AMPS - Altus Power: H2 2023 EBITDA Guidance Is Achievable And FY24 Outlook Is Positive

2023-09-15 12:07:02 ET

Summary

- Despite a recent stock decline, the analysis maintains a Buy rating for AMPS due to its favorable positioning to meet its H2 2023 guidance.

- AMPS reported robust 2Q23 pro forma EBITDA and revenue figures, instilling confidence in their ability to reach 2023 targets.

- AMPS' potential for expansion in the community solar sector through strategic partnerships and its optimistic medium-term outlook for asset development in 2024 contribute to its growth prospects.

Summary

Following my coverage of Altus Power ( AMPS ), I recommended a buy rating due to my expectation that clean energy is going to be a dominant long-term secular trend that will benefit AMPS. This post is to provide an update on my thoughts on the business and stock. I am reiterating my buy rating for AMPS as I believe the expectations are easier to overcome today vs. the previous time I wrote about them, and I am positive that AMPS can meet its 2H23 guidance.

What happened so far

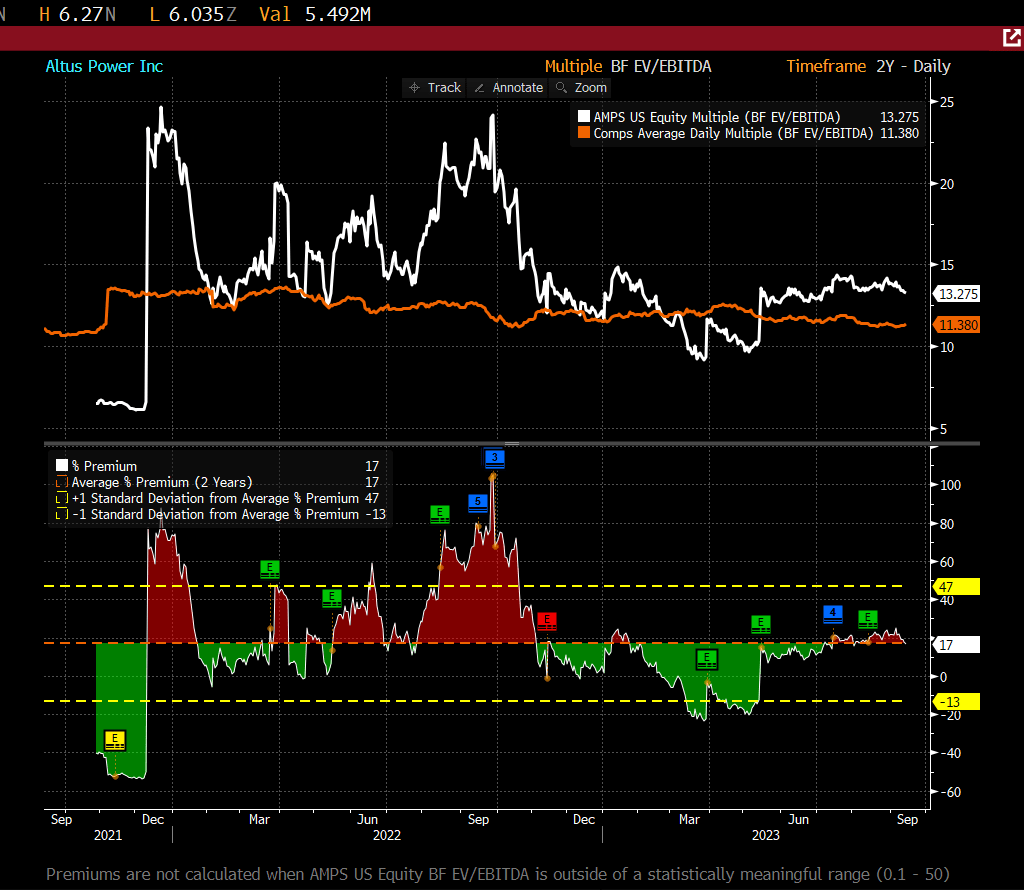

The stock has gone down by about 30% since I last wrote about it, and I think it is fair to give an update on what happened. When I wrote about it, the stock was trading at 15x forward EBITDA, a premium to peers (refer to my valuation section below), but I thought the business deserved a premium because of its fast growth nature and expanding EBITDA margins. However, just days after I wrote my last post, management updated their guidance, saying it would hit the lower end of their targeted range ($57 million to $63 million) due to the administrative delays that led to the later closure of its 88 megawatt acquisition. This led to a series of both revenue and EBITDA downgrades by consensus, which compressed the valuation from 15x to 10x forward EBITDA.

