ABEV - Ambev: Cautious Outlook For A Difficult Proposition

2023-12-11 00:37:55 ET

Summary

- Ambev is a quality business, providing exposure to the LatAm market. Growth has been strong, although the business faces increased competition from Heineken.

- The company has a diverse portfolio of brands, allowing for its market-leading margins. Ambev has faced some erosion but remains attractive.

- Premiumization and non-alcoholic alternatives should support MSD growth in the coming years as consumers increasingly seek differentiation in the face of substantial choice.

- Current economic conditions have contributed to near-term headwinds, with volume declining. This said, positive pricing action has offset this subsequently, with improvements ahead.

- The decline in the Brazilian real and potential FX risks going forward make Ambev a riskier investment compared to its peers.

Company description

Ambev ( ABEV ), headquartered in São Paulo, Brazil, is one of the largest beverage companies in the world. It operates across South America, North America, and Central America, with a diverse portfolio of alcoholic and non-alcoholic beverages. Ambev is currently a subsidiary of Anheuser-Busch InBev ( BUD ), which is currently still facing issues following its poorly received marketing efforts and subsequent responses.

The company also has a licensing agreement with PepsiCo ( PEP ) to produce and distribute its products in certain regions.

{kind=link}

Share price

Ambev's share price movement has been destructive in the last decade, losing over 50% of its value. This is due to declining financial performance and weakness in the BRL.

Financial analysis

{kind=link}

Presented above is Ambev's financial performance for the last decade.

Revenue & Commercial Factors

Ambev's revenue has grown at a healthy level, with a CAGR of 10% into the LTM. The business has generally achieved consistent growth, with only a single period of growth below 4%.

Some have suggested this is a declining or stagnating business but that is not the case in B$. The issues come when you convert this Brazilian company's B$ earnings into USD (Growth rate declines to 1%, the implications of which we will discuss later).

Business Model

Ambev operates in a wide range of beverage categories, including beer, carbonated soft drinks, bottled water, energy drinks, and non-alcoholic malt beverages. This product diversification allows the company to tap into multiple consumer segments and create a robust portfolio that caters to different preferences and occasions. This is critical to success within this industry, as consumer preference for differing tastes is high, meaning the ability to capture high market share requires a broad suite of brands.

Ambev boasts an extensive brand portfolio, featuring both international and regional brands. Globally recognized beer brands like Budweiser, Stella Artois, and Corona are part of its portfolio, along with local beer brands tailored to specific markets. The strength of these brands affords Ambev a premium position in the market, catering to the domestic and tourism markets successfully.

Ambev's market leadership in Latin America, particularly in Brazil, is a key driver of its growth. The company has an unrivaled distribution network, allowing it to reach a large customer base efficiently. Importantly, its brands are positioned well to be the preferred supply to the many institutions that serve beverages, with scope for pushing its competitors out. This ensures the company remains a leader in the market.

Operationally, Ambev emphasizes efficiency and cost management. By optimizing its production processes and supply chain, the company can maintain competitive pricing and profitability while offering products at various price points and brands. S&A spending has remained within a 3% band for the entirety of the decade, illustrating this consistent control.

Our expectation is for these factors to be underpinned by healthy economic development in LatAm, supporting LSD/MSD growth in the coming years. What could derail this return for investors is FX. Ambev earns its revenue in a range of currencies while reporting in B$. Said B$ has declined over 50% against the dollar, essentially eliminating any hope for gains for dollar (or any Western currency)-denominated investors. This continues to be the primary risk for Ambev in the coming years.

Ambev's competitors are the various other leading brewers, such as Heineken ( OTCQX:HEINY ), Carlsberg ( OTCPK:CABGY ) (from an investment perspective, it does not operate in LatAm), Compañía Cervecerías Unidas S.A. ( CCU ), and Molson Coors ( TAP ). Heineken in particular has been executing extremely well, outperforming Ambev and taking market share. The company is investing a further $300m in the country, representing greater risk. As the scope for outsized growth declines, relative performance becomes increasingly important. This makes us slightly concerned that Heineken could force Ambev into slowing growth and/or declining margins.

