beating Wall Street's expectations of $160.9 million (+34% y/y) by a massive sixteen-point margin. Revenue growth also accelerated substantially versus 33% y/y growth in Q1.

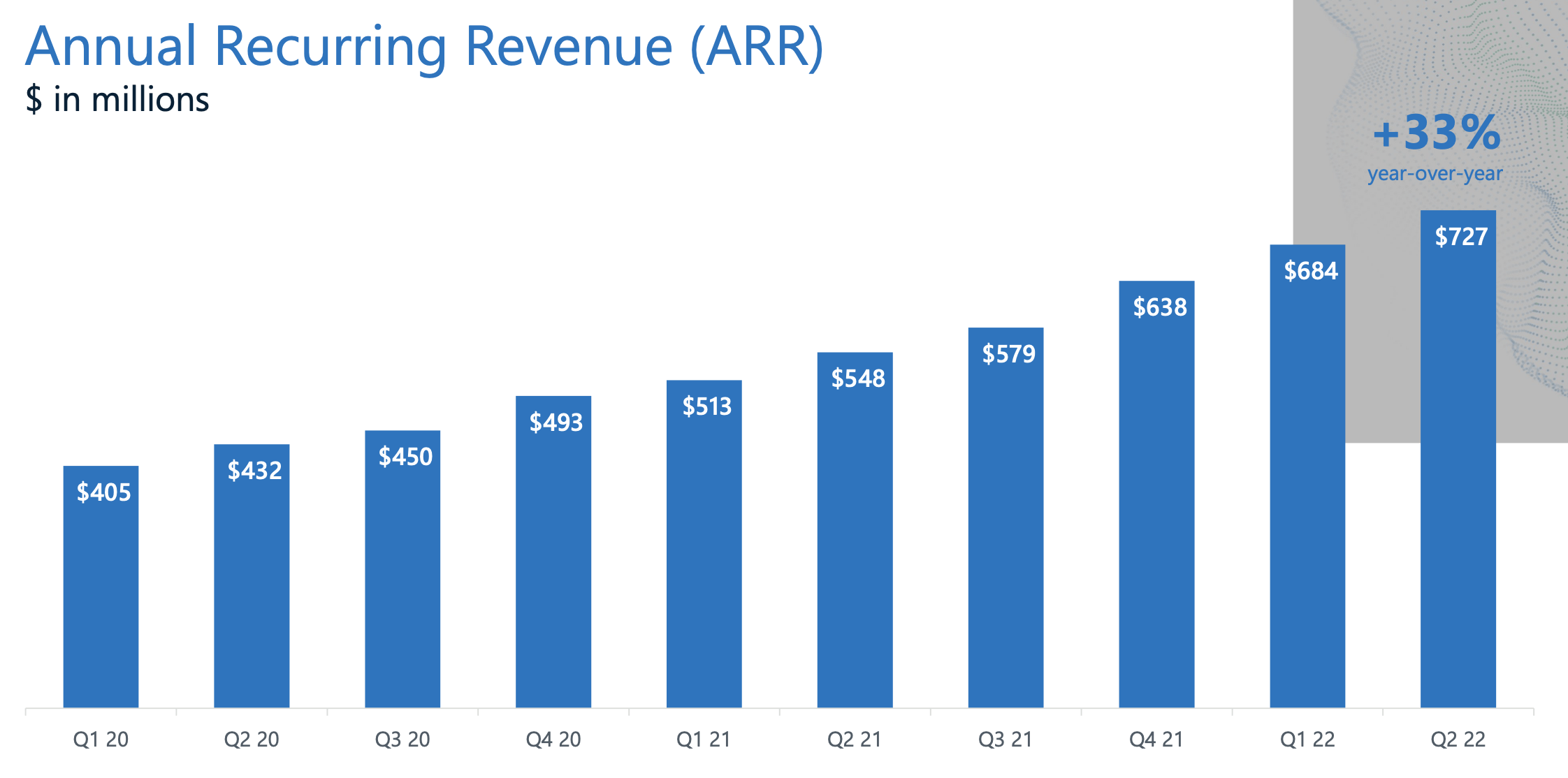

Alteryx also added $43 million of net-new ARR in the quarter, growing quarter-end ARR to $727 million, up 33% y/y. We note that now, Alteryx's ARR base is almost on-par with its annual revenue guidance, signaling that its subscription/recurring-revenue shift is largely complete. The company also expects to add roughly $100 million of new ARR through the end of the year, ending FY22 with $820-$830 million in ARR.

{kind=link}

Several factors drove the outperformance in Q2. The company noted that it saw a double-digit y/y increase in sales productivity. It's also seeing a large class of new sales reps ramp up, which positions Alteryx well for continued go-to-market success.

Partners are also driving an increased amount of business. Alteryx noted that approximately half of new ACV bookings in Q2 were sourced by partners; and the company intends to continue leveraging these resellers to expand its market reach beyond Alteryx's direct sales force.

The company also notes that it's entering Q3 with the biggest opening pipeline it has seen in years. Per CFO Kevin Rubin's prepared remarks on the Q2 earnings call:

In summary, the company is executing at a high level with positive growth trends and improving profitability. Our subscription-based well-diversified business model has us on solid footing entering the second half. Nonetheless, we are mindful of the current macro environment. We are leveraging Alteryx data analytic capabilities to help navigate the current macro environment and are closely monitoring a breadth of key performance indicators.

Pipeline generation is a metric that we track closely. We saw solid year-over-year growth in Q2, resulting in the highest Q3 opening pipeline we've seen in many years. Sales cycles are another key metric where we saw a slight improvement in Q2. And finally, renewal rates provide us a clear lens on the market demand. And as Mark mentioned, this was at a multiyear high in Q2."

And while Alteryx did opt to invest in growth in Q2, the company's -17% pro forma operating margin in the quarter came in well ahead of the -31% implied in the company's guidance for the quarter. The company intends to hit a -3% operating margin for the full year FY22, while hitting 25-30% in the long run after rationalizing down sales and marketing spend.

Key takeaways

Alteryx is on the upswing, and given the company's phenomenal growth performance and its significantly lifted expectations, I think there's plenty more room on the upside here. Stay long.

For further details see:

Alteryx: The Rebound Rally Is Here