AMPS - Altus Power: Unico Solar Acquisition Should Accelerate Growth

2023-12-23 01:53:59 ET

Summary

- Altus Power has acquired Unico Solar to expand its presence on the West Coast and boost its pipeline and capabilities.

- The renewable energy industry, especially solar power, is experiencing strong growth in the US.

- Altus Power's financials show significant growth in operating revenue and net income, and the company expects continued growth in adjusted EBITDA for FY2023.

- Despite the overvaluation, I believe that its expansion to the West Coast can act as a catalyst to boost its growth in the long term by enhancing its development capacities and increasing its geographic footprint, which can facilitate it to serve more customers.

Investment Thesis

Altus Power ( AMPS ) mainly offers clean electric power to the industrial, commercial, public sector, and Community Solar customers. The company has recently acquired Unico Solar, which can accelerate its growth by expanding its presence on the West Coast. This acquisition can also benefit the company by boosting the flow of its pipeline and increasing its capabilities to serve more customers.

About AMPS

AMPS is commercial-scale provider of clean electric power that serves industrial, commercial, public sector, and Community Solar customers with end-to-end solutions. The company mainly develops, originates, operates, and owns large-scale ground, roof, carport-based photovoltaic (PV), and energy storage systems. These systems are located across the United States, from Hawaii to Vermont. The firm’s offerings help customers to increase the accessibility of clean energy, and to lower their electricity bills. Its portfolio comprises 470 megawatts ((MV)) of solar PV. It currently has over 2000 subscribers countrywide. The company possesses long-term power purchase agreements with more than 300 C&I entities. It also has contracts with more than 500 residential customers, with operations of approximately 40 megawatts of Community Solar Projects. It markets its solar energy offerings with the help of a national developer base, using local expertise and intermediaries that connect the company and its partner network with its customers. The geographic regions mainly include New Jersey, Massachusetts, Minnesota, Nevada, California, Maryland, New York, Connecticut, and other states. The company conducts its business in one operating and reportable segment. It has also recently closed its Blackstone Construction Facility, which is a financial arrangement for constructing commercial solar assets. The additional capital from Blackstone can offer a competitive advantage to the firm to optimize its working capital.

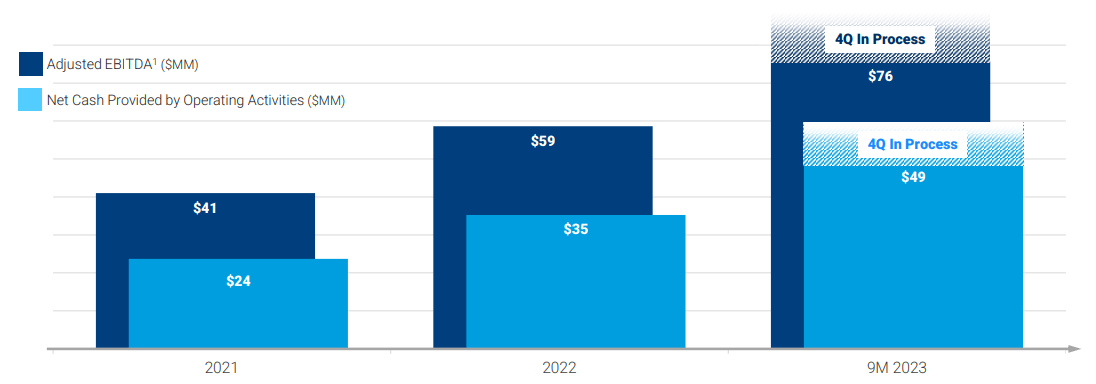

EBITDA and Net Cash Trends of AMPS (Investor Presentation: Slide No: 4)

