AMCR - Amcor's Headwinds From Inflation And Rising Interest Expenses Are Temporary

2023-07-25 07:00:00 ET

Summary

- Amcor plc, a global consumer and healthcare packaging company, is facing pressure from inflationary cost pressures and rising interest expenses, impacting its stock price.

- The company plans to increase capital investments to expand into higher growth, higher margin product lines, and expects a boost in sales volume as inflation cools.

- Despite current challenges, Amcor's ~4.9% dividend yield and potential for growth in healthcare product packaging make it an attractive option for investors.

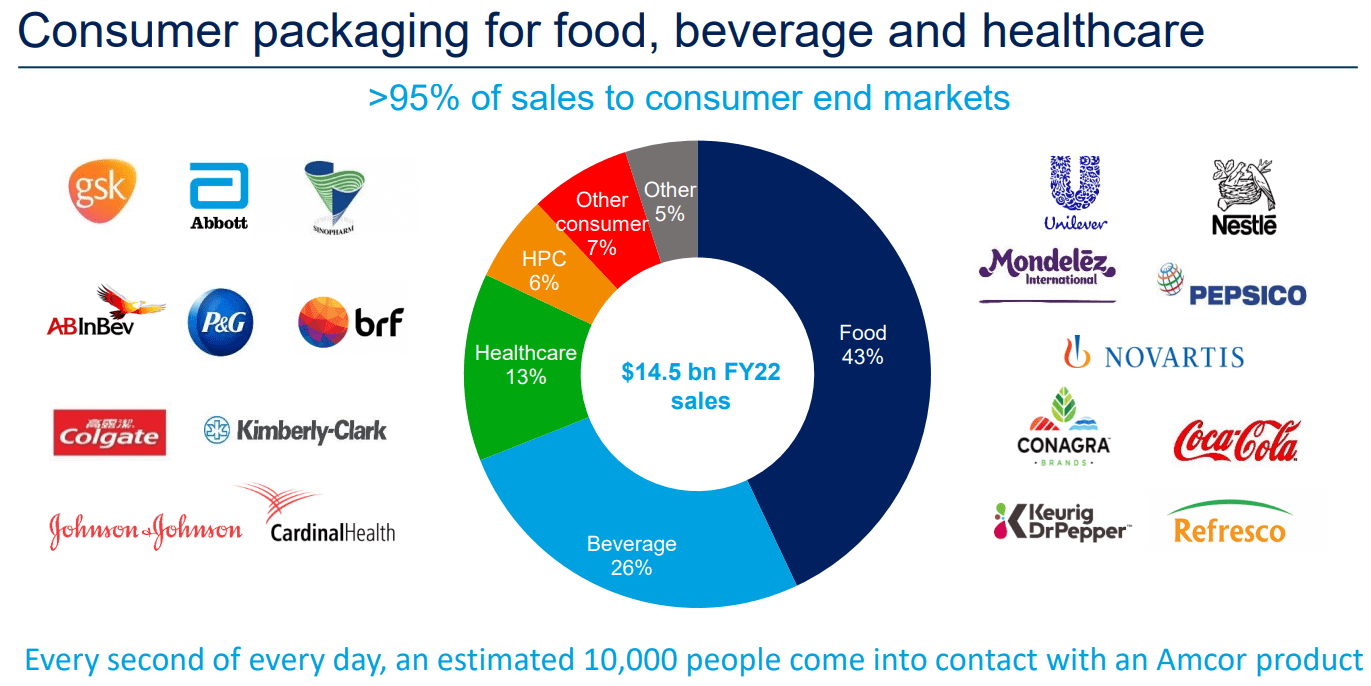

Amcor plc ( AMCR ) is a global consumer and healthcare packaging giant with its product packaging on store shelves around the world, from the US to Europe to various emerging markets.

The company sells two primary types of products: rigid and flexible. Rigid packaging typically takes the form of beverage bottles, plastic or glass jars, and some small boxes. Flexible packaging is anything that crumples or moves, like plastic bags, coffee pods, and collapsible cardboard cup holders.

I've owned AMCR in the past and am considering buying back into it amid its current stock price dip. It pays an attractive ~4.9% dividend yield and (if you count the record of Bemis, with which AMCR merged in 2019) has a 39-year dividend growth streak.

