CRON - Altria Group: Attractive Heading Into Q3 Earnings Despite Continued Pain

2023-10-21 23:41:20 ET

Summary

- Altria Group is expected to announce financial results for Q3 of its 2023 fiscal year, with analysts predicting a decline in revenue compared to the previous year.

- The company's market share for cigarettes continues to drop, and declining smoking rates in the US are impacting sales.

- Despite these challenges, the company's profitability metrics are expected to improve, and shares of Altria Group are trading at attractive valuations.

Later this month, on October 26th, the management team at tobacco giant Altria Group ( MO ) is expected to announce financial results covering the third quarter of the company's 2023 fiscal year. Leading up to that time, analysts had some mixed expectations . And to be honest, they are right too. Financial performance achieved by the company has not been the most stable in recent quarters and there is considerable uncertainty regarding the firm's ability to replace the income stream generated by tobacco products with newer offerings.

This is not to say that investors should be bearish at this time. Based on the data currently available, the cash flow picture for the company will likely come in strong and investors will finally get their first look at the progress management is making regarding its acquisition of NJOY earlier this year. Add on top of this the fact that shares of the company look incredibly cheap and that the hefty 9.3% yield is comfortably supported, and I would say that this picture definitely tilts positive.

Keep an eye on headline news

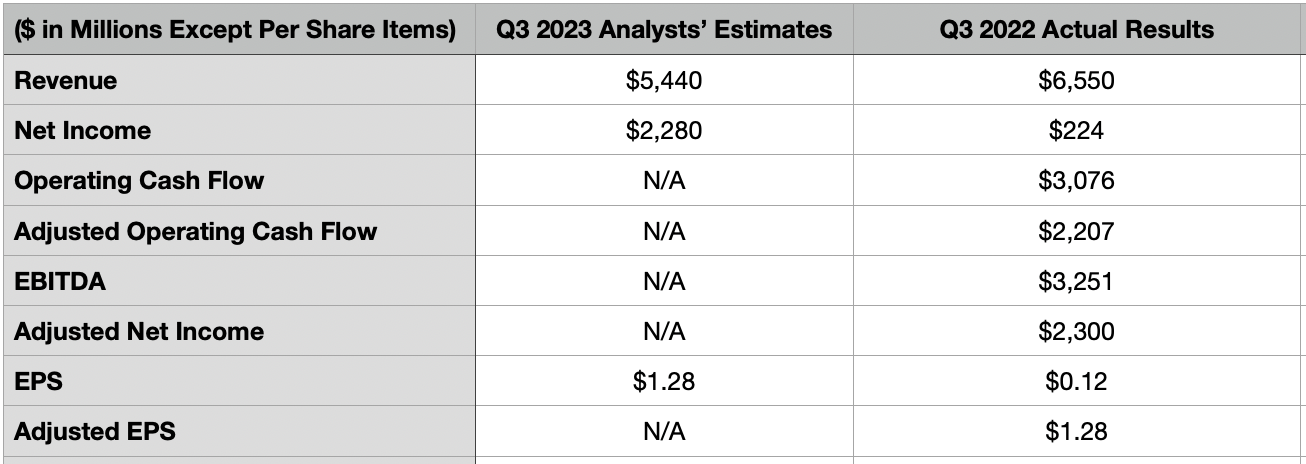

On October 26th, before the market opens, the management team at Altria Group will announce financial results covering the third quarter of the company's 2023 fiscal year. Given that this article is focused on what investors should be looking for in general, it might be appropriate to start with the headline news items that will be made public first. At present, analysts are forecasting revenue for the third quarter of $5.44 billion. Although this is a tremendous amount of money, it would actually represent a decline of 16.9% compared to the $6.55 billion the company reported one year earlier.

