AMCR - Amcor: Hard To Ignore The 5% Dividend Yield

2023-12-12 07:15:56 ET

Summary

- Amcor is a leading provider of packaging solutions, including flexible and rigid packaging for stable industries such as food, beverage or healthcare.

- This sector has proven to be more resilient than the market average in situations of economic stress, such as the great crisis of 2008.

- The company has been divesting from Russia. This, together with the economic slowdown, has caused margins to temporarily worsen and the price to fall.

- It is currently trading around the sector average but offers an attractive 5% dividend that is difficult to ignore.

Investment Thesis

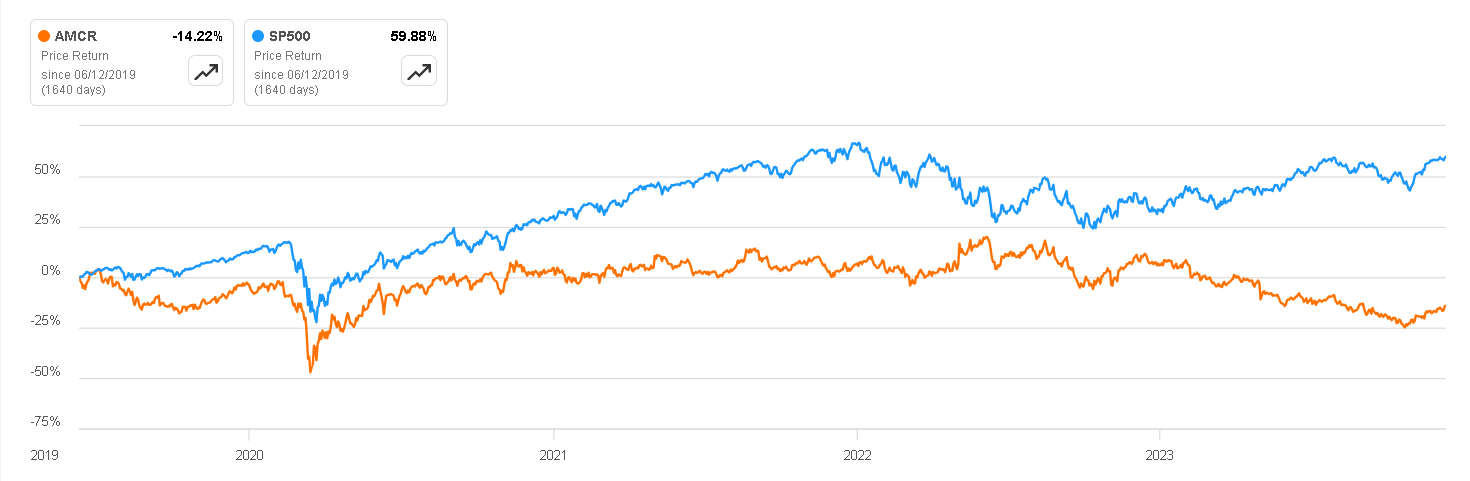

Since its IPO in 2019, Amcor (AMCR) a leading company in the packaging industry has faced significant challenges, resulting in underperformance compared to the S&P500 and other industry competitors. Factors contributing to this performance include the impact of the Covid-19 crisis, inflationary pressures, and, most recently, the sale of divisions in Russia, leading to a decline in margins.

In this article, we will conduct a thorough analysis of the company's business model, compare it with its competitors, and delve into the temporary challenges it is currently navigating. The objective is to understand why the company could represent an attractive investment opportunity if it successfully recovers from its current situation and manages to return to growth and improve its margins to levels of previous years. And in the meantime, we could be receiving a healthy dividend yield of 5% with a payout ratio of 75%.

Price Return vs S&P500 (Seeking Alpha)

{kind=link}

Business Overview

Amcor is a packaging company headquartered in Switzerland. Amcor is a leading provider of packaging solutions, including flexible and rigid packaging for various industries such as food and beverage, healthcare, personal care, and more. The company operates globally and has a significant presence in North America, Europe, Asia, and other regions.

