ALTO - Alto Ingredients Has To Prove It Can Execute On Its Strategy

Summary

- Over the last decade, the company has never been able to generate consistent, sustainable growth.

- After a weak quarter and increased expenditures, the company must prove it can execute on its strategy.

- With the available capital to advance its initiatives, I think the company is now in the position of having to deliver the goods.

Alto Ingredients ( ALTO ), a company that produces and markets specialty alcohols and essential ingredients in the United States, has struggled to find momentum and support, as it has traded in a wide range, with primary tendency to move consistently down rather than up with its share price.

Looking at a 10-year chart, you can get a clearer look at the price movement of the stock as it reflected the company's performance over time. At its low point over the last decade, it traded at approximately $0.15 per share in March 2020, and from there made a big upward move to about $11.50.

From that time, it has traded choppy on a consistent downward trend, reaching its 52-week low of $2.61 on December 29, 2022, before starting a modest rebound. Based upon its historical performance, it's anyone's guess as to whether or not it'll find support.

In this article, we'll look at some of the weak numbers from its latest earnings report, whether or not it has the legs to sustainably grow, and what the long-term outlook for the company looks like.

{kind=link}

Some of the latest earnings numbers

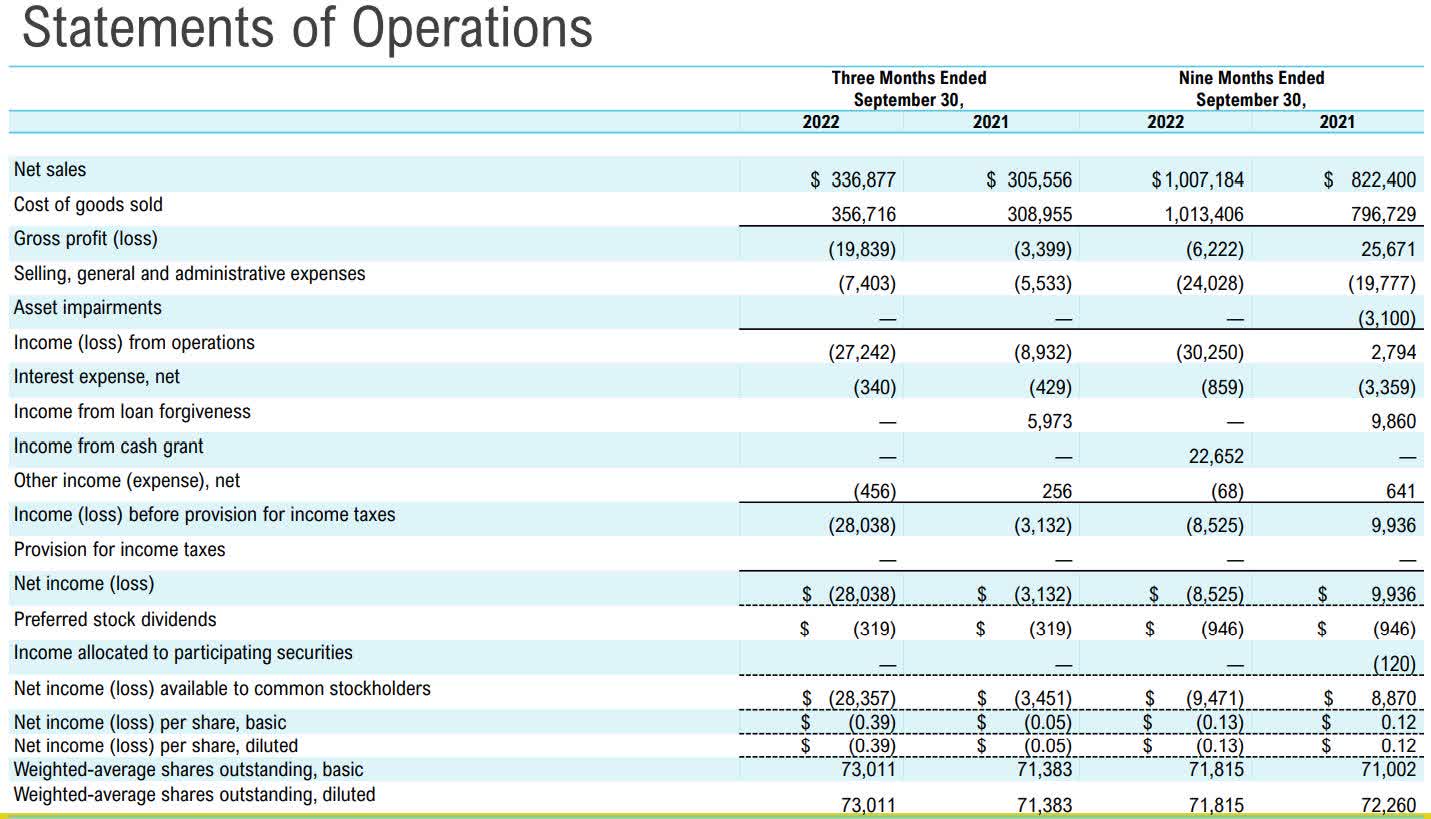

Revenue in the third quarter was $336.9 million, compared to revenue of $305.56 million in the third quarter of 2021. Revenue in the first nine months of 2020 was $1 million, compared to $822.4 million in the first nine months of 2021.