Key industry trends

Premiumization refers to the increasing consumer demand for higher-quality, premium products that offer superior taste, unique flavors, and added value. This trend has been prevalent in the beverage industry, particularly in the beer segment, where consumers are willing to pay a premium for craft beers, specialty brews, and high-end brands. Craft Breweries in particular have been taking market share from all the leading players, although not necessarily to a material level. Based on its current brand portfolio, we believe Heineken is better placed than Ambev to capitalize on this, and its $300m investment is specifically into expanding its premium portfolio. This is not to say Ambev will also not do well, with outsized growth from its Premium & Super Premium segment.

The rising awareness of health and wellness has led to increased demand for non-alcoholic beverages globally. Consumers, especially younger demographics, are seeking healthier alternatives to traditional sugary and caloric beverages. Ambev, in line with its ultimate owner, has developed a range of zero-alcohol alternatives to its most popular products. We do note that its marketing for said products is not at the same level as Heineken, calling into question its commitment. If this trend continues to accelerate rapidly, we could see it losing pace. As an example, Heineken uses its highly coveted F1 sponsorship on track to advertise Heineken 0.0.

Economic & External Consideration

Current Economic Conditions are defined by elevated Inflation and elevated interest rates, creating uncertainty and softening market and economic conditions. We believe this is impacting the business in the following ways:

- Inflationary Pressures - Higher inflation has led to increased input and operational costs, contributing to a reduction in margins.

- Consumer Spending - The combination of these economic factors has contributed to softening discretionary spending, as consumer finances are squeezed.

Our expectation is for economic improvement to develop over the coming 6-18 months, as rates finally begin to decline and expansionary policy can be enacted. The Brazilian economy is forecast to grow by 1.2% in 2024 , with lower employment growth and high inflation remaining. This will drag on Ambev's financial performance, likely meaning LSD growth at best.

Margins

Ambev's margin deterioration in the last decade has been incredibly poor. The business has lost 20ppts of EBITDA-M in 10 years, creating a 6ppt delta in the growth of Revenue vs. EBITDA. This has been driven by industry development during this period, with substantially higher competition.

We cannot confidently say this decline will subside, but Management considers this a key area for improvement. Progress looks position in the most recent quarter but the outlook remains uncertain. This will likely negatively impact its competitive position but we believe action must be taken as the industry matures and the scope for growth declines.

