AMCX - AMC Networks: Cheap And Misunderstood

2023-10-18 10:18:30 ET

Summary

- AMC Networks has been negatively impacted by ad market weakness, the end of hit shows, an uptick in cord cutting in 2023, and investor pessimism around streaming.

- It trades at low single-digit multiples that are not often seen for a company that is fairly profitable, and could be a takeover target in a downside scenario.

- AMC Networks has attracted ~11M subscribers to its niche streaming platforms, accounting for 20% of total revenues. This gives at least some credibility to its plan to offset cable's decline.

- Management emphasizes the better economics of its niche streaming services, as a result of more targeted and lower content costs.

- Commentators regularly overlook the niche strategy, instead comparing AMCX Networks directly to bigger players.

Investment Thesis

AMC Networks Inc. ( AMCX ) joins the many other media companies that have been hammered by the ad recession and a deterioration in sentiment around linear TV and streaming. The market has evidently also not been receptive to AMC Networks' strategy of pursuing niche audiences in genres like horror, British content, and anime -- the stock is down around 41% in the past year. AMCX regularly gets highlighted as an expected under-performer due to its exposure to linear TV and presumably sub-scale efforts in streaming.

With only around $1-$1.35B in content spend per year, AMCX has attracted around 11M subscribers to its niche streaming platforms in just a few years -- this is for a company with a $0.6B market cap and enterprise value of ~$2.6B. Management stresses that they can pull this off by producing content at a significantly lower cost than the seven-figures-per-episode for marquee content by the bigger players. Many of the themes that I recently wrote about for Warner Bros. Discovery ( WBD ) around the potential for improvements in streaming economics should also arguably apply here.

There are legitimate questions around the long-term future of AMC Networks, as with any stock. But its low single-digit multiples seem to hold almost no regard for any positive qualities including continued profitability, streaming efforts that have apparently already achieved better economics than most peers, and downside protection as an acquisition target.

Background -- Misunderstood Niche Player

With the ad recession and AMC Networks' exposure to linear TV as a backdrop, AMCX reported a y/y decline in revenue of 8% in 2Q2023 , a larger drop than sector peers WBD ( -4% ), PARA ( -2% ), and DIS's Media and Entertainment Distribution segment ( -1% ). To a large extent, though, this isn't entirely surprising. In 2022, popular shows " Better Call Saul " and The Walking Dead (TWD) both ended, which was expected to lead to a sharp decline in viewership . The headwinds for overall performance were also partially offset by 13% growth in streaming revenue.

Risks stemming from litigation by the TWD creator and producers also seem to have been mitigated after parties agreed to confidential arbitration rather than a trial. While this could still involve a significant cost, it presumably removes a worst-case scenario. The stock price pullback along with the abatement of risks around litigation and the end of hit shows have perhaps contributed to short interest coming down significantly from a year ago, to a single digit percent level. It's now creeping up again, somewhat.

The biggest players in the media/streaming sector aim to produce content to cater to a broad range of interests, as well as tentpole hits, to attract the largest possible audience. Their content spend is commensurate with this something-for-everyone approach -- Disney ( DIS ), Warner Bros. Discovery, and Netflix ( NFLX ) are each expected to spend over $17B on content in 2023.

The strategy of targeting niche audiences eschews the goal of pleasing everyone, and instead focuses on catering to super-fans of genres that are unlikely to be completely satisfied with mainstream services. I don't find it hard to believe that a super fan of horror, British content, or anime, etc., would mind forking out a few extra dollars per month for something that catered specifically to that interest. But mainstream consumers/investors might not grasp this (they're likely not fans of these genres, after all), and it has been a stumbling block for the market.

Most commentators on AMCX don't even acknowledge the niche approach, whether this is because of a lack of awareness or a belief that it won't make any difference. In one article, industry commentators described AMCX's situation as "terrifying", and "tragic" . This is for a company with normalized free cash flow of close to ~$200M for 2023 (minus one-time restructuring payments and an accelerated return-of-rights payment), with a market cap of $0.6B. The long-term coexistence of larger-scale versus niche players is also common to other industries.

Subscribers have tapered off from 11.8M in 4Q2022 , to 11M in 2Q2023, which is still up 6% from a year ago. Management's assertion is that this is because of the roll-off of promotions, with a focus on higher-value subscribers. If subscribers instead do not stabilize, it could lead to a negative feedback loop whereby even AMCX's focused content spend starts to suffer. If such a loop did start to take hold, I expect that it could help to catalyze a sale.

Challenging Macro Backdrop

The ad recession that has broadly affected the media sector adds to the difficulty of interpreting AMCX's situation in terms of secular decline of linear TV and the end of hit shows. Management provided the following perspective about ad market weakness on the 2Q2023 earnings call:

We'd love to get your take on the pressures we're seeing in advertising, how much of that do you think is secular versus cyclical?

Kim Kelleher

I'll grab that one. Luke, this is Kim Kelleher. I would say a combination of things are challenging right now. Broadly, our ad supported networks, as Patrick and Kristen referenced, are experiencing the same environment as everyone else in this space. It's a soft scatter market. Marketers are being relatively conservative with their spending. We are seeing some modest improvements in scatter, but overall, we expect, as Patrick said, the landscape to continue to be challenging through the remainder of this year.