{kind=link}

Acquisition of Unico Solar

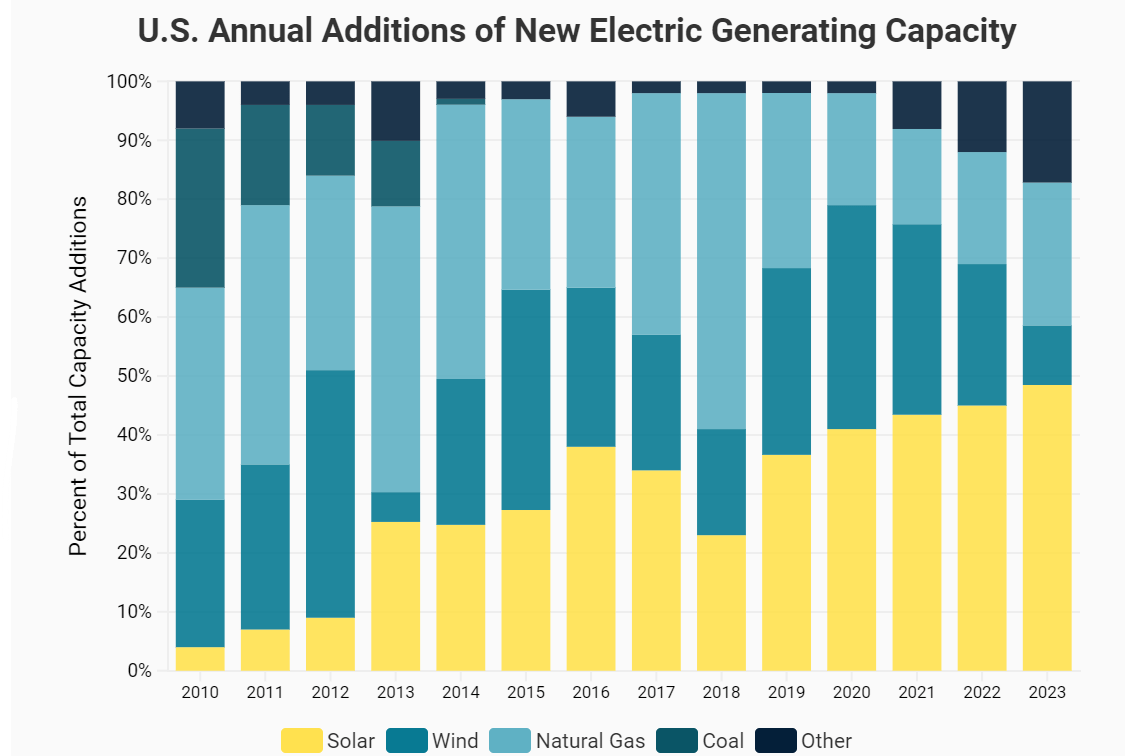

The renewable energy industry, especially the solar power sector, is booming in the United States. It experienced a 24% annual average growth rate in the last decade. This development mainly resulted from federal policies such as the Solar Investment Tax credit, the increasing need for clean energy in the public and private sectors, and declining costs. The installation cost has almost experienced a 40% drop from the last decade, which has expanded its market exponentially in a shorter period. However, I think supply chain issues and inflationary pressures resisted the industry growth to some extent. Despite this, In 2023, solar has contributed 48% to the electric capacity that was added to the grid. The industry has strong dynamics as many of the industrial and commercial sector companies are heavily investing in cleaner energy alternatives. The increasing installation of solar capacity has outpaced hydropower and observing these trends, EIA expects that the US might generate 14% more electricity from solar compared to hydropower in 2024. It is estimated that solar energy might be the largest source of total capacity in 2050 . This indicates that there is a robust demand in the industry. Identifying these scenarios, the company has recently acquired Unico Solar which is one of the independent power providers of clean energy to industrial and commercial property owners. As per this deal, AMPS will acquire Unico’s pipeline, development platform, senior leadership team, and offices in Seattle and Denver. This increased capacity can diversify its portfolio of clean energy assets. It can also benefit the company to gain significant access to the West Coast, which can allow it to serve real estate and enterprise customers. In addition, the synergies can help the company enhance its strengths by combining the operations, which can further reduce its costs and make it competitive. I believe this acquisition can act as a catalyst to boost the firm’s growth and profitability as it can strengthen and boost its flow of pipeline, which can further help it to cater to the growing demand and capture additional market share by adding more customers to its portfolio. In addition, I think the company’s strong access to capital and robust balance sheet also gives it a competitive edge in the market and might help it to capitalize on industrial opportunities.

U.S. Annual Additions of New Electric Generating Capacity (Solar Energy Industries Association)

{kind=link}

Financials

The company has reported its quarterly results. It reported operating revenue of $45.07 million, up 48.10% compared to $30.43 million in Q3FY22. This growth was mainly fueled by construction completion and significant acquisitions during the past twelve months. Net income surged by 107.01% YoY, from a loss of $96.62 million to a profit of $6.77 million. It reported a diluted EPS of $0.03. AMPS reported $68.18 million in liquidity and adjusted EBITDA stood at $29.06 million, a 50% increase compared to Q3FY22.

The company has rebounded significantly despite the challenging environment and I believe it can further maintain its growth trajectory as it has recently focused on acquisition which can potentially attract new customers by increasing its presence in the West and developing its pipeline. The company also has a positive view and expects adjusted EBITDA for FY2023 to be between $97-$103 million, which is almost 70% growth over FY2022. Observing the robust demand and the company’s increased presence, I think these estimates are correct.

Gregg Felton, Co-CEO of Altus Power, states that they have a unique opportunity to expand their leadership position in the current environment. He noted that while developers are struggling with limited access to capital, Altus Power has excellent and growing access, providing them with a competitive advantage and allowing them to continue to scale their construction across the country.

Valuation

Solar energy is gaining prominence to reduce carbon emissions and promote sustainability. This increased need has accelerated the industry demand. Though the demand is accelerating, this sector is highly underpenetrated and presents a large addressable market for the company. Identifying these scenarios, the firm has acquired Unico Solar which can increase its customer base by developing its capacities and presence on the West Coast, which can further contribute to its growth of profit margins. After considering all these factors, I am estimating an EPS of $0.22 for FY2024, which gives the forward P/E ratio of 5.26x (share price:$6.54). After comparing this with the sector median of 14.85x, we can conclude that the company is overvalued. Despite the overvaluation, I believe that its expansion to the West Coast can act as a catalyst to boost its growth in the long term by enhancing its development capacities and increasing its geographic footprint, which can facilitate it to serve more customers. In addition, the company’s strong access to capital also makes it competitive in the market, which can help it to capitalize on tremendous demand in industry. Observing industrial tailwinds, its expansion activities, and strong positioning of the company, I think it's an attractive stock to hold in the portfolio.

Conclusion

Altus Power offers clean electric power. The company is experiencing tremendous demand due to industrial tailwinds, which is reflected in its quarterly results. It has recently acquired Unico Solar, which can boost its growth in the long term by developing flow of its pipeline and expanding its presence on the West Coast. It is exposed to risk of supply chain disruptions, which can reduce its profit margins. The stock is currently overvalued, however, I think that we can expect decent growth in profitability as it has been aligned with its expansion activities which can potentially increase its customer base due to increased capabilities. After considering all the above factors, I assign a hold rating to AMPS.

For further details see:

Altus Power: Unico Solar Acquisition Should Accelerate Growth