JAPAF - Altria: Multiple Disappointments From Investor Day

2023-03-24 07:31:53 ET

Summary

- Altria shares fell 3.7% on Thursday after its investor day, more than other tobacco stocks. They have fallen 17% in the past year.

- The dividend is moving from an 80% payout ratio to a mid-single-digit annual increase as EPS will likely become more volatile.

- The Medium-term EPS CAGR target has been set at mid-single-digits, formalizing a deceleration from the pre-Juul range of 7-9%.

- The Japan Tobacco JV's product will only be ready after 2026, and the new Heated Tobacco Capsule product was underwhelming.

- There is no indication the ABI stake will be sold in the near term. We are left with few positives except Altria's 8.7% Dividend Yield.

Introduction: Why Is Altria Stock Down?

Altria Group Inc. (MO) held an investor day on Thursday (March 23). Altria shares finished the day down 3.7% (partly due to Thursday being the ex-dividend date ) and are now down 17% in the past year:

| Altria Share Price (Last 1 Year) Source: Google Finance (23-Mar-23). |

We have had a Buy rating on Altria since our upgrade in February 2020. Altria stock has been a disappointment since then, returning only 13.7% in three years, with dividends offsetting an 8.6% decline in the share price.

The investor day gave multiple disappointments. The dividend is moving from an 80% Payout Ratio to a mid-single-digit annual growth target, explicitly signalling near-term volatility in Altria's EPS. Medium-term EPS CAGR target has been set at mid-single-digits, formalising the deceleration from the 7-9% range before Juul's emergence. Cigarette industry price elasticity has been revised upwards from 0.30 to 0.35. The NJOY acquisition seems to rely on the FDA banning leading competitors from the market. It was confirmed that the new Heated Tobacco JV with Japan Tobacco will only applying for FDA approval for its product in 2025, and the unveiling of Altria's internally-developed Heated Tobacco Capsule device was underwhelming. There is no indication that ABI stake will be sold in the near term, despite the offset now available from Juul tax losses. We are left with few positives except Altria's 8.7% Dividend Yield and its likely moderate growth in the next few years. We reiterate our Buy rating on but continue to monitor the situation closely.

Moving Away From 80% Dividend Payout

The key announcement on Thursday was a move in Altria's dividend policy from an 80% Dividend Payout Ratio target to a mid-single-digit annual growth target, with CFO Sal Manuco posting a standalone letter to explain the reasoning.

The 80% Payout Ratio has been in place since 2010; removing it marks a major change. In essence, Altria now expects its EPS to be more volatile and does not want this to affect dividend expectations. As Manuco wrote in the letter:

As we invest in our Vision, earnings growth may be slightly more variable year-to-year compared to our history of steady and consistent growth … Therefore, to provide investors with confidence in consistent dividend growth, we are establishing a new progressive dividend goal that targets mid-single digits dividend growth annually."

Not only is Altria's EPS expected to be more volatile, its growth is expected to be lower as well