That said, in our upfront conversations, we are very pleased, as Kristen mentioned, with the results of our up-fronts and the strength of our pricing around our key products like AMC, BBC America, We TV, and then the huge reception we received to AMC Plus's newly launched ad supported tier coming in October. So, to address your question specifically, I would say we are feeling that the marketplace should improve as we get into 2024.

-Kim Kelleher, Chief Commercial Officer, AMCX 2Q2023 Earnings Call

This is entirely qualitative and doesn't give any concrete indication of an impending turnaround in the ad market. But it gives some colour, and, for what it's worth, articulates an optimistic view. I'd also refer to my recent WBD article for some arguments about why the ad market downturn should eventually come to an end.

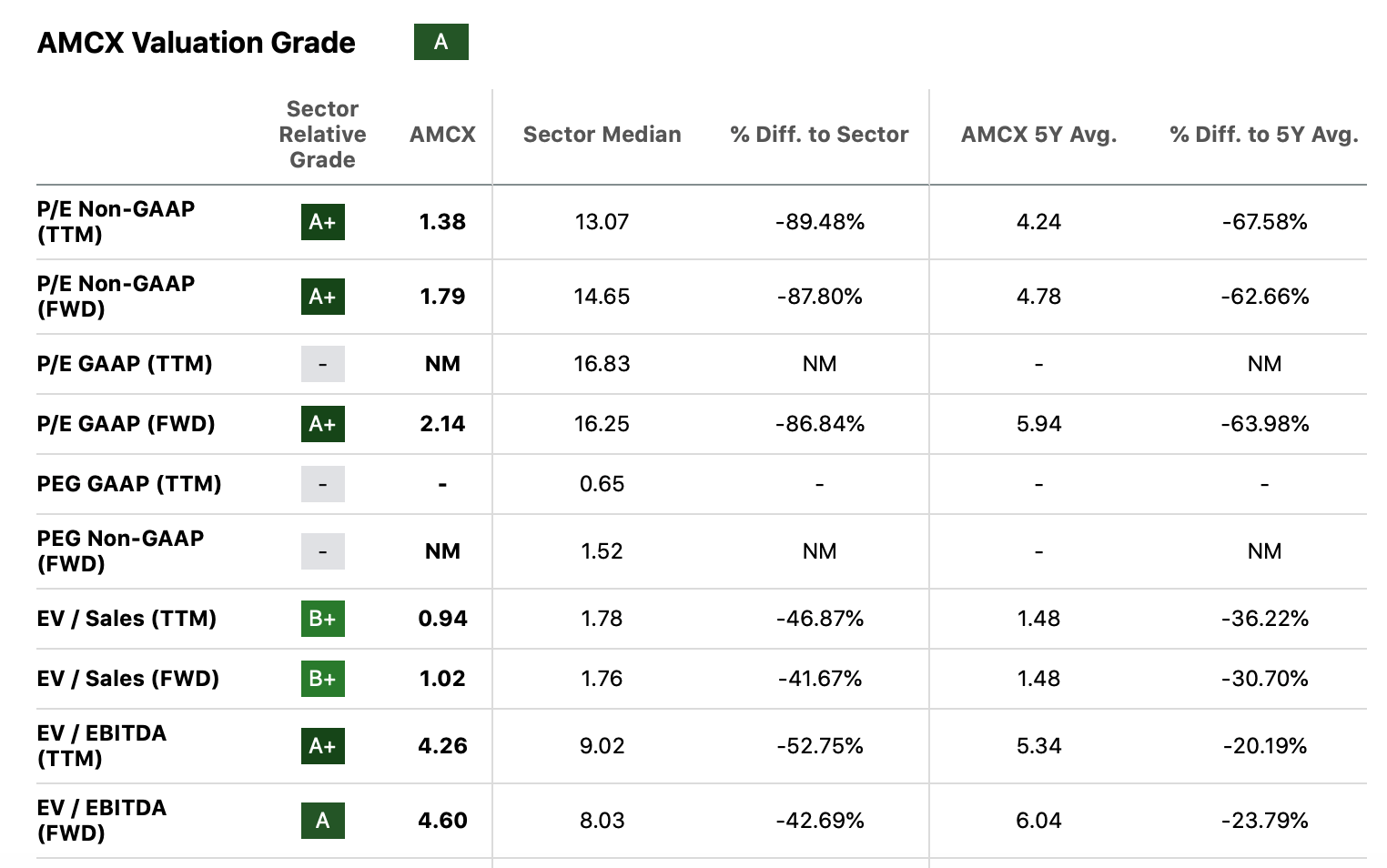

Observations on Valuation

Relative to a stock price that has ranged from ~$10-$14 since June 2023, and a market cap of ~$0.6B, the company has reported the following results:

- Diluted EPS of $3.97 and Adjusted EPS of $4.64 in 1H2023. Annualized, this implies a P/E multiple of ~2x .

- Operating income of $279M and adjusted operating income of $392.5M in 1H2023.