As is usually the case in this type of business, the company's income could be considered highly stable and resilient to adverse economic environments because its clients range from food producers such as Mondelez to beverage producers such as Coca-Cola, or health products like Johnson & Johnson. This means that regardless of the macroeconomic situation, Amcor's customers will continue to place their orders because, in turn, its customers also consume its products steadily.

This makes this type of business quite solid, with the possibility of growing for decades and with a low risk of disruption , since it is not so simple for a competitor to appear out of nowhere and reach the scale of Amcor. For example, achieving working relationships with the same clients who already trust Amcor and have been working together for years is a complex task.

{kind=link}

Performance During Crisis

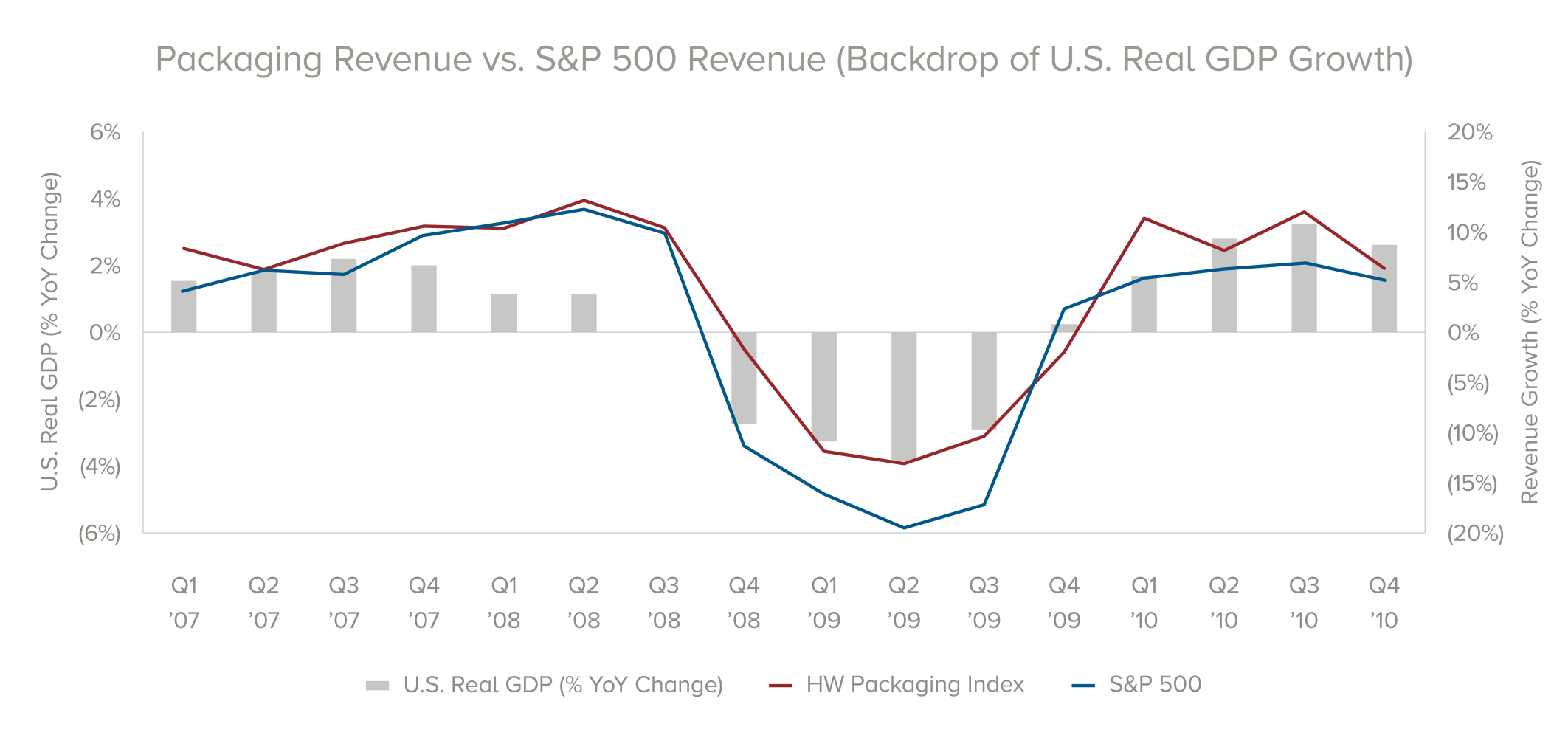

An excellent demonstration of the defensive nature of these businesses is their performance during the Great Recession of 2008-2009. In a study conducted by the global investment bank Harris Williams , the revenue performance and EBITDA margins of 18 companies in the packaging sector were analyzed. The results showed that the overall revenue decline for the packaging industry was slight compared to the decline in S&P 500 revenue.

Both the Packaging sector and the S&P 500 experienced revenue declines for four consecutive quarters. However, packaging revenues only declined by 9%, whereas S&P 500 revenues declined by about 16%. Furthermore, when the markets recovered, packaging revenue growth rates returned to pre-recession levels within three quarters after bottoming out, while it took the S&P 500 seven quarters to do the same. Not only did it decrease less, but it also recovered its usual growth faster.

