LIFZF - Altius Minerals Is Placed On The Sell List

Summary

- 2023 will be a challenging year for potash, copper and iron ore operators.

- Altius Minerals is not expected to perform well as 80% of its business is exposed to potentially underperforming commodities.

- At current levels, which are not low, investors should consider selling some shares of Altius.

Price Outlook for Potash, Copper and Iron Ore

For operators that exploit the following markets: potash, copper and iron ore, 2023 is not likely to be favorable as certain macroeconomic and geopolitical headwinds will be strong enough to create downward pressure on commodity prices and production.

The war in Ukraine has significantly upset the balance between potash demand and supply on world markets. With more than 40% of potash traded on world markets coming from Black Sea ports, concerns about potash stocks due to the war in Ukraine have led to the following situation. A glut of potash as countries decided to ramp up production while demand collapsed as farmers limited spending on potash at record prices in 2022. Due to this situation, some analysts are now predicting that the potash fertilizer price in the US markets could fall by more than 25% this year, while plant utilization could be slightly lower.

Copper doesn't appear to be doing particularly well in 2023 either. Traders have revised downwards their copper demand forecasts on an expected recession due to central banks' rate-hiking maneuvers, completely shattering optimism sparked by the reopening of the Chinese economy. Copper Futures - March 23 (HGH2023), trading at $4.02 per pound at the time of writing, is expected to fall about 8% over the next few months to end 2023 at $3.71.

On the same rationale for the fall in copper prices and likely lower production, iron ore is expected to trade lower this year, falling more than 10% from current levels to $111.62 a tonne within 12 months.

Why Altius Minerals Corporation Is Not Expected To Perform Well

Given the poor prospects for potash, copper, and iron ore in 2023, investors should adjust their holdings in US-listed companies involved in these commodities accordingly.

They may want to sell shares of Altius Minerals Corporation ( ATUSF ) stock, as the business of this diversified Canadian mining royalty and streaming company has momentum depending on the commodities in question. Lower prospects for the price and production of potash, base metals, and iron ore will impact nearly 80% of Altius Minerals Corporation's overall business. There are currently many negative catalysts for this stock to trade lower.

About Altius Minerals Corporation in the Metals and Mining Industry

Headquartered in St. John's, Newfoundland and Labrador, Canada, Altius Minerals Corporation derives its revenue from the management of royalties and streaming interests in potash, base metals and coal mines throughout North America and South America.

Altius also manages some renewable energy royalties and investments, and it participates in early-stage projects to develop future royalty and other minority interests.

In terms of total royalty revenue, potash accounted for 40% of total royalty revenue of Canadian dollars [CA$] 103.35 million ($76.3 million) in full-year 2022 , while base metals (mainly copper) and iron ore accounted for 30% and 10% of total royalty.

The remaining 20% of total royalty comes from thermal coal, renewable energy and other revenue streams, but as developed countries enter a recessionary phase this year, those revenues are likely to take their toll in 2023 as well.

Analysts are indeed forecasting a higher price for coal through 2023, but with such a prospect for the economy of industrialized countries, there is a high chance they will downgrade their estimate.

What Royalty Income Looked Like in 2022 and What It Could Look Like After 2022

Royalty revenue of CA$103.35 million (or $76.3 million) in 2022 represents a 23.14% increase over the prior year and a 53.1% increase over the full year 2020.

Potash revenue (40% of total royalty revenue) increased 115% year-on-year thanks to higher realized prices, but only in the first half of the year due to a market overreaction to concerns about regular potash sourcing during the Russo-Ukrainian War.

Those strong geopolitical upward pressures have now eased while analysts are forecasting a significantly lower potash price as there is too much potash on deck relative to the demand, leaving the Altius segment without a tailwind from higher prices in 2023.

In terms of potash production attributed to royalties, raw material tonnage in 2022 was close to 2021 levels, but with the global potash market on the brink of oversupply in the near term, investors should expect miners to slow production activity throughout the current year.

With production and price being the two key components of royalty revenue, Altius is likely to see lower potash revenue going forward, which could potentially impact its share price in a negative way.

The replacement of lost production from certain units with the commissioning of a new production unit in Canada in 2022, coupled with a plan to ramp up production capacity at most potash mines, has required the allocation of significant financial resources to capital projects.

Leaving aside long-term forecasts that may be unreliable given the high volatility of commodities, the mining companies have announced that the investments were also made to respond to the current needs of global supply constraints.

