CANO - Am I Wrong About CVS?

Summary

- CVS is still trading below its intrinsic value and the stock is clearly undervalued in my opinion.

- In my opinion, neither the quarterly results nor the looming recession or the current opioid litigations are reasons for concern in my opinion.

- CVS acquired Signify Health last year and might make further acquisitions in the coming quarters.

- In my opinion, the stock is a clear buy.

CVS Health ( CVS ) is one of the stocks for which I see high growth potential in the years to come. In my opinion, the stock is clearly undervalued and should trade much higher. I know it often takes time for a stock to return to its intrinsic value (actually, stocks rather seldom trade for their intrinsic value but are mostly over- or undervalued). Nevertheless, CVS continues to trade clearly below the intrinsic value I calculate for the stock and it is a bit irritating.

It is not that I am getting impatient. CVS is paying me a quarterly dividend and my position, which I built in 2019 and 2021 is up about 65% and both positions clearly outperformed the S&P 500 ( SPY ). My 2019 position more than doubled the performance of the S&P 500 and the 2021 position returned 38% while the S&P 500 returned 5% in the same timeframe.

And even when being really confident about a position – or especially then – we should question our thesis on a regular basis and ask ourselves if our premises, our assumptions and our conclusion are correct. So: Am I wrong about CVS?

Valuation

We could start by looking at simple valuation metrics and with a price-earnings ratio of 39, the stock seems to be clearly overvalued. But to explain that rather high P/E ratio we must take into account the opioid litigation and recorded pretax charges of $5.2 billion for legal settlements (we will get to this). When looking at the adjusted numbers instead (management is expecting adjusted EPS to be around $8.60) we get a P/E ratio of only 10.6.

And one could now argue not to use adjusted numbers but when looking at the price-free-cash-flow ratio we see even lower valuation multiples. According to the chart above, CVS is trading for only 6.2 times free cash flow. This is not only below the 10-year average of 13.26, but an extremely low valuation multiple for any business that is healthy and growing. However, I don’t really know how that metric was calculated. CVS Health is expecting free cash flow for fiscal 2022 to be around $11.1 billion (midpoint of guidance) which would lead to a P/FCF ratio of 11 – still very cheap.

As usual, I will pay more attention to a discount cash flow calculation to determine an intrinsic value for the stock. Management is expecting free cash flow to be $11.1 billion in fiscal 2022 (midpoint of current guidance). And from now till perpetuity let’s assume 5% growth (similar to my previous articles about CVS). When calculating with these assumptions and a 10% discount rate as well as 1,315 million in outstanding shares we get an intrinsic value of $168.82 for CVS and the stock would trade about 45% below its intrinsic value.

