BUDFF - Altria Stock Q1 Earnings Preview: What To Watch For

2023-04-20 09:00:29 ET

Summary

- Altria Group, Inc.'s Q1 results will be released on Thursday, April 27 - a month after the company somewhat disappointed investors with the news announced at its recent investor day.

- In this update, I'll point out four aspects worth paying attention to in Altria's upcoming earnings call.

- I will also explore the question of whether MO is still a safe stock to invest in or whether there are signs that the stock has become a value trap.

Introduction

U.S. tobacco company Altria Group, Inc. ( MO ) will release its first-quarter earnings on Thursday, April 27 at about 7 a.m. and hold a conference call at 9 a.m. I've covered Altria stock several times before, with my last article focusing on the tobacco giant's 2022 full-year results.

In the meantime, Altria held an insightful investor day event where management gave updates on the smoke-free portfolio, particularly as it relates to vaping and heated tobacco. The company also updated its dividend policy , thereby implicitly suggesting higher earnings volatility going forward.

Following the somewhat discouraging investor day event, and with first quarter results just around the corner, it's a good time to re-evaluate whether Altria is still a safe stock to buy. In this update, I'll point out four aspects worth paying attention to in Altria's upcoming earnings call.

Combustibles Volumes And Inflation

For 2022, Altria reported a volume decline of nearly 10% in its combustible products segment. As always, the secular decline in the industry played a big role, but part of the decline was also due to the ongoing normalization effects from the pandemic - recall that smokers were stocking up on cigarettes especially in 2020, resulting in inventory issues at retailers. However, I think the most important aspect to keep an eye on is Altria's declining retail share and increasing elasticity. Marlboro saw a 9.1% year-over-year volume decline, and Altria's other premium brands saw a similar 8.3% decline. Marlboro's retail share remained very high at 42.5% for the full year, but declined 0.4 percentage points due to lower disposable income. It is evident that consumers are trading down, from which discount brand manufacturers such as Vector Group ( VGR ) are benefiting greatly. Of course, Altria is also in the discount segment, but with a 6.4% share of shipment volume and lower margins compared to premium cigarettes, it is hardly moving the needle. Moreover, Altria's discount brands appear to be spurned by smokers, as evidenced by a year-over-year volume decline of more than 18%.