Now, with a global potash market that analysts predict will have no problem with limited supply this year while prices are expected to fall sharply, the investments threaten to cost miners more than what they can get back in the short term. If these unfavorable dynamics materialize in 2023, the indirect effect for Altius could weigh heavily on profit margins and potentially on share prices as well.

Base and battery metals revenue (30% of total royalty revenue) fell 22% year over year due to flat copper prices and a drop in copper production following the closure of a facility in Canada.

The discovery of a new copper deposit in Brazil in early 2022 with indicated copper grades in excess of those currently being mined by Altius' royalty payers is now part of a project to extend the life of a specific operation in Brazil. The company has promised to release an initial resource estimate early this year. Altius is also engaging in the development of royalty revenues from lithium production in Brazil.

Surely these projects will face unfriendly internal politics in the field of mining activities in the next 4 years. Unlike the previous government of President Jair Bolsonaro, the current government of President Luiz Inácio Lula da Silva, a former trade unionist, is pro-environment and anti-deforestation and anti-drilling. As such, Altius sees the country's risk to its Brazilian royalty revenues increasing, and investors should take that aspect into consideration as well.

Altius is also looking forward to royalty revenues from the commissioning of a project called the Curipamba copper-gold project in Ecuador. The project now requires the necessary permits to operate, but the decision to build the facility will not be made until early 2024.

The internal situation in Ecuador could pose a risk to the miners and Altius' future plans. In recent times, indigenous peoples have often been the protagonists of violent anti-government demonstrations against the sharp rise in the cost of living. In addition to social tensions, the country is grappling with political crises, one of the most notable being the attempt to overthrow President Guillermo Lasso by opposition members of Parliament in June 2022.

Iron ore income (10% of total royalty income) in the form of dividends from Labrador Iron Ore Royalty Corporation ( LIFZF ) ( LIF:CA ) fell 38% year over year as a larger percentage of Labrador's free cash flow was allocated to growth and sustaining capital investments rather than paying dividends.

In 2022, Altius increased its stake in Labrador Iron Ore Royalty Corporation [LIORC is the acronym] by purchasing 866,000 shares for a total consideration of CA$ 25.9 million. The investment returns 9.4% (CA$0.70 x 4 quarters x 866,000 shares / CA$25.9 million) versus Labrador Iron Ore Royalty Corporation's TTM dividend yield of 8.41% .

Altius' return on LIORC's equity is very high as it is 5.7 times the average of the entire stock market , but the investor should consider the following aspect instead. Since the market in which LIORC operates is as volatile as Altius', the dividend can fluctuate widely from one period to another.

That means for Altius shareholders, iron ore royalty revenue could decline significantly in 2023 as iron ore market conditions are expected to deteriorate. The effects of the recession and higher borrowing costs are likely to weigh on construction activity. Demand for iron ore to make steel products for use in construction will fall, and lower demand will push iron ore prices down.

Perhaps it is no coincidence that analysts expect LIORC earnings per share to fall 27.70% year-on-year in 2023 and 17.20% year-on-year in 2024.

Because dividends are earnings not retained by the company for growth initiatives and sustained capital investments, Altius' iron ore royalty revenue could mimic the same negative trend expected for LIORC's earnings and potentially impact Altius' stock price.

Thermal [electric] coal revenue (14-15% of total royalty revenue) increased 68% year-over-year thanks to the temporary factor of higher inflation and higher coal consumption at a power plant in Genesee, Canada.

The use of coal can also be seen as temporary because the Genesee power plant operator plans to phase out coal use by 2024 as it continues to invest in the coal-to-natural gas conversion project to address global climate change.

Altius is targeting higher royalty revenue from its 58% interest in Altius Renewable Royalties, and the attributable royalty revenue from investments in U.S. renewable energy projects increased 12 times year-over-year to $4.8 million, or 4% to 5% of total revenues in 2022.

Later in 2022, a $20.7 million equity loan received from Altius allowed venture capital company Altius Renewable Royalties to earn two production-stage royalties.

The Financial Condition

As of September 30, 2022, Altius' balance sheet was characterized by net debt of $18.6 million , which led to financial expenses of $4.6 million for the 12-month period that ended Q3 2022.

When the financial cost of $4.6 million is divided by the 12-month operating income of $41.7 million , it gives an interest coverage ratio of 9.06x.

