VGR - Altria 2022 Earnings: Hoping For Capital Gains Is A Bad Strategy

Summary

- Altria Group, Inc. reported solid profits despite nearly double-digit volume declines.

- The company is feeling the pinch from lower disposable income, which is hardly surprising, but of course benefits discount brands. Altria's discount segment nonetheless underperformed.

- In this update, I discuss Altria's full-year results, focusing on cash flow, debt maturities, volume trends and growth prospects.

- I'll also present an updated valuation based on adjusted earnings and discounted cash flows, and explain why I consider it foolish to hope for capital gains when investing in MO stock.

Discussion Of Altria’s Full-Year Earnings And Cash Flows

Altria Group, Inc. ( MO ) reported full-year 2022 results on Feb. 1, 2023. Revenue net of excise tax of $20.7 billion was in line with analyst estimates , down 2.0% year-over-year (YoY). Adjusted earnings per share ((EPS)) of $4.84 were slightly above consensus. The primary driver of the significant variance from GAAP earnings ($3.19) was charges related to Altria's investments in Anheuser-Busch InBev SA/NV ( BUD ) ($1.12) and JUUL (JUUL) ($0.81), slightly offset by $0.40 related to the release of deferred tax asset valuation allowances.

While adjusted EPS growth of 5% sounds very solid, it should not be forgotten that share repurchases made a significant contribution - at 2.35% in absolute terms, representing 47% of total adjusted EPS growth. The company reported the completion of its $3.5 billion buyback authorization. Shares repurchased during 2022 totaled $1.8 billion, representing 38.1 million shares at an average price of $47.8 per share. Altria's Board of Directors announced a new $1 billion share repurchase program that should be good for approximately 22 million shares at today's price, representing approximately 1.2% of the weighted average diluted shares outstanding in 2022. This will help Altria achieve its full-year 2023 adjusted earnings per share guidance of $4.98 to $5.13, representing growth of 3% to 6%. Growth will be achieved - as usual - by more than offsetting volume declines with price increases. On the flip side, Altria will continue to invest in smoke-free products and the company will also increasingly feel the impact of rising interest rates.

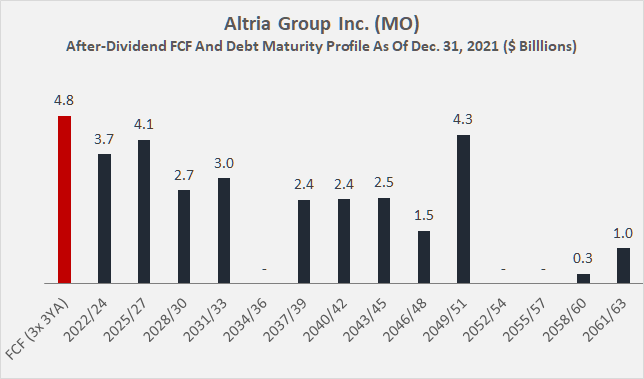

However, I would not overstate this effect, as I pointed out in my recent article in which I modeled the interest rate burden of Altria, The Home Depot ( HD ), and V.F. Corp ( VFC ) under two stress scenarios. Altria's maturity profile (based on the 2021 10-K , Figure 1) is quite reassuring, especially given its still substantial after-dividend free cash flow of around $1.5 billion. Indeed, management announced its intention to redeem approximately $1.3 billion of bonds maturing on Feb. 15 (€1.25 billion, 1.00% Notes, CUSIP 02209SAW3). The company is also likely to redeem the 2.95% Notes due in early May (CUSIP 02209SAP8, $350 million).