{kind=link}

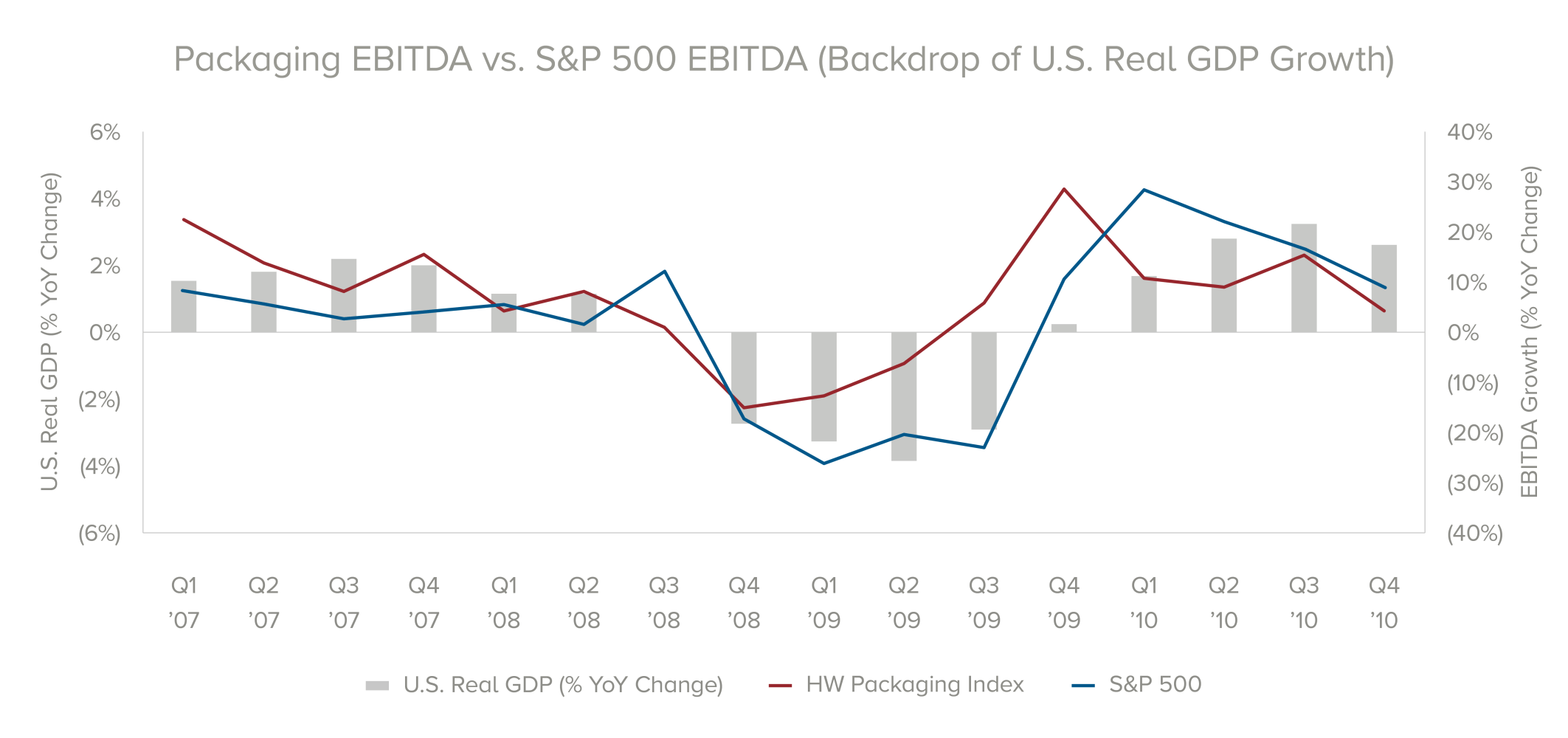

Similarly, when comparing EBITDA, the packaging industry experienced a smaller decline, dropping only 14% compared to the 22% drop for the S&P 500. Once again, the Packaging companies bounced back at a more rapid pace compared to the S&P 500.

{kind=link}

Revenue Distribution

The company's revenue is divided into two main segments: Flexible and Rigid Packaging.

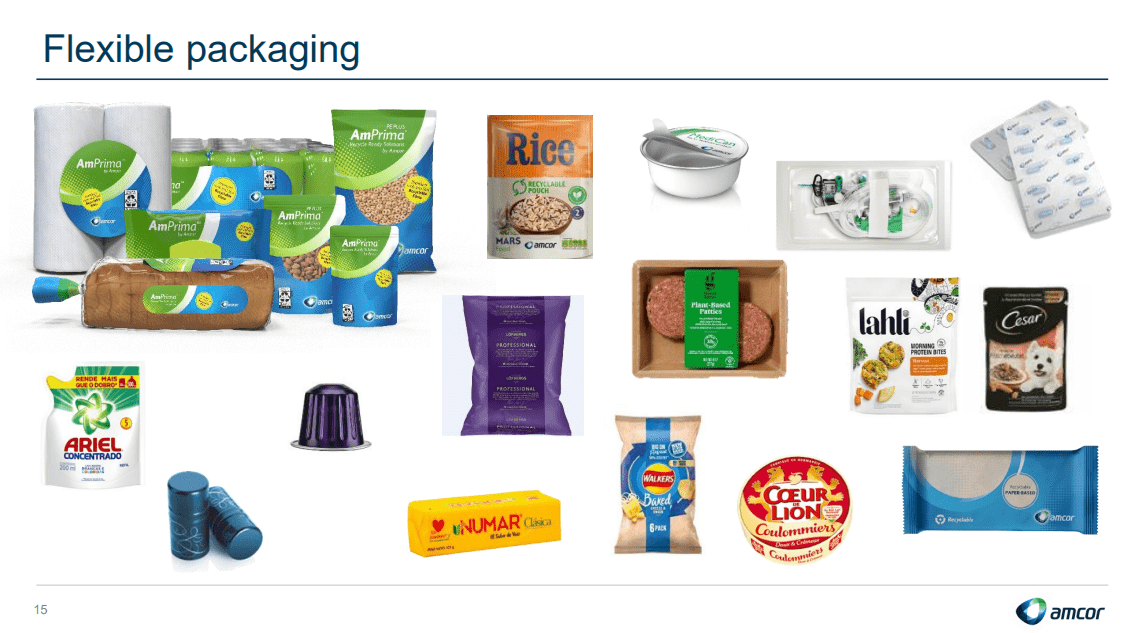

Currently, the Flexible Packaging segment represents 75% of revenue, compared to 68% six years ago. Flexible packaging refers to a type of packaging made from materials that are pliable and can be easily shaped or deformed, such as plastic films, aluminum foil, or even paper.

This segment of the company has grown at a rate of 10% annually since 2017; however, a significant part of this growth is attributed to the acquisition of Bemis Company in 2020. Normalized growth would be around 4%, consistent with the expected growth for this sector .

