GPRE - Alto Ingredients Growth Story Temporarily Lost In A 'Maize'

2023-05-02 14:05:00 ET

Summary

- Alto Ingredients is significantly undervalued, with shares trading at <1x 2026 EBITDA, <2x 2025 EBITDA, and <25% of tangible book value!

- Market completely overreacted to a Q4 (and year) full of extremely unusual one-time factors (Ukraine war, drought, lightning strikes, rail strikes, massive spikes in natural gas prices and corn basis).

- Elevated corn basis, natural gas, and freight is not permanent and is responsible for the market's massive blind spot in failing to recognize ALTO's successful transformation.

- ALTO has a clear path toward funding the CAPEX required to generate over $120M in incremental EBITDA by the end of 2026.

- My analysis suggests that shares should be valued at $10+ to $20+ by 2026-27 in worst-case/base-case scenarios with a 10x EBITDA multiple, but a 15x EBITDA multiple is certainly possible.

Introduction

Alto Ingredients (ALTO) represents a relatively straight-forward business: Converting corn into ethanol, with corn oil and protein (essential ingredients) as derivative products. But understanding ALTO's quarterly profits and expenses is apparently not so straight forward, as sell-side analysts frequently both under and over-estimate ALTO's quarterly earnings. Kingdom Capital recently wrote an update that did a fine job of explaining how ALTO underperformed his expectations; you'll find it of value to digest before reading my thoughts.

The article explains how Kingdom Capital's previous profit estimates were overly optimistic, breaking down many of the variables. He further concludes that, in a scenario where the company were to lose $20M a year on their current business (which he clarifies is not his actual estimate, only a hypothetical), ALTO may struggle to fund the projects they are planning to generate new revenue streams. I do want to discuss the current earnings outlook, but a primary intent of mine in this article is to show how I believe they can, in a very straight forward manner, fund these projects without dilution or a massive increase in financing.

It's my belief that the market simply doesn't understand why ALTO performed so poorly in 2022, misunderstanding the sheer range of cost impacts this past year, and the likelihood they will continue to be a headwind. Even Kingdom Capital's article under-emphasizes the impact of corn basis as the reason for ALTO's underperformance - mentioning basis only once. Since corn basis was the #1 factor impacting ALTO's results in 2022, responsible for the majority of the decline in profitability across ALTO's products, we are convinced of the importance of more clarity into this cost variable.

The market's failure to understand the drivers of ALTO's business has led to a significant overreaction to temporary operating conditions, which is in turn causing an unjustified fear for ALTO's liquidity, resulting in a valuation I believe to be substantially skewed.

I intend to address why ALTO underperformed margin expectations in 2022, and will share specifics on my conclusion that the company does not have CapEx liquidity concerns. Buckle-up! This is going to be a long and extremely detailed analysis; however, the full-read will be well worth your time.

Crush Margin vs Corn Basis

Understanding crush margin and corn basis is going to be a key part of understanding the economics behind ALTO's business.

It takes roughly 1 bushel of corn to make 2.8 gallons of ethanol. Since corn is the main input cost, the crush margin , in simple terms, is the relationship between the current cost of corn and the value of ethanol. For example, divide the CBOT price of corn by 2.8 and compare it to the CBOT price of Chicago ethanol - you will see whether fuel ethanol is currently at a positive or negative crush margin in Pekin, Illinois. As of May 1st, the crush margin for May is a positive $0.17 (July CBOT corn contract is at $5.844 , ALTO May basis (based off July contract) is at $0.42 , and CBOT price of Chicago ethanol for May is $2.41 ).

The price that ALTO pays for corn generally tracks the CBOT price of corn very well, with one exception, which is corn basis . Corn basis, again in simple terms, is the cash cost to have the corn delivered now. If corn is in high supply (such as at harvest time in the Fall) - the basis is often negative. If corn is not readily available, then the basis will be positive, which is an added cost for ALTO.

When calculating the crush margin, one must use the actual cash cost; therefore, tracking basis is very important.

This was just a primer - we'll be going into the weeds a little bit later to explain what "crushed" ALTO in 2022 and why ALTO's complete transformation has been lost in a "maize" (I promise - no more corny humor!).

I agree with Kingdom Capital that Q1, 2023 will result in an operating loss, but Q2 is already looking significantly better. For historical reference, April of 2022 averaged a 15-cent negative margin while April of 2023 has averaged a positive crush margin and ended the month at a $0.20 positive crush margin. Current 2023 May and June crush margins are also currently forecast to be higher than 2022, which combined with significantly lower freight/natural gas costs suggest that Q2 is likely to be profitable. But I am getting ahead of myself; let's first explore last year's operating results.

Part 1 - 2022 - What Went Wrong?

Seriously, what didn't go wrong? ALTO could just not catch a break in 2022...

Investors have to ask themselves - were the events of 2022 extraordinary and unlikely to repeat, likely to recur annually, or perhaps something in-between?

Let's examine the details of each quarter.

