DG - Amazon: Dead Money Over 4 Years What's It Really Worth?

Summary

- Amazon has an income and cash flow problem, assuming a deep recession is coming in 2023.

- The pandemic years of 2020-21 may prove the peak in its business operations and profitability for some time.

- Stock trading and business results may be following Amazon's 1999-2002 Dotcom Tech Bust pattern.

- The further downside as low as $50 a share could become reality over the next 6-12 months.

In my view, Amazon.com (AMZN) has always run a perplexing business model, all the way back to 1997. Sure, it has been able to grow revenue and steal market share in the retail world over the decades, in a truly remarkable fashion. But this is my issue and question: Will the operating business ever earn a serious GAAP profit or generate substantial free cash flow, 25 years after inception?

During a recession in 2022-23, the answer is NO. Amazon has run into serious headwinds preventing material income for shareholders. You heard me right. Despite the fact it reached a market-cap of nearly $2 trillion in 2021, the company is still struggling to generate both sustainable profits and free cash flow for owners.

The Business Model

Why? The reason is the business model. Selling goods online is perhaps the most competitive retail landscape in mankind's history. Potential profitability is a function of large physical size (economies of scale), slick advertising campaigns, efficient computer networks, tight cost controls for labor and plant & equipment, with ample and overlapping shipping options. Finally, the ability to extract some sort of pricing for goods from consumers is crucial.

The argument has always been... Amazon will eventually earn a profit after it has grabbed enough market share and can more easily raise prices. The problem is we are not there yet. Walmart ( WMT ) and Target ( TGT ) remain major competitors with online ordering and store pickup options for speedy "delivery" of goods. If Amazon tried to increase retail prices to earn a substantial profit, both store chains would likely offer many of the same goods "cheaper," ready for pickup right down the street from 95% of American consumers.

The saving grace for founder Jeff Bezos and shareholders has been the introduction of technology services and subscriptions, utilizing Amazon's computer infrastructure. AWS cloud storage has produced mountains of earnings and cash flow to fund warehouse and vehicle purchases/expansion. AWS continues to grow sales nicely in 2022 at rates around 25%. Subscriptions for online streaming movies, music, the Alexa/Echo project and now home cameras actually do and will continue to outline profitability.

However, the initial Bezos idea of online retailing has found difficulties earning sizable money. If anything, advertising revenues from third-party seller placements on its website have been the main driver of higher-margin sales for the retail division. Basically, related "services" hosting has become the bread-and-butter business model driving the stock quote.

Developing Recession

Today, the daunting obstacle for the company is a looming recession into 2023. My last Seeking Alpha article here discussed the growing odds of a serious recession next year, largely a function of the inverted Treasury yield curve in October. Amazon management just released horrible guidance for the important Christmas sales season. As it turns out, Wall Street estimates for Q4 sales overstated by 5% to 10% the new revenue projection made by the company. A huge downward revision to almost no revenue growth vs. 2022's equivalent period (+2% to +8%) is what has shocked the share price.

I mentioned the near mathematical impossibility for Amazon to grow sales beyond rates of 10% in my last Amazon article posted in December 2021 here . I suggested investors sell shares on overenthusiastic outlooks for the company by Wall Street analysts and retail investors alike. The share price has declined -40% over the last 11 months. And, as I will explain in this article, the drop in price could easily continue during 2023.

Seeking Alpha - Paul Franke, Amazon Article - December 24th, 2021

{kind=link}

Where Are the Earnings?

Let's look at the earnings conundrum. When you review financial reports and the balance sheet specifically, you can find the "Retained Earnings" line has actually expanded over the last decade. The company has achieved a net earnings intake of about $80 billion since 2012. The huge sum, nevertheless, does not stack up well with the current $1 trillion market cap (down from nearly $2 trillion at 2021's peak). If GAAP earnings could resume growing $20 to $30 billion annually, like 2020-21, one could argue today's valuation is not totally out of whack. But notice how net losses have already begun in 2022, before the recession even takes hold in 2023. What if the pandemic years actually marked the outlier peak for Amazon operating profitability? Common sense argues Amazon income may revert back to pre-Covid difficulties.

Seeking Alpha Table - Amazon Retained Earnings, 10 Years

{kind=link}

Revenue per share has grown tremendously over the past decade, but EPS has only grudgingly increased, picture below. Now, EPS is declining, with a personal expectation of decent losses appearing again in 2023.