{kind=link}

The flexible packaging sector is anticipated to continue growing at around 4 or 5% by 2030, with the Asia Pacific region representing almost half of this growth. Flexible packaging is lightweight, easy to handle, and often comes with features like resealable closures, spouts, and easy-open mechanisms. This convenience aligns with evolving consumer preferences for on-the-go and convenient packaging solutions. Additionally, it is often more cost-effective in terms of production, transportation, and storage, making it a foundation for the development of emerging economies.

Currently, 25% of Amcor's revenue comes from emerging markets, so mid-single-digit growth can be expected in the coming years. Furthermore, the segment's EBIT margins have proven more resilient than those of the Rigid Packaging segment, as we will see below.

{kind=link}

Rigid Packaging refers to packaging materials that are sturdy, inflexible, and maintain their shape even when empty. These materials are typically made of substances such as glass, metal, or rigid plastics like PET (polyethylene terephthalate) and HDPE (high-density polyethylene), commonly used for bottles, jars, and containers.

This segment accounts for the remaining 24% of 2023 revenue and has experienced an annual growth rate of 3.5% since 2017, with slightly lower EBIT margins compared to Flexible Packaging.

{kind=link}

On the other hand, this segment is substantial, and greater growth between 5 and 6% is anticipated in the coming years. This expectation is grounded in the fact that rigid packaging is essential for products that are unlikely to find substitutes , especially in industries like high-end beverages, perfumes, beauty and health products (e.g., those requiring aerosol cans). Rigid packaging also offers excellent protection against external factors such as light, moisture, and air.

As innovation continues to make rigid packaging more environmentally friendly, growth is likely to persist, given the challenging nature of finding viable substitutes for this type of material.

Amcor Investor Presentation

Key Ratios

Overall, the company's revenue has grown at a rate of 4.4% in the last decade, maintaining EBITDA margins of between 14 and 15% and Free Cash Flow margins of between 6 and 7%.

{kind=link}

In the last five years, the company has sourced 64% of its capital from debt and 35% from cash generated by operations. This capital has primarily been utilized to retire issued debt and to reward shareholders through buybacks and dividends. Notably, the company currently boasts an appealing dividend yield of 5.2%. In FY2023 alone, it distributed $717 million in dividends against a net income of $968 million, resulting in a sustainable payout ratio of 74%, assuming the capital allocation policy remains unchanged.