Q1:

The quarter started off as well as Q4 of 2021, with a crush margin over 20 cents the first week of January. That changed quickly, however, as Russian threats of invading Ukraine were taken more seriously and eventually became a reality on February 24, 2022. This event, in retrospect, ended up having a massively negative impact on the operating results of ALTO: It caused incredible volatility in oil, natural gas, and agricultural products such as corn and fertilizer (a key cost input in planting corn).

Almost immediately the price of corn moved higher, decimating the crush margin by 50 cents to a negative 30-cent margin by the end of the first quarter. The YOY spike in natural gas prices, a key input cost in ethanol production, also weighed heavily.

This table shows the year-over-year percent change in the price per therm of natural gas from ALTO's local utility in Pekin - Ameren Illinois :

| Natural Gas YOY % Change (Pekin) |

| 2021 |

| 2022 |

| 2023 |

| January |

| 4% |

| 124% |

| -8% |

| February |

| 6% |

| 142% |

| -17% |

| March |

| 26% |

| 112% |

| -30% |

| April |

| 198% |

| 6% |

| -47% |

| May |

| 203% |

| 9% |

| -53% |

| June |

| 208% |

| 26% |

| July |

| 204% |

| 32% |

| August |

| 201% |

| 37% |

| September |

| 178% |

| 33% |

| October |

| 162% |

| 40% |

| November |

| 129% |

| 19% |

| December |

| 102% |

| 11% |

Source: DOMO Capital Management, LLC; Ameren Illinois

With approximately 200 million gallons of ethanol produced in Pekin, the increased natural gas prices would have raised input costs by over $11M for the year with nearly $5M in Q1 alone given the much lower Q1 base in 2021.

Looking forward; however, note that while there will be some savings on natural gas in Q1 of 2023, the current rate for May, 2023 is down 53% YOY and also down 50% from just January! April and May of 2023 already provide YOY savings of nearly double the entire Q1 savings. If June's natural gas price matches May's price, Q2 natural gas savings should exceed $5M YOY!

Q2:

In Q2, freight costs doubled over Q1 as the price of crude also increased sharply. Higher freight impacted ALTO from an ethanol production standpoint as well as with the Eagle acquisition as existing contracts did not fully anticipate major changes in delivery costs.

Corn basis continued its sharp increase, as Ukraine was the world's 4th largest corn exporter and made-up over 15% of the world corn trade.

Rail interruptions started to impact the Western plants, and a lightning strike (really?) at the local utility in Pekin caused a $10M hit due to an unplanned power outage. What are the odds??!?

This was largely offset by a $10 million noncash lower of cost or market adjustment on ending inventories largely related to an unplanned power outage at our Pekin campus resulting from a lightning strike to the local utility.

ALTO did receive a $22.7M cash grant due to the impact from COVID. While many have been quick to point out the grant, few remember the impact of the lightning strike.

Net impact for Q2 is a $12.7M benefit to ALTO (grant minus lightning strike) minus higher freight and a massive increase in basis that we will quantify later. Also, in April, ALTO hit its high for the year of just over $7 a share.

Q3:

Supply chain restraints continued, and rail interruptions also became material with over six days of unplanned outages at ALTO's Western plants, which led to negative margins. The threatened train strike never occurred, but Union Pacific stopped accepting shipments of hazardous materials (such as ethanol) in early September to ensure that the cargo wouldn't be left on an unattended or unsecured train. The disruptions also prevented corn from reaching ALTO's facilities as ALTO is the single largest receiver of corn on the Union Pacific rail system.

Corn basis rose yet again during the quarter resulting in an additional $11M in costs YOY. This was due in part to the war, but even more-so because a severe drought hit the corn belt. June of 2022, for example, was the 3rd driest in 30+ years - if only the phrase, "when it rains, it pours" could have been literal instead of figurative! The drought caused the greatest decline in corn yield below the annual trend yield in more than 10 years.

And then, quite suddenly, freight costs rose again, for just Pekin this time, as barge prices started to skyrocket in September from $20 per ton to over $100 per ton (a 500% increase). Why? War in Ukraine? Nope: The Mississippi river simply dried-up…you just can't make this stuff up:

Spot Barge Rates Soar (Farmdocdaily)

As a somewhat separate side note, ALTO specifically calls out barge access via the Illinois River to the Mississippi River as one of their competitive strengths, enabling them to efficiently service international markets (specifically with essential ingredient sales).

Additionally, $3M of capital expenditures were expensed instead of capitalized, resulting in an immediate increase to COGS that hit in Q3. (It is worth parenthetically noting that this will increase profitability in future quarters, since the expense will have neither depreciation nor amortization.)

Q4:

High corn basis and freight costs continued, and barge pricing stayed extremely high through year-end, but Q4 got even more interesting...