{kind=link}

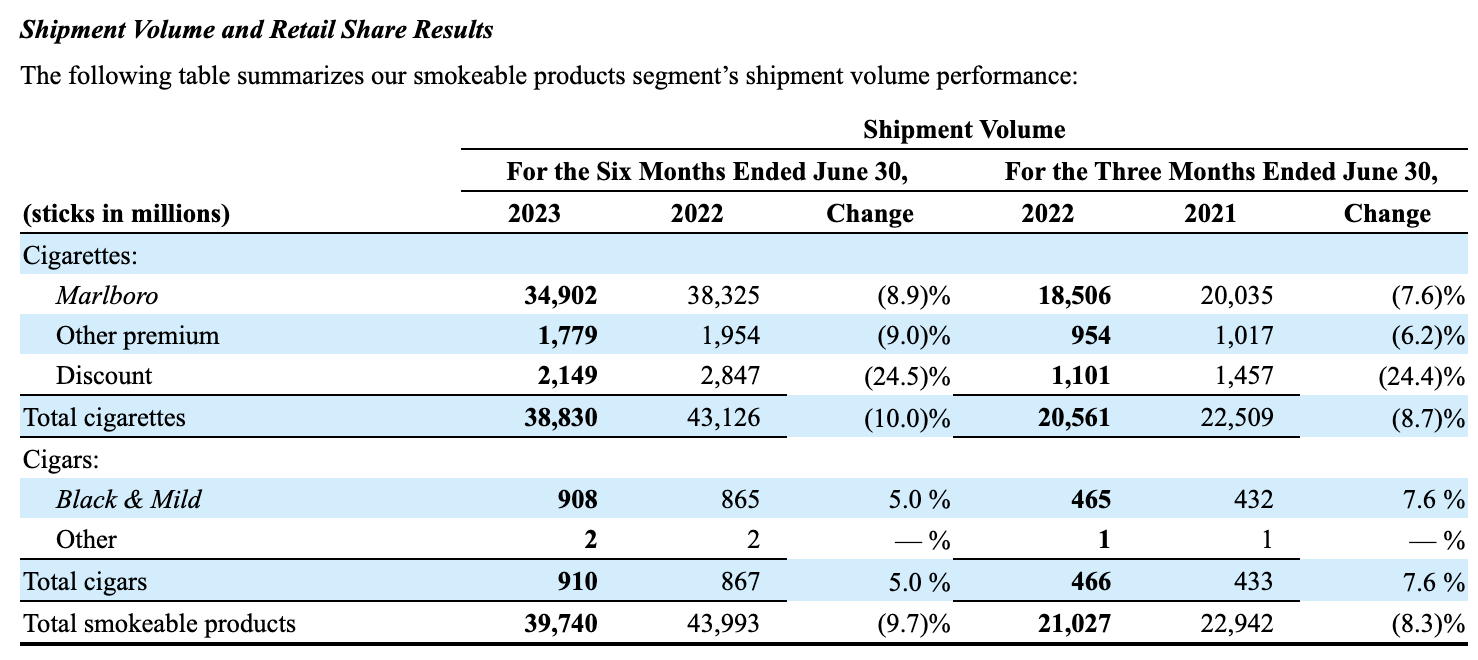

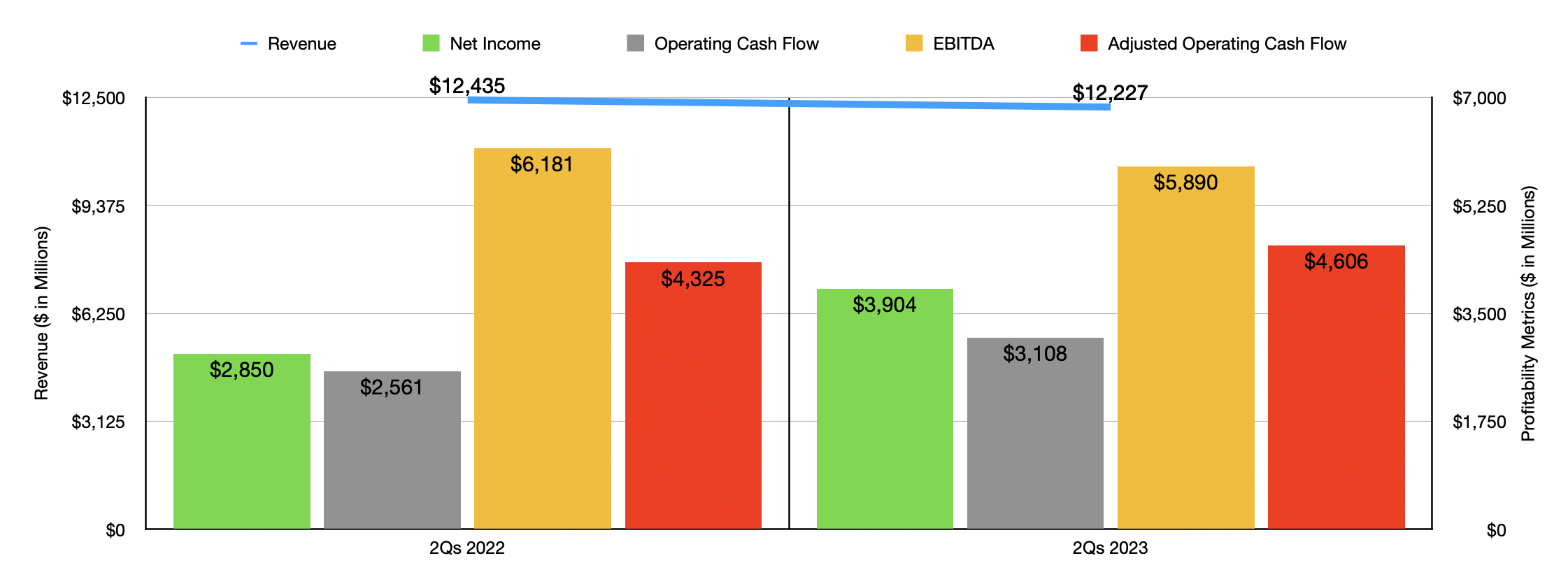

Truth be told, I find such a sizable drop in revenue to be unlikely. Don't get me wrong. The fact of the matter is that Altria Group is facing some long-term issues that have impacted sales. In the first half of the 2023 fiscal year , for instance, the company reported revenue of $12.23 billion. This was down 1.7% compared to the $12.44 billion generated one year earlier. Even though the company has been increasing prices recently, those have been more than offset by a decline in total cigarette and cigar shipments. In the first half of the 2023 fiscal year, the enterprise reported shipments of 38.83 billion ‘sticks’ worth of cigarettes. That's 10% lower than the 43.13 billion reported at the same time one year earlier. Cigar shipments did increase a modest 5%. But at 910 million ‘sticks’ during the first two quarters of the 2023 fiscal year, they represent a very small portion of the company's overall revenue stream.