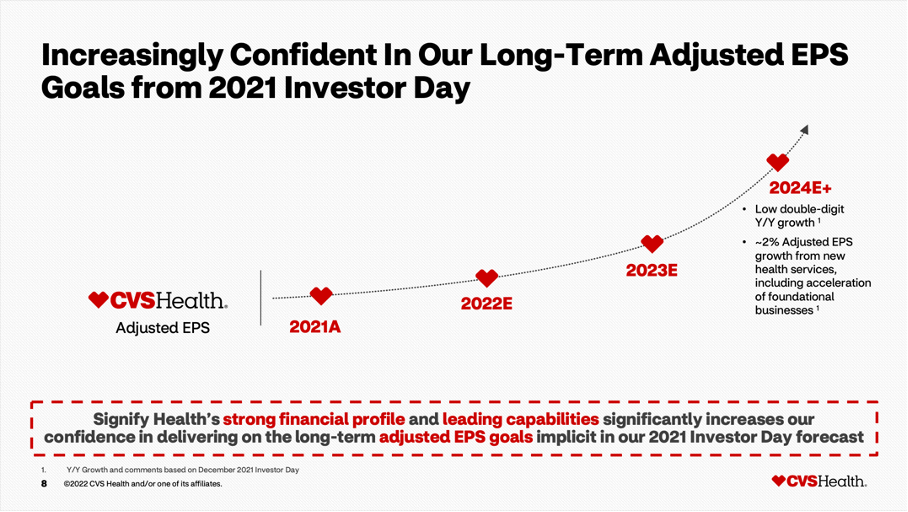

And the assumption of 5% annual growth is also in-line with past growth rates as well as the company’s long-term guidance. When looking at past growth rates, CVS grew with a CAGR of 8.76% in the last ten years. And since 2000, earnings per share grew with a CAGR of 9.30% and since 1990 earnings per share grew with a CAGR of 6.28%. When looking at these growth rates, 5% growth till perpetuity seems reasonable. And management is even more optimistic in the years to come. From 2024 going forward, the company is expecting earnings per share to grow in the low double digits year-over-year.

CVS Signify Health Acquisition Presentation

{kind=link}

We can also offer a different perspective. Even when CVS is not able to grow in the years to come, the intrinsic value would be $84.41, and the stock would almost be fairly valued. And don’t forget: This is calculated with a 10% discount rate and therefore assuming a return on our investment of 10% annually, which is still solid.

Quarterly Results

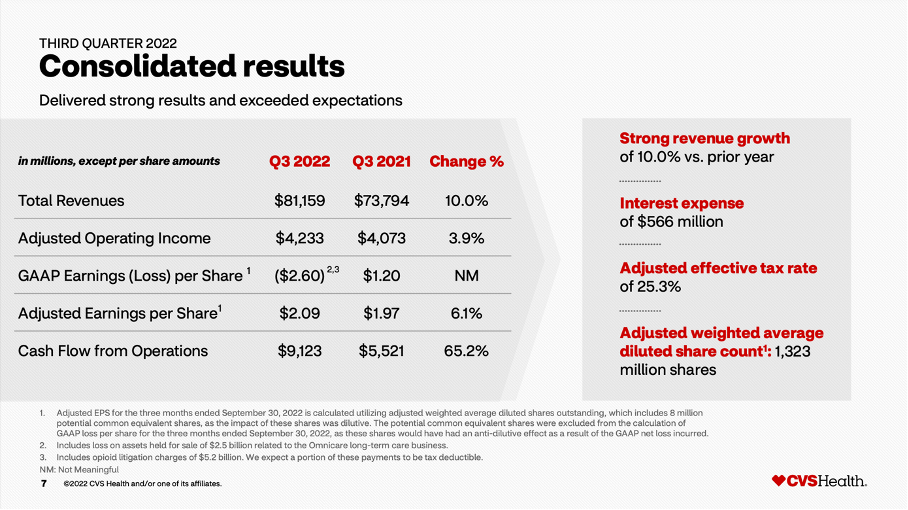

Another reason for a poor performance could be quarterly results and CVS disappointing investors. But not only did CVS beat estimates for earnings per share as well as revenue, the results were also solid. Revenue increased from $73,794 million in Q3/21 to $81,159 million in Q3/22 – resulting in 10.0% year-over-year growth. But while the top line could increase with a solid pace, CVS had to report an operating loss of $3,931 million in Q3/22 – instead of an operating income of $3,061 million in Q3/21. And diluted earnings per share also “switched” from $1.20 earnings per share in Q3/21 to $2.60 loss per share in Q3/22.

{kind=link}

Adjusted earnings per share however increased 6.1% year-over-year from $1.97 in Q3/21 to $2.09 in Q3/22. And the major reason for the negative operating income and loss per share (according to GAAP) are $5,220 million in opioid litigation charges (we will get back to this).

When looking at the different segments, all three could contribute to growth. Retail/LTC generated $26,706 million in revenue (reflecting an increase of 6.9% YoY growth) and Pharmacy Service Segments reported a revenue of $43,216 million (an increase of 10.7% year-over-year). Finally, the Health-Care Benefits Segment reported a revenue of $22,511 million (resulting in an increase of 9.9% YoY).