Figure 1: Comparing Altria’s three-year average after-dividend free cash flow to its debt maturity profile (own work, based on the company’s 2021 10-K)

{kind=link}

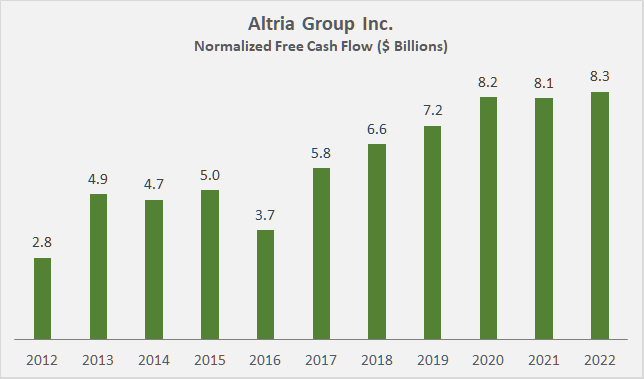

From a cash flow perspective, Altria continues to perform well. Given the low input costs, cash flow has understandably not been significantly impacted and also working capital related effects were negligible. Normalizing free cash flow for working capital movements and other charges (e.g., accrued settlement charges), and taking into account estimated stock-based compensation, Altria generated approximately $8.3 billion of free cash flow last year (Figure 2).

Figure 2: Altria’s historical free cash flow, normalized with respect to working capital movements and other charges, and adjusted for estimated stock-based compensation (own work, based on the company’s 2012 to 2021 10-Ks and the 2022 full-year earnings release published on Feb. 1, 2023)

{kind=link}

Altria also recorded a $1.0 billion cash inflow from Philip Morris International ( PM ) related to the agreement to end the commercial relationship for IQOS in the U.S. beginning in May 2024. Altria will receive an additional $1.7 billion plus interest (6% p.a.) in July 2023, but PM has the right to pay at an earlier date. Of course, the $1.0 billion cash inflow is not included in Figure 2 because it is a non-recurring cash flow from investing activities. Under the agreement, Altria will launch its own heated tobacco product later rather than sooner, due to regulatory hurdles, via its 75% stake in Horizon Innovations (the remaining 25% is held by JT Group). The commercialization of IQOS, which PM is pursuing starting in May 2024, will of course be much easier from a regulatory perspective, as the system has already been authorized as a modified risk tobacco product in 2020.

In Oral Tobacco, Altria reported a 0.6% decline in net sales after excise taxes due to lower shipment volumes and a change in product mix, partially offset by higher pricing. To put the segment in perspective: Oral Tobacco sales represent about 12% of total net sales after excise taxes in 2022, but of course the 730 basis points higher adjusted operating margin of 66.3% compared to the Smokable Products segment is very encouraging. Nonetheless, the segment's operating margin declined 220 basis points YoY, primarily due to higher input costs and increased promotional investments in on! , which grew 70.5% YoY in volume terms. Of course, it should not be forgotten that on! still only accounted for 10.3% of reported segment shipment volume for the year, while Copenhagen and Skoal together accounted for over 80% of reported shipment volume, a decrease of 7.3% year-on-year.

A Closer Look At Altria’s Smokeable Products' Volumes

Overall, smokeable product volumes declined by 9.6% YoY, and Altria's cigarette business recorded a 9.7% decline in in terms of volumes. In addition to the expected continuation of the industry decline (due in part to pandemic-related normalization effects), Altria lost retail share due to lower disposable income resulting from higher rates of consumer price inflation. The industry-wide decline is, unsurprisingly, the elephant in the room with an attributable 8% year-over-year decline after adjusting for trade inventory movements, calendar differences and other effects.

On a net basis, Altria's shipment volume declined 150 basis points more than the industry, largely due to increasing demand for discount cigarettes as smokers trade down in this inflationary environment. Marlboro slightly increased its share in the premium segment, but lost 40 basis points overall to 42.5% market share. I think the somewhat more pronounced decline due to Altria's focus on premium brands is understandable, but it shows that most smokers generally remain loyal to their preferred brand, even in the current environment.

