BUDFF - Ambev's Brewing Trouble: A Sobering Outlook

2023-09-14 12:38:50 ET

Summary

- Ambev faces operational challenges due to inadequate logistics infrastructure in Brazil and increasing competition with low entry barriers in the sector.

- The Brazilian government's potential discontinuation of interest in shareholders' equity (JCP) could significantly impact Ambev's profitability and capital structure.

- Recent inquiries by the Brazilian tax authorities into Ambev's operations related to income tax payments on profits earned abroad have raised additional concerns, adding to the company's challenges.

Brazilian beverage giant Ambev ( ABEV ) operates across the Americas, including Brazil, Canada, and Argentina, under the control of Anheuser-Busch InBev ( BUD ) ( BUDFF ), the world's largest brewer.

However, the company has faced operational challenges stemming from Brazil's inadequate logistics infrastructure, impacting its efficiency and market reach. Additionally, the sector's low barriers to entry have led to increased competition. The partnership between Coca-Cola and Heineken to restructure distribution in Brazil presents concerns, as it may heighten competition for Ambev due to the competitive nature of the involved companies.

Despite Ambev's recovery in profitability due to lower commodity prices, its stock has underperformed the Ibovespa (Brazil's stock exchange) tracked by the iShares MSCI Brazil ETF ( EWZ ) year-to-date.

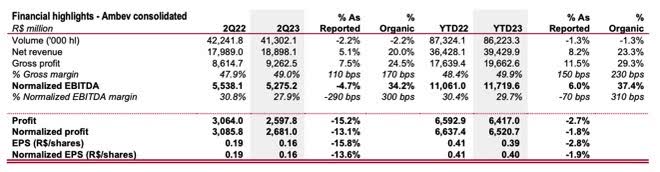

The company's second-quarter results met expectations but showed modest margin expansion, disappointing volumes, and ongoing challenges in the Latin American South region, particularly Argentina.

Furthermore, Ambev's shares have been impacted by the government's proposal to eliminate interest on equity, which could significantly affect the company's capital structure. There is also an ongoing investigation by the Brazilian federal government (see section below) into potential irregular tax operations abroad.

Given its unattractive valuation and potential for medium-term underperformance, Ambev should face profitability challenges in the coming years.

Ambev's latest results

Ambev delivered reasonable second-quarter earnings results, with modest revenue and slightly improved margins.

Positive highlights were seen in the Brazil Beer and NAB Brazil segments, with net revenue per hectoliter (ROL/hl) showing growth. The CAC operation also showed optimism with a year-over-year expansion in EBITDA margins.

The premium beer segment, including brands like Original, Spaten, Corona, and Stella, outpaced competitor Heineken in Brazil, with a 10% increase in the beer segment compared to the second quarter of 2022. Non-alcoholic beverages in Brazil accounted for 3% of sales.

However, Canada's volume continued to be impacted by a weak beer industry, although the segment managed a slight margin expansion. The LAS segment, particularly the operation in Argentina, was the negative highlight due to the country's volatile macroeconomic situation.

{kind=link}

Ambev's IR

Ambev reported net revenue of R$18.9 billion, up 5.1% year-over-year, and EBITDA of R$5.3 billion, a 4.7% year-over-year decrease, resulting in an EBITDA margin of 27.9%, down 3.5 percentage points year-over-year. Net profit also decreased by 30.2% year-on-year, reaching R$2.6 billion.

Breaking down Ambev's results by segment:

-

Brazil Beer: Showed net solid revenue per hectoliter (ROL/hl) growth, cost per hectoliter (COGS/hl) deceleration, and stable SG&A. Revenues were R$8.7 billion, up 10% YoY, with an EBITDA of R$2.3 billion, down 10.5% YoY.

-

Non-alcoholic beverages (NAB) Brazil: Achieved slight year-on-year growth in net revenue per hectoliter (ROL/hl) and reported a slight sequential increase in cost per hectoliter (COGS/hl). Revenues reached R$1.7 billion, up 7.5% YoY, while EBITDA was R$376 million, down 11.5% YoY.

-

Central America and the Caribbean ((CAC)): Showed decent figures with sequential volume improvement but a year-on-year retraction. Revenues amounted to R$2.5 billion, a 1.2% YoY increase, with EBITDA of R$920 million, up 15.1% YoY.

