AMADF - Amadeus: Fortunes Tied To A Travel Downswing

2023-09-26 02:53:30 ET

Summary

- Amadeus has benefited from a post-COVID travel upswing over the last year.

- As this tailwind fades, though, the company will have to navigate the grim reality of stagflation pressures globally.

- With the stock still pricey and guidance numbers yet to be reset lower, I am neutral here.

The post-COVID travel recovery has taken shape over the last year despite some bumps along the way (on/off movement restrictions in China and the Russia/Ukraine conflict). Amadeus ( AMADF ), the dominant provider of tech infrastructure underlying global airline travel (mainly via its core ‘Amadeus Global Distribution System’ ((GDS)) which facilitates real-time bookings across the industry), has generally benefited.

The outlook from here could still prove challenging, though, given the company’s strong ties to broader travel trends, which are coming under pressure from the one-two punch of higher interest rates and rising inflation globally. Compounding the issue is the company’s limited diversification beyond discretionary travel, with the ‘pay per use’ model of its second largest revenue generator, its ‘passenger service system’ offering, Altéa (i.e., the airline system handling the business end, e.g., revenue and cost management), also exposed to cyclical swings. Even ‘new addressable markets’ like hospitality (mainly reservation systems for major hotels) and payments (gateway/wallet solutions for airlines and travel agencies) are tied to slowing and increasingly price-sensitive global travel demand .

With H1 2023 results confirming long-held fears of a sharp bookings deceleration in North America/Europe and a faltering China reopening-led Asian recovery offering little offset against this weakness, the near-term guidance revision path remains skewed to the downside. Another key hurdle to owning the stock is the pricey valuation at >30x P/E (~27x fwd), which doesn’t seem particularly compelling given the challenging backdrop. As much as I like the competitive moat Amadeus has built through the years, I don’t see a strong reason to be long here - pending a meaningful correction.

Recovery Momentum Intact, but Warning Signs Emerge in Q2

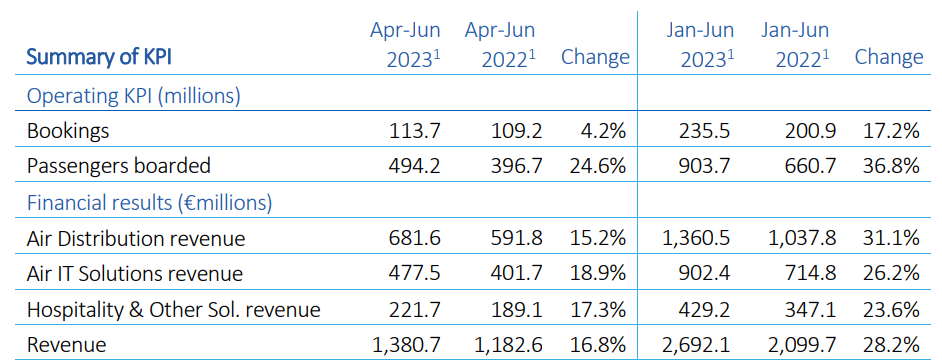

On a headline basis, Amadeus outperformed in H1 2023, with group revenue up a solid +28% YoY and EBITDA growth at +41% YoY to EUR1.1bn (+120bps margin expansion to 38.9%). The Q2 recovery (+16.8% YoY) was more gradual than Q1, however, with top-line growth for the company’s key air distribution and air IT solutions segments decelerating YoY. Fundamentally, the slowing post-COVID bookings recovery (+4% YoY in Q2 vs. +33% in Q1), led by North America and Western Europe, has emerged as the key drag. While higher average booking fees helped, air distribution revenue, which tracks bookings closely, still saw Q2 growth falter to +15% YoY (down from >50% in Q1). Given major airlines also reported sluggish corporate travel over the period, the operating environment is clearly a big issue here.

{kind=link}

As for air IT solutions (mainly Passenger Service System Altéa, a core airline solution spanning customer reservation and inventory management), the key metric, passengers boarded, has also slowed, though segment revenue is inching closer to pre-COVID levels. More tellingly, however, segment revenue per passenger boarded was down high-single-digits % YoY in H1.