{kind=link}

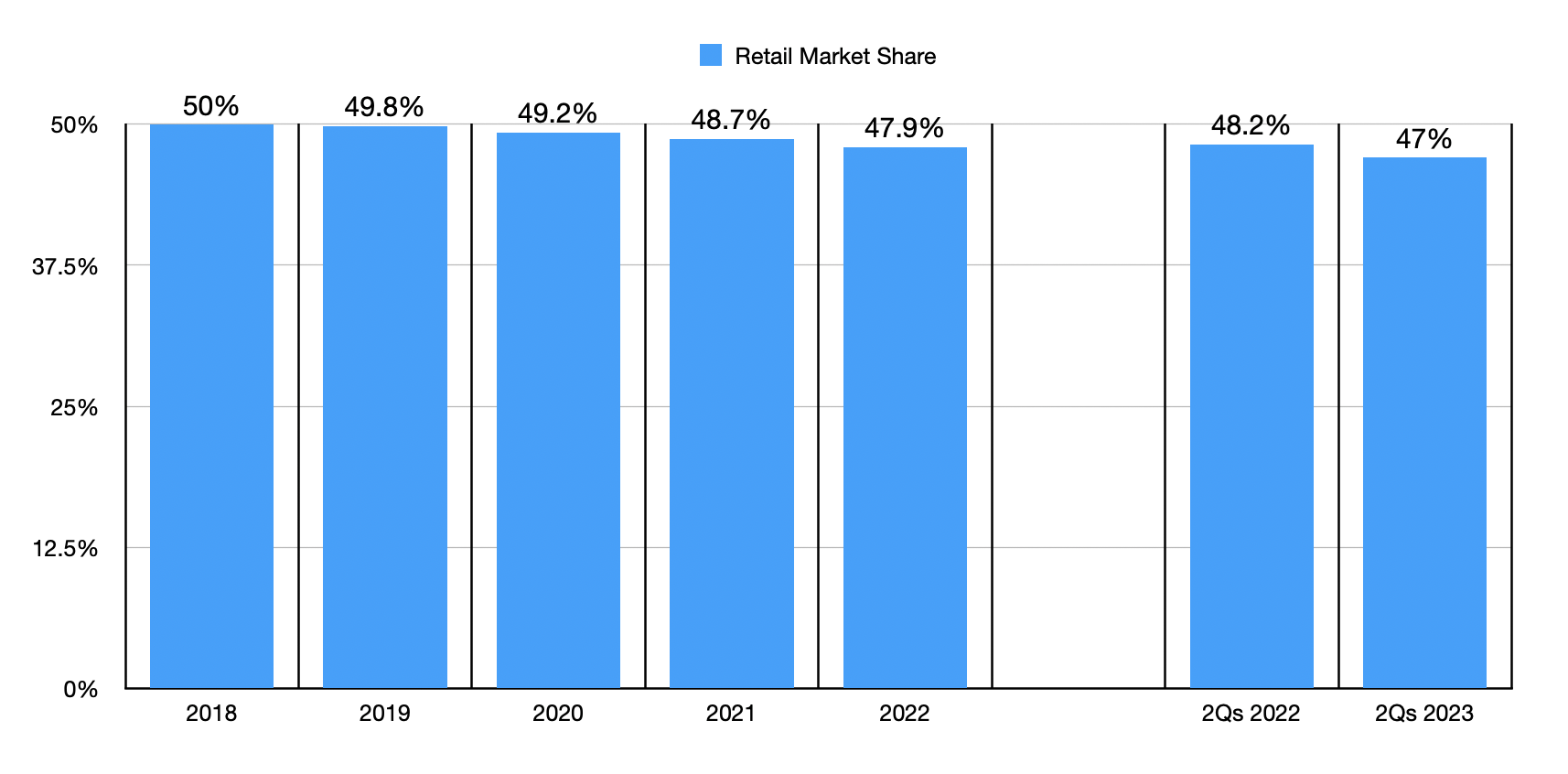

As I wrote about in a prior article , there have been signs that the recent price increases by the company could be a harbinger of additional pain to come. But those price increases occurred shortly before the second quarter earnings release. So this would be the quarter in which we see some impact on that front and whether or not a decline in shipments occurred. In general, investors should expect a trend of declining shipments from year to year. And this is because smoking rates in the US are well on the decline. But it goes beyond just that for Altria Group. The fact of the matter is that its retail market share for cigarettes continues to drop as well. At the end of the most recent quarter, covering the first half of 2023 in its entirety, the company had a 47% retail market share. That's down from the 48.2% seen one year earlier. It's important to note that this is not a one-time dip. The fact of the matter is that the company's market share has been declining for some time. For all of its cigarette products combined, the market share was at 50% back in 2018. And by 2022, it had fallen to 47.9%.

{kind=link}

When it comes to the bottom line, analysts are forecasting profits per share of $1.28. This would represent a surge over the $0.12 per share reported the same quarter last year and it would match the $1.28 per share in adjusted earnings for that time. Although I am always skeptical of using adjusted earnings, I do believe that they should be considered on a case-by-case basis. And given the nature of the adjustments for this particular enterprise, I would argue that the adjusted earnings would be the better way of evaluating the company. Of course, this does not mean that net profits will remain flat. In the third quarter of 2022, they totaled $2.30 billion. But the fact of the matter is that the company has decreased its share count since then. Using the most recent share count figures provided for the second quarter of this year, we would expect net income of $2.28 billion.