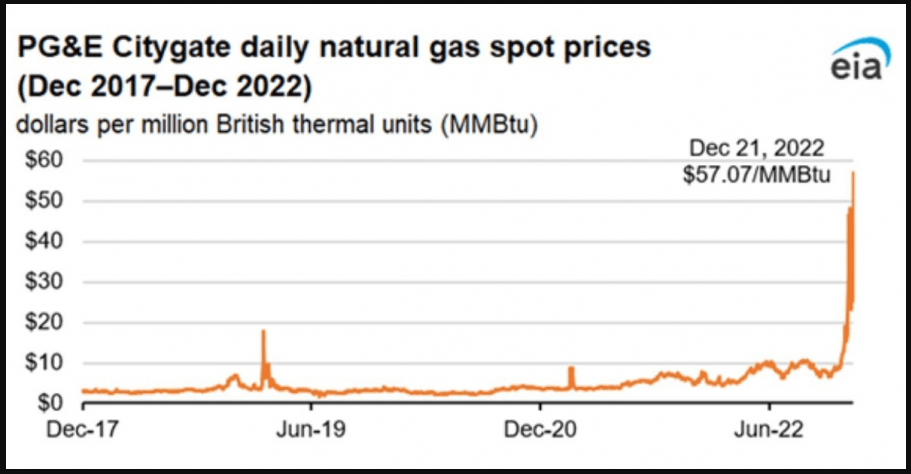

Suddenly, natural gas prices in the western region soared to TWENTY YEAR HIGHS in December and reached levels 400% higher than Q3 prices, reaching a high of $57.07/MMBtu on December 21st :

Natural Gas Soars to Twenty Year High (EIA)

{kind=link}

It takes about 0.3111 therms of natural gas to produce a gallon of ethanol. ALTO's production capacity in OR and ID is 100M gallons of ethanol/year, or 8.3M gallons/month, requiring about 2.6M therms of natural gas per month. A 400% increase in the price of natural gas, for just a single month, would result in an $11M+ cost increase. As production was significantly moderated at these facilities, the actual impact, while still painful and material, was probably closer to $5M for the quarter.

2022 Summary

2022 brought the invasion of Ukraine which resulted in an overall spike of corn, oil, and natural gas prices (and thus corn basis due to decreased supply), a lightning strike to a local utility, a severe drought along the corn belt that further increased corn and corn basis and also dried-up the Mississippi River leading to massive increases in barge rates, unplanned shutdowns due to a potential rail strike (you will recall that both Congress and Biden intervened), and natural gas spikes in the West to twenty-year highs, unrelated to Ukraine.

Wouldn't you agree that the majority of these items fall into the "extraordinary and unlikely to repeat" category?

I want to dig deeper into the impact of corn basis, natural gas, and freight costs, as these (other than the 4th quarter incident) have been less defined yet are perhaps the most material.

Quantification of Corn Basis/Other Costs

| Year |

| Gallons Produced |

| Bushels Required |

| Avg Corn Cost |

| Corn Cost per Bushel |

| Average Basis |

| Basis per Bushel |

| Delivered Cost of Corn |

| Total Corn Cost |

| 2022 |

| 300M |

| 107.1M |

| $6.92 |

| $741.4M |

| $0.85 |

| $91.1M |

| $7.77 |

| $832.5M |

| 2021 |

| 251.7M |

| 89.9M |

| $5.70 |

| $512.4M |

| $0.52 |

| $46.7M |

| $6.22 |

| $559.1M |

| 2020 |

| 262.1M |

| 93.6M |

| $3.56 |

| $333.2M |

| $0.28 |

| $26.2M |

| $3.84 |

| $359.5M |

| 2019 |

| 494.6M |

| 176.6M |

| $3.83 |

| $676.5M |

| $0.43 |

| $76.0M |

| $4.26 |

| $752.5M |

| Total Corn Cost |

| COGS (Pekin & Other Production) |

| Corn Cost as % of COGS |

| Dollar Cost of Other COGS |

| $832.5M |

| $1,126.5M |

| 73.9% |

| $294.0M |

| $559.1M |

| $774.8M |

| 72.2% |

| $215.6M |

| $359.5M |

| $595.5M |

| 60.4% |

| $236.1M |

| $752.5M |

| $1,093.3M |

| 68.8% |

| $340.8M |

*Source Alto Ingredients 10-Ks and DOMO Capital Management, LLC

I apologize for the above format, as I was forced to put the data into two separate tables.

Using ALTO's 10-K's, we can separate the cost of corn as an input from other costs, and we can also specifically separate out the basis cost.

Bushels required assumes 2.8 bushels of corn for every gallon produced (ex. 300M gallons / 2.8 bushels = 107.1M bushels of corn).

There are two takeaways from this table:

First, it's all about that basis, 'bout that basis , as the increase in basis in 2022 was extreme and unexpected. Typically, basis in the 4th quarter is negative, not positive, and certainly not close to a dollar!

In the 3rd quarter, ALTO highlighted that corn basis added $11M in cost; however, the worst of it was actually in Q4 where basis doubled from $0.49 in 2021 to $1.01 in 2022! The only place to see this is on the press release - you won't find the detail in the 10-K. Therefore, in Q4 alone, the increased basis impact was closer to $15M!