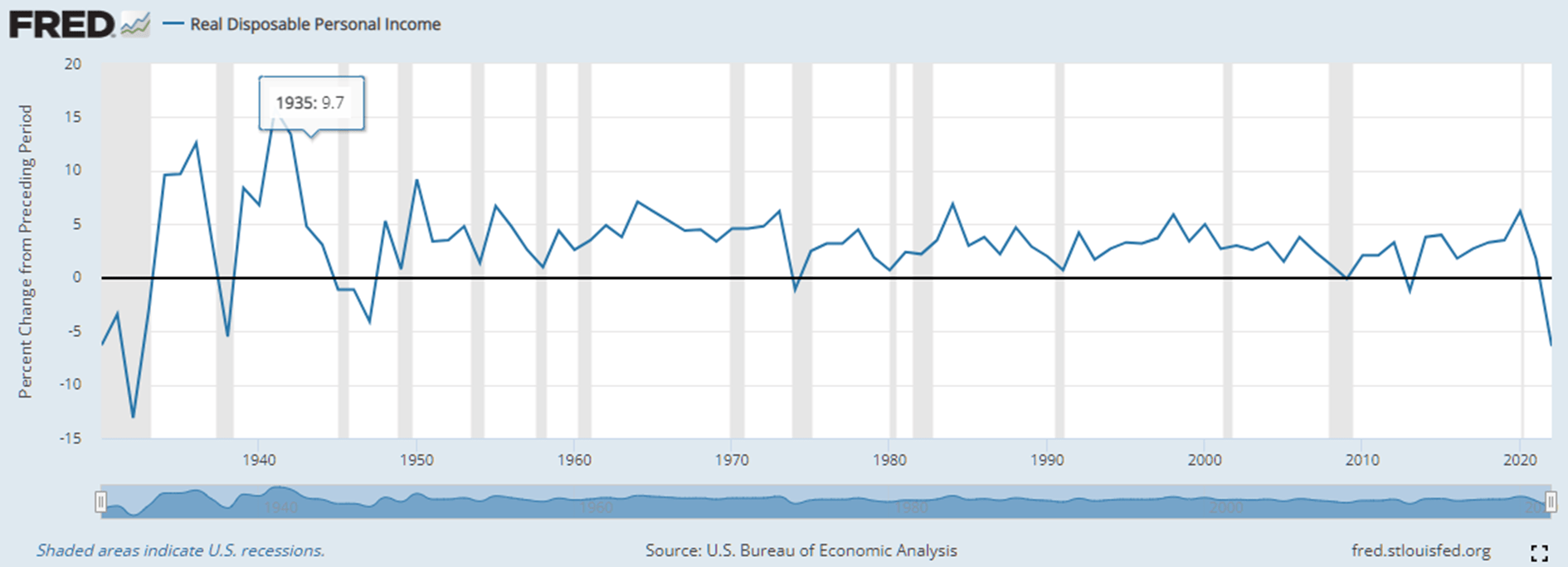

The trend in Altria's discount segment (which is not particularly significant per se with 6.4% volume share), is nonetheless interesting and slightly concerning. The 18.2% YoY volume decline suggests that Altria's offering in this segment is not competitive enough. In absolute and relative terms, the discount segment declined 40 basis points (or over 11%) YoY to 3.1% of retail share. Discount brand-focused Vector Group ( VGR ), with brands such as Eagle 20's, Pyramid, Montego, Grand Prix, Eve, and Liggett Select, is the beneficiary in an environment characterized by sharply declining disposable incomes (Figure 3).

I compared Altria and Vector in May 2022 and concluded that the latter "could outperform in an environment of continued high inflation and consumers with lower discretionary income." I also noted that Altria continues to report declining volumes, while Vector has increased volumes over the past decade. Still, I ultimately rated the stock a "Sell" due to its strained balance sheet and irresponsible dividend policy, which has already resulted in a 50% cut in early 2020.

Figure 3: U.S. Bureau of Economic Analysis, Real Disposable Personal Income [A067RL1A156NBEA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/A067RL1A156NBEA, February 1, 2023.