{kind=link}

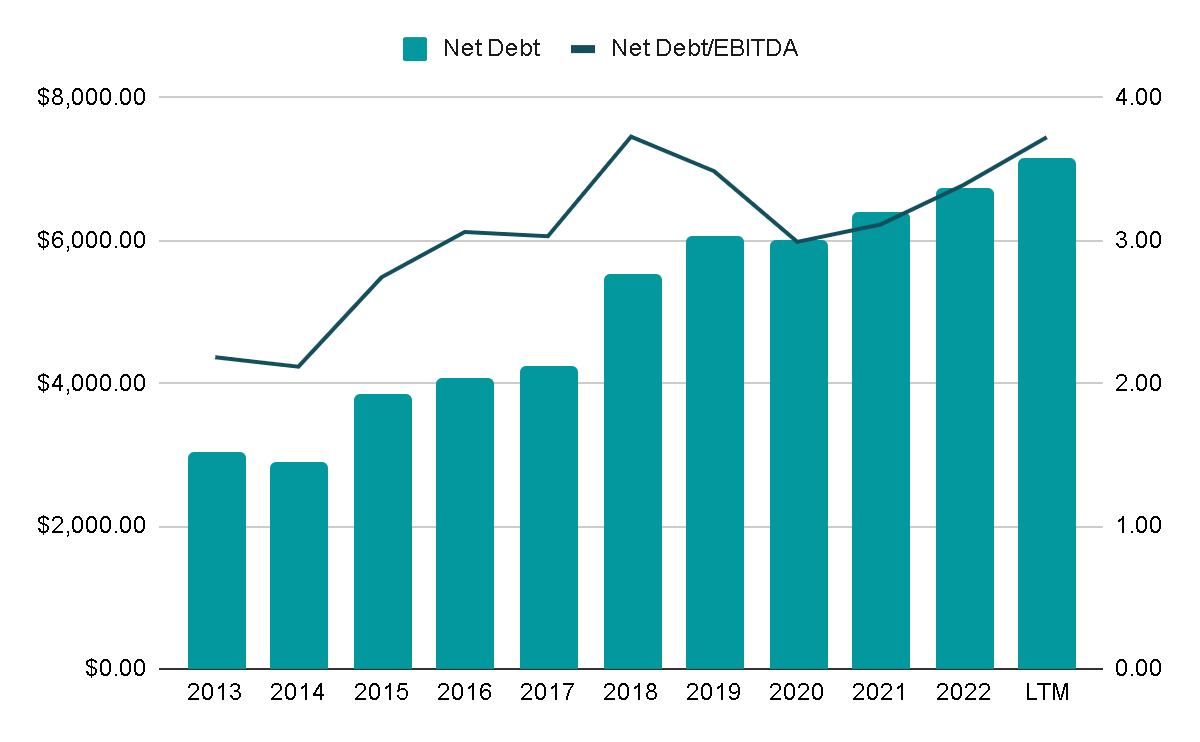

However, there is a potential concern regarding the sustainability of the dividend. The company has heavily relied on debt financing, which was advantageous during periods of low interest rates but could pose challenges in the current environment. And considering that net debt represents 3.7x the last twelve months EBITDA, this is an issue that undoubtedly requires further analysis .

