JAPAF - Altria: Earnings Growth Despite Bad 2022 Macro But Little Other Good News

Summary

- Altria Group, Inc. grew its operating income by 2% in 2022 despite reporting a cigarette volume decline of 9.5%, its worst since 2009.

- The traditional tobacco earnings model of price hikes that exceed excise increases has produced earnings growth despite weak volumes.

- Management has guided to a lower-than-usual 3-6% EPS growth in 2023 and also promised buybacks that are smaller than we expected.

- The smaller Oral Tobacco segment has continued to lose profits and market share. Philip Morris is a threat, though only from 2024.

- With Altria Group, Inc. shares at $47.06, the Dividend Yield is 8% and we expect a total return of 44% (15.4% annualized) by 2025 year-end. Buy.

Introduction

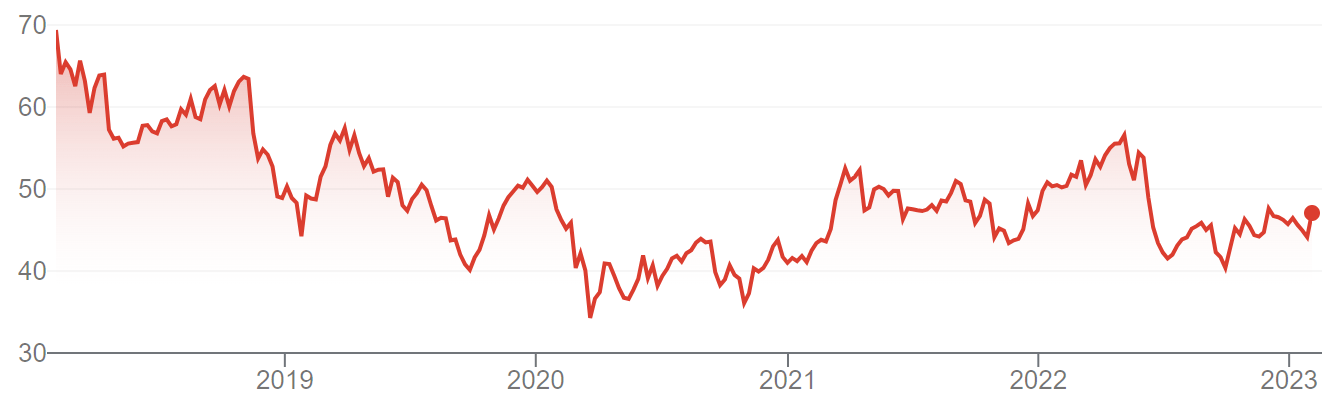

Altria Group, Inc. ( MO ) released Q4 2022 results this morning (February 1). As of 13:30 Eastern Standard Time, MO shares are up 4.5%, though still down 7.1% in the past twelve months:

{kind=link}

We upgraded our rating on Altria to Buy in February 2020. Since then, MO shares have gained 21% (including dividends), though they have fallen back 17.5% from their roughly $57 peak in May 2022.

Q4 2022 results were mixed. Adjusted Operating Companies Income (“OCI”) grew 2% in 2022 despite macroeconomic headwinds. Adjusted EPS grew 5% year-on-year, benefiting as much from buybacks and lower debt as from operational growth. As of Q4, Altria’s cigarette volumes were down 12% year-on-year, though Smokeable's revenues were flat net of excise and Adjusted OCI grew 4.0%, benefiting from the traditional tobacco earnings model. The Oral Tobacco segment has continued to lose profits and market share. For 2023, management is guiding to a lower-than-usual 3-6% Adjusted EPS growth, and buybacks are likely to be lower than 2022. We attribute most of the 2022 weakness to cyclical macro factors, but also expect Philip Morris to be a real strategic threat from 2024. Altria shares are at a correspondingly undemanding 9.6x 2022 EPS and an 8.0% Dividend Yield. Our base case forecasts indicate a total return of 44% (15.4% annualized) by 2025 year-end, but there are significant tail risks. We reiterate our Buy rating for now.

Altria Buy Case Recap

Our investment case on Altria Group, Inc. has been based on the continuing ability of its cigarette business to deliver on its traditional earnings algorithm, which includes:

- A low-to-mid single-digit annual decline in cigarette volumes

- A mid-to-high single-digit annual rise in average cigarette prices

- Together these give a low-single-digit annual growth in revenues

- Revenues After Excise tend to grow even faster as excise growth lags

- OCI margin expands with higher unit price and operational savings

- Including buybacks, EPS tends to grow at mid-to-high single-digits.

The U.S. cigarette market has historically been exceptionally profitable, due to relatively favorable tax levels and FDA regulations serving as strong barriers to entry against most potential competitors.