{kind=link}

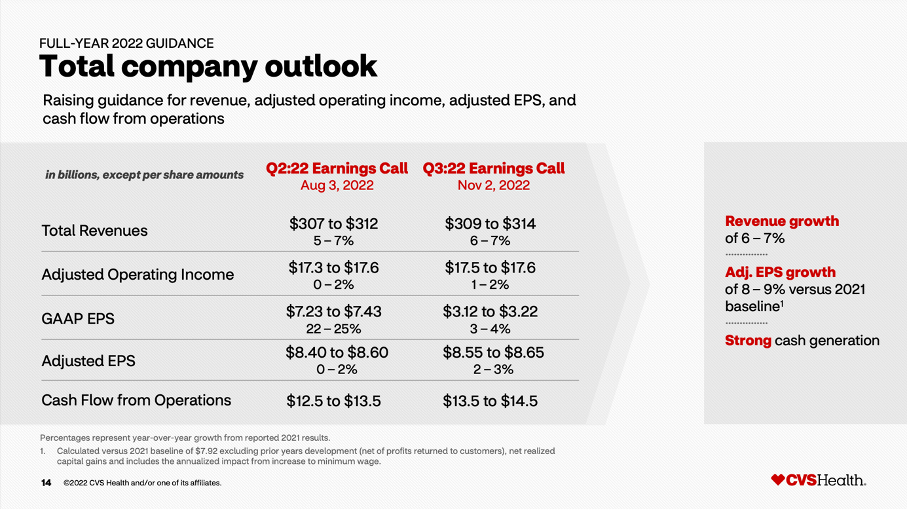

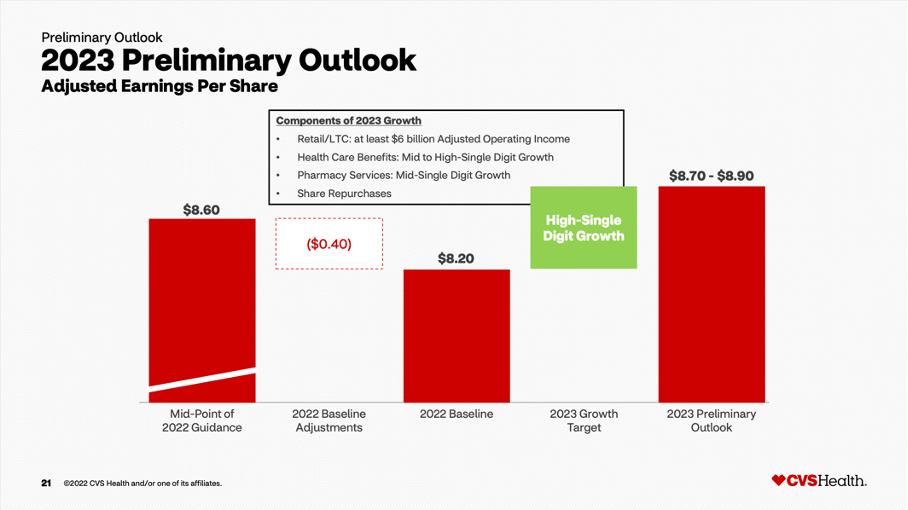

Another reason for a mediocre performance could be a lowered guidance. But CVS raised its guidance – for revenue, adjusted EPS and cash flow from operations. Only GAAP EPS estimates had to be lower. Additionally, CVS also appears slightly optimistic for 2023.

{kind=link}

Recession

Another reason for the performance could be the looming recession. But in the past, CVS was quite recession resilient (I am not necessarily talking about the stock price). I already argued in my past article that CVS could withstand past recessions quite well and will most likely perform solid in the next potential recession.

Opioid Litigation

We already mentioned the opioid litigations briefly – and they could be another reason for the mediocre stock price performance and a reason why CVS is trading for such a huge discount (in my opinion). At the beginning of November 2022, it was also reported that CVS is close to settlement of nearly all opioid-related lawsuits and claims. During the last earnings call , management commented on the process:

This morning, we made an important announcement on our ongoing opioid legal matter. In late October, we began a mediation to resolve substantially all opioid lawsuits and claims against CVS Health by states, political subdivisions and tribes. We reached an agreement in principle to pay approximately $5 billion over 10 years beginning in 2023, an outcome that is in the best interest of all parties and one that will help put a decades old issue behind us as we continue to focus on delivering a superior health experience for the millions of consumers who rely on us.