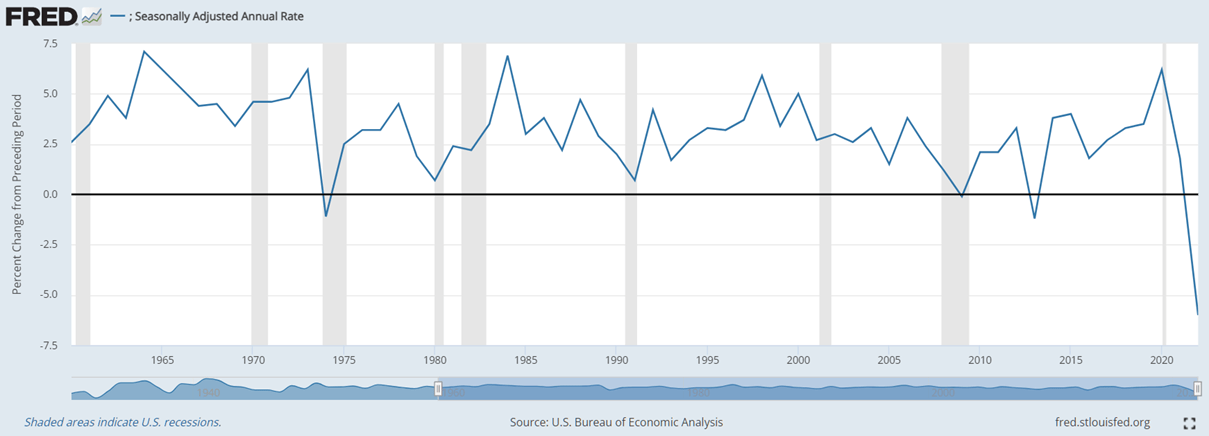

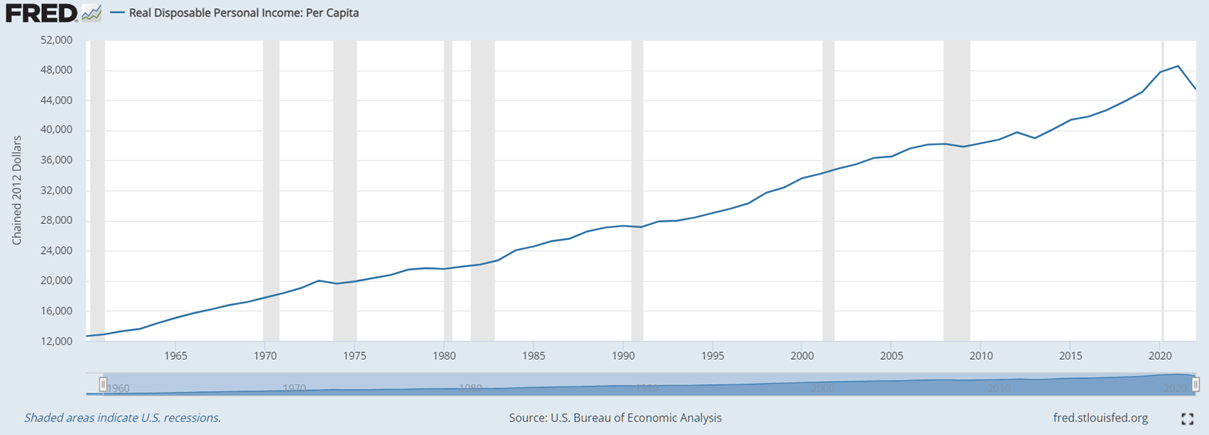

The increasing trade down to discount cigarettes is quite understandable when looking at the change in real disposable personal income (Figure 1). Even though the decline appears extremely worrying from a historical perspective (the graph goes back to 1960), it should also be viewed in the context of absolute numbers (Figure 2). I do not want to downplay the current situation, but in absolute terms it does not look so dramatic. Nonetheless, the difference between actual and perceived inflation should not be underestimated, as should the increasing coverage of inflation-related issues in the news. In addition, further weakening of the U.S. dollar will lead to a slower deceleration in the rate of inflation (or perhaps even stagnation or a renewed uptick), and with other inflationary forces such as demographics (retiring baby boomers), on-shoring of manufacturing, and the focus on non-fossil energy sources, I am among those who believe that inflation will stabilize at a much higher rate than we were used to ten years ago – around 4-5% is my guess.

Figure 1: Real disposable income (percent change from preceding period), A067RL1A156NBEA (U.S. Bureau of Economic Analysis, retrieved from FRED, Federal Reserve Bank of St. Louis; retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/A067RL1A156NBEA, April 19, 2023.) Figure 2: Real disposable income in chained 2012 dollars, A067RL1A156NBEA (U.S. Bureau of Economic Analysis, retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/A067RL1A156NBEA, April 19, 2023.)

{kind=link}

{kind=link}

All in all, I think it is important to continue to monitor Altria's volume trends. After all, conventional cigarettes are Altria's major source of profit, as the company still doesn't have a viable smoke-free portfolio (except from oral tobacco products) and it will take a lot of time and investment to gain a foothold in this sector (see below). Of course, the inelasticity of cigarettes should not be underestimated, but it is finite nonetheless. I think that Altria's change in dividend policy and also the midpoint 2023 earnings per share ((EPS)) guidance of 4.5% confirm this. So far, however, I am not really concerned about the volume trend (Marlboro's share among premium cigarettes actually increased slightly in 2022), but I am still keeping a close eye on Altria's volumes and pricing power.

