ABEV - Ambev: Improving Operating Metrics With Healthy Dividend Yield Buy

2023-09-14 01:25:35 ET

Summary

- Ambev faced a shrinking bottom line during the past year and a half as higher commodity prices squeezed gross margins.

- Trends have improved in Brazil beer driven by increasing market share within the premium category along with recovery in international segments.

- ABEV upgraded its COGS guidance for 2023 and now expects an improvement in gross margins for H2 2023.

- We ascribe a Buy rating due to improving operational performance, a healthy dividend yield of 5.3% along with a relatively cheap valuation.

Investment Thesis

Ambev ( ABEV ) had a relatively challenging last two years as higher commodity prices squeezed their gross margins with the shares falling about a fifth of its value since peaking in 2021.

We believe the secular trends are improving with a respite in commodity prices and lowering of distribution expenses. Its significant improvement in premiumization grabbing market share in Brazil beer segment along with recovery in international prices bodes well for the company in long term. With a comfortable valuation at a discount to its peers and historical averages along with a healthy dividend yield of 5.3%, we ascribe a Buy rating to Ambev with a target price of $3.2.

Company Background

Ambev produces and markets beer, carbonated soft drinks, and other non alcoholic beverages and products across about 18 countries in the Americas. It has a leading position in Brazil through its wide portfolio of offerings in its key brands such as Brahma, Skol, Beck's and Antarctica.

Improving Earnings

ABEV reported strong earnings momentum in Q2 with revenue growth of 5% YoY while it was up 20% YoY excluding FX. The strong growth was driven by growth across beer and NAB brands in Brazil partially offset by decline in L. America South ((LAS)) segment as well as in Canada. Brazil beer sales grew 10% YoY despite a 2.5% decline in volumes on tough comps as a result of strong pricing and revenue management along with premiumization. Volume growth of mid-30s in its premium portfolio (Spaten, Corona and Stella) is encouraging and the company has been able to grab market share within the premium segment. In comparison, Heineken reported a high single digit volume growth in premium category while Amstel reported a low-30s volume growth in the category. Brazil NAB revenue grew 7.5% YoY supported by pricing actions with volumes declining 2.2% YoY, despite Pepsi volumes growing in low single digits. International segments continue to recover within CAC, where Dominican Republic constitutes majority of sales, on the back of improvements attributable to tourism recovery, with sales growing 4.8%. Also, in LAS segment Chile made significant improvements enabling strong EBITDA margin expansion and cash generation bearing the fruits from its establishment of local production facility in lieu of the partnership with Coke bottlers enabling higher product coverage and favorable mix as well as improvement in macros in Dominican Republic and Chile.

Gross margins expanded by 170 bps YoY on the back of gross margin expansion across all regions except for Canada due to pricing actions and product mix. SG&A leveraged on the back of lower distribution expenses due to a fall in crude prices and operational efficiencies which were partly offset by continued investment in brands leading to Adj. Organic EBITDA margin expansion by 300 bps.

| Particulars |

| Brazil Beer |

| Brazil NAB |

| CAC |

| LAS |

| Canada |

| Vol. growth |

| (2.5%) |

| (2.2%) |

| (2.8%) |

| 0.6% |

| (6.2%) |

| Rev/ HL growth |

| 12.9% |

| 10.0% |

| 7.7% |

| 81.1% |

| 6.6% |

| Rev growth |

| 10.1% |

| 7.5% |

| 4.8% |

| 82.1% |

| (0.0%) |

| EBITDA % chg. |

| 400 bps |

| 310 bps |

| 100 bps |

| 380 bps |

| 120 bps |

Balance sheet position remains robust as the company ended with cash balance of $2.6 bn with a total debt outstanding of just over $850 mn yielding a net cash position allowing greater flexibility in capital management.

It upgraded its growth guidance for full year Brazil Beer COGS/ hl from 6.0-9.9% to 2.5-5.5% leading to further upsides on the margin front. Brazil Beer cash COGS/ hl has been easing from 18% in 2022 to 12% in H1 2023 further implying about a decline of ~3% in H2 2023 as a result of respite in commodity prices such as barley and malt which has declined substantially over the past one to two years.

