SWMAY - Altria: A Conservative Pick To Click For 2023

Summary

- Altria is one of my picks for 2023, and it could be a good fit for conservative income investors.

- Shares are dirt cheap today below 10x earnings, and a bit of multiple expansion could easily send shares above $60 in a couple years.

- The dividend hikes keep coming, with another 4.4% hike from $0.90 to $0.94. That puts the yield at 8.2%.

- The buybacks are set to continue and the company will probably announce a new buyback program in the next quarter or two.

I have been working on my top picks for 2023 over the last couple days, and it is a fantastic exercise in my opinion. Trying to go through a portfolio full of individual companies and picking a couple that have more potential to provide attractive returns for investors is a great exercise and one that makes me think about what the markets will do and how these companies should perform over the next year. One of my picks for 2023 is Altria (MO). The company sports an impressive margin profile, solid balance sheet, a cheap valuation, and a large dividend that pays investors to wait for share price appreciation.

Investment Thesis

Altria is a large tobacco company and the owner of the famous Marlboro brand here in the US. Shares have outperformed the market in 2022, and I think there is a good chance of that happening again in 2023. This is mostly due to the cheap valuation under 10x earnings and a yield over 8%. They hiked the dividend again this year, and I don’t see any reason why they would break the streak and lose their dividend king status.

The company has an impressive margin profile and they have been working to grow product lines outside of their typical combustible products, including nicotine pouches. Declining volumes will be something for investors to keep an eye on, but I still think the risk/reward is favorable today. The company has been buying back stock at a decent clip, which will boost EPS, and I think investors could also see some multiple expansion. Overall, there are way more reasons to be bullish on Altria than bearish, especially when you get paid over 8% to wait for share price appreciation.

Q3 Update

My last article on Altria was in August, and since then, the company has released its Q3 results. While revenues were basically flat, operating margins improved slightly. Debt has also come down a bit since the end of 2021, which is a good sign considering that the company has a debt load over $25B. I would like to see that number continue to come down over time, but they don’t have too much debt on their balance sheet considering the defensive nature of their business. They also accepted a $2.7B payment from Philip Morris (PM) as a buyout of the iQOS licensing rights.

This should give them some dry powder to work with, and Philip Morris will still have to wait until 2024 to sell iQOS products in the US. I’m curious to see how Altria handles a transition to products outside of the traditional cigarette line of business, but they have seen impressive growth in the On! nicotine pouches. They still have some work to do to catch up with Swedish Match’s (SWMAF) (SWMAY) Zyn pouches, but market share is up to 5.2% in Q3, and volumes were up almost 70% YoY. Marlboro has also maintained its dominant position in the cigarette sector. One of the things that investors point to as a reason to be cautious is declining volumes, but I think the cheap valuation more than offsets that risk.

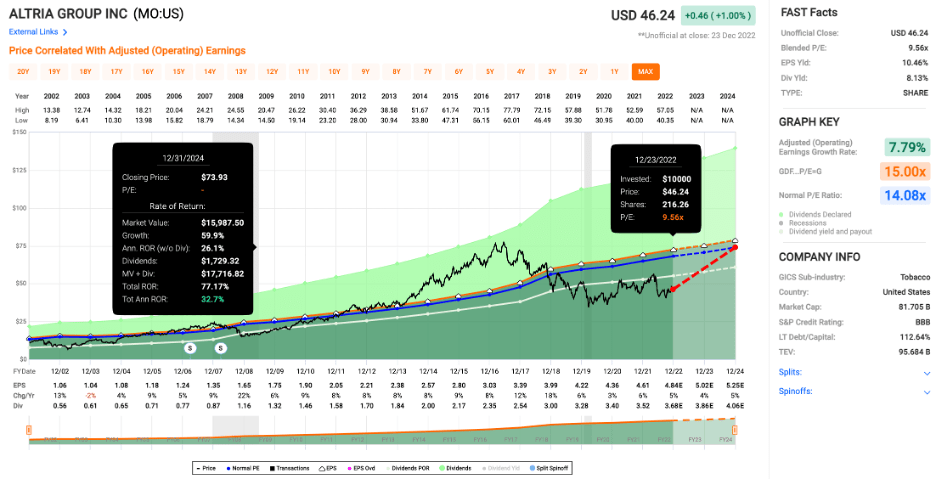

Valuation

The cheap valuation is one of the biggest reasons to be bullish on Altria. Shares trade at an earnings multiple of 9.6x, which is far too cheap in my opinion. While it isn’t growing revenues at a rapid rate, they still have impressive margins, and continued buybacks should provide a boost to EPS. I think we will see some multiple expansion in the next couple years, which would give investors double digit returns when you factor in the 8.2% dividend.

Price/Earnings (fastgraphs.com)

{kind=link}

Shares are just far too cheap today under $50. If you think Altria will head back to its 14.1x average multiple in the next couple years, investors are in for returns over 20%. Even if we only see a 12x multiple, that will put shares over $60 by the end of 2024. The other main reason to be bullish on Altria is the growing dividend over 8%.

Dividends & Buybacks

While Altria has been out of favor with the market in recent years, they have a consistent track record of dividend growth. It has been so consistent that the company is part of a select group that has earned the title of dividend king with over 50 years of consecutive raises. Their most recent increase was a 4.4% hike from a quarterly payout of $0.90 to $0.94. I think they will be able to raise the dividend for several years to come, but I will be watching to see if declining volumes eventually has an impact on the company’s ability to pay out its juicy 8.2% dividend.

If the yield over 8% isn’t enough, Altria has also been repurchasing shares at a decent clip. They bought back another 8.5M shares in Q3, for $368M, at an average price of $43.68. At the end of the quarter, they only had $374M remaining on the current buyback authorization. My guess is that they will finish it off in Q4, or early in Q1 of 2023. A lot of companies have been buying back shares at high valuations in the last decade, but Altria’s buybacks are a huge boost for shareholders, especially since shares have been dirt cheap over the last couple years.

Conclusion

My top picks for 2023 both pay large dividends, and I think we are going to see dividend stocks like Altria perform well next year. It’s tough to justify buying an index when it is skewed towards tech stocks with rich valuations and small dividends, but that doesn’t mean all stocks are unattractive today. If I can find a good business with an attractively valued stock attached to it, I’m automatically interested, especially if it has a history of paying a growing dividend.

Altria checks all of these boxes. While I will be keeping an eye on declining revenues, the company has solid margins, a good balance sheet, a cheap valuation below 10x earnings, and a yield over 8% that has over 50 years of hikes in a row. You can also throw in buybacks for good measure. I think we will see some multiple expansion, but I just have a hard time seeing how investors lose money in Altria over the next 3 to 5 years. Altria is a good candidate for income investors looking for current income, and I think shares have a good chance of outperforming broader market indices in 2023.

Editor's Note : This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Altria: A Conservative Pick To Click For 2023