Formalizing Post-Juul EPS Deceleration

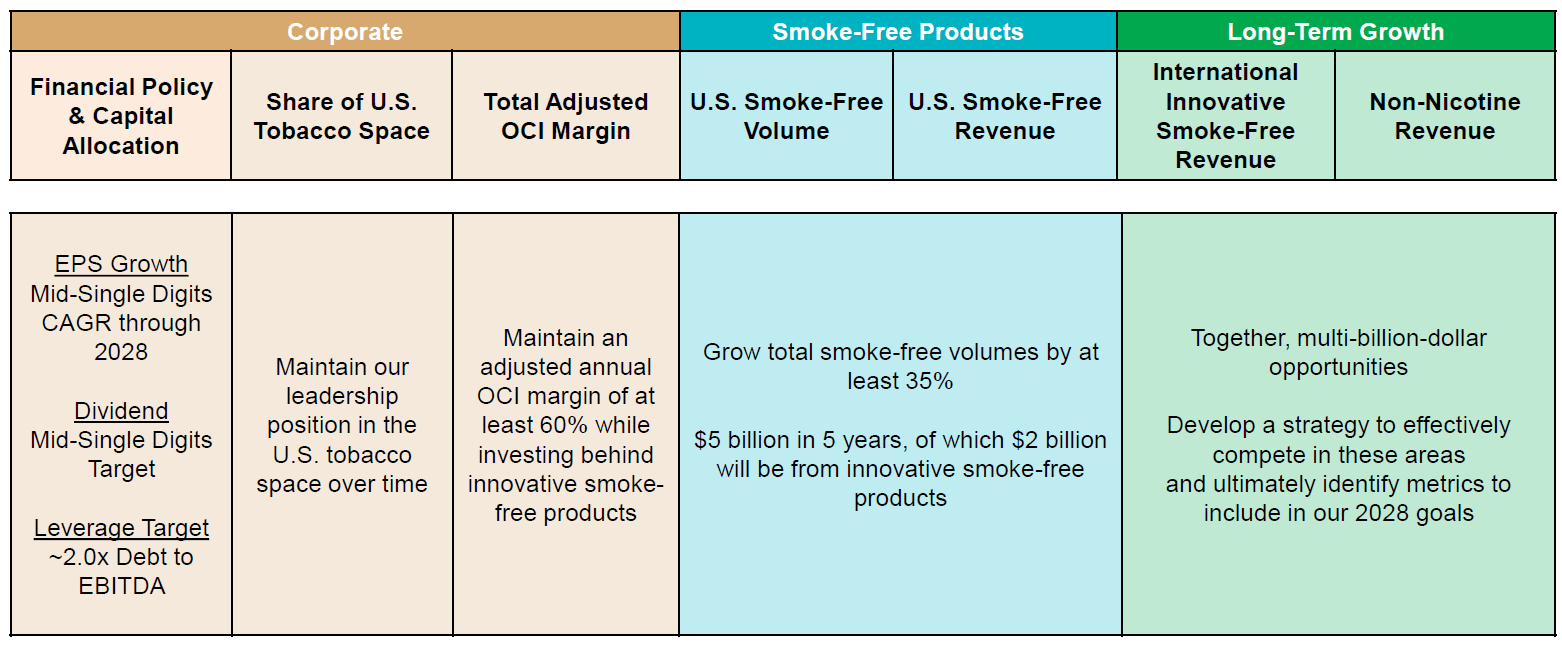

A medium-term mid-single-digits EPS CAGR was among the 2028 targets announced at the investor day:

{kind=link}

While a mid-single-digit EPS CAGR is roughly in line with the 4-7% EPS CAGR target announced at Q4 2019 results (on January 30, 2020), the latter was a downward revision after Altria decided it would no longer expect any equity earnings contributions from Juul through 2022. Altria's 2020-22 EPS CAGR target was 5-8% before this revision and, before Q3 2019 results , management had historically targeted an EPS CAGR range of 7-9%. The new mid-single-digits EPS CAGR target is thus an explicit admission that growth will not return to pre-Juul levels in the medium term.

The target to "maintain an adjusted annual OCI (Operating Companies Income) margin of at least 60% while investing" similarly signals an acceptance of how the competitive landscape has changed, as it implies a minimal amount of margin expansion from the 59.6% already achieved in 2022 (including 59.0% in Smokeables and 66.3% in Smokefree).

Cigarette Price Elasticity Has Increased

For its core cigarette business, Altria has also revised its estimate of the national price elasticity coefficient upwards from 0.30 to 0.35. (The estimate for the secular decline rate has been kept unchanged at 2.5%.)

If we take pre-COVID 2019 figures as an example, what this change means is that the same price increase that previously created a volume decline of 1.2% for the industry will now create one of 1.4%:

| U.S. Cigarette Industry Volume Decline by Component (Rolling 12 Months) Source: Altria results presentation (Q4 2019). |

While the impact appears minor, it is another acknowledgement that the U.S. cigarette market may be becoming less stable. The price elasticity coefficient is also for the whole industry, and in recent years Altria has lost volume 1.5-2.0 ppt faster than the industry each year because of its higher price and some smokers trading down to discount brands.

