AE - Alto Ingredients: The Decline Has Created A Buying Opportunity

Summary

- Alto Ingredients has experienced some downward pressure over the past few months, even in spite of growing revenue and profits.

- Some of the bottom-line figures are deceptive given the role that a grant played in the matter, but the overall picture is still improving.

- Risk appears fairly low and shares look attractively priced right now.

Just because an investment didn't offer attractive prospects at one point in time doesn't mean that the picture can't change for the better. As strong performance continues to be demonstrated and as shares of a company decline in price, the attractiveness of the firm in question can become more appealing, eventually reaching the point that assigning it a ‘buy’ rating just makes sense. One example of this can be seen by looking at Alto Ingredients ( ALTO ), a firm that produces and markets specialty alcohols and other essential ingredients for its customers. Recently, shares of the company have fallen even as fundamental performance remains strong. In addition to shares getting cheaper, the company continues to have cash in excess of debt totaling $22.2 million, leaving it with a good amount of wiggle room should market conditions worsen. Long term, investors should still expect significant volatility from a fundamental perspective. But given where shares are priced today, I do feel comfortable increasing my rating on the firm from a ‘hold’ to a ‘buy’, reflecting my opinion that the company’s stock should outperform the broader market for the foreseeable future.

Robust strength changed my opinion

Back in July of this year, I wrote an article that looked upon Alto Ingredients in a very neutral way. In truth, I was turned off by the volatility the company had seen in prior years, especially when it came to profitability. Having said that, profits in 2020 and 2021 proved to be rather robust for the company thanks to the change in market conditions. These changes, combined with a refusal by the market to push shares higher, leads into the stock looking rather cheap. But I still couldn't get over the company's business model and volatility as risk factors, ultimately resulting in a ‘hold’ rating for the business. Since then, shares of the firm have performed slightly better than I would have anticipated. While the S&P 500 has dropped by 12.9%, Alto Ingredients has seen a drop of 9.8%.