If ALTO had paid 2021 level corn basis multiplied by 2022 production levels, corn basis would have been $56.7M ($0.52 * 107.1M bushels) instead of the $91.1M they actually paid. While ethanol prices tend to track corn prices over time, they do not track changes in corn basis which is specifically why it's so important to understand the magnitude of the impact that corn basis had on the ethanol industry in 2022.

Increased corn basis added $34.4 million in costs for ALTO in 2022!

Second, the dollar value of other costs rose from $215.6M to $294M - an increase of about $78M. Some of this increase is a result of the fact that Magic Valley was open for the entire year (Magic Valley was restarted in November of 2021) which explains most of the additional 48.3M gallons of fuel ethanol produced. However, most of the increase of these other costs is due to the increases in freight costs and natural gas, which can be deduced by examining cost per gallon produced:

In 2022, the cost of other COGS totaled $0.98M per gallon, while in 2021 the cost of other COGS was $0.86M per gallon. Applying the 2021 rate to the 2022 production of gallons (just as we did with corn basis) shows that the cost of other COGS, adjusted for the production increase, rose by $37M over 2021 ($294M minus $257M). It is not unreasonable to conclude that a substantial portion of this increase is attributable to the increased costs associated with the various incidents we have identified.

2023 Expectations

Let's review the biggest impacts from 2022:

Corn Basis: ~$34M

Natural Gas increases: ~$20M

Lightning Strike: ~$10M

Rail Interruptions at Western Plants: Unknown, ~$5M-$10M

Freight (truck/barge): Unknown, ~$5M-10M

December Natural Gas spike in West: ~$5M-10M

ALTO lost $61.4M from operations in 2022 ( excluding the benefit of the cash grant) vs a $40.1M profit in 2021. A review of the above costs plus consideration of $3.5M in temporary SG&A due to the Eagle acquisition and a $3M increase in COGS from uncapitalized CapEx gets you pretty close to the $100M swing in profitability.

I would make the argument that large portions of the above costs are unlikely to reoccur and/or are likely to materially decline in 2023:

Lightning never strikes twice in the same spot, right?!

Railroad labor issues have been resolved by Congress.

Freight costs should be down significantly YOY.

The Mississippi river water levels have substantially risen due to a very wet winter and drought is not in the forecast for 2023 ( Iowa had the wettest December in 150+ years! ) - this will not only ensure normalized barge rates later in the year, but will also help moderate basis as the 2023 corn yield expectations continue to rise.

Natural gas prices were still 50% to 110% higher in Q1, 2023 vs Q1, 2021 (despite being down about 18% YOY vs 2022); however, starting in April, natural gas prices are down 43% to 48% vs 2021 as well as down 44% to 49% YOY. Therefore, once we get beyond Q1, investors can expect a material decline in input costs.

2022 was an extreme year. It won't repeat, in our view, but it may well be challenging the market's ability to understand and appreciate the totality of ALTO's transformation.

A better way to visualize the transformation that has already occurred may be through this one graphic from ALTO's 10-K :

Alto Ingredients 10-K (Alto Ingredients)

{kind=link}

In 2020 - ALTO's entire gain was wiped out by $18M in annual interest. In 2022, interest expense was under $2M.

Over the last three years, ALTO paid off $173M in debt (this includes the recent increase in debt from the $59.1M Orion term loan draw in Q4 of 2022) while also spending over $80M in capital expenditures (including the acquisition of Eagle and uncapitalized CapEx). Only ~36% of the ~$250M in debt payoff / CapEx was funded via issuance of stock and warrants that generated proceeds of ~$90M. These offerings, in 2020, ended-up resulting in ~15.8M shares of dilution as the warrants to purchase an additional ~9M shares (sold to CVI Investments for ~$58,000) expired unexercised last year.

Yet - despite this remarkable transformation - the market continues to doubt a conservative and non-promotional management team's ability to execute.

Will more dilution or financing be required?

Part 2 - Project Cost & Cash Flow Analysis

Digging through the company's most recent presentation (which has provided the most detail yet on future CapEx) as well as through the quarterly transcripts for the last couple of years has allowed me to generate a roadmap for how the company will fund future CapEx.

First - here is a list of projects that recently completed or that will start and end over the next 3 years:

| Project |

| Costs |

| Cost Start Date |

| Expected Completion Date |

| Cash Flow Start Date |

| Annual Cash Flow |

| Eagle Acquisition |

| $14M + 3.5M as SG&A paid in '22 ($5.5M SG&A remaining) |

| Q1, 2022 |

| Q4, 2024 (for additional SG&A costs) |

| Q1, 2023 |

| $5M |

| Corn Silos |

| $6M - Paid in '22 |

| Q1, 2022 |

| Q1, 2023 |

| Q2, 2023 |

| $2M |

| Magic Valley Corn Oil |

| $4.5M - Paid in '22 |

| Q1, 2022 |

| Q3, 2023 |

| Q2, 2023 (whenever Magic Valley restarts) |

| $4.5M |

| Magic Valley Protein |

| $13M Total - $9.5M Est. Paid in '22 |

| Q3, 2022 |

| Q3, 2023 |

| Q4, 2023 |

| $4.5M |

| High Quality GNS |

| $5M - Paid in '22 |

| Q1, 2022 |

| Completed |

| Q1, 2024 |

| $5M |

| GNS Tote/Drum Packaging & Distribution |

| $4M - Paid in '22 |

| Q1, 2022 |

| Completed |

| Q1, 2024 |

| $4M |

| High Efficiency Boilers |

| $3M Est. paid in '22 |

| Complete |

| Q1, 2024 |

| Q2, 2024 |

| $1.5M |

| Natural Gas |

| $9M |

| Q2, 2023 |

| Q2, 2024 |

| Q3, 2024 |

| $3M |

| ICP Corn Oil |

| $6M |

| Q4, 2023 |

| Q3, 2024 |

| Q4, 2024 |

| $6M |

| Pekin Corn Oil |

| $6M |

| Q1, 2024 |

| Q4, 2024 |

| Q1, 2025 |

| $4.5M |

| Columbia Corn Oil |

| $6M |

| Q2, 2024 |

| Q1, 2025 |

| Q2, 2025 |

| $3M |

| ICP Protein |

| $14M |

| Q3, 2024 |

| Q1, 2025 |

| Q2, 2025 |

| $6M |

| Yeast |

| $40M Est. |

| Q1, 2024 |

| Q3, 2025 |

| Q4, 2025 |

| $19M for first 12 months then $25M a year. |

| Carbon Sequestration Compression |

| $100M Est. |

| Q1, 2023 |

| Q1, 2026 |

| Q2, 2026 |

| $30M Net in 45Q Credits |

| Co-Generation |

| $25M Est. |

| Q2, 2024 |

| Q1, 2026 |

| Q2, 2026 |

| $15M |

| Pekin Protein |

| $14M |

| Q2, 2026 |

| Q4, 2026 |

| Q1, 2027 |

| $4.5M |

| Columbia Protein |

| $14M |

| Expect to be delayed to 2027 or beyond. |

| Delayed |

| Delayed |

| $3M |

Source: DOMO Capital Management, LLC

Project Notes:

This table is fairly conservative. In most cases, the start date of the cash flows is a full quarter out from the quarter of completion in order to help anticipate any sort of delays.

The Eagle acquisition was $14M, but it included $9M in cash incentives after three years. ALTO is accruing for these annually within SG&A. $3.5M was accrued in 2022, and I expect another $3.5M and then $2.5M to be accrued in 2023 and 2024.

Magic Valley cost ~$17.5M to install the corn oil/protein (based on previous earnings transcripts), but I conservatively assumed the other plants will cost $20M due to inflation. This may be a false assumption and the total may not have materially changed.

One extremely important piece of information is the fact that the corn oil implementation yields the same benefit as the protein implementation but totals only about 25%-30% of the total project cost . Therefore, the corn oil installation costs ~$6M per plant vs ~$14M for the protein installation.

Natural gas benefit does not include renewable natural gas. RNG may be a separate project cost / benefit - as more information is needed from management.

The Pekin-ICP plant has 50% more capacity than Magic Valley while the Columbia plant has about 67% less capacity. Therefore, I expect Pekin-ICP to be implemented first to get the most benefit per cost. Further, given the relatively high cost of $14M at Columbia for just a $3M annual gain on protein, I make the assumption that ALTO will eventually decide to delay the protein installation at Columbia until all other projects are complete.

Carbon sequestration is a large range - hopefully we'll have much greater detail within weeks. The upside is much greater than just the $30M in 45Q credits that management quantified as sequestration will allow ALTO to generate additional income/margin from blue ethanol and sustainable aviation fuel of which the benefit is not yet included in any projections. More importantly, additional CapEx isn't required to benefit from these additional revenue streams that carbon sequestration creates.

In my opinion, the management team had an unenforced error by listing the carbon sequestration credits at $30M annually. The $30M is the net amount expected after all costs, such as connecting to a pipeline. I believe that management gave the market the impression that the proceeds are only $30M (instead of the actual $60M figure) and the market assumed that there were then additional costs on top of that.

By using the above project table, a roadmap of anticipated costs and cash flows can be created, because it must be acknowledged that as these projects come online, the associated cash flows can be used to fund additional projects.