NJOY Benefits May Rely on the FDA

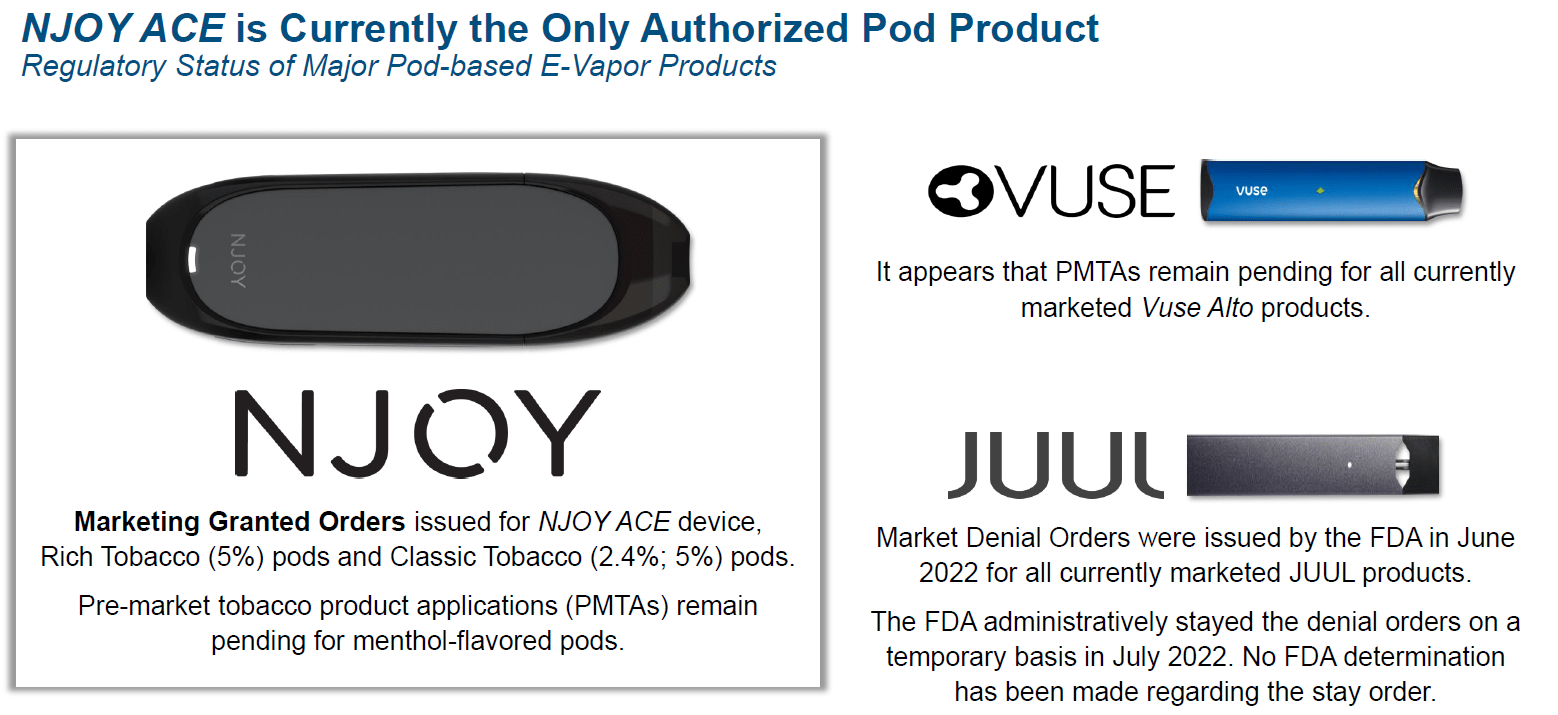

Altria comments at the investor day also imply that benefits from the NJOY acquisition may rely on the FDA banning British American Tobacco's (referred here as "BAT") ( BTI ) Vuse Alto and/or Juul from the market.

In their presentation, management again highlighted how "NJOY ACE is currently the only authorized pod product", and that BAT's Vuse Alto products remain unapproved while Juul products have been issued with Marketing Denial Orders:

{kind=link}

Our base case is that both Vuse Alto and Juul will eventually receive FDA marketing authorizations. Juul is appealing the FDA's decision and has obtained a temporary stay, while BAT has received authorizations for some of the less popular Vuse products. Both Vuse Alto and Juul products remain on sale. We note that, for Altria's nicotine pouch portfolio, COO Jody Begley acknowledged that "PMTAs for the entire on! portfolio remain pending with the FDA".