Altria Group's Earnings Volatility And Implied Slower Growth

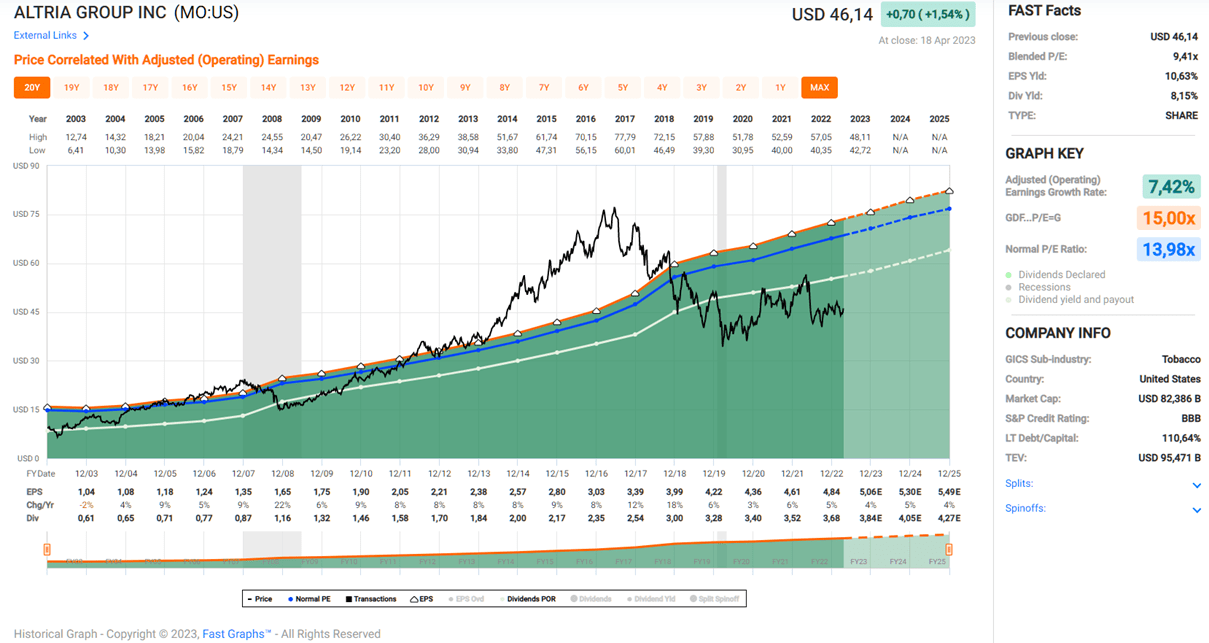

Altria has changed its dividend policy from an earnings-based figure to a dividend growth-based figure. The previous dividend policy was based on adjusted diluted earnings per share, leaving room to exclude one-time events such as impairment charges. This means that the company expects increased earnings volatility and likely weaker overall growth, even before special items. According to FAST Graphs, Altria's adjusted operating earnings growth has averaged 7.4% per year over the past twenty years (Figure 3). Shortening the time frame to ten years, growth still averaged 7.0%. Over the last five years, Altria's average annual profit growth has been only 5.0%, confirming the trend of slowing growth.

Figure 3: FAST Graphs chart for Altria Group stock [MO], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

{kind=link}

With a mid-single-digit dividend growth policy, Altria is essentially confirming that it expects slower growth going forward. Don't get me wrong - mid-single-digit earnings growth is definitely not bad for a de facto declining business, but it does show that the market isn't wrong in valuing Altria at a rather modest price-to-earnings ratio.

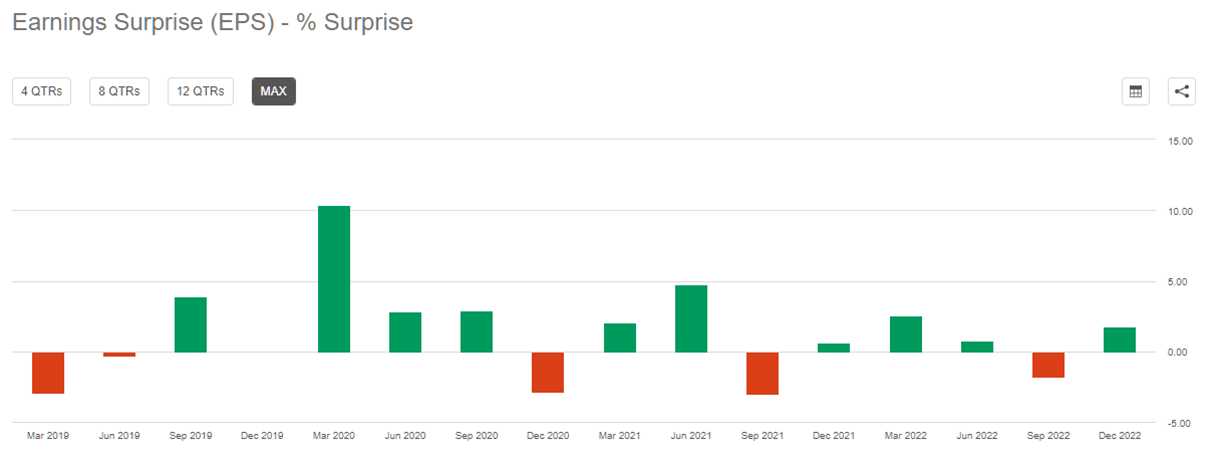

For 2023, management guided for midpoint adjusted diluted EPS growth of 4.5%. According to Seeking Alpha , analysts have turned somewhat more positive on the company's first-quarter results in recent months. However, Altria has occasionally missed EPS estimates in the past (Figure 4), so I wouldn't bet on analysts being right next Thursday. This is not a concern for me, as I am a long-term investor. I own MO stock for the dividend, not the capital appreciation. Reinvesting dividends when valuations are low can have a huge positive impact on long-term total return and is psychologically beneficial in retirement.

