ALTO - Alto Ingredients: Poised To Grow In Stature But Better To Wait For A Pullback

2023-07-11 11:51:53 ET

Summary

- Alto Ingredients is poised to see a surge in its short-term and medium-term EBITDA profile.

- The company is deepening its presence in high-margin products such as grain-neutral spirits, corn oil, and high-quality protein, and enhancing its manufacturing efficiency and fuel sourcing, which could result in a 4x EBITDA growth over the next three years.

- The stock could benefit from further rotation momentum within the micro-cap space but we are not enthused by the risk-reward on the standalone chart.

Company Snapshot

Alto Ingredients (ALTO), a micro-cap stock, has built a name for itself in the American specialty alcohol market, and is currently believed to be the market leader there . It currently operates five alcohol production facilities, aggregating to a production capacity of 350m gallons. Besides specialty alcohol, ALTO also produces and distributes essential ingredients (dry yeast, liquid feed, distiller grains, corn gluten meals, and feeds, etc.). ALTO's customer base lies in end markets such as food and beverage, consumer products, beauty, etc.

EBITDA Profile Is Poised To Surge

Novice investors who may have cast a cursory glance at ALTO's recent EBITDA trajectory could be forgiven for feeling put off by three successive negative readings on the EBITDA front, including the first quarter of 2023.

YCharts

It now appears that we may be close to seeing the last of these negative prints; on the recent earnings call, management implied that crushing margins were in a better place, and with a rebound in travel activities in the spring and summer months, one would think these fuel-grade ethanol margins would hold up well at least in Q2 and Q3. ALTO has already been carrying out a few transformational projects (more on that later), and that as well should bring in a $10m uplift this year.

All in all, despite a negative reading of over -$5m in Q1, FY23 consensus numbers for ALTO suggest that ALTO could be poised to generate positive EBITDA of over $8m per quarter for the remaining three quarters. At the FY23 estimate of roughly $19m, ALTO would be priced at a 5% discount to its long-term EV/EBITDA average of 18.3x.

YCharts

That's not bad, but extend your investment horizon by a few more years, and you're looking at a totally different valuation backdrop which essentially makes ALTO look like a real steal.