FDA Marketing Denial Orders so far seem to be targeted at either flavored products (including menthol) or manufacturers with a perceived poor record of preventing under-age usage. Altria evidently believes the latter is the key, and is developing Bluetooth-enabled age verification technology that it plans to use in a PMTA for a menthol product.

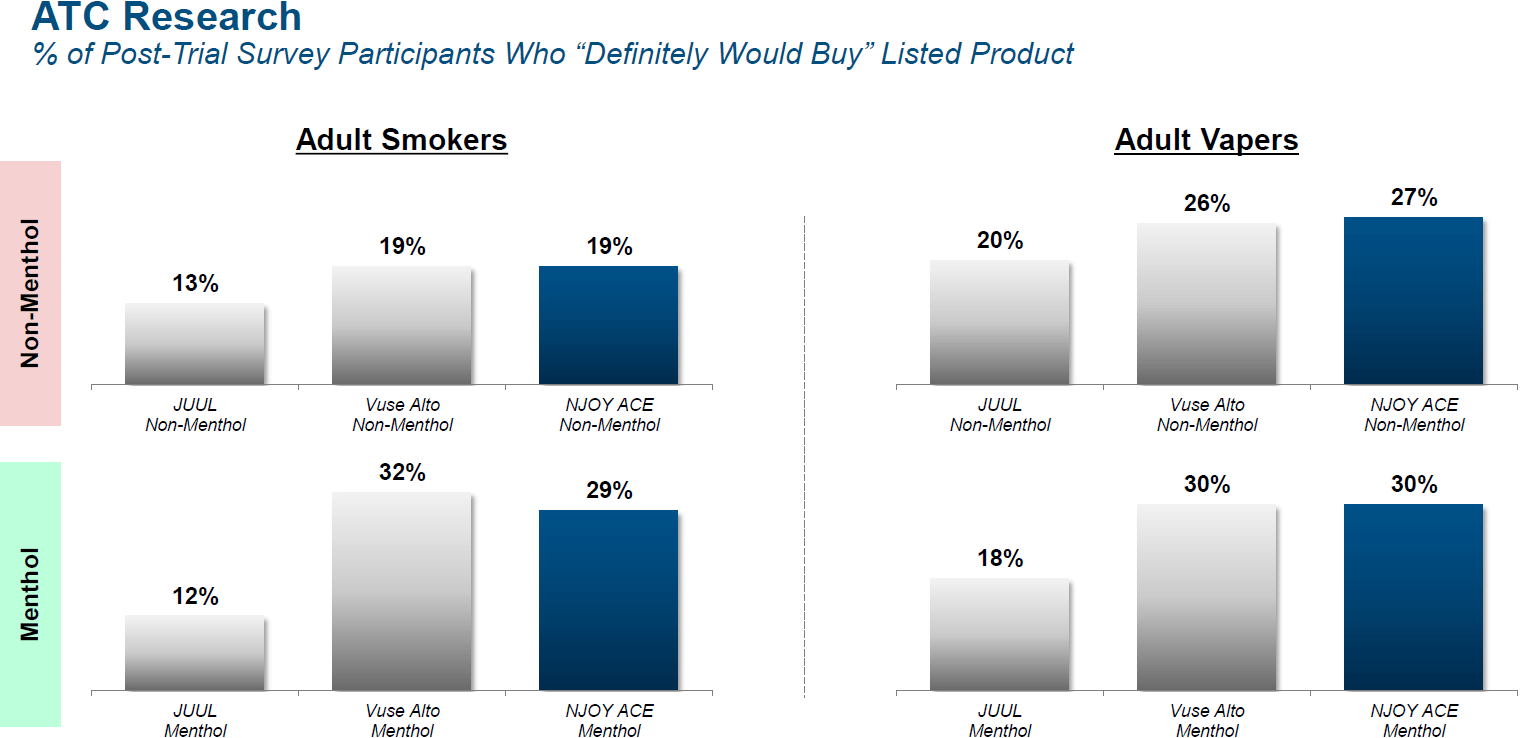

Another reason benefits from NJOY may depend on the FDA is that Altria's consumer surveys have continued to show that it receives similar to slightly lower preferences compared to BAT's Vuse Alto, though doing much better than Juul:

{kind=link}

We continue to expect benefits from the NJOY acquisition to be modest, as we explained when talks were first reported.

