AMADY - Amadeus IT Group: Leading Global Travel Technology Company With Attractive Upside

2023-08-24 04:47:25 ET

Summary

- Amadeus IT Group is a Spanish IT provider for the global travel and tourism industry.

- We are drawn by the quality of the Air IT business, the competitive positioning of the company, and superior mid-term growth.

- We believe there is significant upside left.

We present our note on Amadeus IT Group ( OTCPK:AMADY ), a Spanish IT provider for the global travel and tourism industry, with a Buy rating. We are drawn by the structural outlook of the industry, the quality of the Air IT business, the cash-generative nature and the relative predictability of the business, as well as the superior competitive positioning of the company. We believe there is additional upside left in the stock. We will provide a brief overview of the business and analyze the key drivers of our thesis as well as potential risks.

Introduction To Amadeus IT

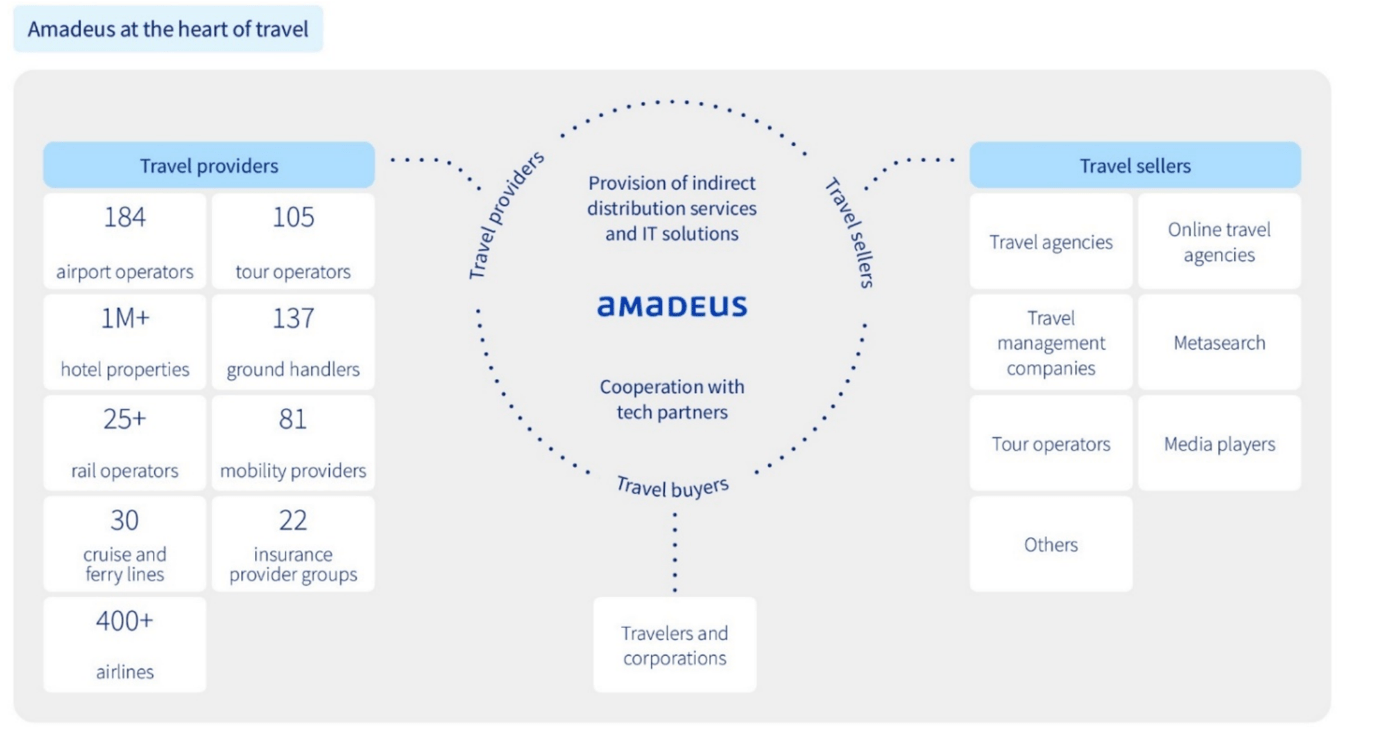

Amadeus is the leading global travel technology company. It provides services and solutions to travel providers and travel agencies. Amadeus was founded in 1987 by four major European airlines to support airline distribution and later expanded to serve customers across the entire travel industry.