{kind=link}

Updated Valuation Of MO Stock And Conclusion

Altria reported solid earnings for 2022, in line with expectations. Free cash flow remains strong, but future growth will be more elusive, as evidenced by the continued decline in cigarette volumes. Altria will continue to face tough competition in its Oral Tobacco segment from Swedish Match's (now PM) top-selling ZYN oral nicotine pouch brand, and in Heated Tobacco, Altria will get off to a slow start given the termination of the marketing agreement for IQOS beginning in May 2024. I expect Altria to continue to defend its position in the premium cigarette segment and maintain strong cash flow through price increases, slightly offset by investments in Heated Tobacco and Oral Tobacco. I don't really expect Altria's free cash flow to grow on a corporate basis. In 2022, the company paid out $6.6 billion in dividends to shareholders, a payout ratio of 80% of normalized free cash flow. Altria's latest 4.4% dividend increase was certainly meaningful, but I believe it reflects the new normal .

Given the elusive cash flow growth, continued volume decline, and late start in heated tobacco, investors should not expect their yield on cost to grow excessively. That said, an 8%-plus starting yield is definitely not bad, but of course it also reflects Altria's focus on the U.S. market, which makes the company disproportionately vulnerable to adverse regulatory developments.

While the company currently pays out 80% of its normalized free cash flow in dividends, it still has more than $1.5 billion to spend on share repurchases (which drive EPS growth) and debt reduction. It should also be remembered that Altria is likely to sell its stake in BUD sooner or later, which should significantly boost free cash flow per share as well. These additional share repurchases will lower Altria's dividend payout ratio, which will help sustain dividend growth. Assuming the company does not commit any other serious execution errors (i.e., JUUL and Cronos), the company should also be able to reduce its (already manageable) debt.

