AAMC - Altisource Growth Engine Is Way Ahead Of Expectations

2023-05-31 10:00:00 ET

Summary

- Altisource was for many years a cash shell company that traded at a discount to net cash as it slowly leaked value for almost a decade.

- The value proposition radically changed when a decision was made to hire CEO Jason Kopcak to use Altisource assets to create a low risk loan origination "flow" business.

- The company's wholesale loan origination platform is tracking far ahead of expectations. This became clear on the recent earnings call.

- I now expect originations to hit at least a $10B annual run rate in 2024, more than triple my previous estimate.

- That works out to an annualized EPS run rate of $67 a share by Q4 2024. And it may be conservative.

Altisource Asset Management ( AAMC ) is an ultra fast growing mortgage originator and reseller with more than $25 a share of net financial assets. I wrote about the company previously, so you can check that out if you want. to. In that article I made the case for a $22 EPS run rate by Q4 2024 as a base case. However, when AAMC reported earnings on May 15 2023 it was clear that my base case estimate was far too low.

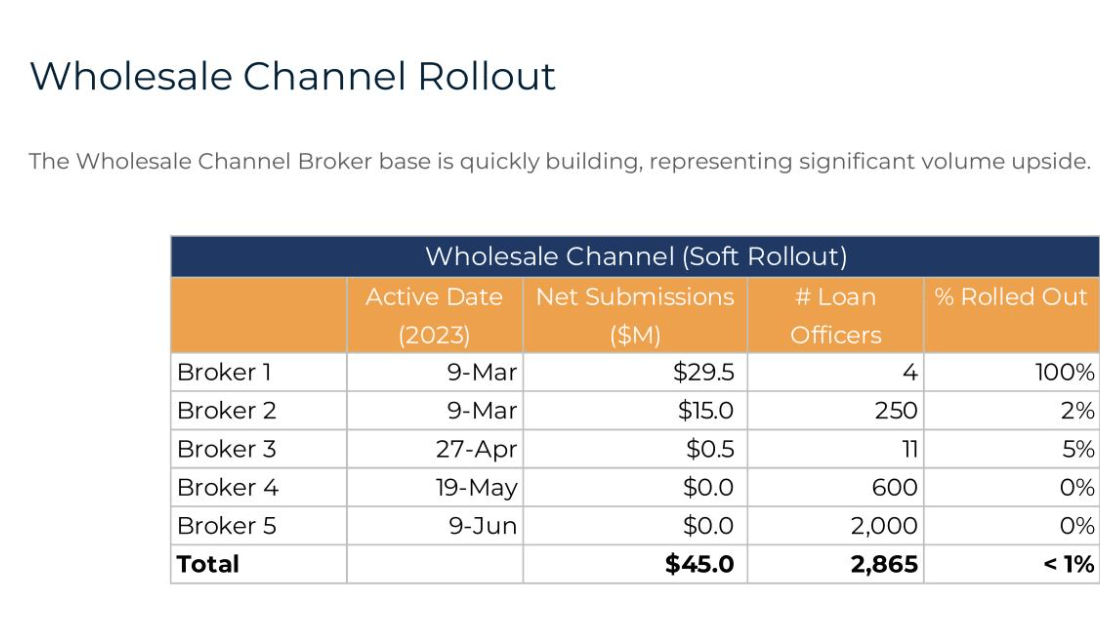

The Wholesale Channel

I won't bury the lede. During the Q1 2023 earnings call, the company included the following slide from their earnings deck :

{kind=link}

The wholesale channel was active for roughly 2 months, and was less than 1% rolled out. And $45M of loans have been submitted so far. Not all submitted loans will close, but still, let's just think that through for a minute. The lofty goal - I thought it was lofty - that I had set for them in my first article was a $3B loan origination run rate by YE 2024, split roughly 50-50 between their direct-to-borrower channel and their wholesale channel, $1.5B each. The former is still on track, but wholesale is, well... What is it exactly?

They did $45M in 2 months. Annualized, that's $270M. If it's 1% rolled out, then we need to scale that up 100x, so. Right. Take a deep breath. Right. It's $27B. That's what this slide is telling us.

AAMC's value proposition to wholesale brokers

There are tons of loan officers in the US, most of them at banks. And banks are constrained by regulators from handling the kinds of products that AAMC offers. I'll talk more about that below, but for now I just note that banks can't meet the demand. Anyway, they have lots of loan officers, and Kopcak thought he might approach them with the following value proposition. Not a new idea or anything, it's been done before. But he would reach out and see what could be done.

And the idea - essentially a regulatory arbitrage - is that the banks' loan officers can originate on behalf of AAMC for a fee. That keeps the whole thing off the banks' balance sheet and doesn't ever touch deposits, and that means regulators don't object. No credit risk, just a fee, nothing to object to. Again, not a new idea, but how much uptake would there be?

