ABEV - Ambev: Strong Growth Levers With Massive Upside Potential

2023-03-21 09:22:47 ET

Summary

- On the back of rising prices and rural recession, the consumer staples sector did not fare well in 2022, with the NSE and BSE consumer indexes plummeting by double digits.

- This year, there is expected to be a pick-up in growth along with margin expansion for consumer staples.

- This inexpensive, high-potential company has a potential upside of more than 50%, making it a good pick for investors looking to capitalize on market upticks.

Investment Thesis

On the back of rising prices and rural recession, the consumer staples sector did not fare well in 2022, with the NSE and BSE consumer indexes plummeting by double digits. Notwithstanding a low base (Covid-19), pent-up demand, and network expansion, the companies reported good YoY growth. These factors account for Ambev S.A.'s ( ABEV ) 9.41% year-over-year revenue growth and 14.17% year-over-year EPS diluted growth.

This year, there is expected to be a pick-up in growth along with margin expansion for consumer staples. I believe the future of ABEV is bright because of the optimistic perspective of the sector and the potential beer developments that we'll see in 2023. Furthermore, the company's balance sheet is robust, featuring very low leverage and high liquidity. This is an excellent investment because the company is undervalued and operates in an up-and-coming industry. Still, investors should be mindful of the risks involved, as detailed in the risk section.

The Outlook

The consumer staples market had a dull 2022, with the NSE and BSE consumer indexes dropping by double due to rising prices and a slowdown in rural areas. Yet, the businesses reported robust year-over-year growth thanks to factors like a low base (Covid-19), pent-up demand, and the expansion of their networks. However, a major international stockbroker, Jefferies, estimates that growth and profit margins for consumer essentials will accelerate in 2023.

The brokerage noted that consumer staples faced substantial headwinds due to a sharp rise in input prices over the past several quarters. While the industry raised product prices, the gross margin dropped sharply, with 150 bps YoY Ebitda margin contraction in 1HFY23. However, Jefferies anticipates that the benefit of reduced crude & palm oil prices would be felt in coming quarters; further price hikes by food firms should counteract agro price inflation and, in turn, push up gross margins. Even with the increase in A&P costs, the Ebitda margin should grow year over year.

As inflationary headwinds abate, the brokerage expects earnings growth for consumer goods to accelerate in 2023. Despite a 20-40% drop from their peak, prices for key commodities like crude oil and palm derivatives have stabilized, but the high inventory costs have slowed the benefits of this. To sum it all together, Jefferies forecasts that consumer staples will see their most significant yearly increase in earnings per share in nearly a decade in FY24, at 18%.

Major Beer Trends for 2023

In 2023, IWSR expects a 1%-2% beer volume growth. Beer has worldwide prospects despite macroeconomic and geopolitical volatility. While consumers put off more expensive purchases due to the cost of living constraint, IWSR projects that beer will continue to show strong growth courtesy of the following major trends .

Recovering on-site

Although beer sales in the on-premise channel are predicted to regain pre-Covid levels by 2025, the weak economic environment may delay the recovery of alcohol sales in the channel. The brewing community, notably smaller craft players, will be affected by this. This year, pressure on disposable incomes may discourage footfall in pubs, bars, and restaurants. Still, some share should transfer back to the off-premise, with sub-channels like e-commerce projected to gain share.

Better results in the top three markets

Due to restrictions, China's beer market underperformed last year. After three years of travel restrictions and quarantine, China reopened its borders in January 2023, which is expected to strengthen the on-premise channel and the beer category. As Covid-related limitations were lifted in Vietnam, Malaysia, Cambodia, and Indonesia last year, some brewers saw a market comeback.

In the US, imports, led by Mexican beer, increased by 4% in 2022. The second-largest beer market may not lose as much beer as expected. Beer decline is slowing, and hard seltzer saturation has reduced RTD growth. In the US, the rise of seltzers hurt beer sales, but in other markets, the impact is smaller.

Beer consumption will increase in Brazil, Mexico, and Latin America in 2023. Brewers have recently invested heavily in this region, and their efforts have paid off. According to IWSR, Brazil and Mexico's third and fourth-largest beer markets will see rising beer volumes in the coming years.

Increasing beer e-commerce

Since the big brewers increasingly see this channel's benefits and view it as the direction of travel long term, beer will create the strongest online growth across the 16 most prominent e-commerce markets over the next few years.

Premiumization grows despite declining disposable incomes

The growth of online beer sales should aid the further premiumization of the beer category, as the online environment is well adapted to promoting premium brands. Premiumization appears to continue and is likely to resume this year despite the inflationary pressures of 2022. Beer's rising status as an "affordable luxury" among consumers will likely keep it buoying the category's value through at least 2023.

No-alcohol niche to grow

Brewer's profit margins will increase as premiumization causes value to surpass volume performance. No-alcohol beers are typically not liable to any duty but often fetch an attractive retail price for operators. Widening availability, improved marketing assistance, innovation, better-tasting product, and rising consumer interaction create a potential for the segment. With the help of new technologies, non-alcoholic beers served on tap will likely become even more common in bars and restaurants nationwide by 2023. More NPD is anticipated from brewers, with alcohol-free brands like Lucky Saint raising over £10 million in Series A funding.