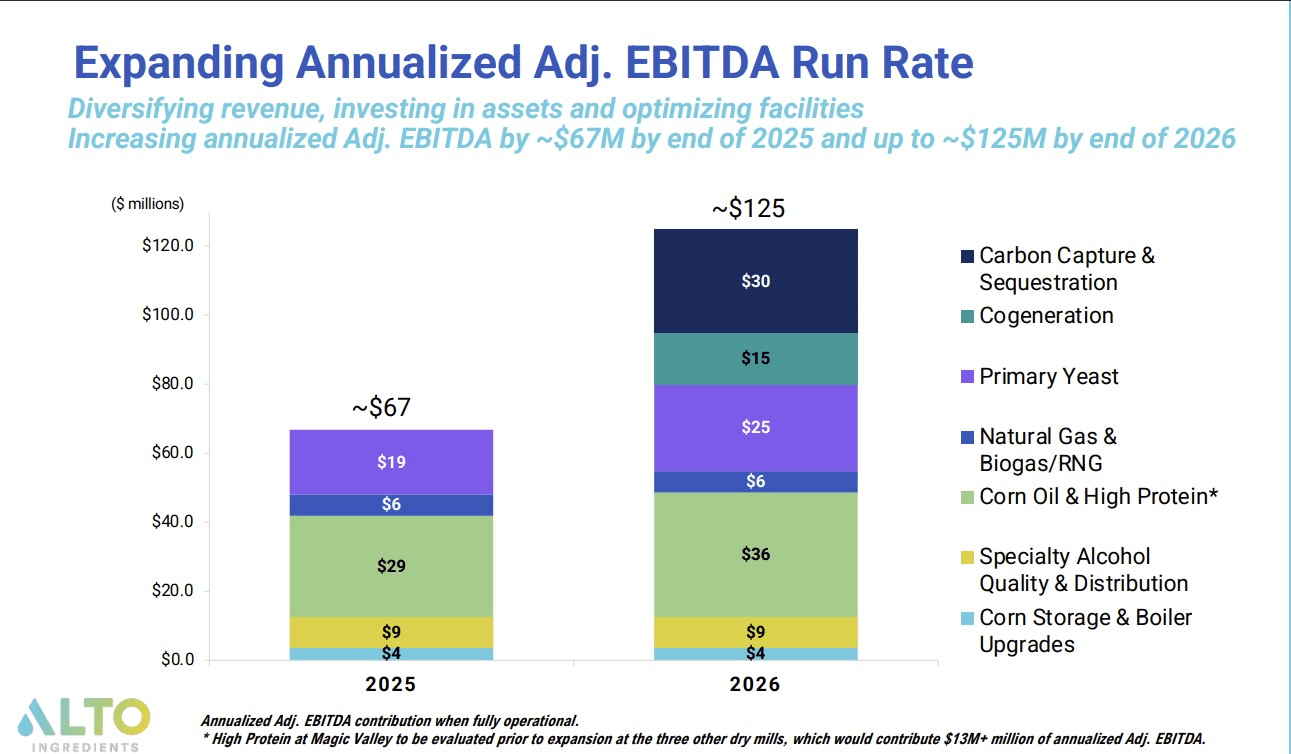

Before we get to medium-term valuations, it's worth noting that ALTO is currently in the midst of a transformation journey where it intends to mitigate its inherent susceptibility to the vicissitudes of ethanol-crushing margins. To facilitate this, ALTO has been deepening its presence in high-margin product pockets such as grain-neutral spirits ((GNS)), corn oil, and high-quality protein.

Last year ALTO upgraded the distillation of its GNS systems to produce high-quality 190-proof and low-moisture 200-proof products which are typically used in the food and beverage, pharma, and personal care industries. Management is currently in the midst of placing its GNS products on a spot purchase basis for the remainder of the year, even as they start getting into discussions regarding annual contracts for next year; they expect these products to contribute $5m of EBITDA p.a and this will likely hit a $ 9m runrate by next year.

Prospects for the corn-oil segment look even more alluring (given its salutary qualities as a cooking agent) and the market is poised to double over the next decade. Management has been putting in place new tech (CoProMax tech material) to enhance corn oil production in one of their plants (by approx 40% in pounds per bushel), and soon it will be extended to three other plants. These enhancements will likely boost group EBITDA by $9m p.a. per plant, so you could be looking at $36m of benefits by FY25.

Besides higher quality products, ALTO has also been finetuning its manufacturing prowess, plant efficiency, and fuel sourcing. Efforts have been made to double their corn storage facilities which will now give them ample elbow room during the corn-procurement initiatives. This is expected to boost EBITDA by $2m p.a. Next year, ALTO will also have a new natural gas pipeline in operation which will help reduce energy costs by $4m p.a.

{kind=link}

All these efforts in aggregate, will result in ALTO's EBITDA growing by 4x over the next three years hitting levels of $67m by the end of FY25. At that FY25 EBITDA run rate, you're looking at an inordinately cheap specialty commodity play, at less than 5x forward EV/EBITDA!

Closing Thoughts: Stock-related Considerations

YCharts

This year, the ALTO stock has gone through a choppy journey, but despite the relative turbulence this year, it has still managed to deliver positive returns of over 20%, and comfortably outperform its micro-cap peers.

The recent uptrend will no doubt bolster the enthusiasm of ALTO's management team who have been opportunistically buying back the stock as they feel it is undervalued. For context, the company is currently running a $5m buyback plan (it was originally meant to be a $10m plan, but was later curtailed by ALTO's lenders) and recently deployed one-third of that war chest in Q1 alone. ALTO has another $3m in waiting, which will likely be deployed in the quarters ahead, and could offer decent support to the share price.