Seeking Alpha Table - Amazon Revenue per Share and EPS, 10 Years

{kind=link}

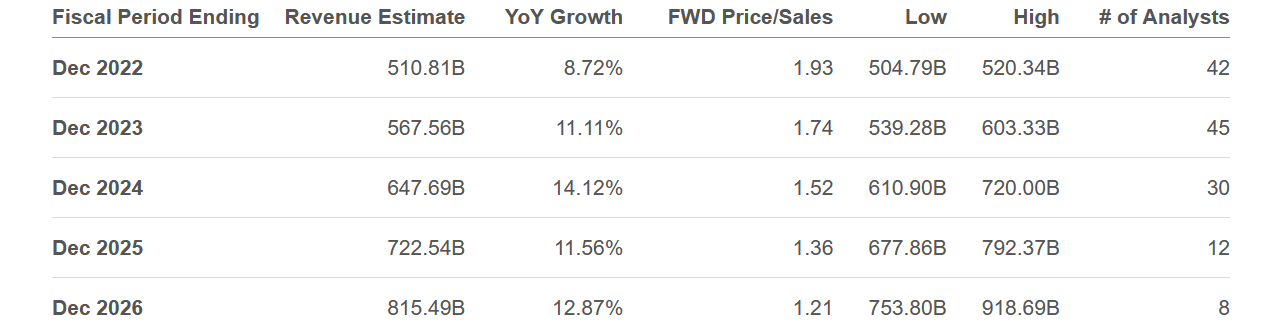

Consensus Wall Street analyst revenue expectations for the next 5 years are outlined below. Basically, I consider this forecast a bit rosy, with an average 12% annual compounded rate for company-wide sales the downshifted reality. Because of its massive size, Amazon can no longer organically grow by +30% or +40% each year like it has since inception.

Seeking Alpha Table - Amazon, 5-Year Analyst Projected Sales

{kind=link}

A 5-year EPS prediction from analysts is drawn below. Even taking these optimistic numbers, it will take a good 60 months for the current stock quote to be generating a GAAP earnings yield anywhere near today's 7.7% CPI cost-of-living adjustment annually.

Seeking Alpha Table - Amazon, 5-Year Analyst Projected EPS and P/E

{kind=link}

Believe it or not, the online-only sales model for mass merchandising is clearly the drag on operating income. Below is a 10-year graph of major competitor and peer retailers on gross margins. Amazon is far and away the weakest setup. If you are searching for an investment churning out high margins, with flexible and conservative results during recession, look elsewhere. The comparison group includes Walmart, Target, TJX Companies ( TJX ), Kroger ( KR ), Macy's ( M ), Dollar General ( DG ), eBay ( EBAY ), and Best Buy ( BBY ).

YCharts - Major U.S. Retailers, Trailing Gross Profit Margins, Since 2012

The "optimistic" analyst forecast for EPS next year still screams Amazon is uniquely expensive. Let's gulp and accept this view as accurate. The forward 1-year P/E of 57x remains the outlier for overvaluation in the major retailing space, roughly TRIPLE the median sector average.

YCharts - Major U.S. Retailers, Forward 1-Year Projected P/Es, Since January 2021

If I can find any good news on the fundamental valuation front, it's enterprise value to EBITDA. On basic stripped-down cash generation, the EV to EBITDA multiple has declined from the regular 40x to 50x range a decade ago to around 20x today. With the median average around 13x, Amazon's sliding growth future is pulling investor enthusiasm in the same direction.

YCharts - Major U.S. Retailers, EV to Trailing EBITDA, Since 2012

Free Cash Flow Problem

The bearish Catch-22 situation for Amazon is its free cash flow story. Successful investors like Warren Buffett of Berkshire Hathaway ( BRK.A ) ( BRK.B ) preach free cash flow as the ultimate goal of every business owner. Amazon is the antithesis of this philosophy. The company spends most all the cash it can find to grow future sales (and hopefully lower net costs). So, free cash flow has been a low 1% or 2% number every year (on an expensive stock quote). A misstep for shareholders, the end of exaggerated pandemic consumer spending for online goods seems to have caught management by surprise. Capital spending has continued to rocket ahead, while sales have stagnated this year.

