ABEV - Ambev: Long-Term Downtrend With Shaky Dividend And Lack Of Catalysts

2023-09-15 22:54:29 ET

Summary

- Ambev is a Brazilian brewing company and the largest PepsiCo bottler outside the United States.

- The company's dividend appears to be at risk based on analysis of its free cash flow, debt load, and cash position.

- The Brazilian beer market is not expected to provide significant growth opportunities for Ambev, and the stock has been on a long-term downtrend.

Ambev S.A. ( ABEV ), formally Companhia de Bebidas das Américas, is a Brazilian brewing company headquartered in São Paulo, Brazil. Ambev operates in nearly 20 countries in the Americas and is the largest PepsiCo, Inc. ( PEP ) bottler outside the United States. Ambev generated $15 billion in 2022 revenue and is one of the largest companies in Brazil.

I have a heavy interest in Consumer Staples stocks, primarily due to their reliable dividend and as the name suggest, their staple nature. Ambev showed up on my screening list, which typically looks for stocks yield above 5% when it comes to this sector. While I was not surprised to find the stock in this screening list, I was indeed surprised to find Seeking Alpha's quant ratings flashing the dividend warning shown below.

Ambev Dividend Warning (Seekingalpha.com)

{kind=link}

Why was I surprised? We are talking about a consumer staple company and one that helps sells popular (some may say addictive) products like Stella Artois. So, how can this company not be strong enough to sustain its dividends? Let's find out if my analysis below agrees with Seeking Alpha's warning.

Dividend History

Ambev has been paying dividends at least since 2006 according to its investor relations page. According to its dividend policy, Ambev is supposed to pay at least 40% of its adjusted annual net income as dividend.

" Our bylaws provide for a minimum mandatory dividend of 40% of our adjusted annual net income, if any, as determined under IFRS at our individual financial statements "

Being an American Depository Receipt [ADR], it is not surprising that Ambev's dividend payment frequency is not the usual four times or even the less common, two times a year. For example, the company paid only one dividend in 2022 vs. three in 2021. But more importantly, the total dividend (in USD) paid in 2022 was 14.43 cents while the 2021 total was 12.19 cents. Add in the currency fluctuations, things get even more trickier when it comes to tracking things like dividend growth rate and dividend growth streak. So, let's just evaluate whether the dividend appears safe in the current context.

Is The Dividend Sustainable?

Let's do a three-prong analysis using my three favorite metrics: Free Cash Flow [FCF], debt load + interest expense, and Cash position. I've used a personal rating scale in analyzing dividend safety where I start my analysis with a "B" on average. You may ask why? Quite simply, B is generally considered an average grade and as a company's metric dictates, I adjust the scale up or down based on the result.

Let's start with Free Cash Flow first.

- Total shares outstanding : 15.75 billion

- 2022's annual dividend: 14.43 cents/share

- FCF required to cover dividends at 2022's rate: $2.27 billion (that is, 15.75 billion shares time 14.43 cents/share)

- Ambev's trailing twelve months' [TTM] FCF: $2.79 billion, which gives the stock a payout ratio of 81% based on TTM FCF. That leaves the company with $520 million (using TTM FCF and 2022's dividend) to handle other expenses including but not limited to interest expense, depreciation, and amortization.

- Ambev's average quarterly FCF over the last 5 years: $752 million, which works to about $3 billion on annualized basis. Using this number, Ambev's payout ratio is a little lower at 75%.

- Based on FCF, it appears like the dividend appears safe for now but dividend growth, if any, is likely to be anemic given the lack of wiggle room. On my personal scale, that would be a "C" at best if there is no reasonable assurance of dividend growth either through history or current metrics.

Let's now look at Ambev's debt load and interest expense on debt. The reason I tend to evaluate this separately is due to the fact that interest expense on debt is not subtracted from reported FCF. Ambev has a total debt load of about $855 million , which in my opinion is remarkably low for a company with $44 billion market capitalization. To be sure, I looked up additional sources and at least one other source has the same information as can be seen here.

Let's now get into the interest expense. I consider this a more important number than the actual debt level for companies like Ambev, which I expect to be around for many years. In the last twelve months, Ambev has paid about $152 million in net interest expense (after subtracting the interest and investment income earned). We calculated above that Ambev has about $520 million left in its FCF after accounting for dividends (that is, TTM FCF of $2.79 minus 2022's dividend commitment of $2.27 billion). Subtracting the TTM net interest expense, we arrive at a paltry balance of $368 million on an annual basis, which makes me push my personal scale rating to "D".