Figure 4: Altria Group's [MO] earnings surprises on a quarterly basis (obtained from Seeking Alpha Premium: https://seekingalpha.com/symbol/MO/earnings/eps-surprise-summary?period=quarterly)

{kind=link}

After Thursday's earnings announcement, I would look for signals that provide deeper insight into the slower expected growth. Altria's combustible cigarette volume will likely play a role (see above), but more importantly, the company's smoke-free portfolio will likely take considerable time to gain momentum. With Philip Morris International Inc. ( PM ) entering the U.S. smoke-free market through Swedish Match (market-leading oral tobacco products - Zyn) and IQOS (starting in May 2024), Altria has a strong competitor well ahead in this game (see my recent stock update ). U.K.-based British American Tobacco ( BTI , BTAFF ), is not as much of a concern in the heated tobacco space, but is very strong in the vaping space (Vuse), as I pointed out in my recent analysis .

However, considering that Altria recently announced the acquisition of e-vapor company NJOY, I wouldn't be too quick to write off the company's smoke-free portfolio. NJOY ACE is currently the only pod-based product with FDA market authorization, putting it ahead of BTI's Vuse, which reportedly has pending premarket tobacco product applications ((PMTAs)).

Altria's Anheuser-Busch Stake

As is widely known, Altria holds a minority stake in brewing company Anheuser-Busch InBev ( BUD ). Altria owns 185 million restricted and 12 million ordinary shares, together valued at $11.9 billion at the end of 2022 but reported at $9.0 billion on the December 31, 2022 balance sheet (p. 22, 2022 10-K ). The brewing company recently made headlines for a controversial ad campaign featuring trans activist Dylan Mulvaney. In response, BUD stock lost a few billion dollars in market cap, but is already back near its 52-week high of $67, making Altria's stake currently (April 20, 2023) worth about $13 billion.

The lock-up period that prevents Altria from selling its BUD shares expired already in 2021, so the company is theoretically able to sell the stake at will. Altria's management, however, has been relatively opaque about its intentions. For example, CFO Sal Mancuso said during the fourth-quarter 2022 earnings conference call :

We continue to view the ABI stake as a financial investment, and our goal remains to maximize the long-term value of the investment for our shareholders.

Sal Mancuso - Executive Vice President and Chief Financial Officer.

Earlier, during the third-quarter earnings conference call , he said Altria did not believe ABI's current share price reflected its underlying long-term value and continued to expect a recovery, albeit a slow one. Back in October, the stake was worth about 25% less than it is today.

It is also worth noting that Altria exited its stake in Juul Labs in March. This maneuver now theoretically puts the company in a position to offset the capital gains tax from the sale of its BUD shares. Of course, there's no guarantee that Altria has already sold or will soon sell its stake in the Belgium-based brewing company.

Granted, Altria could use part of the money considering the NJOY acquisition and necessary investments in Horizon Innovations LLC , a company formed jointly with Japan Tobacco ( JAPAF , JAPAY ) to market heated tobacco products under the Ploom brand in the U.S. It should be remembered, however, that Altria has already received $1.0 billion from PMI following the IQOS marketing agreement and will soon receive another $1.7 billion (plus interest). So the acquisition of NJOY is already de facto paid for, and the recent news that Altria will only repurchase $1.0 billion worth of shares by the end of 2023 (p. 2, 2022 earnings press release ) also suggests that there is no immediate need for a large amount of cash on hand.

In conclusion, Altria has put itself in an actionable position with respect to its stake in Anheuser. Of course, the higher BUD's share price goes, the higher the chance of a sale. However, I don't see any near-term reason to move forward with the transaction, as there is no immediate cash need and the recently announced share buyback program can be founded out of cash from operations. I'll be watching for potential updates from CFO Mancuso during the Q1 call, but I'm not holding my breath on a near-term sale. Also, it's important to watch the upcoming first quarter 10-Q for possible clues as to how long the Juul-related tax loss can be utilized. If Altria does make a move at some point, I will look closely at how capital is deployed. Altria's leverage is fairly modest, so there is no immediate need to aggressively deleverage. At current valuations, and being a conservative investor, I would nonetheless welcome a mix of debt repayment and share buybacks. Of course, the worst possible outcome would be another malinvestment like Juul, but I think the likelihood of such a misstep is pretty low.

Altria’s Heated Tobacco Efforts

The patent dispute between Philip Morris International and British American Tobacco was a major reason for the unsuccessful launch of IQOS in the U.S. to date. Since PMI will market IQOS in the U.S. itself from May 2024, Altria will have to come up with alternatives. I have already referred to the joint venture with Japan Tobacco, based on which the two companies plan to market heated tobacco devices under the Ploom brand name. However, things are still at a very early stage and PMTAs are not expected to be filed until the first half of 2025. So Altria's future in heated tobacco is still very uncertain, and it will be a long time before the company can turn a profit in this segment.