{kind=link}

The company’s main business lines are Air IT Solutions , Air Distribution , and Hospitality and other Solutions. The Air IT business provides technology solutions that facilitate business processes including reservations, ticketing, inventory management, and departure management. It offers integrated Passenger Service Systems, standalone software, as well as analytics and consulting services helping airlines operate efficiently and increase profitability by reaching more customers, optimizing costs, and growing customer loyalty. Moreover, Amadeus offers airport solutions for passenger services and operations management. The Air Distribution business connects on one side travel providers including airlines, car rentals, hospitality providers, cruises, railways, etc., and on the other retail and corporate travel sellers, online travel companies, and other buyers, providing significant economies of scale and efficiency. The scope of the company has broadened, and through the acquisition of Newmarket in 2014 and TravelClick in 2018 Amadeus has expanded into Hotel IT, offering a variety of solutions to hospitality providers. The divisions are highly synergistic.

Amadeus is headquartered in Madrid and is present in more than 190 markets. The company is listed on the Madrid Stock Exchange and has a market capitalization of ca. €28 billion.

{kind=link}

A High-Quality Business Model

Air IT, currently the most important value creation driver of the company, is a high-quality business with a significant growth pathway and major competitive advantages. It has a dominant position in the ex-China market, with ca. 50%+ market share in PSS while nearly 65% of the global market uses at least one type of Amadeus Airline IT Product. The market share continues to expand and there is a market-leading customer retention rate. Clients include more than 180 airlines with a pre-Covid passenger number of nearly 3.5 billion. PSS contracts are of long duration i.e., 10 years+ and there is an opportunity for upselling. PSS revenue grows through organic passenger growth, price increases, as well as new customer wins. There are major scale economies as there is little incremental cost for serving additional customers. Many clients are up for grabs including United, Delta, and Iberia. Amadeus virtually wins all competitive tenders which are objectively awarded on the basis of quality. Additional growth comes through upselling current customers. A majority of customers are eligible for upselling. We believe upselling and new client acquisitions will drive a group's EBIT growth in the mid-teens.

Air Distribution - Stable And Profitable

The Air Distribution business is likely to experience mediocre volume growth as more passengers shift to direct bookings also a result of business travel decline, and as low-cost airlines prioritize direct booking. However, we expect market share to remain satisfactory as Amadeus has invested in new technologies i.e., New Distribution Capability (NDC) improving its product offering. We expect Air Distribution to achieve lower growth but remain highly cash-generative, financing investment in higher-growing segments. In addition, hospitality remains a key growth area likely to compensate for slower growth in Distribution, with the platform being already adopted by IHG Hotels & Resorts and Marriott.