| *All numbers in millions |

| Quarter, Year |

| Project CapEx |

| Project Cash Flows |

| Quarterly Project CapEx less Project Cash Flows |

| Running Total of Cash Outlays less Project Cash Flows |

| Q1, 2023 |

| $4.375 |

| $1.25 |

| -$3.125 |

| -$3.125 |

| Q2, 2023 |

| $3.125 |

| $2.875 |

| -$0.25 |

| -$3.375 |

| Q3, 2023 |

| $8.125 |

| $2.875 |

| -$5.25 |

| -$8.625 |

| Q4, 2023 |

| $4.625 |

| $4.00 |

| -$0.625 |

| -$9.25 |

| Q1, 2024 |

| $10.75 |

| $6.25 |

| -$4.50 |

| -$13.75 |

| Q2, 2024 |

| $18.125 |

| $6.625 |

| -$11.50 |

| -$25.25 |

| Q3, 2024 |

| $27.795 |

| $7.375 |

| -$20.42 |

| -$45.67 |

| Q4, 2024 |

| $31.295 |

| $8.875 |

| -$22.42 |

| -$68.09 |

| Q1, 2025 |

| $34.285 |

| $10.00 |

| -$24.285 |

| -$92.375 |

| Q2, 2025 |

| $13.125 |

| $12.25 |

| -$0.875 |

| -$93.25 |

| Q3, 2025 |

| $13.125 |

| $12.25 |

| -$0.875 |

| -$94.125 |

| Q4, 2025 |

| $23.125 |

| $17.00 |

| -$6.125 |

| -$100.25 |

| Q1, 2026 |

| $23.125 |

| $17.00 |

| -$6.125 |

| -$106.375 |

| Q2, 2026 |

| $4.67 |

| $28.25 |

| $23.58 |

| -$82.795 |

| Q3, 2026 |

| $4.67 |

| $28.25 |

| $23.58 |

| -$59.215 |

| Q4, 2026 |

| $4.66 |

| $29.75 |

| $25.09 |

| -$34.125 |

| 2027 |

| $123.50 |

| $123.50 |

| $103.70 |

Source: DOMO Capital Management, LLC

A reference table is provided at the very end of the article that shows exactly what projects are included in each quarters project CapEx and cash flow projections.

Additional Assumptions:

Assumed $3.5M in Q1, 2023 towards installing protein at Magic Valley in Q1. This figure could be closer to zero.

Assumes zero spot sales of GNS during 2023 in project cash flows, which seems extremely unlikely.

Nearly all projects were broken down into even increments across each quarter.

Yeast costs are unknown and could be more or less than $40M, but I believe this number is in the ballpark. With a yeast project, the majority of costs will be back-end weighted (for the dryers, etc.); therefore, assumed $5M a quarter for 3 quarters, followed by $10M, and then $15M.

Carbon Sequestration costs of $100M and Co-Generation costs of $25M could also be more or less but this should again be in the ballpark.

Carbon Sequestration costs will be almost non-existent until 2nd half of 2024 (based on discussions with management). I assumed $5M of cost in Q3, 2023 and Q2, 2024 followed by $10M a quarter for 5 quarters starting in Q3 of 2024, and then $20M a quarter for 2 quarters starting in Q4 of 2025.

It is possible, perhaps even likely, that some of the revenue streams may come online before the timeline suggested by this roadmap given the conservative assumptions that were applied.

Liquidity Questions Extremely Overblown

The project roadmap provided above shows us that ALTO will need only need, at most, a total of $106.5M of cash to fund the CapEx through 2025 (once taking into account project cash flows), and that starting in 2026, the company will begin generating an additional $25M and then $30M+ of income per quarter.

The company currently has $36M in unrestricted cash, $58M in excess on the line of credit, and $65M available from Orion (including the additional $25M option) which totals $159M or a sum of $52.5M in excess of the greatest amount of project cash outlays less proceeds required (~$106.5M by end of Q1, 2026). Just enough to utilize the entire share repurchase authorization!

In Kingdom Capital's hypothetical example where he has ALTO losing $20M a year for the next 3 years on the current business - ALTO would end Q4, 2025 with an ~$1.5M deficit with another $6M in cash requirements before generating quarterly cash flow of $23M+ in Q2, 2026 and beyond. Would this ~$8M deficit require additional financing or dilution?

Nope, because we haven't even discussed working capital yet!

ALTO has a positive working capital position of $121.1M, and if we exclude the $36.5M in cash that we've already included in current liquidity there is still a positive working capital position of $84.6M!

This means that ALTO's current assets ( excluding unrestricted cash ) exceed current liabilities by ~$85M. In other words, if necessary, the company could easily decrease working capital for a quarter or two to complete any projects that they deem necessary. Including working capital, the company has >$137M in excess liquidity to fund all of their projects. I am under no illusion that the company would take their working capital position down to $0, but it certainly provides considerable wiggle room with the knowledge that $23M+ a quarter of positive cash flow begins in Q2 of 2026 (if not earlier).

In fact - let's compare ALTO's working capital to one their largest competitors - Green Plains ( GPRE ). GPRE has a working capital ratio of 1.91 compared to ALTO at 2.55 (current assets / current liabilities). If we assume ALTO uses the entire $36.5M of unrestricted cash, that would put ALTO's working capital ratio at 2.08 ($162.7M in current assets, less unrestricted cash, divided by current liabilities of $78M) - still materially ahead of GPRE. To arrive at a working capital ratio of 1.91, we can utilize all of ALTO's $36.5M in unrestricted cash, plus an additional $13.7M of the current working capital (through either reductions in current assets or by allowing current liabilities to rise).