Analysts have not provided guidance for any other profitability metrics. But there are certain ones that investors would be wise to keep an eye out for. Operating cash flow is one of these. In the third quarter of last year, it totaled $3.08 billion. If we adjust for changes in working capital, it would be slightly lower at $2.21 billion. And then there is EBITDA, which totaled $3.25 billion in the third quarter of 2022. Obviously, we should also be keeping an eye out on guidance for the year. The most recent guidance provided by management called for adjusted earnings per share of between $4.89 and $5.03. That would be up from the $4.84 reported for 2022.

{kind=link}

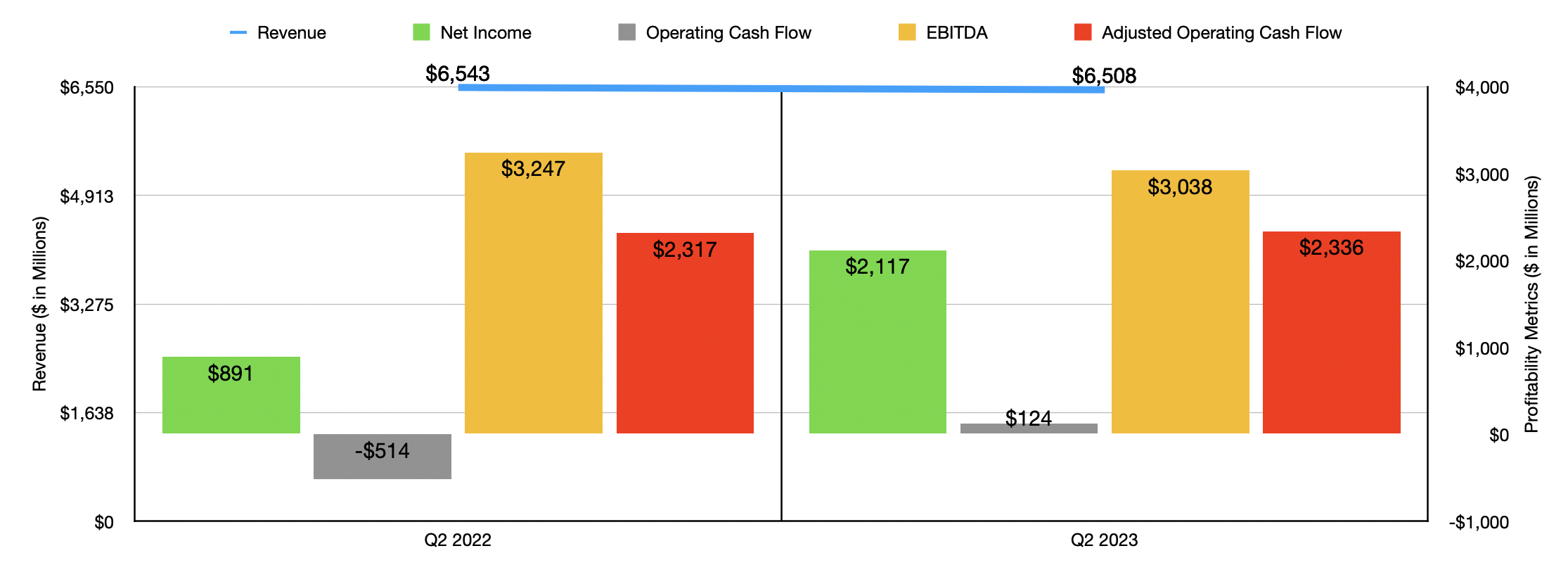

This does not mean that some volatility would be unexpected. As you can see in the chart above, financial performance on both the top and bottom lines for the company has been a bit volatile, particularly when it comes to net income and operating cash flow during the second quarter of this year relative to the same time last year. But for the first six months of the year as a whole, all profitability metrics improved year over year with the exception of EBITDA. And with the aforementioned price increases, so long as volume does not surprise in a significantly negative way, it's likely that the company can post continued improvements on the bottom line for the third quarter.