According to analysts at GuruFocus , Altius isn't able to generate returns that match the cost of the capital it's raising to find the investment. This unfavorable dynamic is evident from the following comparison in which Altius' weighted average cost of capital [WACC] of 9.13% exceeds Altius' return on invested capital [ROIC] of 4.93%.

But looking at the Altman Z-score of 3.55 (on this page , scroll down to the ‘Risk’ section), which means the company has no chance of going bankrupt, Altius isn't in financial trouble.

Overall, Altius' financial situation isn't bad, but it needs to improve, and 2023, with all its challenges, won't be one of the easiest periods to get the job done.

The Stock Valuation

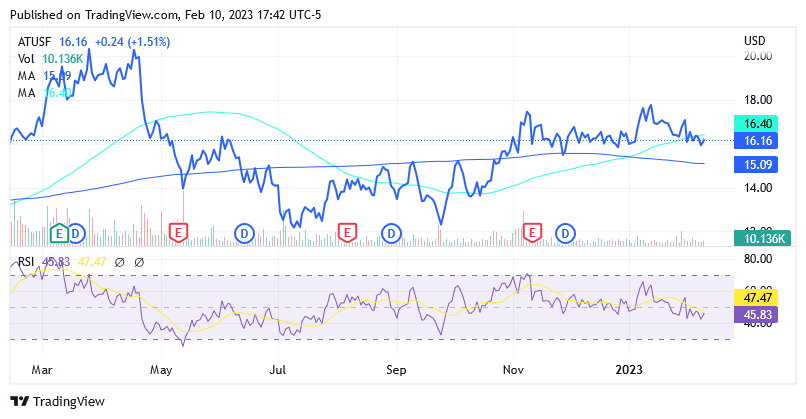

Shares of Altius Minerals Corporation were trading at $16.16 per unit for a market cap of $757.13 million as of this writing. The stock paid a quarterly cash dividend of $0.06 per share on Dec. 15, 2022, determining a TTM dividend yield of 1.44% as of this writing.

{kind=link}

The shares are not trading low as they are almost level with the 75-day simple moving average line while trading well above the 200-day simple moving average line.

Additionally, shares are near the $16.13 midpoint of the 52-week range of $11.90 to $20.36.

The stock also has a 14-day relative strength indicator of 45.83, indicating that the stock is neither oversold nor overbought. However, the RSI's curve is currently in a negative drift, which could suggest a bearish sentiment currently prevailing around this stock.

The current share price development may reflect the following scenario. This year will probably not be a good year for the companies that pay the royalties to Altius, as macroeconomic and geopolitical factors will create very strong headwinds and reduce growth opportunities.

Those expectations do not imply better stock prices than current ones, making the decision to hold the same number of Altius shares in a portfolio uncomfortable at this point. There is a high opportunity cost to owning Altius, rather than other investments that may have a better chance of success.

Since the shares are not trading low, as some technical indicators suggest, these levels could still present an opportunity to reduce the position without incurring a loss and freeing up some money for other uses in the financial market.

Of course, a reverse scenario is also possible, in which Altius would benefit from rising commodity prices and other market conditions that would stimulate increased production. Achieving this requires two things: that there is no recession or that the global economy is at least slightly slowing down. It is also necessary that there are no other interest rate hikes nor inflation so that these can help to strengthen the demand for commodities and create a favorable environment for ever higher prices to form.

A further reduction in the number of favorable events comes from running multiple rate hikes in the past, as their cumulative effect on the economy has not yet fully unfolded. This is because the impact of a single monetary policy decision takes time to produce results.

From today's perspective, a bullish scenario has a very low probability of occurrence.

Altius Minerals Corporation shares are also traded on the Toronto Stock Exchange under the symbol (ALS:CA). Shares traded at CA$21.38 apiece for a market capitalization of CA$1.02 billion as of this writing. The stock has a 52-week range of CA$15.63 to CA$25.71. The shares are below the 75-day simple moving average line of CA$22.16, but well above the 200-day simple moving average line of CA$20. Also, the 14-day RSI comes in at 40.61, showing neither oversold nor overbought levels.

Conclusion

At current levels, which are not low, investors should consider selling some shares of Altius stock. This stock faces near-term headwinds from falling commodity prices and weak demand. Altius' royalty revenue is largely dependent on commodity prices and production rates at mine sites. With prices expected to trade lower and mining productions likely to be in the lower half of the predicted ranges, Altius' royalty income should not increase substantially in 2023, potentially impacting the stock price.

For further details see:

Altius Minerals Is Placed On The Sell List