Below, I update my investment thesis for the recent quarter (2Q23) performance and explain why I think this is still a long.

{kind=link}

{kind=link}

Investment thesis

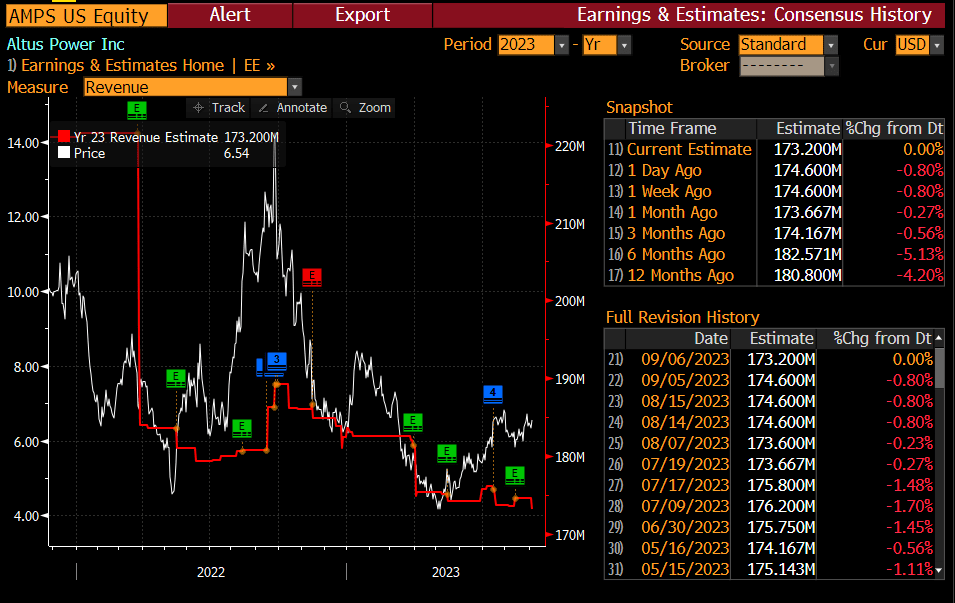

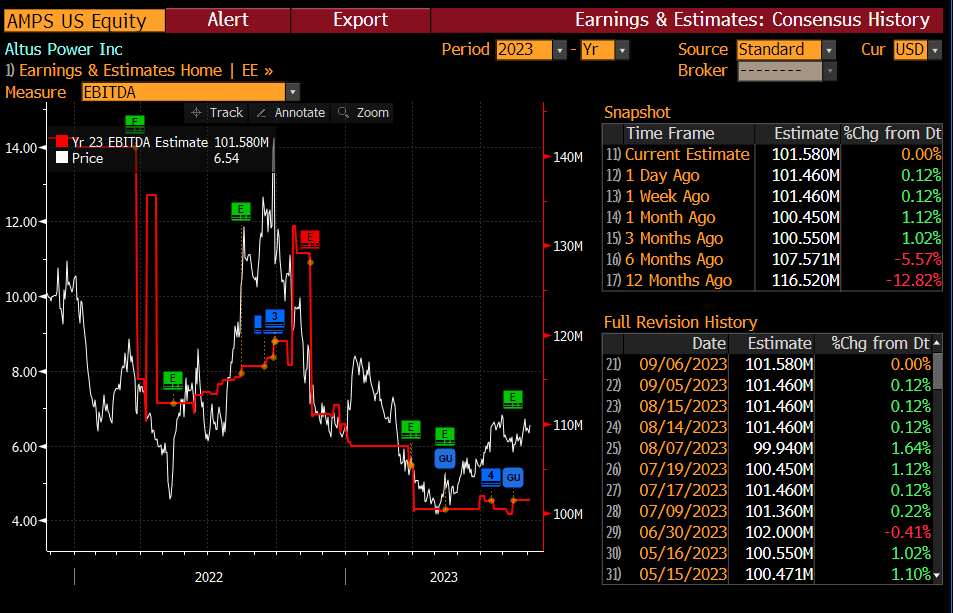

AMPS reported 2Q23 pro forma EBITDA of $30.6 million and 2Q23 revenue of $46.5 million, implying a pro forma EBITDA margin of 65.8%, which is way above consensus estimate of 59.8%. Due to the completion of several in-house development projects and the portfolio acquisition from Apollo, AMPS was able to increase its operating asset portfolio to 698 MW, up from 678MW in the first quarter. I am paying closer attention to expectations, as they were a major factor in the previous stock price crash. The solid 1H23 results give me more faith in AMPS's ability to achieve its 2023 adjusted EBITDA target. Management has restated its 2023 guidance of $97-$103 million in adjusted EBITDA and the mid- to high 50s% range in adjusted EBITDA margin. Total pro forma EBITDA is $46.7 million based on 1H23 performance, so AMPS must generate $53.3 million in EBITDA in 2H23. A 2H23 revenue of $93 million is implied by the midpoint of management's adjusted EBITDA guidance (57.5% margin). Since AMPS only needs to increase revenue by about 62% in 2H23—a slower pace of growth than in 1H23—the bar is lower and the target more plausible.

My confidence in AMPS is bolstered by the potential for community solar to significantly expand AMPS' Total Addressable Market. I believe AMPS can capitalize on this potential by leveraging its strategic partnerships. To illustrate this, AMPS recently forged a strategic alliance with High Street Logistics , the proprietor of 144 industrial and logistics sites spanning the United States, with a collective hosting capacity of 4 MW to 5 MW, equating to approximately 630 MW available for solar deployment. During the 2Q23 call, the management indicated that each of these facilities likely necessitates only 1 MW of power, summing up to 144 MW to operate High Street Logistics' data centers. This implies that, pending compliance with state regulations, AMPS could potentially build and implement the remaining ~490 MW as part of a community solar initiative. Given the possibility of more partnerships akin to this one, I believe the growth potential is vast.