The fast-growing hospitality business continues to hold long-term promise as one of Amadeus’ new market opportunities. And though its sequential slowdown in Q2 (+17.3% YoY) wasn’t as steep as the airline side, the numbers were helped by a more favorable base effect (the hospitality industry was slower to recover post-COVID) and remains levered to slower corporate travel trends. In the meantime, onboarding major hotel chains (e.g., the long-term central reservation system contract with Marriott (MAR)) helps but remains a long-term project.

Status Quo Guidance Update; Bigger Reset Possibly on the Horizon

Management cited ‘improvement in Amadeus’ bookings evolution’ in July but opted not to revise full-year guidance for 2023. This might seem conservative, but combined with the recent wave of airline downgrades in anticipation of a more challenging macro backdrop, I suspect the company’s next guidance revision is more likely to skew down, not up. Thus, concerns about the pace of air distribution recovery back to pre-COVID booking levels are warranted, in my view. From here, Amadeus will probably need to lean on pricing to make up the shortfall (low teens % increase in revenue per booking through H1). Given recent gains were down to a mix shift toward higher-yielding international bookings, though, it seems unlikely that pricing will be a source of strength in a global macro slowdown where international would be hardest hit.

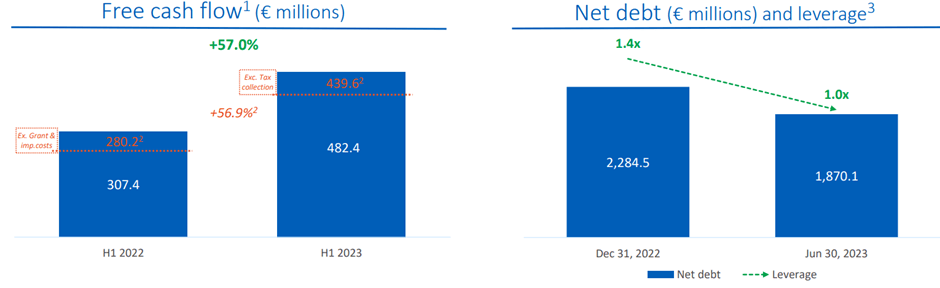

Alongside the unchanged revenue guide, management also sees the cost base increasing in H2 2023 at a similar pace to H1, implying a +10-14% range. Having just gone through a multi-year cost-cutting exercise that ended in 2022 (including capex reductions), there likely aren’t too many levers available to shield margins should revenue further decelerate in the back half. Thus, I wouldn’t be surprised to see EBITDA estimate downgrades down the line as passenger traffic slows following the initial post-COVID bounce back through 2022 (and early 2023 in Asia Pacific). Also worth watching will be potential knock-on impacts for leverage, which remains manageable within the company’s 1-1.5x mid-term target, as well as dividend payments (currently at a 50% payout ratio or a ~2% yield).

{kind=link}

Fortunes Tied to a Travel Downswing

Having already rallied on the back of a post-COVID travel industry rebound, the path ahead could prove far more challenging for Amadeus. Fundamentally, not a lot has changed - the company maintains one of the most profitable moats in the travel industry, backed by its GDS booking system, still the go-to airline travel solution despite numerous attempts to dislodge its competitive position. But its fee income remains tied to bookings, which are, in turn, linked to the broader travel cycle, so the P&L is exposed to an increasingly likely economic slowdown globally. The rest of its IT solutions (for airlines, hospitality, etc.) are similarly cyclical; thus, the same tailwinds that propelled the company post-COVID could reverse in the coming months.

The below par H1 2023 report, highlighting a slowdown in bookings, represents an early warning sign, in my view. Given the impacts of monetary tightening tend to work with a lag, I see more guidance downgrades on the horizon as the passenger demand curve turns even more elastic. In contrast, the stock seems to be pricing in an optimistic ‘soft landing’ scenario at ~30x earnings and will be vulnerable to further valuation resets.

For further details see:

Amadeus: Fortunes Tied To A Travel Downswing