If the deal is finalized, CVS will have to pay about $5 billion to states and political entities, but the payments will be spread over the next ten years (starting in 2023). CVS has already reported $5.2 billion in pre-tax opioid litigation charges in the third quarter of fiscal 2023 leading to a GAAP loss per share of $2.60.

Acquisition

When looking for further reasons why CVS Health is still trading below what I consider a fair value for the stock, we can also mention acquisitions. Maybe investors assume that acquisitions are a mistake (which is often true) that don’t add much value to a company – or CVS Health in this case.

In the last few quarters, CVS Health generated a lot of headlines due to acquisitions, potential acquisitions, and rumors about acquisitions. And considering that the acquisition of Aetna was one of the major reasons the stock tanked and clearly underperformed since 2016, CVS once again making (major) acquisitions doesn't seem like the best news for investors – it could also be one of the reasons why the stock is trading clearly below its intrinsic value in my opinion (we will get to that). On the other hand, acquisitions have been a part of CVS’s strategy for a long time – in 2015 the company acquired Omnicare as well as 1,600 pharmacies from Target ( TGT ). And the Aetna acquisition has also been a major success – in my opinion.

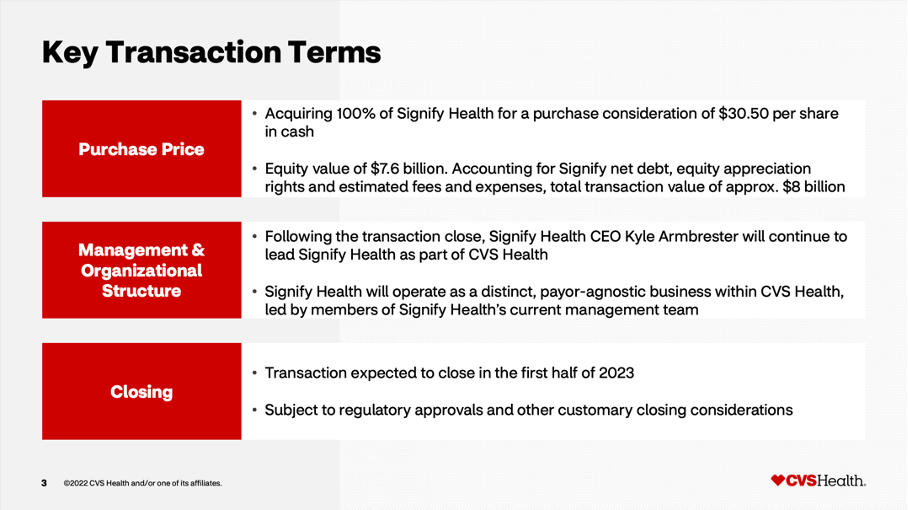

In September 2022, the company announced the acquisition of Signify Health ( SGFY ) and purchased the company for $30.50 per share resulting in a total transaction value of approximately $8 billion (including net debt as well as estimated fees and expenses). The acquisition was paid all in cash from CVS’ balance sheet.

CVS Signify Health Acquisition Presentation

{kind=link}

The transaction is expected to close in the first half of 2023 and the deal will add about 10,000 contracted doctors and clinicians to CVS Health. It was also reported that other companies were interested in Signify Health as well – including UnitedHealth ( UNH ) and Amazon ( AMZN ).

And aside from this actual acquisition, there were many rumors and talks about potential acquisitions. Since the summer of 2022, there have been rumors about a potential acquisition of Cano Health ( CANO ). At the beginning of October 2022, it was reported that CVS Health is in exclusive talks to acquire Cano Health, but about two weeks later it was reported that CVS walked away from the deal and as result Cano Health went into freefall. I don’t know if this is the end of story, but Cano Health would be extremely cheap (and more than 90% below the implied worth of $14 per share).