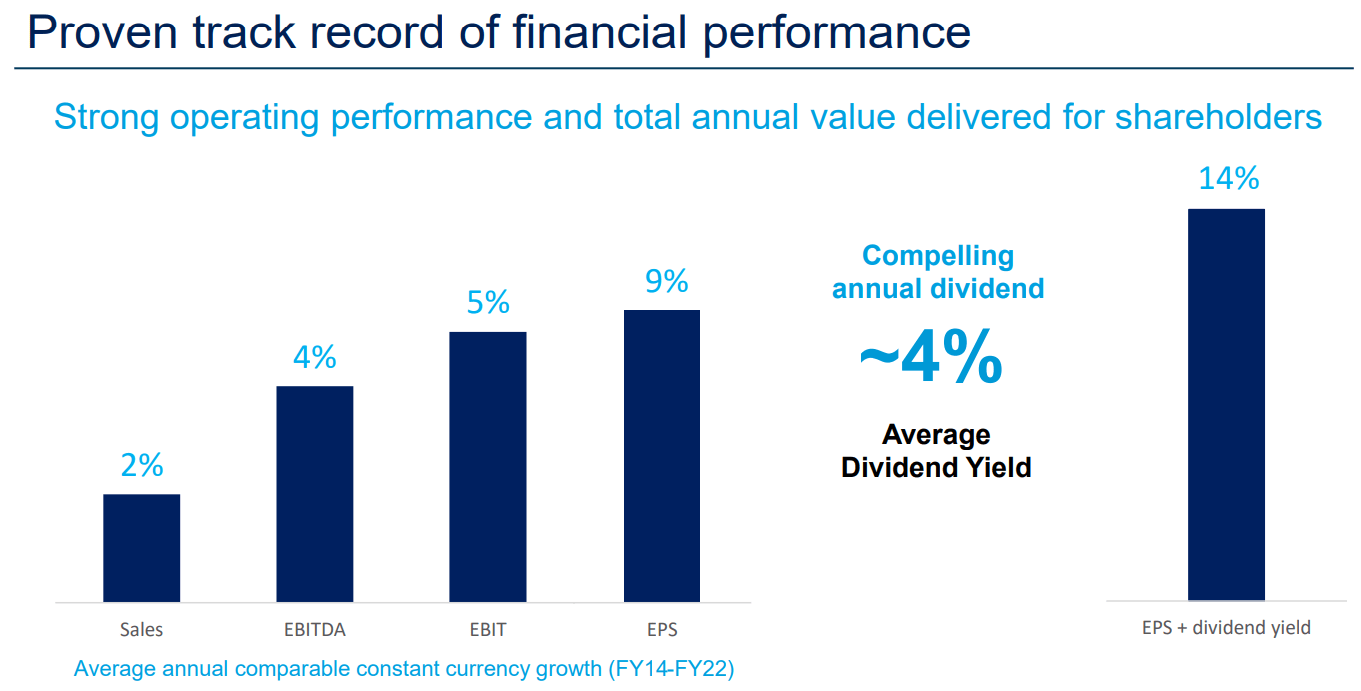

Management asserts that AMCR's EPS growth plus its dividend yield should provide investors with total returns in the 10-15% range, and from fiscal 2014 through 2022, AMCR did just that by delivering ~9% average annual EPS growth.

Lately, however, AMCR has been under pressure from inflationary cost pressures and rising interest expenses. The company is also taking a relatively small hit right now from the sale of three manufacturing plants in Russia that was not planned prior to the war in Ukraine. Moreover, as consumer product prices have risen, the unit volume of sales has decreased. Lower unit sales volume translates into less demand for product packaging from producers like AMCR.

However, the company plans to increase capital investments to 4-5% of sales (both from R&D and acquisitions) in order to expand into higher growth, higher margin product lines.

My thesis is that as inflation continues to cool (both on the raw materials and consumer goods side), unit sales volume of consumer products should increase, raising both AMCR's topline revenue and its earnings. Plus, healthcare product packaging is an exciting area of growth with lots of potential.