{kind=link}

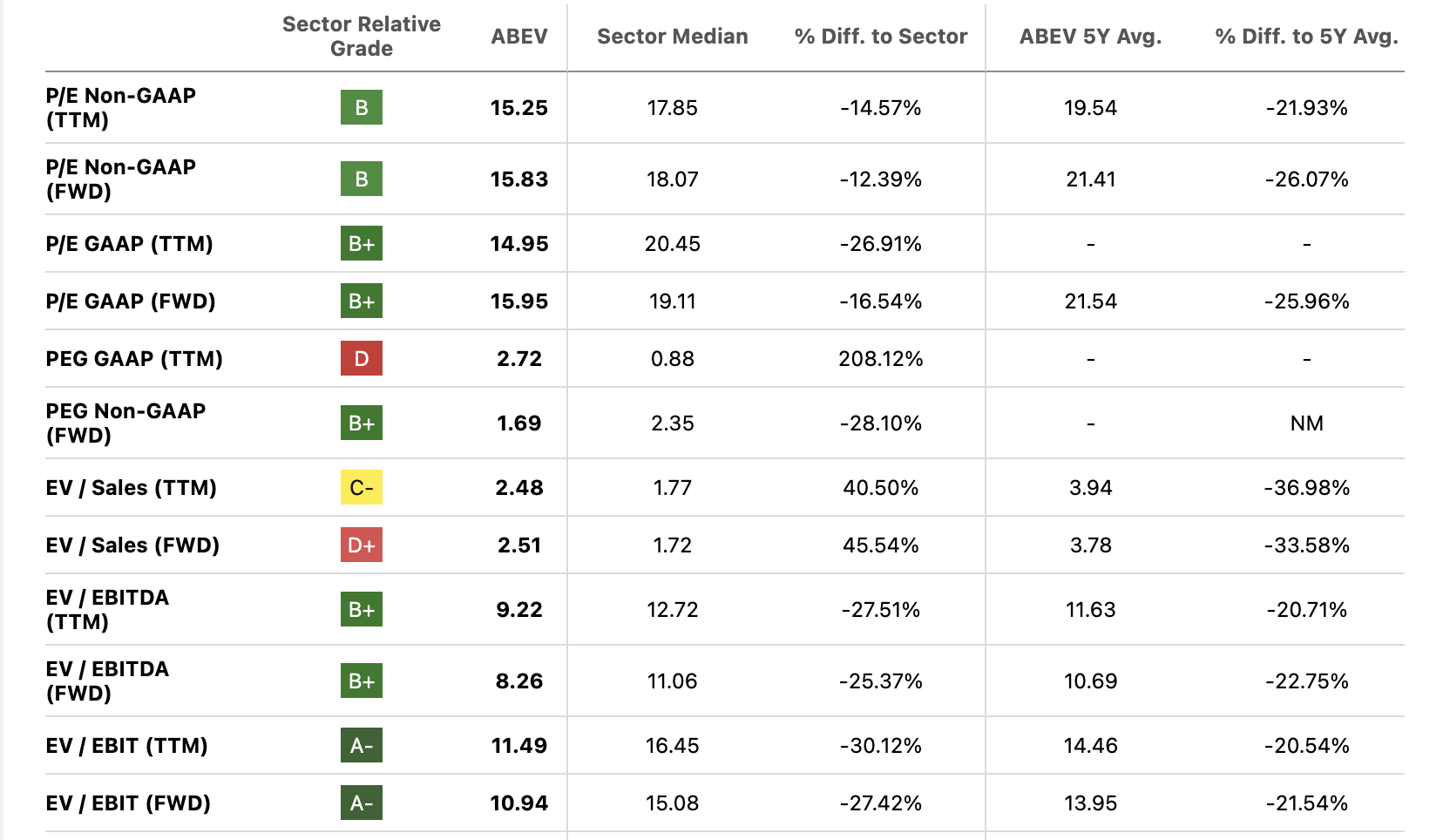

Valuation

ABEV trades at 15.8x Fwd P/E, at a discount to its peers as well as at a steep discount to its long term historical average. We rate it as Buy as a result of strong earnings and improving outlook along with fundamental improvements within Brazil beer industry. We ascribe a target price of US$3.2 at 18.2x Fwd P/E, in line with the peers.

{kind=link}

Risks to Rating

Risks to rating include

1) Any significant increase in input costs including that of commodities such as barley, malt and sugar and packaging material such as PET and glass could squeeze gross margins

2) Macro uncertainties and any decline in consumer spending can significantly impact volumes

3) Its exposure in emerging markets such as Brazil, Argentina, Colombia and other South American countries exposes them to significant political risks as those countries have witnessed periods of political instability

4) Competitive pressures can intensify leading to higher promotional environment and squeeze operating margins

Conclusion

We believe Brazil beer industry is fundamentally stronger with low price elasticity as price hikes has been absorbed by the consumers which has not led to a meaningful decline in volumes. ABEV's growing market share in premium category driven by management's efforts on brand investments remains a key moat. We believe with the recovery in international segments and relatively comfortable valuation warrants a Buy rating for Ambev. Along with that, it offers a healthy dividend yield of 5.3% and have a historical average dividend payout ratio of 80-90%. We believe ABEV is likely to achieve the bottom line estimates driven by gross margin expansion in H2 and with a track record of higher dividend payouts would be able to generate a dividend yield of 5.3%.

For further details see:

Ambev: Improving Operating Metrics With Healthy Dividend Yield, Buy