Altria has also been working on its own device. During the investor day event, the company unveiled an internally developed device called SWIC (slide 47 of this presentation ). Unlike PMI's IQOS and BTI's glo , SWIC does not resemble the feel of a cigarette in the mouth, which could lead to low acceptance among former cigarette smokers willing to switch. Management in fact has already indicated that SWIC's target audience is a small group of people who are not traditional e-vapor and heated tobacco users. COO Begley noted that these people " find heated tobacco stick products cumbersome and complex " and " are interested in innovative heated tobacco products that bear less physical resemblance to traditional cigarettes " (p. 9, investor day remarks ). This is definitely not good news in my opinion.

However, as with e-vapor, I wouldn't completely write off Altria in heated tobacco, but PMI's lead and the great uncertainty surrounding Ploom's approval in the U.S. leave much to be desired at this point. Similarly, it's too early to hastily dismiss SWIC as inferior to IQOS and glo, but it's obviously important to pay close attention to the data that may be released during the upcoming earnings presentation regarding the acceptance of this novel design.

Conclusion – Is Altria Still A Good Investment?

While this article may come across as overly negative, my regular readers know that I'm basically a happy Altria shareholder. The company is highly profitable, has been able to repair its battered balance sheet after its acquisition of a minority stake in Juul Labs, and continues to treat its shareholders well.

Of course, CFO Mancuso's open letter was somewhat discouraging, and it seems reasonable to expect weaker earnings growth going forward. My base case assumes that Altria will continue to grow its earnings by 4% to 5% per year on an adjusted, diluted basis, with only a small contribution from smoke-free products. As a reminder, in 2022, oral tobacco contributed only about 13% of Altria's adjusted operating income (down slightly year-over-year). It will be a long time, and require significant investments, before heated tobacco products can contribute to Altria's bottom line. Patience is also required with NJOY - the pod-based NJOY ACE product is currently available in only 33,000 stores, while BTI's Vuse is available in 121,000 stores (slide 41 of this presentation ).

Hence, I view Altria as a cigarette company with a portfolio of high-quality brands that continues to have strong pricing power. That said, investors should keep in mind that elasticity has increased and declining volumes can only be offset by price increases for so long. I closely monitor volume trends and also keep an eye on competitors in the premium segment (e.g., British American Tobacco) and the discount segment (e.g., Vector Group). Even though Altria only sells its products in the U.S., it is still important to keep an eye on the Dollar Index . A strong dollar curbs inflation through cheaper imports, bolstering disposable income. Continued high inflation could lead to more consumers switching to discount brands. For this reason, I also think it is important to keep an eye on Altria's discount brand portfolio, even if it is a small contributor to sales.

In addition, I watch for other signs that could confirm weaker earnings expectations going forward - in particular, I keep an eye on margins and capital expenditures (i.e., capex ratio). Because of the need to catch up with competition in heated tobacco and e-vapor, Altria is likely to increase its capital expenditures, which will put modest pressure on free cash flow. This was likely another reason for management's decision to change its dividend policy.

I view Altria more and more similarly to the smaller U.K.-based company Imperial Brands ( IMBBY , IMBBF ) as both lack a meaningful smoke-free portfolio, but I think Altria still has an ace up its sleeve through its stake in Anheuser-Busch. The stake is currently worth $13 billion, which is obviously much less than it was in 2016, but realizing that amount of money would definitely go a long way toward de-risking Altria's investment case. If the company refrains from spending money on another potentially not worthwhile acquisition like the Juul minority stake (NJOY is de facto already paid for by PMI's $2.7 billion), it could reduce its net debt to a conservative two times annual free cash flow from currently above 2.8 times and reduce the number of diluted shares outstanding by over 8%. In this way, Altria could increase EPS by more than 9% and reduce the cost of servicing its dividend accordingly. Perhaps management's comments in the Q1 earnings call will contain new information about the expected course of action.

In closing, I believe Altria remains a good investment with a reasonable potential return of about 12% per year through the end of 2025, assuming no multiple expansion and dividend growth at about 5% per year. If the market grants Altria stock a price-to-earnings ratio of 12 by the end of 2025, the annualized rate of return would be over 20%. However, given the significant uncertainties associated with the smoke-free portfolio and increasing elasticity of the traditional product, I remain more conservative. For this reason, and especially because I already own a sizable position, I rarely add new shares, even though the valuation of Altria stock is certainly compelling.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Altria Stock Q1 Earnings Preview: What To Watch For