Overview of Amcor Today

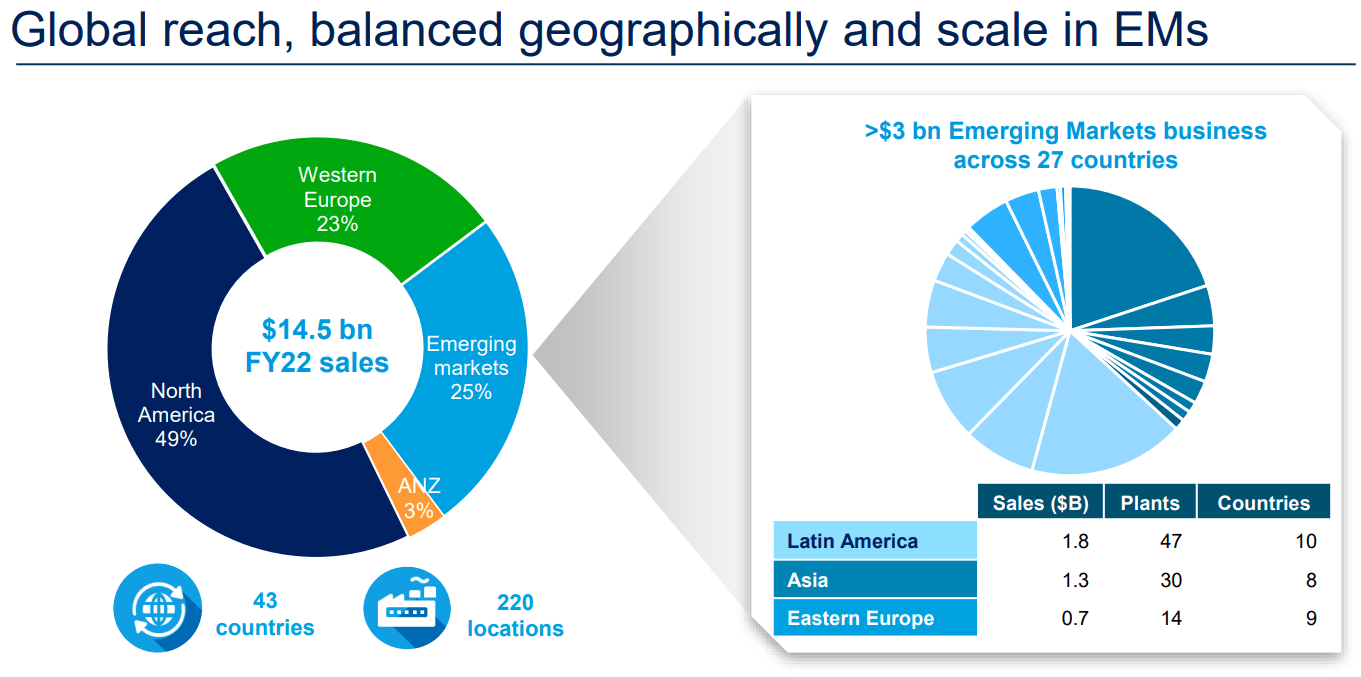

AMCR's origin story goes back over 150 years to Australia, but through multiple mergers & acquisitions (most notably the merger of Amcor and Bemis in 2019) and changes in domicile, the company is now headquartered in Zurich, Switzerland and boasts a global footprint.

The company's consumer packaging is used by the vast majority of major consumer staples names. In fact, it would be difficult to fill a grocery cart at your local supermarket without picking up at least a handful of packages produced by AMCR.

{kind=link}

After the acquisition of/merger with US-based Bemis, roughly half of AMCR's sales now derive from North America, while a quarter comes from various emerging markets and slightly under that comes from Europe.

{kind=link}

Though AMCR originated in Australia, a mere 3% of sales came Australia and New Zealand.

While population growth is stagnant across most of the developed world, younger populations with more middle class growth in certain EMs gives AMCR opportunities to tap into more organic growth.