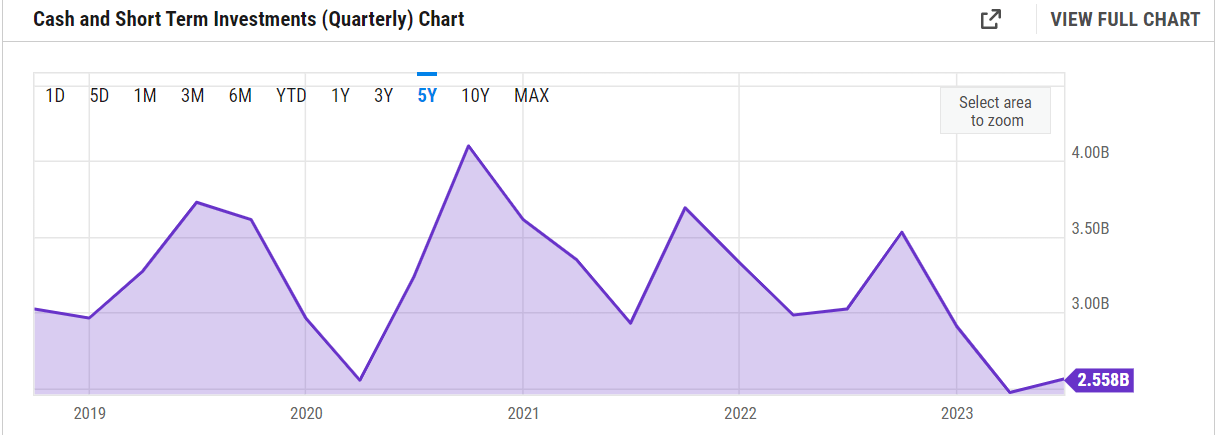

Finally, I analyze a company's cash reserves and its ability to pull funds quickly (short-term investments) in case of an immediate need, like a debt being called or operational challenges. Ambev's cash and short-term investment pile of $2.55 billion its almost at its lowest point in the last 5 years, suggesting cash burn, which when combined with the low margin in FCF and high interest expense on debt makes me push the dividend safety to a "F", which brings it in line with Seeking Alpha's grade.