In short - ALTO could easily engineer the necessary $8M of liquidity from their current working capital position and still have a better working capital ratio than one of their largest competitors.

Now - what if the current business earns $20-30M a year instead of losing $20M? Or perhaps loses $20M in 2023 due to a rough first quarter only to generate $20-$30M a year after that point? Suddenly, the company's remaining $48M availability to repurchase shares starts to look very enticing. Afterall, the heavy cash requirements don't even begin until Q2 of 2024. It is incredible that ALTO has a share repurchase plan authorization that would currently allow them to purchase nearly half the company!

Liquidity is not an issue!

Is ALTO likely to dilute shareholders to raise cash?

No! they are more likely to repurchase shares than to issue shares. Frankly, it may even make sense to delay some projects to do just that!

Is ALTO likely to raise additional debt?

Yes!

There is a difference between what may be required and what is prudent and while the scenario laid out above is conservative, an unforeseen event (which is possible given 2022) could have a material impact.

Therefore, ALTO should raise an additional $50M to $100M in debt as soon as possible in order to be able to proceed with certainty on carbon sequestration and co-generation. Another option would be to partner-up on carbon sequestration and forego some of the $30M in EBITDA.

The company should pursue the debt option, because if the current business is able to earn $20M to $30M or even break-even, then it would allow ALTO to stop taking additional draws from the Orion term loan where the interest is only applied once a draw is taken and/or would allow them to pay back the loan early. Even better - an improvement in operating results would give the board of directors and management more incentive and confidence to aggressively repurchase shares.

The market will catch-on eventually; therefore, the question really becomes - how does the market value ALTO by the end of 2026 once it is on the verge of increasing its earnings power by over $120M annually?

Part 3 - Valuation

By 2026, ALTO's current business will still likely average $30M a year with the potential to lose $20M in a bad year ($40M in an extremely bad year) and to earn over $50M in a great year. The new revenue streams will be generating over $120M annually and the probable material increase in specialty alcohol volumes ( we didn't even touch on this ) will raise the floor in bad years and the ceiling in good years. Additionally, the company will still have additional EBITDA growth opportunities with blue ethanol and sustainable aviation fuel becoming possible, at no additional CapEx cost, once carbon sequestration is implemented.

GPRE had negative adjusted EBITDA in 2022, but in 2021 they had $87.4M in adjusted EBITDA (adjusting out a gain on the sale of an asset). At a price of $33, GPRE currently trades at an ~$2B market cap or ~23x Adjusted EBITDA (or ~25x using $2.2B enterprise value)

ALTO had adjusted EBITDA of $76.8M in 2021 and at a price of $1.30 trades just under a market cap of ~$100M or a 1.3x multiple to Adjusted EBITDA (or 1.9x using $148.5M enterprise value).

The relative value differential makes no logical sense, especially given the fact that ALTO has actually been the better operator.

I believe that by the end of 2026, ALTO will be trading at a valuation of at least 10x 2027 EBITDA. The company will be in a position to pay-off all of their outstanding debt by the end of 2027, if they want to, and will be earning anywhere from $80M in EBITDA in an extremely bad year to $170M EBITDA in a good year with a base case of about $150M EBITDA annually.

With 75.1M shares outstanding (assuming they don't repurchase any shares) and a 10x EBITDA multiple - the market can choose whether to value ALTO as though extremely bad years will happen annually (unlikely) or with the expectation that either bad/average/good years will happen annually.

Here are the scenarios:

Extremely Bad Year: $80M EBITDA = $800M Market Cap = $10.7/share

Bad Year: $100M EBITDA = $1B Market Cap = $13.3/share

Average Year: $150M EBITDA = $1.5B Market Cap = $20/share

Good Year: $170M EBITDA = $1.7B Market Cap = $22.6/share

One thing is clear - with a tangible book value of ~$4 per share - ALTO is extremely undervalued by any metric! GPRE has a tangible book value of only $14.55 - ALTO would need to trade over $9 per share to match this valuation!

Risks

The greatest risk to my thesis would be a sustained environment, similar to Q4 of 2022, where fuel ethanol prices sharply decline while corn, basis, and natural gas prices increase in value. While this would lead many ethanol plants to curtail / idle ethanol production to stabilize the price of ethanol, it is still a risk. In short - a sustained period of an extremely negative crush margin would materially, negatively impact ALTO.

Other risks:

- A sharp decline in specialty alcohol sales and/or the inability to lock prices in at a premium to renewable fuel.

- If the items that impacted 2022 results are, in-fact, not extraordinary and repeat (lightning strikes, railroad strikes, natural gas spikes, drought).

- Any sort of event that would cause an outage at one of ALTO's ethanol plants. Green Plains just had one of their largest plants explode .

- Any future laws that would limit the benefit of carbon sequestration and/or decrease the use of ethanol as a renewable fuel.

- A material increase in expected CapEx for projects and/or a material delay in the completion date of projects.