And... it turns out, a lot. There are a lot of idle loan officers right now, and this gives them something to do. So instead of having to try to talk a good sales game and get partners on board in some sort of long process, they just all say yes right away. And yes, Kopcak is well pedigreed in the industry and the takeout partners he has lined up are giant insurance companies. The banks see all that before they say yes. But no one has to talk them into it. They are on board the moment the offer is made.

And no one knew that until now. I don't think Kopcak knew it, I certainly didn't... did you? Kudos if you did, but I'm guessing for most of us, no. And so a business which was supposed to be rolled out as a 50-50 direct-to-borrower and wholesale business is now going to be 90% wholesale. And not because direct-to-borrower is going worse than expected.

On the origination side, it appears that AAMC will not be constrained to anything remotely as low as $3B. Whatever the demand is from takeout partners, they will be able to provide it.

Regulatory arbitrage: why banks don't compete with AAMC

As an aside, I get asked all the time how this can be. That is, how do regulators make this opportunity possible? The opportunity for AAMC is all in products that banks are kept away from by regulators. These are products that make all the sense in the world, but banks can't hold as much of these as they can originate. Why is that?

Our bank regulators - in my view - are not exactly rational, as a group. As a recent example, we have seen them allow truly extraordinary risks to show up on bank balance sheets as long as these have no credit risk. 10 year duration Treasuries at 1.5% are just incredibly risky if they are being funded by floating rate deposits of any kind. If rates are at zero the banks make 1.5% per year, less the cost of servicing the depositors. But then if rates go to 4% they lose 2.5% per year, plus of course the cost of servicing the deposits. $100B tied up for 10 years means a bank - maybe one which has less than $10B of its own money - will lose $30B if rates go up. Which they did, in some cases, and regulators let this happen. It was not hidden, or even particularly unexpected that rates might go up, but regulators let it pass right on through. Treasuries are square pegs and regulators are square holes. Or something. Massive duration and interest rate risk at institutions with deposit flight risk passed regulators, and we've all seen the result in the recent banking mini-crisis.

But a product that's more of a round peg? Credit risk - even if it's a good risk - doesn't happen as much at banks any more. It's a poor regulatory reaction to the GFC. Prior to that, regulators allowed lots of freedom for banks. They asked for careful modeling of risk, but the problem at that time was that the new securitized products at the time were modeled... maybe not dishonestly, but very poorly. And in that case it was credit risk that blew everything up. So there was an overreaction to this from regulators and a regulatory risk arbitrage has developed, wherein products that perhaps should be handled by banks are instead in the hands of others.

Insurance companies have a different regulator and they are allowed to own round pegs. The round peg stuff that AAMC originates is way less risky than those 10 year treasuries. Way less. Consider RTL loans. Here's what Kopcak said about these on the Q1 2023 earnings call :

short duration one to two-year term, high-yielding fixed income assets with a gross weighted average coupon of 9.5% to 12%, secured by one to four family residential or multifamily residential properties going through value improvements... known as residential transitional loans or RTLs

The interest rates are high, credit default does happen but is modest. And duration is short, so it's hard to get hurt if interest rates change. It's a perfectly cromulent product, which is why insurance companies are happy to own it. But, round pegs they are, and banks can't own as much as they'd otherwise like to. So until that changes - and here we are 15 years later and regulators show no signs of waking up - this opportunity will be there.

AAMC's business model

On the Q3 2022 call Kopcak laid out his vision. He would turn AAMC into a mortgage origination "flow" business, which will hit a $1B origination run rate by 2h 2023, and then ramp from there. The idea is to originate loans and then sell them with an extremely rapid turnover to end customers in pre-arranged agreements. The hold time they are targeting is three days; that's why it's a "flow" business, and also why it's low risk to AAMC. The buyers are in place ahead of time, so the only risk is execution. As long as AAMC can deliver the product to spec - all the documentation in order, that sort of thing - then the buyer has already agreed to buy the loans.

Kopcak then summarized the business model in a tremendously clear way on the Q4 2022 earnings call (emphasis mine):

Our strategy which is unique in the industry is that we are capital light originator of private credit products . These products include both short duration, high yielding fixed income assets, secured by one to four single family residential or multifamily residential properties going through value improvements, also known as residential transitional loans or RTLs, as well as long duration interest only secured by income producing residential properties, also known as DSCR loans. Such products are distributed to institutions with permanent capital, such as insurance companies, pension funds and endowments.