{kind=link}

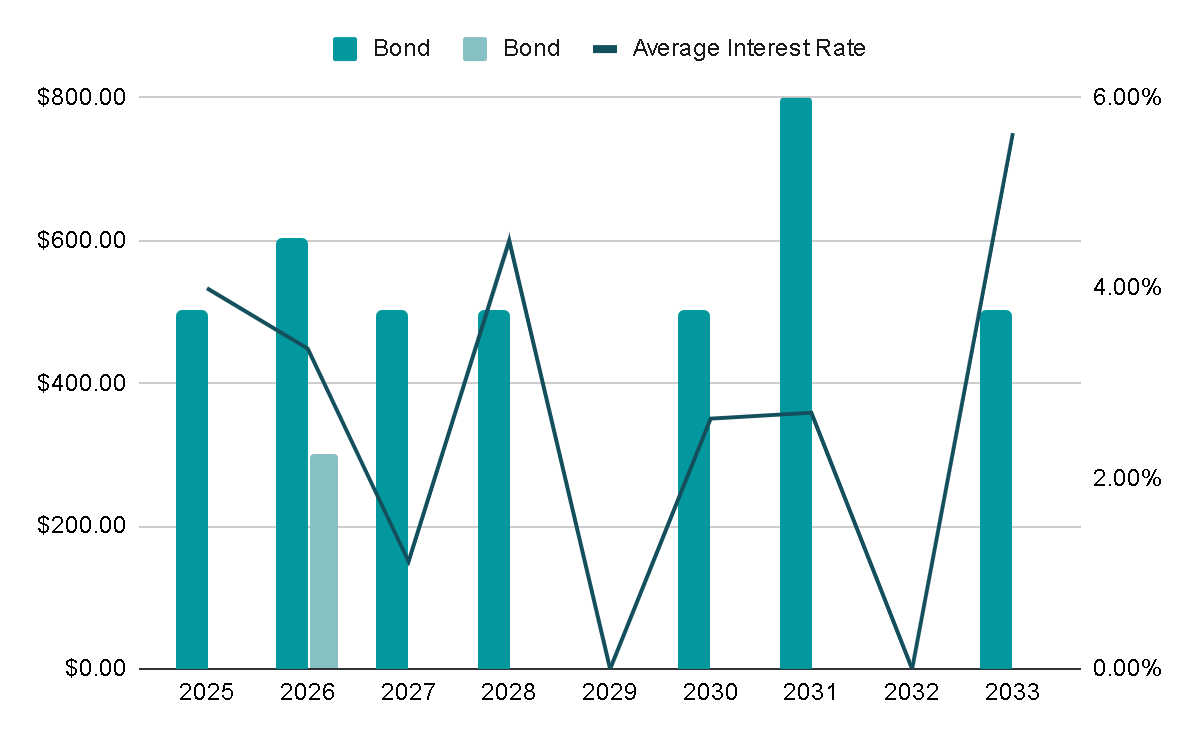

Upon closer examination, the company holds $4.2 billion in bonds with maturity dates spanning from 2025 to 2033. The average interest rate on these bonds is 3.4%. While the debt is sizable, the predictability of the business's profits provides a high level of certainty regarding its ability to service this debt. Moreover, with the Federal Reserve adopting a more dovish stance, it is plausible that by 2025, when the next bond matures, the company may not face challenges negotiating debt at high rates.

In summary, while the debt warrants careful monitoring and caution, the company appears to have the situation under control. As of now, under current conditions, there don't seem to be any imminent risks that would lead to a serious problem in the short term.

{kind=link}

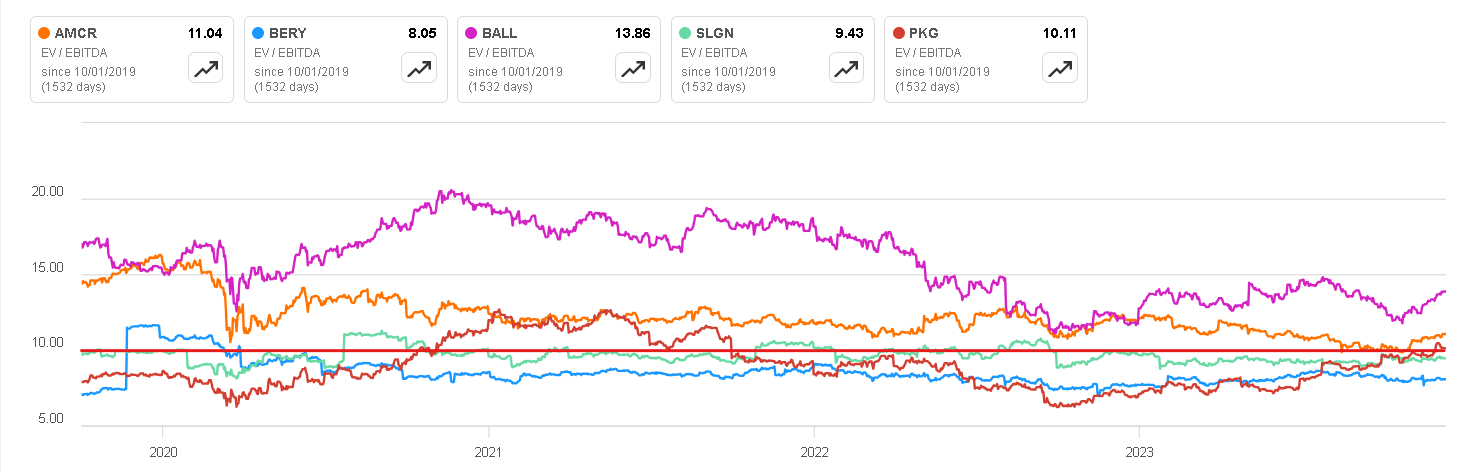

To contextualize these numbers, let's compare them with various companies in the packaging sector. While the margins and growth of each company depend on factors such as product mix and scale, they serve as a useful benchmark .

Over the last five years, the sector, on average, achieved a revenue growth of 9%, whereas Amcor outperformed with an 11% growth rate. It's worth noting that although Amcor's debt may seem high initially, it is in line with common debt levels in the sector. In fact, Amcor maintains a lower leverage ratio compared to its peers and trades at multiples that are in line, if not lower.

However, not all aspects are positive. Despite being listed at a more attractive valuation than some competitors, Amcor's Return on Invested Capital ((ROIC)) is lower than the sector average , and its EBITDA margin is the lowest among its peers. This suggests potential issues with cost control and possibly suboptimal investments, so it seems that the company is justifying this lower valuation due to lower quality in the business, which we will take into account for the valuation later.