{kind=link}

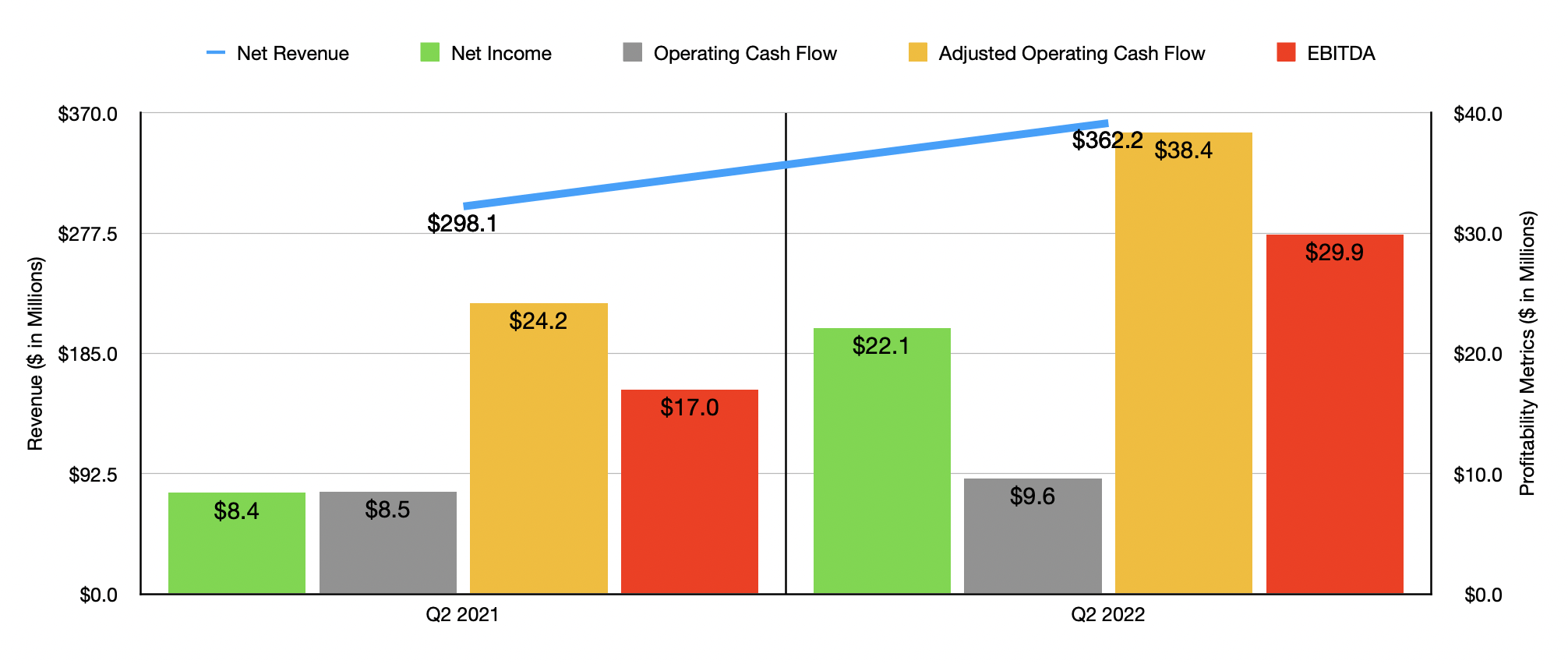

This return disparity is not necessarily large enough to be anything more than statistical noise. Having said that, it is also true that the company has continued to generate strong fundamental growth during this window of time. To see what I mean, we need only look at results covering the second quarter of the company's 2022 fiscal year. This is the only quarter for which data is now available that was not available when I last wrote about it. During that quarter, revenue came in at $362.2 million. That's 21.5% higher than the $298.1 million generated the same quarter only one year earlier. Total gallons of specialty alcohols the company sold actually dropped, declining from 125 million to 107.1 million. However, the firm did benefit from an increase in average pricing per gallon from $2.41 to $2.84. This drop in gallons sold was largely driven by a reduction in 3rd party gallons as the company continued to focus on the marketing and sales efforts associated with its own core production assets. The company also saw a more than doubling of sales of alcohol from its other production segment, driven by a rise in gallons sold of 14.4 million. This represents a 176% rise year over year. That unit also benefited from a $0.27 per gallon increase year over year. Meanwhile, essential ingredients revenue jumped by 221% to $23.4 million, driven by a 140% rise in volume and a 34% increase in average sales price per ton.