I have 15 years of unique experience relationships with these institutions. Unlike our peers, we do not use loan securitizations as an exit for our loans. Instead, we establish individual criteria, or a Buy Box, to sell loans to insurance companies or other funds that are backed by endowments and pension funds. These institutions have large stable cash that needs to be invested in fixed income products. We then go to market to originate these loans via our three channels: direct to borrower, wholesale, [and our] broker direct channel...

Insurance companies, pension funds and endowments have potentially over a trillion dollars allocated to be invested in alternative fixed income assets...

AAMC refers to these end buyers as "takeout partners". AAMC's business model is to only originate loans that it can quickly sell, in a week or less, and in pre-arranged contracts, with their takeout partners. AAMC expects to hold loans they originate for a week or less, so that, for example, $10B of annual originations can be accomplished with $200M of originations per week, and therefore with a balance sheet that only holds $200M or loans at a time. AAMC needs to hold 10% of this amount - this is a requirement from their warehouse lender - using its own capital. $20M of capital is all that's needed to originate $10B of loans per year.

That's the business model. A capital lite mortgage origination flow business, where all the credit and interest rate risk is borne by takeout partners who don't have the infrastructure to originate loans. The only risk to AAMC is execution.

Demand from takeout partners

Origination is only one side of the equation. They also have to have enough takeout partners lined up to buy the loans they originate. So if it looks like they can originate at a $10B or more annual run rate in 2024, the natural question is, are there enough buyers?

They are not there yet, but it looks really promising that they will get there. Kopcak has said that their takeout partners look to transact at least as much as $50M per month each. And some more than others, depending on size and appetite. I'm going to guess these will average $100M per month each.

AAMC has ramped from zero takeout partners in 2022, to 2 early in 2023, and then added 3 more as of May 12 2023. One of these partners has an incredible $500B of assets under management:

The Company entered into forward contracts to sell alternative credit products to three additional institutional counterparties, bringing our total to five, that manage insurance and credit investments. One of the new institutions has over $500 billion in assets under management.

And then on the Q1 2023 earnings call , Kopcak noted that they are in talks to add more takeout partners, and noted once again his long standing relationships with these giant institutions:

We added three additional takeout investors, two of which have insurance money. We are in talks with several additional takeout investors... I have 15 years of experience and unique relationships with these institutions.

At 5 takeout investors, this is a minimum of $3B of demand already in hand. Remember, Kopcak has been clear that these giant partners prefer to transact at least $50M per month each in order for to be worth their time and effort. And using my own rough guess that on average they will transact above this minimum, to perhaps $100M per month - just a guess - they are already at $6B.

And yet they are in talks to add more. If one were to wonder about the scale AMMC is expecting to hit, just think about it for a minute. Are they aiming for $3B in originations? No, they are not. If they hit 10 take-out partners - by 2024 that doesn't seem too aggressive in my view - that's $12B of annual demand.

Valuation

The math is simple enough. I estimate AAMC will generate an EBITDA margin of 140 bps on loan volume once it's fully up and running. That's a 40% EBITDA margin on revenue, assuming an average of 350 bps of revenue on loan volume. AAMC seems to agree, using a 150 bps EBITDA margin in their Q1 2023 slide deck .

At 140 bps and $10B of originations as a run rate by YE 2024, that's $140M of EBITDA. They will also generate some net interest income on loans, perhaps $10M or so, for pre-tax profit of $150M. Fully taxed at 15% - their USVI domicile, a legacy from their days as a subsidiary of Ocwen, means a low tax rate - results in $127.5M of earnings. With 1.9M fully diluted shares, EPS is $67.

There's a ton of uncertainty on this number. It could be lower. It could also be higher. All the elements are in place for $15B of originations - a $100 EPS - or indeed $20B. The market is ~$1T. They don't have to corner the market in order to get to $20B of originations.

That said, I will use an 8 PE on $67 EPS for purposes of valuation, or $536 a share.

Risks to the Thesis

By far the biggest risk is execution. The company has big plans, and they are off to a great start, and CEO Jason Kopcak has done this twice before. That sounds great, but they have to actually execute. If something goes wrong, then they will be falling back on their roughly $25 a share of net financial assets. The stock could easily trade under that if the current business plan doesn't pan out.

There is also clearly a "key man" risk. None of this works without Kopcak. He's not old - only 50 - and appears in robust good health to me. And I think he is highly motivated to stay at AAMC, to take advantage of the incredible opportunity right in front of him. So I don't think the key man risk is a high probability. However, it might be ugly for AAMC shareholders if, for some reason, Kopcak could no longer serve as CEO.

Conclusion

AAMC is quickly ramping to an EPS in excess of $50, and maybe $100 or more. The ramp is dependent on execution, but CEO Jason Kopcak has done this twice already, albeit on a smaller scale. The current sub $100 stock price is absurd, and the stock should be bought.

For further details see:

Altisource Growth Engine Is Way Ahead Of Expectations