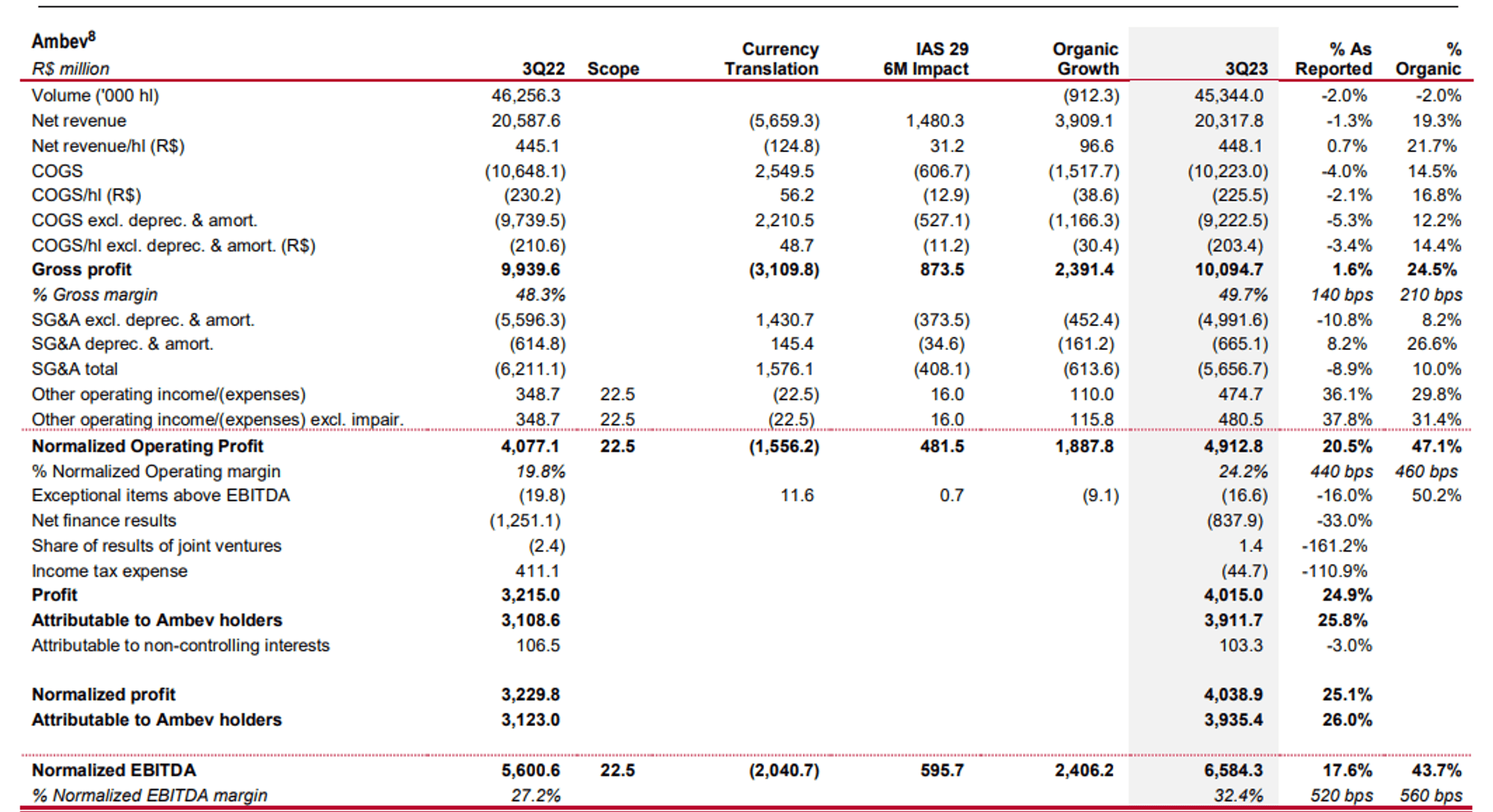

Quarterly results

{kind=link}

Presented above is Ambev's most recent quarterly results.

Key takeaways from this are:

- Volume growth decline (-2.0%). This illustrates the wider macro weakness experienced and the knock-on effect on demand, alongside the impact of elasticity following price increases.

- Revenue/hl exceeds COGS/hl, suggesting the business is continuing to benefit from actions to increase margins, with GPM up 1.4ppts.

- Revenue growth has turned negative (-1.3%), which we attribute to the rapid increase of prices to protect margins coinciding with slowing demand. Pricing is no longer able to offset the decline in volume.

- Although we are disappointed to see revenue growth declining, the significant improvement in adj. EBITDA-M (+5.2ppts) is far more important for the long-term success of the company.

We believe this was a positive quarter for the business but we believe the company is at a potential crossroads. Margins are trending upward and will likely do so for another quarter or two as the full-year impact of pricing is felt. This said, we struggle to see a bounce back of volume immediately as macroeconomic conditions weaken.