{kind=link}

Other items to be watchful of

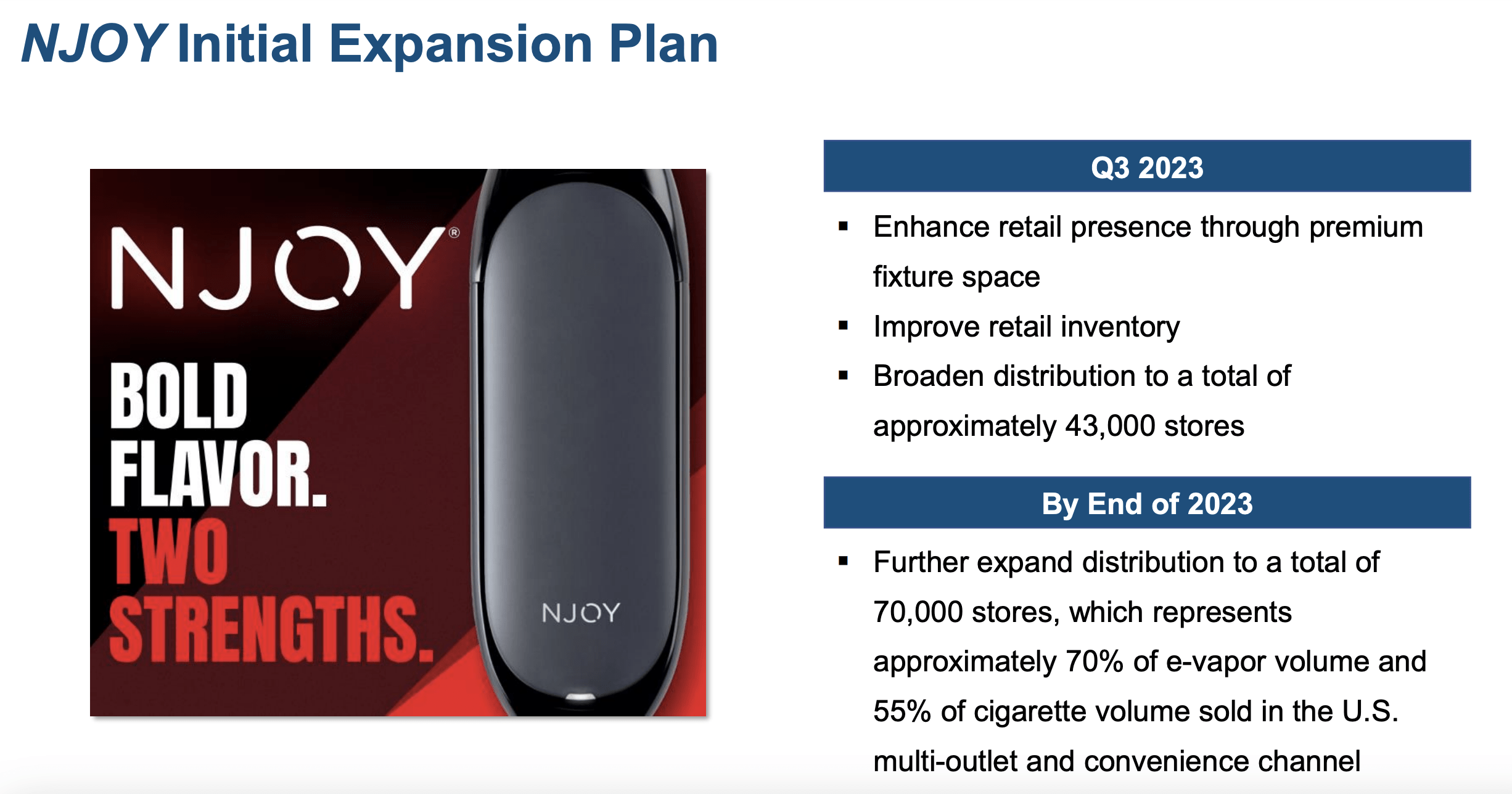

Outside of the headline news, there are some other items that will be very important for investors to pay attention to. Top of mind for many investors will be the NJOY brand that the company acquired. That purchase was completed in early June of this year. So a lot of focus will be on how well that asset is playing out. For $2.75 billion, plus contingencies of up to another $500 million, there's a lot at stake for Altria Group and its investors, particularly when you consider the company's long-term ambitions as I detailed in a prior article .