Brewers can expect another year of ups and downs in 2023, but the positives are expected to exceed the negatives, and the coming year is predicted to bring expansion. There would be a dramatic improvement in outcomes if inflationary pressures subsided and hostilities in Ukraine were to halt.

Strong Balance Sheet

ABEV has a robust balance sheet characterized by low leverage and strong liquidity. The company has a debt of $727.65B and an equity of $83.32, translating to a debt-to-equity ratio of less than one, which is very attractive. Further, its liquidity is very pleasing, with a cash and cash equivalent of $15.38B, 21X its current total debt; this shows how secure this company is in its current cash position. Further, to show this liquidity's strength, I can cover the company's total debt and TTM's total operating expenses of 3.2X. Undoubtedly, this is a very secure position for a company to be in, and I believe that it will assist it in weathering any storms that may come into the macroenvironment, especially during increased uncertainties in the macroeconomic climate.

Wallstreet

Regarding debt coverage, the company's decent operating cash flows cover its debt by 2836.8%, and its interest is adequately covered by EBIT(142.8X coverage). This means that the corporation can satisfy its financial commitments quickly and fully.

Valuation

ABEV is undervalued based on relative valuation criteria, providing a low-cost entry point into this promising company. With a PE of 15.63X, ABEV is selling at a discount to the sector average of 21.33X. Based on the comparison of ABEV's FWD PE of 17.23X to the industry's FWD PE of 19.4X, it's clear that investors anticipate a rapid expansion for the firm in the years ahead, lending credence to my thesis that the industry's upbeat outlook is good news for ABEV.

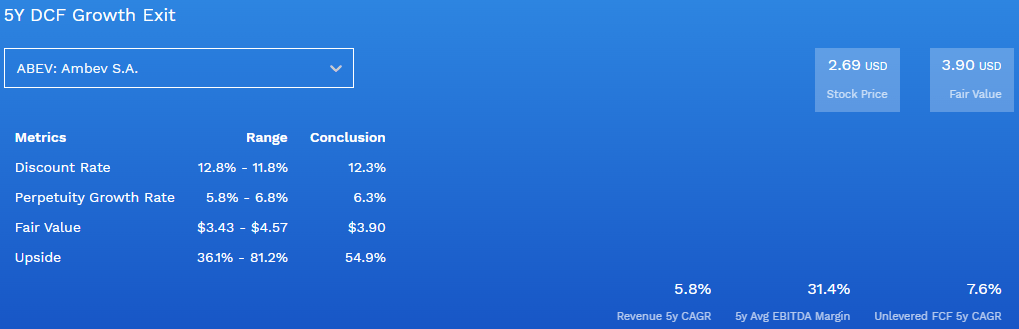

Further, a DCF model by finbox estimates the company's fair value to be $3.90, which is way higher than the current share price of $2.69; this implies that the company has an upside potential of more than 50%, which I believe it can achieve given the strong growth levers in its business environment coupled by its robust balance sheet.

{kind=link}

Risks

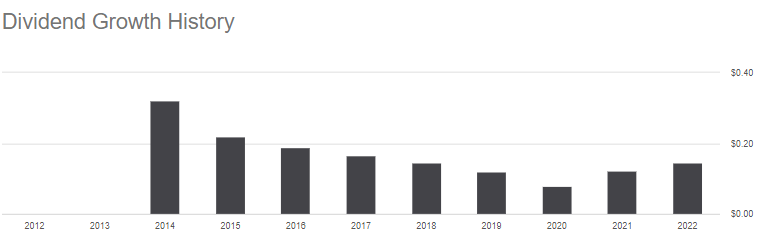

This company has a lot of potential; however, it's not without flaws. Inconsistent dividend payments and falling ROCE are two of its central concerns. To begin with, in the less than ten years that ABEV has been paying dividends, payments have fluctuated a lot.

{kind=link}

For dividend investors, the company's lack of reliability, poor dividend safety record, and dismal dividend growth track record all add up to a dismal dividend score.

Secondly is the company's declining ROCE. If you want to find the next multi-bagger, you should watch for specific trends. Both the rate of return on capital employed (ROCE) and the total quantity of capital used should rise over time in a successful business. This indicates a compounding machine in which a corporation has profitable initiatives to reinvest in. As a result, I wasn't very enthusiastic about the trajectory of Ambev's ROCE.

Looking at the ROCE trend over the past few years at Ambev, things don't look great. Five years ago, capital returns were closer to 25%, but today they're down to 16%.

YCharts

While a rise in revenue and total assets employed may indicate that the company is investing in future growth, the additional capital has resulted in a temporary drop in return on capital employed. Long-term stock performance may benefit significantly from these investments if they are successful.

Even though Ambev's returns have decreased in recent years, it's good to see that sales are increasing and the company is putting money back into its operations. But these trends haven't led to growth returns since the stock has dropped 27% in the last five years.

Conclusion

After a rough 2022, the consumer staples industry is expected to rebound strongly. This comes amid up-and-coming trends in the beer industry, which, combined with the company's solid balance sheet, bodes well for the company's future, as evidenced by the higher FWD PE, which shows the optimism the market has for the company's future growth potential. So, I have a positive outlook on this stock and think growth-focused investors should consider buying it, with the caveat that they should be prepared for the inherent risks.

For further details see:

Ambev: Strong Growth Levers With Massive Upside Potential