Gross loss in the reporting period was $(19.8) million, compared to a gross loss of $(3.4) million in the third quarter of 2021. Gross loss for the first nine months of 2022 was $(6.2) million, compared to a gross profit of $25.7 million in the first nine months of 2021.

{kind=link}

Net loss in the third quarter was $(28.4) million, or $(0.39) per diluted share, compared to a net loss of $(3.5) million, or $(0.05) per diluted share in the third quarter of 2021.

Adjusted EBITDA in the third quarter was negative $(20.6) million, compared to adjusted EBITDA of $3.0 million in the third quarter of 2021.

Cost of goods sold jumped to $357 million, up from $309 million in the third quarter of 2021. That was attributed to higher delivery costs, logistical and service disruptions, and charges connected to the uncapitalized portion of infrastructure upgrades.

At the end of the third quarter of 2022 the company held $28.5 million in cash and cash equivalents, compared to $57.4 million in cash and cash equivalents it had at the end of June 2022. I has long-term debt (net of current portion) of $45.88 million.

In the reporting period the company entered into a new six-year term loan facility of up to $125 million, which includes the flexibility of periodic draws up to $100 million, and another $25 million if the company satisfies certain conditions.

The strategy

Some of the major reasons for the poor performance were the shutdown of its ICP facility, low commodity margins, logistical and supply chain constraints, and a record corn basis. Corn basis refers to the difference between the local cash price at the time and the futures price of the contract related to the closest delivery month.

In order to mitigate some of these issues and improve the top and bottom lines, the company has initiated several projects as part of its strategy for the future.

Expanding storage

One of the steps ALTO's taking to mitigate logistical and supply chain issues is to expand its storage capacity in Illinois. The doubling of its storage capacity will allow the company to hold more corn reserves during difficult conditions related to winter weather, holiday periods, and when there are issues with the supply chain.

The company believes by increasing its storage capacity it'll lower the volatility associated with input costs.

CoProMaX system

Management announced that at its Idaho plant it had completed the first phase of its CoProMaX system. What it does is boost the amount of corn oil it can extract. The results of the initiative is the yield has significantly grown upon completion of the first phase.

Now that yield has met expectations, the company is going to expand the system to its other dry mills.

The next phase is to of the project is projected to be completed in the first quarter of 2023, and when completed will focus on separating enhanced protein. If results are positive there, the company will deploy it to other places.

Specialty alcohol

The other major project the company has been working on is upgrading equipment at its wet mill during the third quarter. The new equipment has been delivered and the upgrades are expected to be fully operational in the first quarter of 2023.

Upon completion the company says it'll "provide production redundancy, providing surety of supply to our customers and enable us to improve our product mix and capture higher premiums in the alcohol value chain."

Concerning specialty alcohol contracts in 2023, management says it believes it will be able to maintain and grow share with its current customer base, and once its Pekin GNS production system improvements are online, they expect to attract new business in its beverage category.

Adding it all up together, ALTO believes with the available funding from its new term loan, it'll be able to leverage the improvements in its specialty alcohol and essential ingredient products to further diversify its offerings.