One thing that we do know is that management has already provided some outlook as to what they expect for this brand in the near term. For the third quarter, the company had planned to improve retail inventory and to broaden distribution of the brand to somewhere around 43,000 stores. But this is only the start. Their goal is to, by the end of 2023, expand distribution to roughly 70,000 stores, accounting for 70% of all e-vapor and 55% of cigarette volume sold across the nation using both the multi-outlet and convenience channels.

{kind=link}

There are a couple of other items that investors should be paying attention to. In late August, for instance, the company had NJOY file a complaint against JUUL Labs with the US International Trade Commission. In that complaint, the company called for a ban on the importation and sale of some JUUL e-vapor products. The reason behind this proposed ban is that Altria Group believes that some JUUL products are infringing upon certain patents that are currently owned by NJOY. A similar complaint was filed by the company in the US District Court in Delaware.

Another topic that I think some might be focused on is the distribution that the company pays out. Declining sales are not exactly a sign of strong distributions in the long run. While I am concerned about the picture several years out from now, I would argue that the distribution, which has resulted in a 9.3% yield as of this writing, is not at risk. This is because, in the first half of this year, the company paid out $3.37 billion in distributions. That stacks up against the $4.61 billion in adjusted operating cash flow seen during the same window of time. That implies a 73.1% distribution coverage. Of course, there are capital expenditures to take into consideration. But given the nature of Altria Group, those are fairly small. In the first six months of this year, they totaled only $103 million. We can and should expect them to increase moving forward because of the aforementioned NJOY purchase. But I can't see the picture worsening to the extent of jeopardizing the distribution.

To be perfectly honest with you, I would prefer that the company did not pay out a dividend. I understand that dividends are important for many different types of investors, particularly retirees. They also offer certain benefits like a guaranteed return that helps offset a decline in price if a long-term holding plunges after many years of ownership. In general, however, I am of the mindset that allocating capital toward attractive investments can generate better returns down the road. Though to be completely honest with you, confidence in this strategy when it comes to Altria Group has not exactly paid off. Back in 2018, for instance, the company acquired a 35% stake in JUUL Labs that it later exchanged at an implied value of only $250 million for heated tobacco intellectual property rights owned by JUUL Labs itself.

Though nowhere near as large as the $12.8 billion the company allocated toward acquiring its stake in JUUL, there have been other investments that so far are not working out. A few years ago, the company allocated $2.4 billion toward a large minority ownership interest in Cronos Group ( CRON ) that included some warrants with it. Last year, the company abandoned the warrants, recognizing a $483 million loss. And as of this writing, the common units that it has in the company are only worth about $293 million. And then there's its current ownership of Anheuser-Busch InBev SA/NV ( BUD ). At present, the company owns 197 million shares in the company, a stake that is worth $10.56 billion. However, at the end of last year, that stake was worth about $11.9 billion. The sizable drop in value during this time was driven by an overreaction that seems to continue to the current day. But unlike the other situations, this is one that I am bullish on.