Conclusion

In conclusion, I believe it is clear that many of the factors that impacted 2022 results will not impact 2023 results. Furthermore, some of the stickier problems (such as corn basis) show signs of moderating year-over-year due to a strong projected corn harvest. The corn harvest even has the potential to get more bullish if El Nino comes to fruition as this analyst notes :

I also ran simulations based on yields in the 15 El Nino summers experienced in the U.S. since 1950. Based on trends in those years, U.S. yields averaged 186.5 bushels per acre, compared to 179.4 in all years. The higher yields also depressed prices. The average cash price in the simulations for El Nino summers was $4.58, compared to $4.97 in the all-years runs.

If the Russian / Ukraine war comes to an end, to which we assign no probabilities, it would greatly benefit ALTO. More corn would enter the global market via Ukraine, fertilizer costs would decrease, and farmers would plant more corn, even at lower prices, due to the lower input costs. That aside, Ukraine has already completed a project that has substantially widened the Bystre canal that links it to the River Danube greatly increasing the amount of corn that can be transported out of the country.

When analyzing ALTO's liquidity and expected CapEx outlays - one must consider the subsequent cash flows as projects come online as well as understand that a project doesn't incur all of its costs on day one. Most importantly, ALTO can reap half of the benefits of the CoPromax installations after about just 25%-30% of the total project cost since corn oil provides half the benefit.

ALTO does not have a liquidity problem. In-fact, if fuel ethanol margins simply break-even as corn basis normalizes and natural gas continues to stay low then the opportunity for ALTO to utilize the remaining $48.7M share repurchase authorization increases dramatically. In-fact, based on the ROI of the protein project at Columbia, the company would be better off prioritizing $14M in share repurchases as opposed to starting the protein project in the scenario where fuel ethanol margins stabilize.

By the end of 2026, even if the market assumes that fuel ethanol will have a horrible year, indefinitely, my analysis suggested that ALTO should still be valued over $10 per share. The odds of a valuation over $20 per share are much more likely; however, and with full clarity of all of the projects coming online and producing cash flow the prospects of an EBITDA multiple exceeding 15x increases significantly which would put the shares over $30.

The future for ALTO is bright. The market will have to get past another uninspiring quarterly report in May, and might continue to ignore the company's guidance. Or - maybe the company will make it clear how the operating environment has significantly improved since 2022 and the first quarter, provide even greater clarity on CapEx and carbon sequestration, and provide confidence to the market that the company will not repeat 2022's performance as several one-time issues are unlikely to reoccur.

Project Reference Table

| Quarter, Year |

| Cost Projects |

| Cash Flow Projects |

| Q1, 2023 |

| Eagle, Magic Valley Protein |

| Eagle |

| Q2, 2023 |

| Eagle, Natural Gas, ICP Corn Oil |

| Eagle, Corn Silos, Magic Valley Corn Oil |

| Q3, 2023 |

| Eagle, Natural Gas, ICP Corn Oil, Pekin Corn Oil, Compression ($5M) |

| Eagle, Corn Silos, Magic Valley Corn Oil |

| Q4, 2023 |

| Eagle, Natural Gas, ICP Corn Oil, Pekin Corn Oil |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein |

| Q1, 2024 |

| Eagle, Natural Gas, ICP, Corn Oil, Pekin Corn Oil, Columbia Corn Oil, Yeast ($5M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution |

| Q2, 2024 |

| Eagle, Pekin Corn Oil, Columbia Corn Oil, Yeast ($5M), ICP Protein, Co-Generation, Compression ($5M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers |

| Q3, 2024 |

| Eagle, Columbia Corn Oil, Yeast ($5M), ICP Protein, Co-Generation, Compression ($10M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil |

| Q4, 2024 |

| Eagle, Columbia Corn Oil, Yeast ($10M), ICP Protein, Co-Generation, Compression ($10M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil |

| Q1, 2025 |

| Yeast ($15M), ICP Protein, Co-Generation, Compression ($10M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil |

| Q2, 2025 |

| Co-Generation, Compression ($10M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil |

| Q3, 2025 |

| Co-Generation, Compression ($10M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein |

| Q4, 2025 |

| Co-Generation, Compression ($20M), Pekin Protein |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast |

| Q1, 2026 |

| Co-Generation, Compression ($20M) |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast |

| Q2, 2026 |

| Pekin Protein |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast, Carbon Sequestration, Co-Generation |

| Q3, 2026 |

| Pekin Protein |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast, Carbon Sequestration, Co-Generation |

| Q4, 2026 |

| Pekin Protein |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast, Carbon Sequestration, Co-Generation, Additional Yeast |

| Full Year 2027: |

| None |

| Eagle, Corn Silos, Magic Valley Corn Oil/Protein, GNS, Tote/Drum Packaging & Distribution, Boilers, Natural Gas Bypass, ICP Corn Oil, Pekin Corn Oil, Columbia Corn Oil, ICP Protein, Yeast, Carbon Sequestration, Co-Generation, Additional Yeast, Pekin Protein |

Source: DOMO Capital Management, LLC

For further details see:

Alto Ingredients Growth Story Temporarily Lost In A 'Maize'