Potential impact on its performance

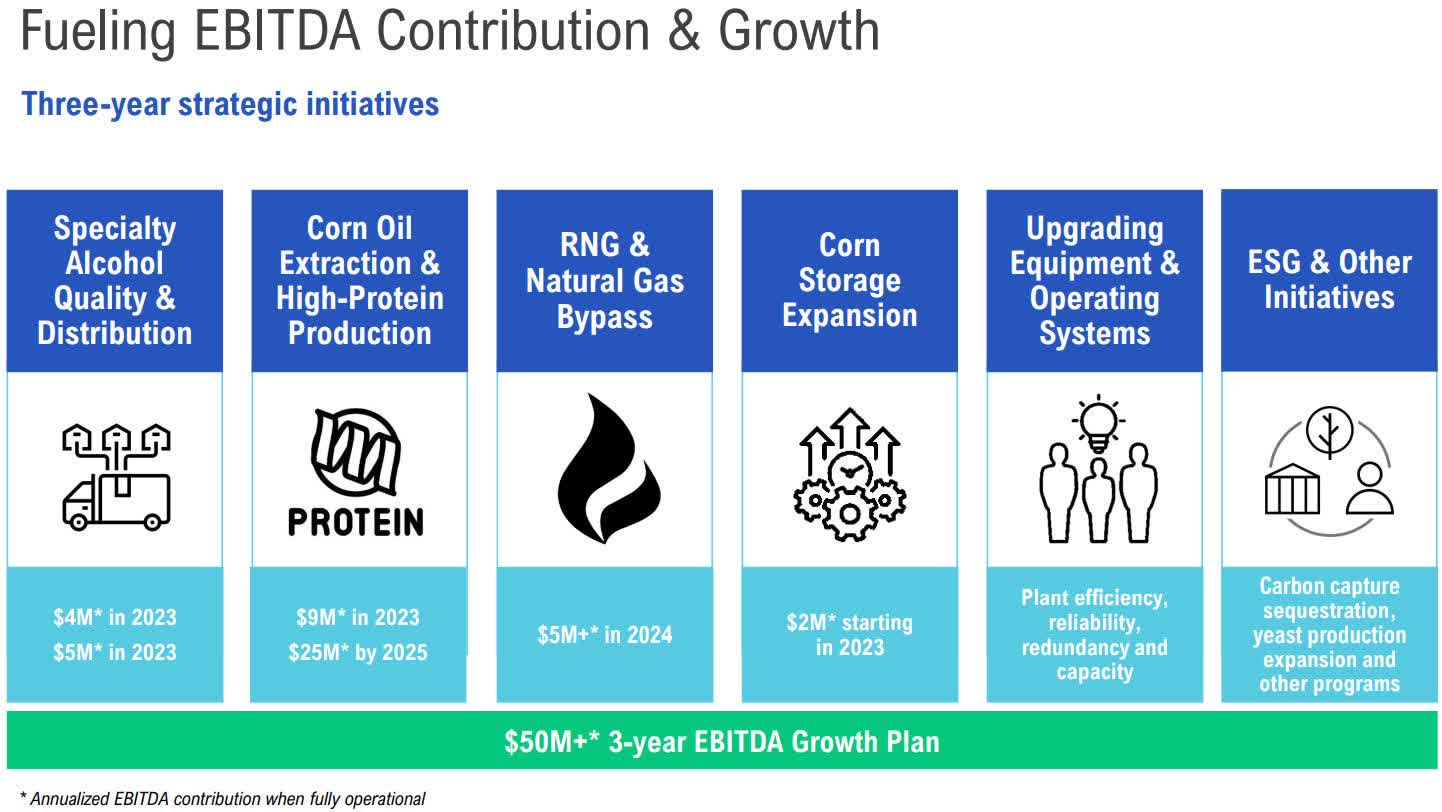

Based upon the investments in the various projects, ALTO projects that by the end of 2023 it will boost EBITDA by over $20 million, adding another $30 million in EBITDA on an annual basis by 2025. It also stated that this doesn't include other projects that are currently under development, such as "primary used expansion and carbon capture and sequestration."

The largest contributor to EBITDA growth will be corn oil and extraction and high-protein production, which is expected to add $9 million in EBITDA in 2023, and $25 million by 2025. This is the key category to watch as it's expected to contribute over half of the EBITDA growth associated with the company's strategy over the next three years.

The other major contributor in the short term will be specialty alcohol, which is estimated to add $4 million EBITDA in 2023. Corn storage expansion is projected to add $2 million in EBITDA in 2023.

RNG and natural gas bypass is expected to add another $5 million+ in EBITDA in 2024.

{kind=link}

Conclusion

Over the last decade, ALTO hasn't been able to consistently and sustainably grow the company. It has had periods of time when it looked like it could, but after a period of an upward movement in its share price, it has entered into prolonged periods of decline.

Based upon its recent quarter and its poor performance, and the capital it is allocating across very parts of the company, I see it as a crucial part of the company's history. I don't believe it has the luxury of failing to deliver the goods again.

That is especially true now that it has the available capital to push its strategy forward. It has taken steps to mitigate issues surrounding logistics and the supply chain, boost corn oil extraction, doubled its storage for corn reserves, and upgrading equipment in order to improve premiums in its specialty alcohol business while diversifying its product line.

All of these improvement, and other projects, are expected to add another $20 million in EBITDA in 2023, and boost that to at least $50 million in additional EBITDA in 2023.

With improvement in its logistics and supply chain, and expected increase in revenue and EBITDA, the company must execute on its strategy in the near term and further out if it wants to break out of its decade-long inability to consistently grow and support its share price.

My opinion is if the company doesn't come through now, I'm not sure what it has left that it can do that will boost the stock.

For further details see:

Alto Ingredients Has To Prove It Can Execute On Its Strategy