{kind=link}

Valuation

Upon reviewing the results of the first quarter of fiscal year 2024, it appears that this year might pose challenges for the company. However, management has assured that these difficulties are temporary , attributing them to the sale of plants in Russia and the ongoing disinvestment in that region. According to statements made in the recent conference call , management anticipates normalization and the realization of cost optimization benefits in the second half of the fiscal year.

The other factors impacting leverage are really on -- through temporary impacts. Firstly, we're lapping now three quarters of devested Russia earnings and that's being reflected in the last 12-months EBITDA and that's ahead of us getting the benefit of the restructuring, which is going to start to come through in H2.

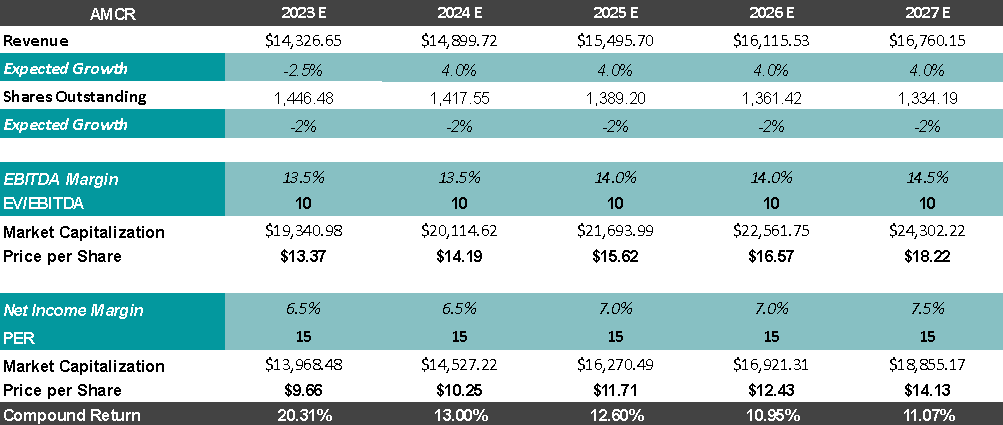

Consequently, I expect a temporary dip in revenue and anticipate margins to remain at current levels for this year. However, in the following years, I foresee the company growing at the pace of its operating market, with margins gradually improving. Additionally, I anticipate the company to continue its share repurchase program at a rate of 2%, consistent with its activity over the past five years.

For the current fiscal year, I estimate the company to generate around $930 million in net profits, equivalent to $0.64 earnings per share. Looking five years ahead, my expectation is for earnings per share to range between $0.9 and $1. Applying a multiple of 10x EBITDA and 15x earnings, based on market trends for similar companies in the last four years, I project a potential share price between $14 and $18. This implies a compound annualized return of ?11% if purchased at the current price, complemented by an attractive 5% dividend yield.

Author's Representation EV/EBITDA Ratio (Seeking Alpha)

{kind=link}

{kind=link}

Final Thoughts

Given the nature of businesses in this sector, it's inherently challenging for a company to perform poorly. Many have established themselves over decades, boasting low disruption risk due to the difficulty of substituting their products. Furthermore, the scale of operations, particularly for Amcor, the largest among its previously compared competitors, magnifies the benefits. The scale allows for securing high-profile clients, leveraging a well-established reputation, and efficiently handling substantial order volumes. Undoubtedly, Amcor stands out as one of the sector's premier players .

{kind=link}

Under ordinary circumstances, a company with these characteristics would likely command a higher valuation. However, the current market conditions might be presenting a compelling opportunity due to temporary setbacks inflicted by the company itself. Once these negative effects pass, the expectation is that the company will recover margins, potentially leading to a significant re-rating in the market. This, coupled with a dividend yield exceeding 5%, could make the current price an attractive entry point.

While it's crucial not to underestimate the risks associated with debt and the potential challenges in executing cost optimization plans, the current valuation suggests that the company may be a ' buy. ' A conservative valuation indicates the potential for double-digit returns in a leading sector player.

For further details see:

Amcor: Hard To Ignore The 5% Dividend Yield