The bad news result: free cash flow is plummeting during 2022 and is now quite negative. Compared to the stock price, Amazon has generated a negative -2.5% free cash flow yield over the trailing four quarters. Conversely. competitors have fared much better, especially those operating physical stores.

YCharts - Major U.S. Retailers, Trailing Free Cash Flow Yields, Since 2012

The kicker is this negative free cash flow problem is happening at the same time as inflation and interest rates are skyrocketing. For example, when we adjust for 1-year Treasury yields, the "real" cash flow yield at Amazon vs. risk-free bond rates has collapsed to a negative -7.7%!

YCharts - Amazon, Trailing Free Cash Flow Yield, Adjusted for 1-Year Treasury Yield, Since 2012

This number is the worst showing for the company since the end of the original Dotcom Tech Bust and recession in 2002. If you own Amazon because of an expectation for strong free cash flow generation, it has been a complete failure this year. Below is 25-year graph highlighting Amazon's clear need to borrow money, dip into cash reserves, and/or issue new equity to plug the accounting hole in 2022. One scary data point: 40% of Amazon's cash stash (including short-term investments) has disappeared over the last 9 months (a reduction of $38 billion), on capital expenditures, small acquisitions, and share buybacks.

YCharts - Amazon, Trailing Free Cash Flow Yield, Adjusted for 1-Year Treasury Yield, Since 1997

You might be asking yourself: Amazon has already declined -50% from its high last year, how much further can it drop? Great question, but you may not like my answer.

The original Tech Boom ended in the year 2000. This year also proved one of the worst to own/buy Amazon. At the stock's blowout bottom in late 2001 during a recession, Wall Street questioned if the company would stay solvent or close down. My worry is we have entered a second Big Tech bust in 2022.

If we get a monster recession in retail next year, Amazon's earnings will again be a negative number (like projected for 2022), and free cash flow could be even worse than this year. Once Amazon's bearish cash-burn picture sinks in, investors may soon give up on the stock en masse.

I have drawn the rotten free cash flow situation of 2000-2002 below for closer inspection. Even after the initial 50% decline in the quote (marked with the red arrow), Amazon would still fall another 80% into its October 2001 bottom. That's right, Amazon collapsed 90% in value over 2 years from its peak in late 1999. Trust me, if that is our future again, long-term, buy-and-hold Amazon shareholders will remember the painful bust much more than the multi-year boom that preceded it.

YCharts - Amazon, Price vs. Free Cash Flow Yield, Author Reference Point, 1998-2002

Price Target Summary

Is a Tech Bust 2.0 underway, with a 90% or greater share price loss (peak to trough) guaranteed for Amazon? No, I doubt the price decline will reach the same immediate proportions. Amazon has a number of computer-infrastructure business units worth hundreds of billions, and it is one of the largest enterprises in the world (by sales, consumers, and employees). However, recession realities have not completely played out for a Wall Street valuation of the whole corporation. If history repeats, it is entirely possible price will overshoot on the downside vs. what bulls are hoping for, as worsening operating results roll in and investor fear of the future takes control.

An approaching recession should have all Amazon shareholders concerned. Pulling all the valuation ideas together, and assuming operating results will stagnate or move in reverse vs. current analyst expectations, I come up with a projected share trading range of $50 to $100 during all of 2023. With a recession and bearish forecast of another 20% in downside for the S&P 500, companies with cash burn like Amazon will become sell targets of financial institutions, insurance companies, banks, hedge funds and actively-managed mutual funds.

A 12-month "fair value" target of $80 seems rational to me. My conclusion, depending on the severity of a global economic downturn, is additional Amazon investment losses as great as 50% are probable over the next 6-12 months. My worst-case scenario is EV to EBITDA and revenue ratios for the company will fall back to the same level as slower growing (macroeconomic mimicking) Walmart and Target valuations. For a company experiencing low growth and high cash burn, an abnormally extended valuation makes no logic sense.

YCharts - Major U.S. Retailers, EV to Revenues, Since 2012

Assuming a mild economic downturn hits, the stock quote could absolutely remain around present levels, basically the century mark. In my view, to get any type of material advance in Amazon's price, the economy will need to expand beyond its present size, while management keeps labor and real estate spending costs under control. For sure, higher oil prices (shipping costs) have been a drag on 2022 results. Further jumps in energy expense would not be welcome news.