Heated Tobacco JV Product A Long Way Off

The Heated Tobacco JV with Japan Tobacco ( JAPAY ) is confirmed to be applying for marketing approval for its product only in 2025. As COO Jody Begley remarked:

The teams plan to formally begin regulatory preparations later this year and plan to file a PMTA in the first half of 2025 and a modified risk tobacco product ("MRTP") application later that year."

Given a PMTA authorization can take a few years, this means it can be received several years after Philip Morris ( PM ) has launched IQOS in the U.S., likely to be immediately after it has regained U.S. rights after April 2024.

Altria confirmed that it will be selling Marlboro branded heatsticks with this new product. Again, as Begley said:

Our research indicates that some of the smokers looking for an innovative heated tobacco product are hesitant to try something entirely new and can be overwhelmed by too many choices. We believe the Ploom system can appeal to this particular audience, as the stick format provides a familiar tactile experience to cigarettes. When paired with the Marlboro brand, we expect Ploom to be an approachable and familiar heated tobacco proposition for U.S. smokers."

Philip Morris's experience with IQOS outside the U.S. shows that the relevance of the Marlboro brand to a Reduced Risk Product may be limited. As PM CEO Jacek Olczak said on PM's Q3 2022 earnings call :

IQOS TEREA in Japan is now by X factor bigger than the HeatSticks Marlboro. And this was the last market which we still have been using a Marlboro trademark of our heat-not-burn consumables.

And as you know, at the very beginning, six or so years ago in a few markets, I recall it was Switzerland and Italy, we started with Marlboro and, very early in the journey, we have almost overnight … rebranded that thing and we dropped the Marlboro from the brand, from the proposition."

IQOS's expansion in Europe has largely been conducted with the HEETS or HeatSticks brands.

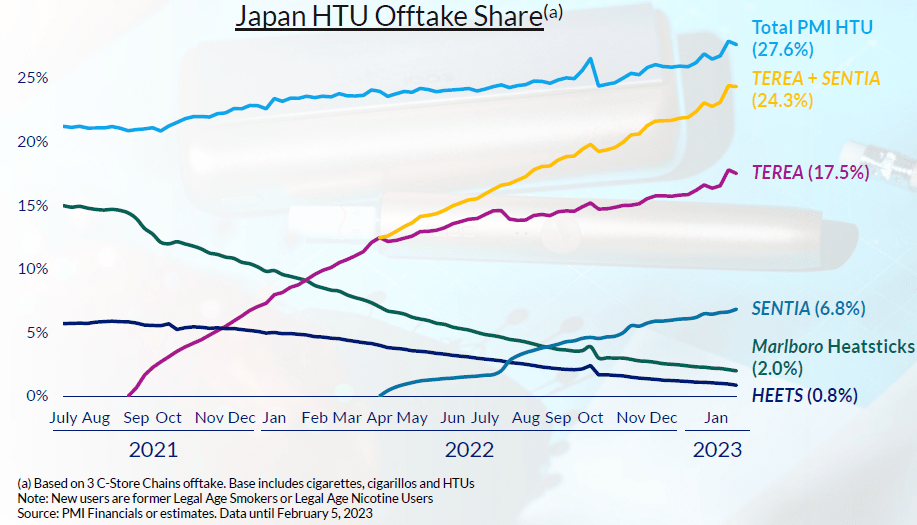

IQOS did start with Marlboro Heatsticks in Japan. However, by October 2018, on reaching around 15% share of the tobacco market, PM introduced HEETS as an additional, lower-priced range. Marlboro Heatsticks' market share was still around 15% in 2021, when the TEREA brands was introduced, followed by SENTIA a year later. The share held by Marlboro Heatsticks has been falling as it is being phased out, and was down to 2.0% by January 2023:

{kind=link}

Every other Tobacco company, including BAT, Imperial Brands (IMBBY), Japan Tobacco and the former Swedish Match (SWMAY) has opted for new names rather than their existing brands for their modern Reduced Risk Products.