Altria's cigarette volume decline accelerated during 2016-19, partly attributed to an explosive growth in U.S. e-vapor. However, Altria still guided to an EPS growth of 4-7% in both 2019 and 2020, and achieved 5.8% in 2019. FDA actions against vaping in late 2019 sent e-vapor volume into a decline until Q1 2020, after which modest growth resumed. The COVID-19 outbreak boosted U.S. cigarette consumption from 2020, as pandemic restrictions generated more smoking occasions and government stimulus programs supported smokers' disposable incomes. Altria's cigarette volume decline decelerated to just 2% in 2020, and was just 4% during H1 2021 (but rose to 6% for the full year):

| Altria Cigarette Volume Declines (Adjusted) (2013-21) Source: Altria company filings. NB. Figures adjusted for inventory movements. |

As we will explain below, Altria’s cigarette volume decline in 2022 was the worst since 2009 (when it was 10.5% following a rise in the Federal Excise Tax), due to both the reversal of COVID benefits and macroeconomic headwinds, and Altria’s financial results were negatively impacted.

Altria Q4 2022 Results Headlines

Q4 2022 results were mixed. Adjusted OCI grew 3.9% year-on-year in Q4 and 1.9% for the full year:

| Altria Group P&L (Q 4 & Full-Year 2022 vs. Prior Year) Source: Altria results release (Q4 2022). |

Adjusted EPS grew 5% year-on-year in 2022, benefiting as much from buybacks and lower debt as from operational growth. Buybacks reduced the average share count by 2.5%, contributing roughly as much to Adjusted EPS growth as Adjusted Net Income growth (2.6%). Lower Interest Expense, from lower debt, added $104m to pre-tax earnings growth, compared to $226m from higher Adjusted OCI.

Group Adjusted OCI growth was entirely due to its Smokeable segment, as Oral Tobacco saw a year-on-year decline in its Adjusted OCI for both Q4 and full-year 2022.

| Altria OCI by Segment (Q 4 & Full-Year 2022 vs. Prior Year) Source: Altria results release (Q4 2022). |

Adjusted OCI growth in Smokeables was in spite of a 12% decline in cigarette volume in Q4.

Altria Cigarette Volume Fell 12% in Q4

In Q4 2022, Altria’s cigarette volumes were down 12% year-on-year, though Smokeable’s Net Revenues After Excise were flat and Adjusted EBIT actually grew 4.0%; for full-year 2022, cigarette volumes were down 10% year-on-year, but Smokeable’s Net Revenues After Excise were similarly flattish and Adjusted EBIT grew 2.9%:

| Altria Smokeable Financials (Q 4 & Full-Year 2022 vs. Prior Year) Source: Altria results release (Q4 2022). |

This is the result of the traditional tobacco earnings model, where price increases offset volume declines, excise taxes lag price increases and so add to net revenue growth, and cost savings help profits grow faster than revenues.

For Q4 2022, Altria achieved a net price realization of 11%. However, the average net pack price for Marlboro rose only 6.4% year-on-year. The gap between the two is due to mix, including Altria optimizing its local pricing and product mix through sophisticated analytics, and retail price increases exceeding excise increases.

Adjusted for inventory and the number of calendar days, Altria’s cigarette volume decline was roughly 1 ppt better than reported shipments, and was 11% for Q4 and 9.5% for the full year, roughly 2 ppts worse than U.S. industry volume declines of 9% and 8% respectively. Even on an adjusted basis, Altria’s cigarette volume decline became worse with each quarter in 2022, whether on a year-on-year basis or on a 3-year stack based on pre-COVID 2019:

| Altria Cigarette Volume Declines (Adjusted) (Since 2020) Source: Altria company filings. |

We attribute most of this weakness to cyclical macro factors, particularly the reversal of COVID benefits and consumer price inflation. Smokers are over-indexed to lower-income groups and thus mores likely to be impacted by the latter. Altria’s more expensive premium brands are also more likely to lose volumes (but not necessarily revenues) when consumers trade down, and the group’s cigarette retail share fell 0.8 ppt from 48.2% in Q4 2021 to 47.4% in Q4 2022.

Altria management data supports this view, for example, by showing how E-Vapor has also experienced volume declines since Q2 2022 and is thus unlikely to be responsible for the acceleration in cigarette volume declines:

| U.S E-Vapor Category Volume by Quarter (Since 2 020 ) Source: Altria results presentation (Q4 2022). |

{kind=link}

(The reduction in E-Vapor volume is likely to be caused in part by FDA actions against the category, including the issuance of Marketing Denial Orders to a number of E-Vapor players, especially on their flavored products.)

Other Reduced Risk Products are also not likely to be a factor in U.S. cigarette volume declines. Heated Tobacco products are currently not available in the country (following the ITC ban on IQOS imports from Philip Morris ( PM ) in 2021). Nicotine Pouches are growing strongly but remain small relative to cigarette volumes.

Altria Oral Tobacco Still In Decline

Altria’s Oral Tobacco segment has continued to lose profits and market share.

Oral Tobacco’s Q4 2022 Adjusted OCI were down 5.1% year-on-year and down 12.9% from Q3:

| Altria Oral Tobacco Financials (Q 4 2022 vs. Prior Periods) Source: Altria results releases. |

Altria’s overall share of the oral tobacco category fell 1.7 ppt year-on-year to 45.9%, though its On! nicotine pouches has seen category share rose to 5.9% (from 5.2% in Q3 and 3.8% in the prior-year quarter). Volumes tell a similar story, with On! volume up 65.9% year-on-year but overall Oral Tobacco volume down 4.3% year-on-year.