YCharts

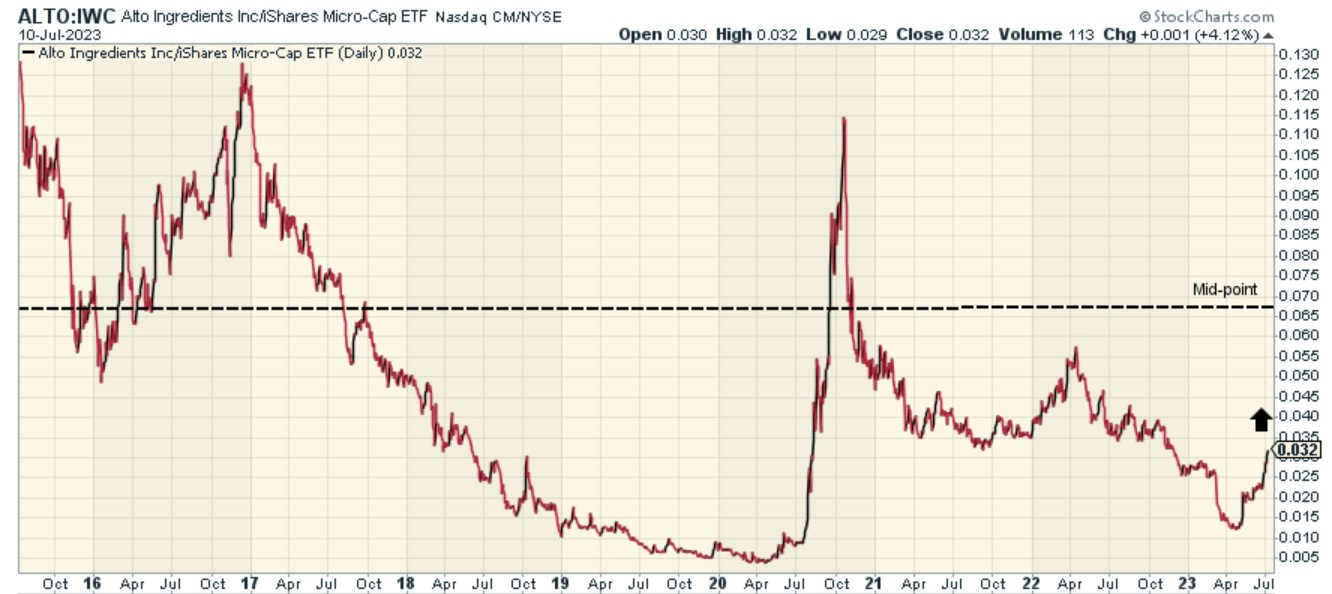

What's also interesting to note is that despite the strong alpha generated this year, it looks like there's still ample scope for more rotation momentum. The image below sheds some light on how ALTO has fared relative to the iShares Micro-Cap ETF; despite a doubling of the ratio from levels seen earlier this year, it is still a long way off from breaching the mid-point of its medium-term range.

{kind=link}

Having said all that, investors may also not want to get overly optimistic as there are still a few concerns worth highlighting.