We do not believe the use of the Marlboro brand will be a material advantage by the time the new product from the Altria / Japan Tobacco JV is ready after 2025.

Weak Heated Tobacco Capsule Unveiling

The unveiling of Altria's internally-developed Heated Tobacco Capsule ("HTC") device was underwhelming.

| Altria's New HTC Device Source: Altria investor day presentation (2023). |

Named SWIC, the new HTC device is supposed to heat tobacco-filled capsules to deliver an inhale. We are cautious of the new device because it is too different from cigarettes in both form factor and touch, both of which are important to persuade smokers to accept a Reduced Risk Product as a cigarette substitute. Indeed Altria seems to describe SWIC as a product for a remaining minority of smokers left by e-vapor and Heated Tobacco:

Some smokers are interested in innovative heated tobacco products that bear less physical resemblance to traditional cigarettes. This includes the millions of U.S. smokers who tried, but ultimately rejected, e-vapor products. These consumers are self-conscious about the image of being a smoker. And, they find heated tobacco stick products cumbersome and complex. This is where our new heated tobacco capsule product fits in."

In addition, SWIC was described as "still in development" and no further details were provided on its timetable.

No News on ABI Stake

There is no indication that Anheuser-Busch InBev ( BUD ) stake will be sold in the near term. Management stated that:

We continue to evaluate the stake as a financial investment and our goal remains to maximize the long-term value of the investment for our shareholders."

This is despite the offset now available from Juul tax losses, which totalled $12.5bn (substantially all of the $12.8bn invested back in 2018), and should be enough to offset both the gain from the IQOS rights (for which PM is paying $2.7bn plus interest) and the gain on the ABI stake (now worth around $11bn, on a cost basis of $3bn).

Altria Stock Valuation

We are left with few positives except Altria's 8.7% Dividend Yield and its likely moderate growth in the next few years

At $43.46, relative to 2022, Altria shares have a 8.9x P/E and a 10.9% Free Cash Flow ("FCF") Yield; however, 2022 included a $1bn cash payment from PM related to the agreement for Altria to return U.S. IQOS rights:

| Altria Valuation & Cashflows (2018-22) Source: Altria company filings. |

Relative to the midpoint of the 2023 EPS guidance ($4.98-5.13), Altria's P/E multiple is 8.6x.

The Dividend Yield is 8.7%, from a dividend of $0.94 per quarter ($3.76 annualized). Excluding the one-off PM payment, Altria currently has about $1bn of surplus cashflow after paying the dividend, which now costs $6.7bn. There is likely enough headroom for Altria to raise its dividend by mid-single-digits annually as per the new target.

Altria's Net Debt / EBITDA was 2.1x at 2022 year-end, against the target of 2.0x. Buying NJOY for $2.75bn and buying back $1bn of shares in 2023 as planned will likely use up the second, $1.7bn plus interest PM payment for IQOS and the post-dividend FCF of around $1bn. This means deleveraging this year will primarily be driven by EBITDA growth.

Altria Stock Forecasts

We lower our forecast assumptions slightly

- 2023 EPS of $5.06, mid-point of outlook (unchanged)

- From 2024, Net Income growth of 3.5% (was 4.0%)

- Share count to fall by 1% in 2023, then 1.5% annually from 2024 (was 2.0%)

- Dividend Payout to grow 5% annually

- P/E at 9.5x at 2025 year-end

Our new 2025 EPS forecast of $5.58 is 2% lower than before ($5.69):

| Illustrative Altria Return Forecasts Source: Librarian Capital estimates. |

With shares at $43.46, we expect an exit price of $53 and a total return of 53% (19.3% annualized) by 2025 year-end.

These figures reflect our base case, our view of what is most likely to happen. However, there are significant tail risks. On the negative side, Philip Morris may take share in the U.S. market quickly and significantly from 2024; on the positive side, there will be significant upside if the U.S. cigarette market remains undisrupted.

Is Altria Stock A Buy? Conclusion

We reiterate our Buy rating for now, but will monitor the situation closely.

For further details see:

Altria: Multiple Disappointments From Investor Day