Shares look cheap

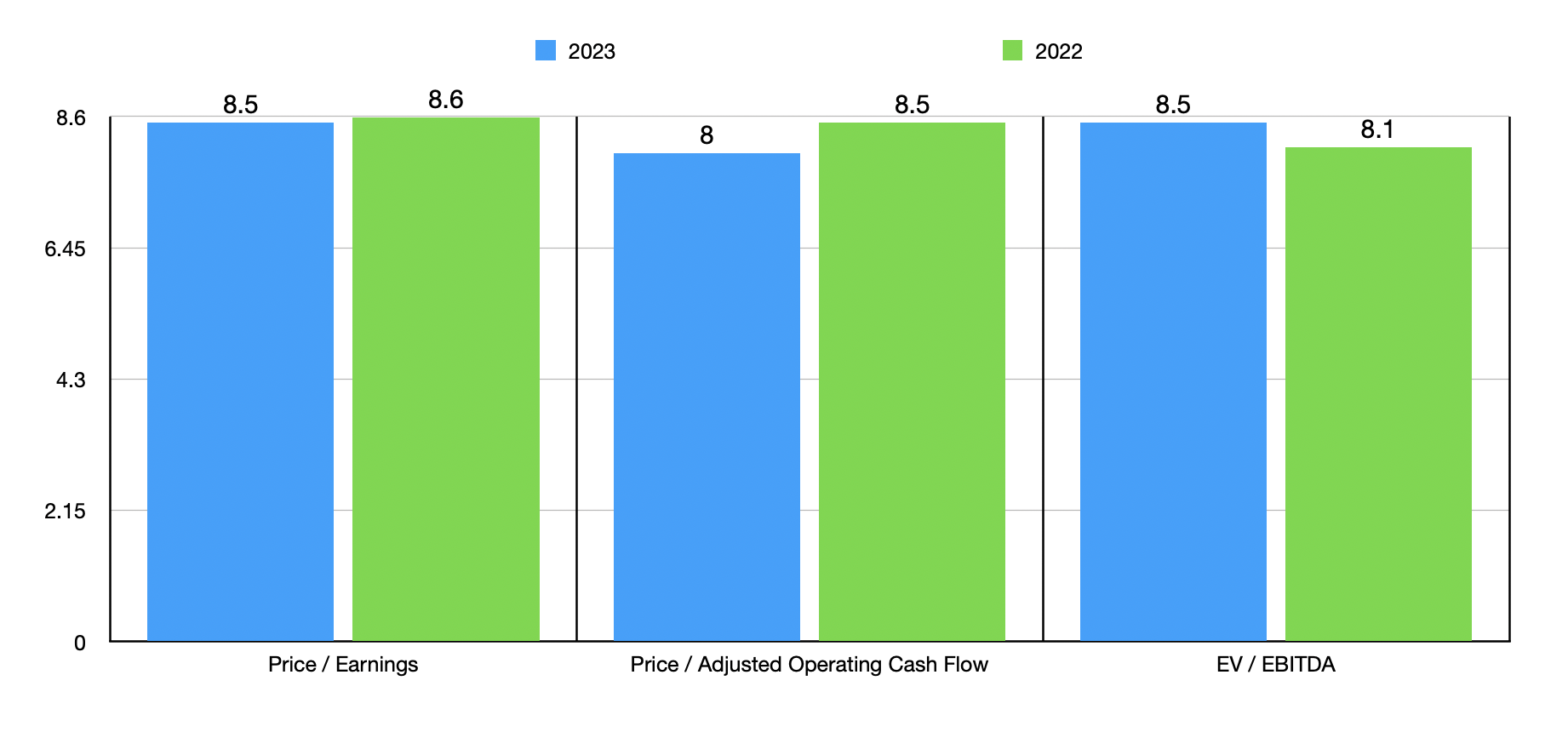

The last thing I would like to touch upon is the fact that shares of Altria Group look quite appealing from a valuation perspective at this time. Using the estimates provided by management for earnings, I then estimated other profitability metrics for the year. I believe that adjusted operating cash flow is likely to come in at around $9.42 billion, while EBITDA should be higher at $11.94 billion. As you can see in the chart below, the company is trading at multiples that are in the single digits. And using the estimates for this year, the stock is cheaper than if we were to use data from last year using two of the three metrics. When you have a hefty yield coming from a company and that company is trading in the single digits, that is definitely something to be optimistic about.

{kind=link}

Takeaway

Truth be told, nobody knows what will happen when earnings get released. Analysts seem to be neutral on profits and pessimistic on revenue. What we do know is that the company continues to generate strong cash flows. But the decline in shipments, as well as the uncertainty that persists about the company's alternative growth avenues, does not bode well for the picture in the long run. For now, matters are not terribly problematic. In fact, the picture is so positive from a fundamental perspective that, if it weren't for these other issues, I would rate the company a ‘strong buy.’ But until we see some path for the long run, the best that I can rate the company is a ‘buy’.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Altria Group: Attractive Heading Into Q3 Earnings Despite Continued Pain