As for the medium-term outlook, management is optimistic about the medium-term future, projecting strong asset under development growth in 2024 thanks to the completion of ongoing construction projects. In particular, they hope to reach a total asset under development of 150 MW. If they were to accomplish this, it would be a remarkable demonstration of their development abilities, especially given the period of accelerated growth through portfolio acquisitions that will begin in 2022. While AMPS's partnership with Altus Power Introduces Community Solar Partnership Program to CBRE and Blackstone Employees across The Northeast gives it a leg up when competing solar asset owners are cutting back, I see significant growth from its in-development assets as a critical milestone regardless. It would increase investors' faith in AMPS' ability to capitalize on growth in the commercial solar power sector.

Valuation

Own calculation

Using my model, I believe the fair value for AMPS based on my model is $8.21.

Given that the business is in a high growth stage, it is difficult to pinpoint how fast it could grow. As such, I am using consensus estimates as a benchmark for my assumptions. My take is that business will continue to grow at a rapid rate, following the 1H23 growth pace (73%), and slowly taper down from there, which is in line with consensus expectations. Margins should gradually improve over time as the business sees operating leverage, which has been happening (EBITDA margin grew from 50+% to 60+%). Unlike my previous model, where I modeled using 15x forward EBITDA, I am now being conservative by using the current forward EBITDA multiple, which is much more in line with the historical premium over peers.

Peers include Brookfield Renewable, Nextera Energy Partners, Clearway Energy, Ormat Technologies, Energy Harbor Corp., First Energy, Constellation Energy, and Exelon Corp. The reason I believe AMPS will continue to trade at a premium is because of its growth profile, which is almost twice that of peers.

{kind=link}

Conclusion

Despite a recent stock decline, I maintain a buy rating, as AMPS seems better positioned to meet its 2H23 guidance. Their 2Q23 results displayed impressive pro forma EBITDA and revenue figures, boosting confidence in their ability to achieve their 2023 targets. Furthermore, AMPS' potential for community solar expansion through strategic partnerships, such as the one with High Street Logistics, offers significant growth prospects. Looking forward, the medium-term outlook appears promising, with anticipated growth in assets under development for 2024. This underscores AMPS' development capabilities amid a period of portfolio acquisitions. In terms of valuation, I've adjusted my approach to align with current market conditions, and the fair value for AMPS is estimated at $8.21.

For further details see:

Altus Power: H2 2023 EBITDA Guidance Is Achievable And FY24 Outlook Is Positive