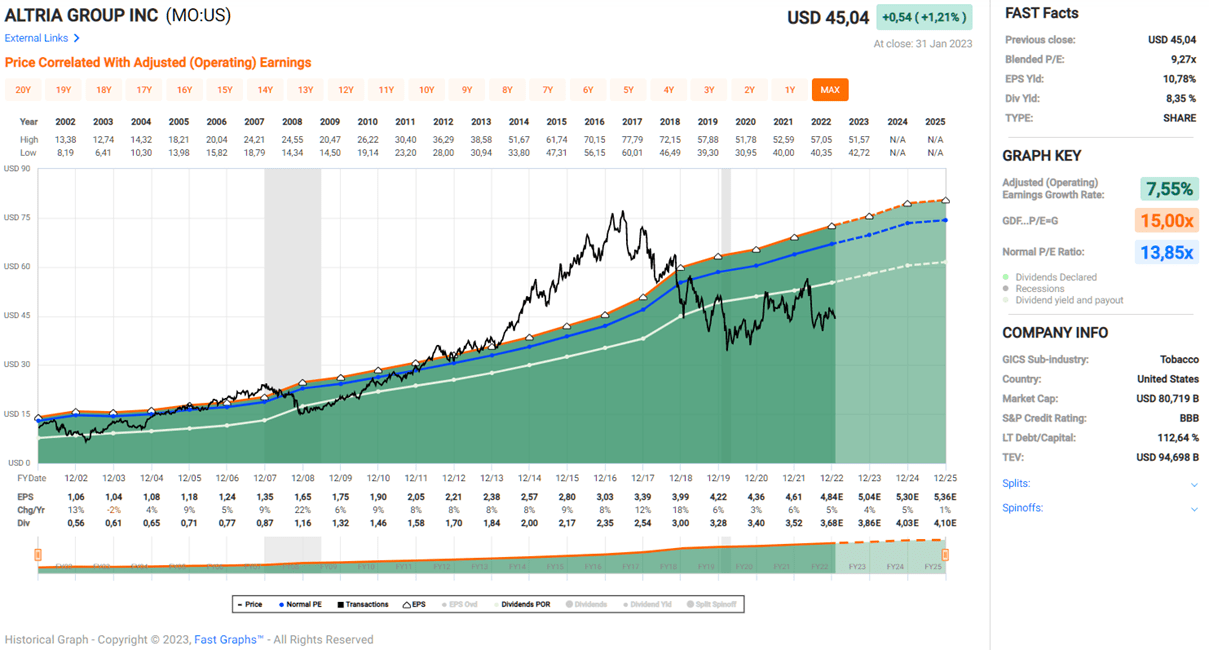

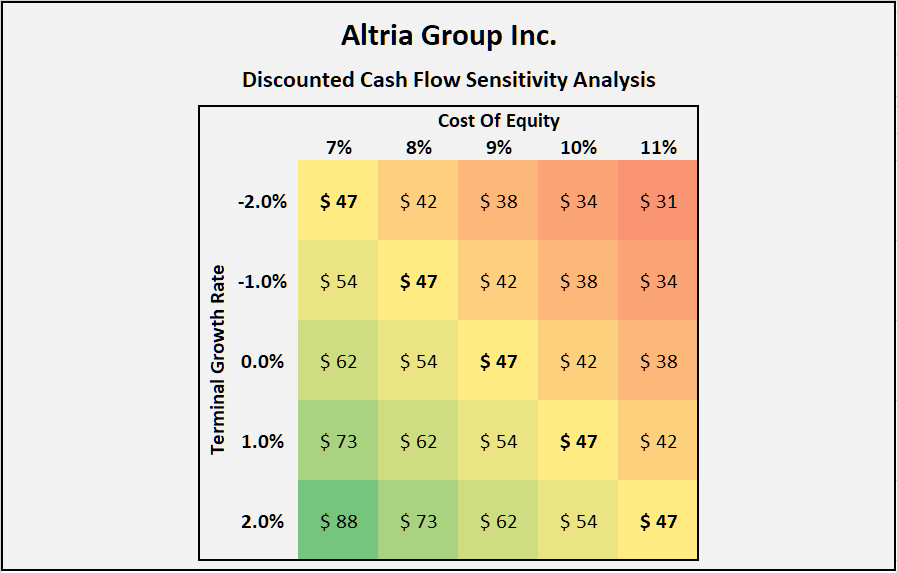

Altria's FAST Graphs chart (blended P/E of under 10, Figure 4) and current nFCF yield of 10% signal that the stock is fairly cheaply valued. Figure 5 shows a discounted cash flow sensitivity analysis to give you a different view of Altria's current valuation. At a baseline nFCF of $8.3 billion, the stock is currently fairly valued if the investor believes a 9% cost of equity is reasonable and expects Altria to be able to maintain its free cash flow. If nFCF declines at an annual rate of 2% in perpetuity, the stock would currently be fairly valued at a 7% cost of equity. However, if management is able to unlock value by selling the BUD stake and thereby increase free cash flow per share, I would consider MO to be quite undervalued. One would have to be a true pessimist to find Altria's current valuation demanding.

However, taking a conservative view and considering the elusive growth prospects, I don't think the potential for a "mean reversion" is significant. That said, a weak share price makes dividend reinvestments - same as share buybacks - very effective, and I believe that ultimately most, if not all, investors own Altria as an income-generating asset. In this regard, I am confident that there are few things worse than hoping for solid capital gains while in the process of building a position in such a stock. I discussed the fallacy of hoping for strong capital gains in a separate article not too long ago. In brief, as an income investor, I have learned to appreciate bear markets and periods when individual stocks underperform, because consistent investment during such periods can significantly increase the portfolio's return on equity.

In my own portfolio, I own a significant position in Altria. Therefore, I am not currently adding any net new capital to my position, but I am of course reinvesting my dividends opportunistically.

Figure 4: FAST Graphs plot for Altria stock [MO] (obtained with permission from www.fastgraphs.com) Figure 5: Discounted cash flow sensitivity analysis of Altria [MO] (own work, based on the 2022 full-year earnings release published on Feb. 1, 2023 and my own nFCF calculation)

{kind=link}

{kind=link}

Thank you very much for taking the time to read my article. How did you like it, my style of presentation, the level of detail? If there is anything you'd like me to improve or expand upon in future articles, do let me know in the comments section below.

For further details see:

Altria 2022 Earnings: Hoping For Capital Gains Is A Bad Strategy