Nevertheless, CVS Health appears still interested in acquisitions in the primary health care space and on Monday it was reported that Oak Street Health ( OSH ) might be a potential target. Oak Street Health is offering healthcare services and operates about 130 primary care centers in 19 different states. The company has been seen as a potential acquisition target for several months and it was already speculated about CVS being a potential buyer. Speculations see a deal being worth about $10 billion, which would be a huge premium on the market cap of about $5 billion before the first news broke.

Balance Sheet

I don’t know how to position myself towards another acquisition. On the one hand, CVS Health is generating more than $10 billion in free cash flow annually and on September 30, 2022, it had $17,197 million in cash and cash equivalents on its balance sheet as well as $2,792 million in short-term investments. CVS Health still must pay about $8 billion for the acquisition of Signify Health resulting in about $12 billion in liquid assets for another acquisition.

Hence, CVS Health would not have to add debt to its balance sheet – even if it would acquire Oak Street Health for $10 billion – and I really don’t want to see additional debt on the balance sheet. CVS Health should rather focus on reducing debt levels. It still has $1,363 million in short-term debt as well as $50,848 million in long-term debt. When comparing the total debt to the total stockholder’s equity of $71,011 million we get a debt-equity ratio of 0.74 – which is acceptable. But when comparing the total debt to the trailing twelve-month operating income of $14,788 million it would still take about 3.5 years to repay the outstanding debt. This is no reason for concern, but I would like to see CVS bring down its debt levels further – especially considering $78,066 million in goodwill on the balance sheet (an extremely high amount for a $120 billion market cap company).

{kind=link}

Of course, CVS Health will manage to repay its outstanding debt and could also pay for another acquisition. I just like to see management make smart and strategic decision by purchasing great businesses for a reasonable price – and not just acquire companies to continue growing.

Further Risks

And of course, there are many additional risks and headwinds. However, I don’t see any of them as a problem CVS Health can’t handle. Until 2024, CVS is planning to close about 900 stores and of course, this is not the best news, but doesn’t create a huge problem right away and can lead to higher profitability for the existing stores in a few years from now.

Another problem could be the mediocre star ratings CVS received from the Center for Medicare & Medicaid Services in early October. In the 8-K the company stated:

On October 6, 2022, the Centers for Medicare & Medicaid Services (“CMS”) released its 2023 Star Ratings for Medicare Advantage (“Medicare Part C”) and Medicare Part D prescription drug plans. Based on the newly released 2023 Star Ratings, which will impact revenues in 2024, the percentage of Aetna Medicare Advantage members in 4+ Star plans is expected to drop to 21% (based on current enrollment and contract affiliation), as compared to 87% based on the 2022 Star Ratings. The main driver of this decrease was a 1 Star decrease in the Aetna National PPO, which dropped from 4.5 to 3.5 Stars, while many other Aetna plans remain rated at 4+ Stars.

As a result, the stock fell about 4.7% during pre-market trading that day. But during the last earnings call, management was optimistic that the negative impact in 2024 will still be manageable for CVS:

Let me talk about the '24 headwinds a little bit more specifically. We project the combined impact of [stars] ((PH)) and Centene on 24 to be approximately $2 billion on an unmitigated basis. My comments today regarding repurchases and achieving our Investor Day commitments assume that we're successful in mitigating approximately half of this headwind. And that work is in process and underway, but not 100% certain at this stage. That would leave a headwind of about $1 billion or $0.55 a share for 2024.

And finally, CVS is facing reimbursement headwinds and a change of the regulatory environment can have a huge impact on the business – at least in theory.

Conclusion

Without doubt, there are several risks and headwinds for CVS right now. But in my opinion none of these risks will have a huge impact on CVS’ business and should keep CVS from growing at least in the low single digits. The opioid litigations seem almost settled (and is already included in the Q3/22 results), CVS can withstand recessions quite well and as a business operating in the healthcare sector it should not be affected much by recessions. All in all, CVS is a clear buy in my opinion and should reward investors at least with double-digit returns in the years to come.

For further details see:

Am I Wrong About CVS?