{kind=link}

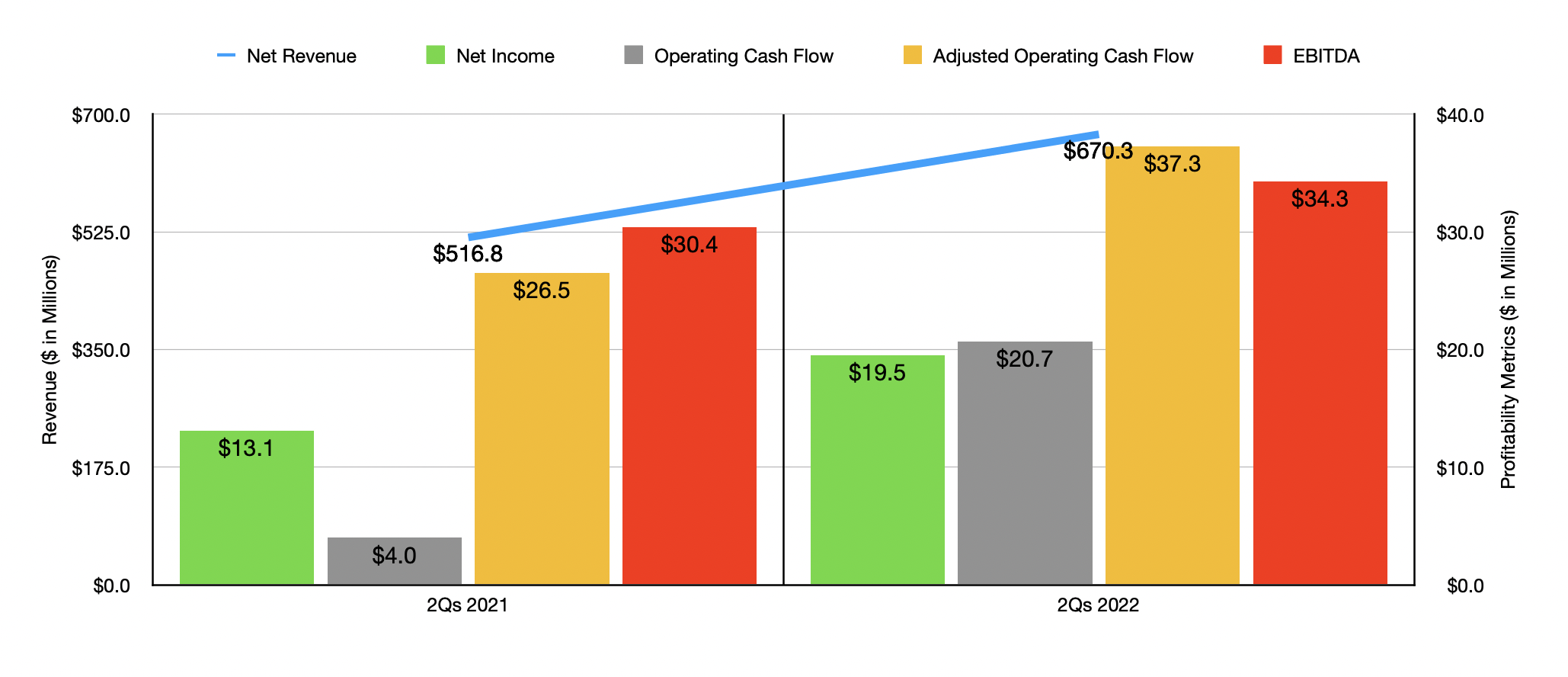

Clearly, the company's growth initiatives, particularly with regard to its emphasis on its own core production and to expanding into the specialty alcohols and essential ingredients spaces have proven to be beneficial for shareholders. The end result has also been an improvement in profitability. Net income in the second quarter of this year totaled $22.1 million. That's significantly higher than the $8.4 million reported one year earlier. Operating cash flow rose from $8.5 million to $9.6 million. But if we adjust for changes in working capital, the picture would have been even better, with the metric growing from $24.2 million to $38.4 million. Meanwhile, EBITDA also improved, rising from $17 million to $29.9 million. It is worth mentioning that profitability for the company was somewhat skewed. Although revenue has been rising, the firm benefited to the tune of $22.7 million from a grant associated with the USDA. Without that, operating income would have actually declined from $6.1 million in the second quarter of 2021 to negative $0.15 million the same time this year. It is worth mentioning that total results for the first half of the year did also come in stronger than what the company achieved in the first half of 2021. This much can be seen in the chart above.

{kind=link}

Unfortunately, we don't really know what to expect for the rest of the current fiscal year. Given the one-time nature of the grant I mentioned, it's difficult to know what the organic potential the firm is. So instead of projecting out what results might look like for the rest of the year, I decided to price the company using data from 2021. Using this approach, the firm is trading at a price to adjusted operating cash flow multiple of 6.9 and at an EV to EBITDA multiple of 3.4. As part of my analysis, I compared the company to two other firms that are somewhat similar in nature. On a price to operating cash flow basis, these companies traded at multiples of 1.5 and 15.3. And using the EV to EBITDA approach, the multiples were 0.6 and 6.3. In both cases, our prospect was in the middle of the two.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Alto Ingredients |

| 6.9 |

| 3.4 |

| Adams Resources & Energy ( AE ) |

| 1.5 |

| 0.6 |

| REX American Resources Corp ( REX ) |

| 15.3 |

| 6.3 |

Takeaway

The data shown right now suggests to me that Alto Ingredients continues to perform well. Yes, this year is a bit deceptive because of the grant income the firm received. Having said that, shares of the firm do you look to be attractively priced at this point in time and revenue continues to increase thanks to management growth initiatives. On top of this management announced , in September, a new $50 million share buyback program. While I fully expect volatility to be commonplace with this firm, I do also believe that those who don't mind this volatility might benefit meaningfully from an eventual appreciation of its stock. Due to this, I've decided to increase my rating on the company from a ‘hold’ to a ‘buy’.

For further details see:

Alto Ingredients: The Decline Has Created A Buying Opportunity