-

Latin America South ((LAS)): Reported weak volumes in Argentina but performed decently in other ex-Argentina countries. Revenues were R$3.3 billion, down 5.3%, and EBITDA reached R$838 million, down 7.4% YoY.

-

Canada: Impacted by a weak industry and soft volumes, with slight net revenue per hectoliter (ROL/hl) growth. Revenues were R$2.8 billion, down 2.5%, and EBITDA was R$838 million, nearly unchanged YoY.

Ambev may expect improved margins in the coming quarters due to declining primary commodity costs. However, inflationary pressures in Argentina and Chile pose challenges for the LAS segment, warranting attention.

Potential discontinuation of interest on shareholders' equity

The risk associated with the potential discontinuation of interest on shareholders' equity (JCP), a practice specific to the Brazilian tax system and corporate finance, revolves around companies paying interest to their shareholders on the equity invested in the company, carrying distinct tax implications in Brazil. Unlike dividends, JCP is accounted for as an "expense" for companies, reducing taxable net income.

This issue has recently influenced Ambev's stock performance, following a proposal by the Brazilian government to address this matter in Congress in early September.

The JCP discontinuation carries significant implications for the Brazilian beverage company. In 2022 alone, Ambev paid its shareholders R$12 billion in interest on shareholder's equity (JCP). Some analysts in the Brazilian market suggest that if the company maintains its current capital structure, the negative impact on profits in 2024 could be as high as 23%. There is a risk that Ambev's capital structure, currently at 0.3 times net cash, might become inefficient.

However, if JCP is removed, Ambev, like other Brazilian companies, will likely explore strategies to mitigate potential impacts that the market may not be considering. These strategies could involve leveraging and utilizing tax credits, among other measures.

One potential approach for Ambev could be to reinvest the money in its operations organically and through acquisitions. This seems more plausible than announcing a substantial one-off dividend, especially given the ongoing deleveraging efforts of controlling shareholder Anheuser-Busch InBev.

However, there are challenges associated with this hypothetical scenario. A significant one-off dividend might not align with Anheuser-Busch InBev's strategic goals for deleveraging. Additionally, the liquidity of the debt capital market could be a constraint, given that Ambev's leverage of 1.0 times equates to R$24.4 billion, while its gross cash position stands at R$12.3 billion.

Moreover, ongoing Brazilian tax reform discussions might introduce a new dividend tax, adding further pressure to the situation.

Ambev under Brazilian tax authority scrutiny

The issues surrounding Ambev's situation do not end here. Recent news reports indicate that the Brazilian tax authority has raised questions about Ambev's operations related to the payment of income tax on profits earned abroad.

The focus of the inquiry was Ambev's practice of refunding billions in taxes paid abroad. Like other companies, the brewery uses the income tax paid by its foreign subsidiaries to offset the income tax owed in Brazil. As a result, this offsets the income tax, and the Social Contribution on Net Profit (a tax companies pay on their net profits) is paid monthly in Brazil.

According to the Brazilian Federal Revenue Service, this practice is irregular because it is akin to the government reimbursing the tax that the company has paid in another country.

The bottom line

Ambev's second-quarter results presented a mixed picture, characterized by weak volume offset by higher revenue per hectoliter and effective cost management.

In the medium term, there is a downward trend in the primary commodities that constitute Ambev's cost of goods sold (COGS). However, I perceive limited growth potential for the company and minimal upside compared to the current market price. Additionally, there is a sense of caution regarding the potential ramifications of implementing the Selective Tax—a tax applied to specific products and services deemed harmful to society or the environment.

Trading at a forward price-to-earnings (P/E) ratio of 15.8x, which is 26% below its historical average , the stock appears somewhat discounted but not enough for a bullish stance in my analysis, considering the relatively restrained growth expected in its operations in the medium term. The EPS projection 2023 indicates a decrease of 1.8%, with a modest growth forecast of only 16% for 2024.

{kind=link}

Seeking Alpha

In summary, I view Ambev's performance as potentially quite fragile, given the challenges the company must confront shortly. These challenges include the impact of the Brazilian tax reform, an ongoing investigation into possible tax irregularities, and the uncertain outlook for Argentina, which continues to cast a shadow over more optimistic operational figures and the potential for medium-term underperformance.

For further details see:

Ambev's Brewing Trouble: A Sobering Outlook