Of course, improving labor and energy cost pressures, alongside strong consumer spending in 2023 would be the bullish scenario to contemplate and weigh in your decision process. A positive economic backdrop could allow for some earnings by 2024 with less cash burn. My theoretical upside math suggests best-case reward for the stock quote is only $120-$150 next year. So, owning Amazon may boil down to a binary choice, dependent on your personal outlook for the global economy during 2023-24.

I'll admit I have never owned a serious position in Amazon shares, because I do not completely understand how the business model creates actual profits in the highly competitive retail field. If sales are no longer growing, why would any potential owner in the business get excited about its long-term future, based on its weak income and free cash flow totals matched against high and rising inflation/interest rates? Today, the argument that Amazon "always" finds a way to grow and enrich shareholders is quickly losing its luster. Too many facts are getting in the way. The stock price is the same as 4 years ago, and downside risks are spiking for 2023. Food for thought anyway.

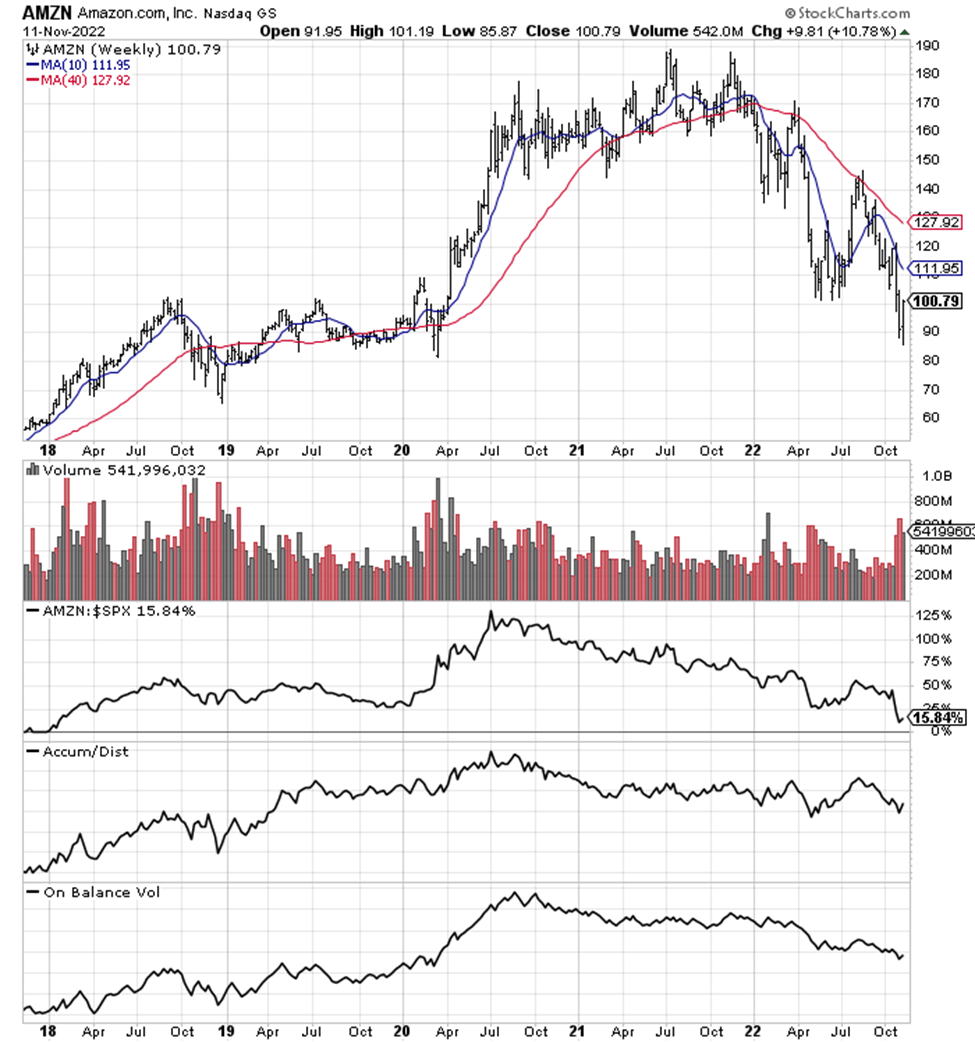

StockCharts.com - Amazon, Weekly Chart of Price and Volume Changes, 5 Years

{kind=link}

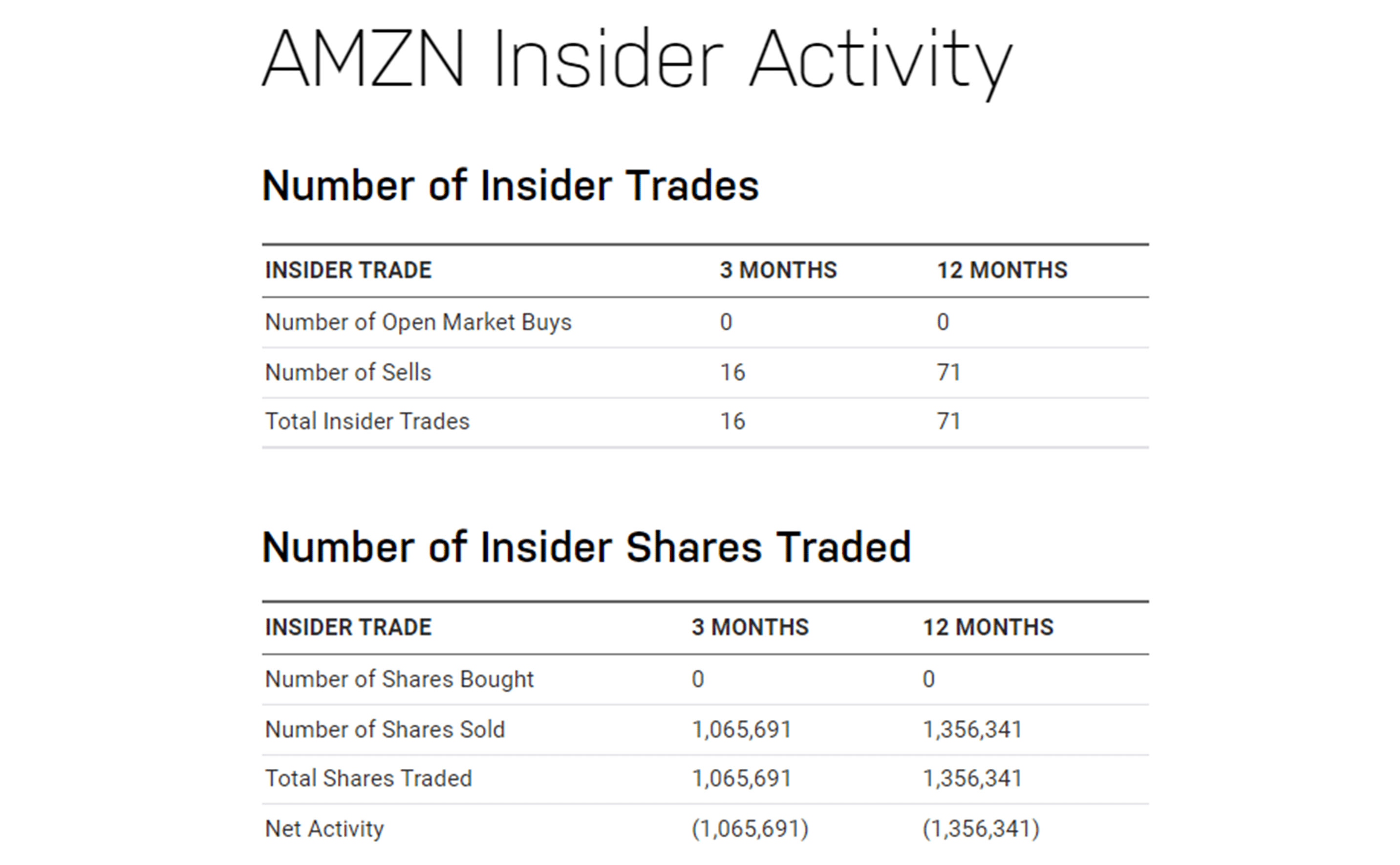

Based on heavy management and insider selling in the stock over the last 12 months, maybe it's time to look elsewhere for a productive positive return on your investment capital. I rate Amazon shares as a Sell .

Nasdaq.com - Amazon, Insider Trading Activity, November 11th, 2022

{kind=link}

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Amazon: Dead Money Over 4 Years, What's It Really Worth?