- Diluted EPS of $0.17, adjusted EPS of $9.21, and free cash flow ((FCF)) of $103M for 2022 (full year) .

- Net debt of $1.93B in 2Q2023, with total liquidity of ~$1.3B , including $893M of cash and an undrawn $400M revolving credit facility

- FCF is expected to be in the range of $120M-$140M for 2023, and excluding the impact of one-time cash restructuring payments, the FCF outlook would be in the range of ~$235M to $255M.

- Cash content spend of $1.1B in 2023 versus $1.35B in 2022. Going forward, content spend of ~$1B.

There's bound to be some lumpiness in these results from quarter to quarter. Seeking Alpha's metrics provide further confirmation of the general story on AMCX valuation :

{kind=link}

AMC Networks valuation (Seeking Alpha)

Decline of Linear TV and Other Risks

As a small-cap company in an embattled sector facing secular decline, risks with AMCX abound. Some risk factors that come to mind:

- Streaming represented 20% of AMCX's total revenue in 2Q2023, leaving the company highly exposed to the secular decline in linear TV.

- Cord cutting hit an all-time high in 1Q2023 , with a cable TV subscriber decline of 9.9%.

- As The Walking Dead and Better Call Saul get more dated, it will probably still be a headwind for content licensing revenues, which stood at $492M in 2022 (18% of domestic revenues).

- The potential for carriage disputes with cable distributors.

- Indebtedness that will have to be refinanced at higher rates.

- As a smaller industry player, AMCX has less power to initiate pricing increases.

- The control by the Dolan family mitigates the risk of an opportunistic takeover at a depressed stock price. But it could also reduce the chance of a takeover at a more attractive price down the road.

- On the other hand, they could opportunistically take the company private. But my guess would be that James Dolan prefers the benefits of the company being publicly traded.

- Investor skepticism will likely continue to a large extent, and without share buybacks being a priority, it could remain a value trap.

- Historically elevated short interest and volatility, such that AMCX could easily drop below $10 without any significant change in fundamentals.

- Other risk factors that I may have overlooked.

On the topic of refinancing, in March 2023, AMCX withdrew a cash tender offer for 2024 and 2025 notes because "market conditions were not suitable". But with total liquidity of $1.3B as of 2Q2023, it looks like they would have the 2024 and 2025 notes essentially covered, anyways, if need be.

{kind=link}

AMC Networks credit facility and senior notes (AMC Networks 2023Q2 10-Q)

The long term secular decline of linear TV is presumably the biggest of these headwinds and risks. Total pay TV subscribers stood at around 71.9M in 2Q2023 -- there has been some expectation of a floor of around 50M where declines would stabilize, but with the recent uptick in cord cutting, maybe this can't be counted on.

Historically, cord cutting has been partially offset by affiliate fee increases. These help to cover sports rights across a smaller base of subscribers. The carriage dispute between Charter and Disney in September 2023 highlighted the risk of an inflection point whereby cable is dropped by even more consumers, sending it into a faster death spiral.

In a world where cable TV disappeared entirely, it seems reasonable to expect that AMC Networks could, say, at least double its streaming revenues (through a combination of increased subscriber counts, prices, and advertising). This would put its revenue at around 40%+ of where it is currently. This wouldn't happen overnight. A silver lining to higher interest rates is that it may help to motivate companies like AMCX to prioritize debt pay-down. With free cash flow roughly in the $100M-$200M range, it should be able to make progress in this regard.

There has been much speculation about whether James Dolan will sell AMC Networks. Since the company is still rather profitable, there isn't any near term pressure to do so -- and management most likely thinks that they can still make the business work, longer-term. If AMCX financial performance *did* deteriorate enough, though, then I think the probability of a sale would increase greatly.

Bigger players will always need content, and at this level of market cap an acquisition of AMC Networks would look like a simple "content arbitrage". AMC Networks' content spend of around $1B+ per year greatly exceeds its current $0.6B market cap (and also compares favourably to the ~$2.6B enterprise value). An acquirer of AMCX would get significantly more content than they could hope to produce for that same amount of money. Even though many AMCX shows are not widely known, Mad Men, Breaking Bad, and The Walking Dead are all examples of shows, initially aired on AMC Networks, that did well once they were exposed to a larger audience.

I'd see a sale of AMCX more as downside protection rather than something that would materialize in the foreseeable future.

Conclusion

Total revenue for AMC Networks saw a notable drop of ~8% in 2Q2023. But this should be put in the context of the weak ad market, and the highly anticipated end of a couple of major shows (i.e., a specific one-time event), rather than just the secular decline of linear TV. Nevertheless, the uptick in cord cutting in 2023 warrants attention.

Relative to 2021, the macroeconomic backdrop has changed considerably. Higher interest rates may have come at a good time because they should help to motivate faster debt pay-down, and AMCX's continued profitability still allows it to do so. Streaming now accounts for 20% of AMCX revenues, and time will tell if this can mitigate the decline of cable, even if ultimately AMCX ends up as a smaller company or being acquired.

I look forward to your comments on AMCX.

For further details see:

AMC Networks: Cheap And Misunderstood