For full-year 2022, Oral Tobacco Net Revenues After Excise were down 0.6% and Adjusted OCI was down 3.8%:

| Altria Oral Tobacco Financials (2022 vs. Prior Y ear) Source: Altria results release (Q4 2022). |

Total U.S. oral tobacco industry volume rose by just 1% in 2022. However, nicotine pouches grew to 21.9% of the category. On! market share in nicotine pouches grew to 23.0%, up 6.1 ppt year-on-year.

Management also stated that they have reduced promotional spend per can by 15% in H2 2022.

Altria 2023 Outlook & Capital Allocation

For 2023, Altria is guiding to an Adjusted EPS of $4.98-5.13, implying growth of 3-6% year-on-year. This is lower than the historical 4-7% range that Altria originally guided for 2022 and also for 2020-22 before COVID-19. (Before that, Altria had guided to Adjusted EPS growth of 5-8% in 2020-22 before Q4 2019 results.)

Management is guiding to $1bn of share repurchases in 2023, from a new program authorized by the Board and expected to be completed by year-end. This is a lower amount than the $1.8bn repurchased in 2022, and does not seem to include the potential benefits of a number of pending or possible transactions:

- An $1.7bn (plus interest) payment will be received from Philip Morris by July 2023 as part of its agreement to regain its U.S. IQOS license

- $1.3bn will be spent to retire existing debt, despite Altria’s Net Debt / EBITDA now being back to 2.1x and its total debt being only 4% higher than the pre-Juul 2018 year-end figure ($26.7bn vs. $25.7bn)

- The $1.1bn Anheuser-Busch InBev ( BUD ) stake now seems likely to stay; management stated on the call that there is nothing new to report and they believe keeping it is in shareholders’ long-term interest

More buybacks would have created value given Altria’s current low P/E. We do not believe the above represents good capital allocation, though it is possible that management is pessimistic about future earnings and/or conserving firepower for a significant strategic acquisition.

Philip Morris Is A Real Threat From 2024

Philip Morris has now taken control of Swedish Match ((SWMA)), but the latter’s U.S. smokefree sales are relatively small ($257m in Q3 2022). PM will not regain its U.S. rights on IQOS until after April 2024, and its other products will likely not receive U.S. marketing approvals from the FDA for some time. (PM only plans to submit a PMTA for its VEEV E-Vapor product in “early 2023”). We believe PM can be a real threat to Altria earnings, but only from H2 2024.

Altria’s own Reduced Risk Products efforts are similarly unlikely to produce material results for some time. On the Q4 earning call, management stated that the internal development of its own Heated Tobacco product is still being finalized. As we described in our last article , Altria only expects to file a PMTA for its Heated Tobacco Capsule by 2024 year-end, and to file a PMTA with Japan Tobacco ( JAPAY ) for a Heated Tobacco device from the latter in H1 2025.

Altria management has promised to share more details on their Reduced Risk Products at an investor day in March.

Altria Stock Valuation

At $47.06, Altria shares trade at a correspondingly undemanding 9.6x 2022 EPS; cashflow figures were not included in Q4 2022 results but, based on 2021 financials, Free Cash Flow (“FCF”) Yield is likely to be just above 10%:

| Altria Valuation & Cashflows (2018-2 2 ) Source: Altria company filings. |

Relative to the midpoint of the 2023 EPS guidance ($4.98-5.13), Altria's P/E multiple is 9.3x.

The Dividend Yield is 8.0%, from a dividend of $0.94 per quarter ($3.76 annualized), which was raised by 4.4% in August 2022. Altria targets an 80% Payout Ratio.

Altria Stock Forecasts

We keep most of our forecast assumptions unchanged:

- 2023 EPS of $5.06, mid-point of outlook (was $5.15)

- From 2024, Net Income growth of 4% (unchanged)

- Share count to fall by 1% in 2023 then 2% annually from 2024 (was 2% for all years)

- Dividend Payout to be 80% (unchanged)

- P/E at 9.5x at 2025 year-end (unchanged).

Our new 2025 EPS forecast of $5.69 is 2% lower than before ($5.80):

| Illustrative Altria Return Forecasts Source: Librarian Capital estimates. |

With shares at $47.06, we expect an exit price of $54 and a total return of 44% (15.4% annualized) by 2025 year-end.

These figures reflect our base case, our view of what is most likely to happen. However, there are significant tail risks. On the negative side, Philip Morris may take share in the U.S. market quickly and significantly from 2024; on the positive side, there will be significant upside if the U.S. cigarette market remains undisrupted.

Is Altria Stock A Buy? Conclusion

We reiterate our Buy rating for now, but will monitor Altria Group, Inc. closely.

For further details see:

Altria: Earnings Growth Despite Bad 2022 Macro, But Little Other Good News