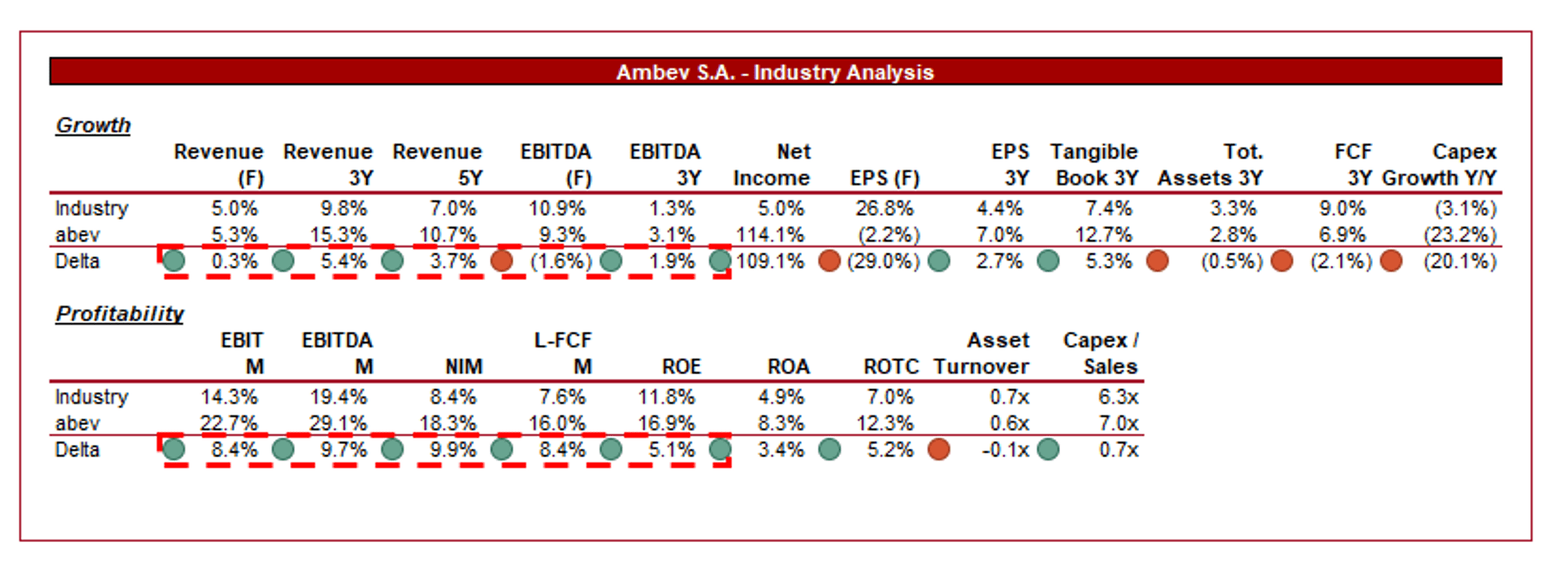

Industry analysis

{kind=link}

Presented above is a comparison of Ambev's growth and profitability to the average of its industry, as defined by Seeking Alpha (7 companies).

Ambev performs extremely well relative to the peer group, with superior growth and margins. The majority of its peers are heavily exposed to the West, allowing Ambev to benefit from the development of the industry in LatAm. Further, its substantial position in LatAm, where there is reduced competition relative to the US or Europe, affords Ambev superior margins.

Despite these factors, Ambev continues to face a material issue, namely FX. Heineken has an EBITDA-M of 19% yet we are demanding Management improve its current level of 27%. The reason is to offset the risks around FX.

Valuation

{kind=link}

Ambev is currently trading at 10x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the increased competition the business faces and the decline in margins. Our suggestion would be 20-30%, as this would reflect the current decline while pricing in the potential for further erosion.

Its relative position to peers is more difficult to assess, as the discount materially reflects the FX risk delta to its peers. The B$ generally performs well relative to the USD when oil prices are high, which is the case currently. This implies near-term stability but beyond this, uncertainty.

We recently wrote a paper on Heineken and rated the stock a buy. It is currently trading at 10x NTM EBITDA with an FCF yield of 5.7%. This is comparable to Ambev, lacking a degree of cash flow while not having the same degree of FX risk. Further, AB-InBev is trading at 11x EBITDA with an EBITDA-M of 3% (acknowledging it is going through problems currently).

Final thoughts

Ambev is a good business. The company has an impressive position in a substantial market, a range of strong brands, and attractive financials. Competition has increased and continues to be a concern, but we still believe healthy LSD growth is sustainable going forward. When combined with its current margins, returns look great relative to its valuation.

The issue for Ambev is its exposure to currencies that historically depreciate against the dollar. This makes this a tough investment for Westerners. We believe a better risk-adjusted return profile is found with Heineken, and potentially even by just owning its parent, ABI.

For further details see:

Ambev: Cautious Outlook For A Difficult Proposition