Investment Case And Valuation

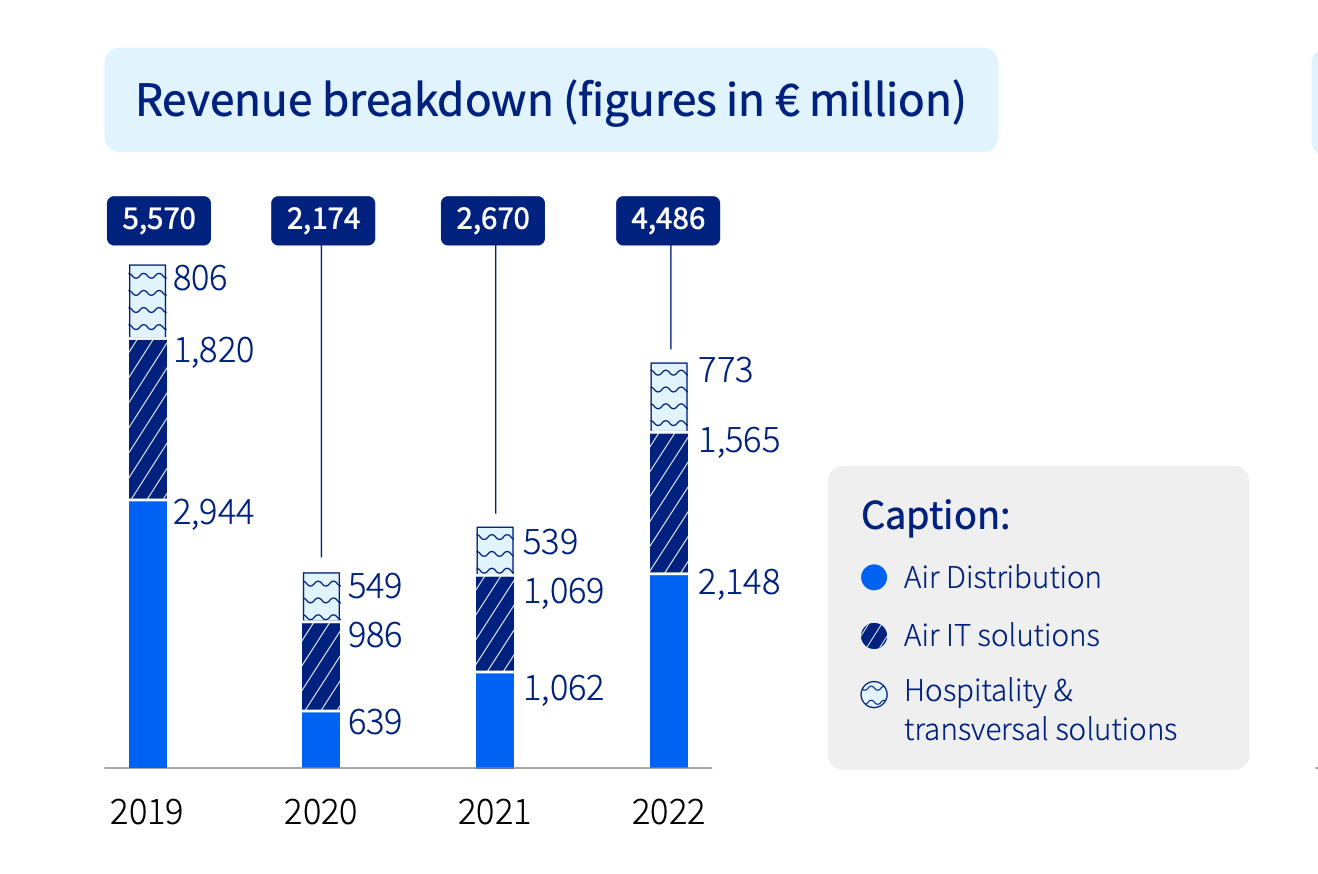

We believe that at the current valuation, Amadeus offers attractive embedded returns. We forecast €6.2 billion of sales in FY2024e and a group EBITDA of €2.4 billion. Our numbers are very much in line with sell-side analyst consensus, and we believe there may be some slight upside to these forecasts. We however remain conservative.

Going forward, in the mid-term we expect Air Distribution divisional EBITDA to grow very modestly at low single digits or >1% remaining within the €1.4-5 billion range. On the other hand, we expect Air IT to grow considerably at low teens and then low double digits % CAGR likely reaching an EBITDA of €2.4 billion by FY2028e. We expect the same growth trajectory in Hospitality, but we have less visibility and are hence less confident about that. As operational leverage comes into play, we expect significant margin improvement and roughly a group EBITDA of nearly €3.5 billion by 2028, almost a double in half a decade.

For the purposes of this valuation exercise, we use less long-dated forecasts, and we apply a forward PE multiple. We forecast an EPS of €3.1 in FY2024e. The current share price implies a forward PE multiple of 20x. Given the outstanding upcoming EPS growth and earnings quality, we believe the group should trade at a higher multiple, in line with the historical range which for the last 5 years has been above 25x EPS. We believe a 20% premium to the current multiple is warranted leading to an implied 20% upside, and a share price of €74 or $80 per share. As EPS growth is eventually achieved and Amadeus's earnings prints come in every quarter the stock should trade higher. Meanwhile, the group also trades on nearly 12x EBITDA which we find cheap given the EBITDA growth. On our mid-term assumptions on EBITDA growth, capital distributions, etc. the group would be trading at around 6x EBITDA 27e, in what we find a cheap valuation. Moreover, the company is returning 50% of the previous year’s net income as dividends and doing buybacks as well with room for more.

Risks

Downside risks include but are not limited to deteriorating macroeconomic conditions, major events impacting air traffic, a further decline in business travel, decline in travel and tourism related to environmental concerns, higher competition in distribution and Air IT, lower than expected upselling in Air IT, more direct bookings, technology risk, operational risk, etc.

Conclusion

Given the attractive fundamentals and valuation, we recommend building a long position in Amadeus IT. The equity story lacks any major short-term catalysts and is rather a long-term quality compounder at a good price.

For further details see:

Amadeus IT Group: Leading Global Travel Technology Company With Attractive Upside