{kind=link}

Business Outlook and Conclusion

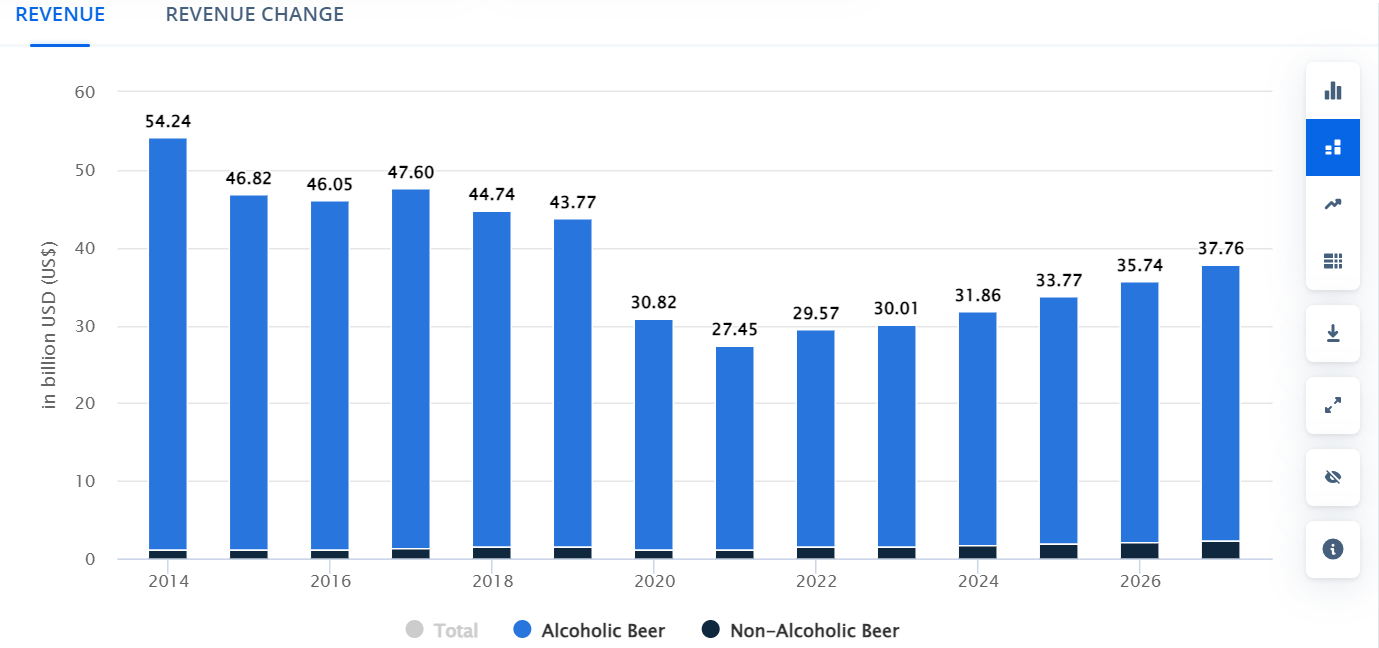

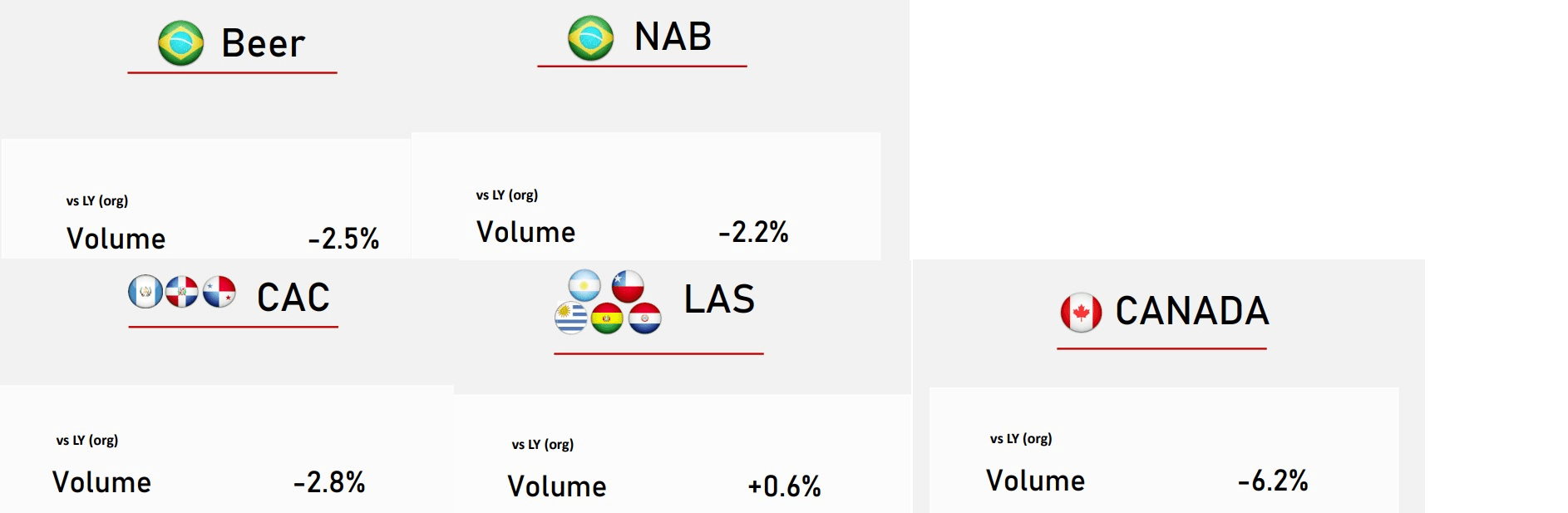

The Brazilian beer market is expected to grow at about 6%/yr till 2027, which is nothing to be excited about. Ambev's own numbers from recent Q2 show volume is under pressure across all categories and locations. Given these two factors, it is hard for me to make a case for the stock at nearly 16 times forward earnings.

Brazil Beer Market (statista.com)

{kind=link}

{kind=link}

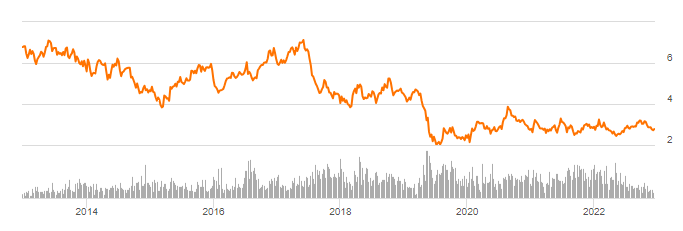

The stock has been on a long-term downtrend as shown in the chart below, losing more than 50% of its value in the last 10 years. If arguably the most popular World sporting event couldn't boost sales and profits significantly, I am not sure there are too many positive catalysts around for the stock to turnaround meaningfully in the medium term.

{kind=link}

I suggest the average investor to stay away from this stock as its business, while mature, lacks catalysts in my opinion for a turnaround and the dividend appears shaky, if not downright dangerous.

For further details see:

Ambev: Long-Term Downtrend With Shaky Dividend And Lack Of Catalysts