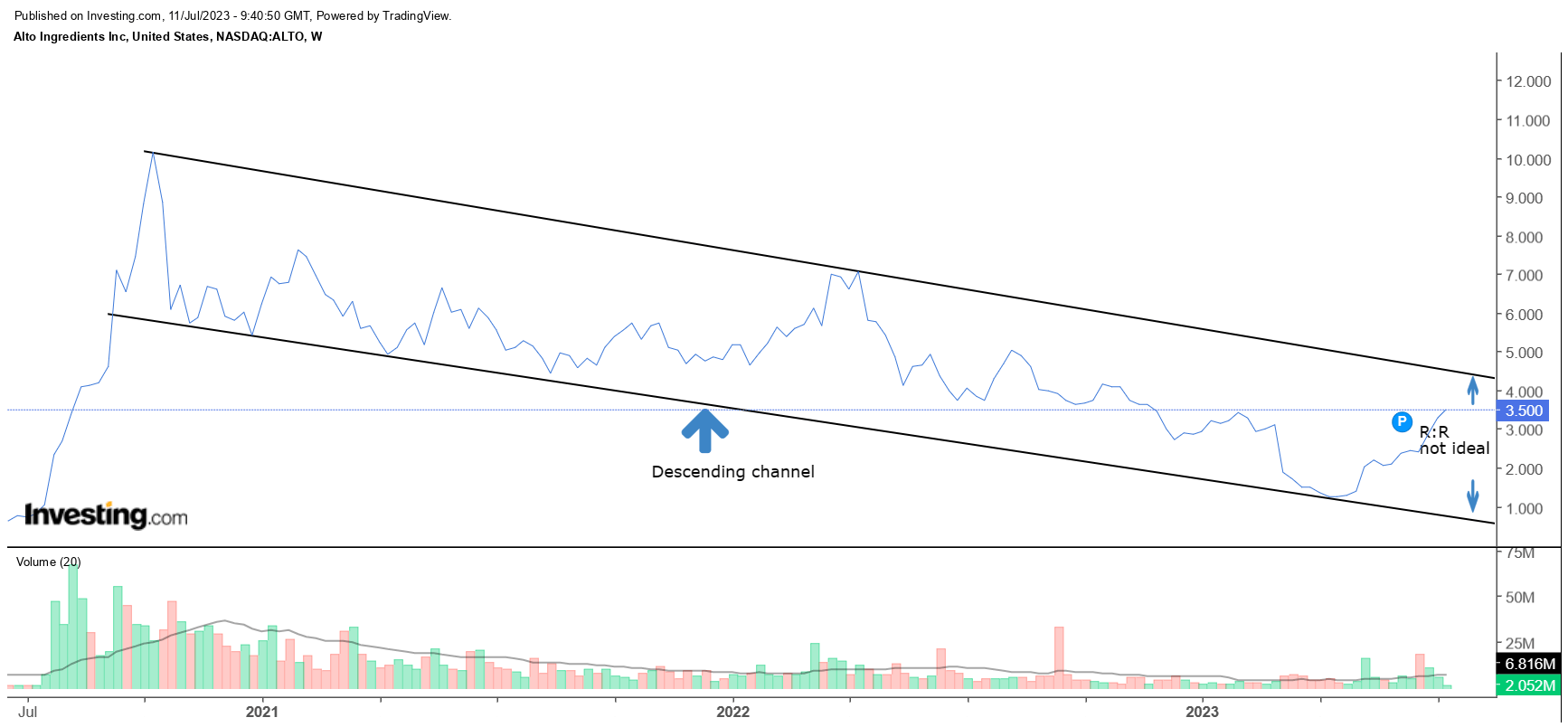

Firstly, consider looking at ALTO's own weekly price imprints over the last two years; whilst there have been intermittent spikes in the stock price every now and then, broadly, it's fair to say that what we're dealing with is a long-term descending channel.

{kind=link}

If one were to contemplate a long position at current levels, using the two boundaries of the channel as guideposts, the risk-reward (R:R) on offer looks unappealing at only around 0.2x (you ideally want to get in when the R:R shifts to 1x or above).

Investors may also want to note that even though we've seen a fairly decent uptrend since April, that has done little to scare off the short-sellers. On the contrary, the short interest has gone up by around 47% since the end of March!

YCharts

Finally, investors may also want to consider that the recent rally has largely been fuelled by retail interest (this doesn't necessarily have to be a bad thing, but more broad-based participation would have been preferred); on the other hand, the guys with the deep pockets- the institutions, continue to reduce their stake in ALTO every other month. Effectively on a YTD basis, the net shares owned by them are down by 20%.

YCharts

For further details see:

Alto Ingredients: Poised To Grow In Stature, But Better To Wait For A Pullback