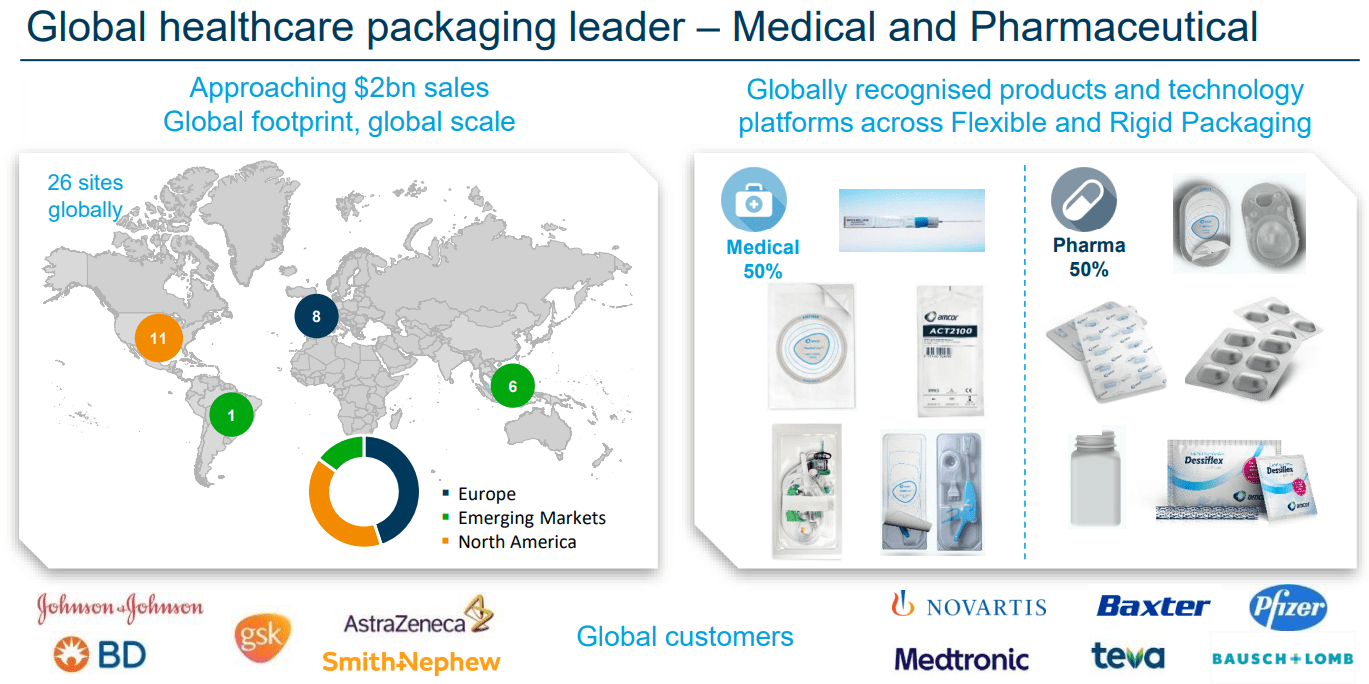

But perhaps the most exciting growth area, in my opinion, is healthcare product packaging.

{kind=link}

Given aging demographics across most of the world, demand for healthcare products should increase for decades. Having a strong positioning in these types of products bodes well for AMCR's future organic growth.

From fiscal 2014 to fiscal 2022, while AMCR's sales growth has averaged only 2%, operational efficiency and buybacks have translated that relatively meager revenue growth into 9% average annual earnings per share growth.

{kind=link}

That trend, however, relied on continuous margin expansion. EBITDA margins kept rising right through COVID-19 and into 2021, but in 2022, inflationary cost pressures from raw materials prices suddenly took their toll on margins.

While this chart of AMCR's EBITDA margin may not be 100% accurate, it is directionally accurate. The trend of margin expansion was halted in 2022, and management has since taken steps to rebuild that margin back toward its previous level.

Very helpful in this process has been the stabilization of cost of goods sold, which is by far AMCR's largest expense.

In 2022, COGS was about $12 billion, compared to $14.5 billion in total sales. Raw materials costs tend to come quickly, while the costs of AMCR's products comes slower, creating a lag between input prices and product prices that results in a temporary dip in margins.

It may take some time for AMCR's margins to be rebuilt, though, because consumer product unit volume has decreased in the face of sticker price hikes. As prices go up, people consume less.

But I do not believe this situation to be permanent.

Firstly, notice above that COGS has already stabilized for AMCR. Raw materials costs are not soaring higher anymore. As the company's product price increases take effect, then, its margins should likewise gradually increase back toward their previous level.

Secondly, as consumer packaged goods inflation cools down back to normal levels, wherein shoppers hardly even notice the gradual rise in prices, and as wage growth rises faster than inflation for a while, unit volume of packaged goods should begin to increase as well.

As previously stated, growth in unit volume of CPGs benefits AMCR, because it means higher demand for its packaging.

Amcor Looks Like A Solid Value

With that thesis in mind, AMCR looks undervalued and attractive based on a number of valuation metrics.

As a dividend growth investor, I care a lot about cash flow, so let's start with price to operating cash flow, or "cash from operations."

Since this chart looks backwards 12 months, and AMCR in its current (post-Bemis merger) form only began to exist in mid-2019, it begins in mid-2020. Right now, AMCR is near its cheapest level in the last three years as measured against operating cash flow.

We find the same when looking at AMCR's enterprise value to EBITDA ratio, which comes in at a low 10.3x.

What about earnings? Here, again, we find AMCR looking quite cheap, with nearly its lowest P/E ratio since the Bemis merger.

The average estimate of forward EPS I have seen for AMCR is $0.734, which would put the company's current forward P/E ratio at 13.75x.

Compare that to some of AMCR's peers in the packaging sector:

- Packaging Corporation of America ( PKG ): 17.3x

- International Paper Company ( IP ): 15.8x

- WestRock Company ( WRK ): 13.0x

- Sonoco Products Co. ( SON ): 10.3x

To be fair, AMCR's closest peer in this list is Sonoco, which also produces consumer goods packaging. Sonoco has a slightly longer dividend growth track record (40 years), a lower dividend payout ratio (~36% compared to AMCR's ~66%), somewhat lower leverage, and is cheaper on both a P/E basis and EV to EBITDA -- about 7.7x, compared to AMCR's 10.3x. So, for those interested in an even more conservative option, SON is another company to consider.

However, these companies have very similar forward earnings estimates, making AMCR with its higher dividend yield (~4.9% compared to SON's 3.5%) the more attractive pick for dividend investors, in my estimation.

Plus, while SON has more exposure on the industrial packaging side, AMCR has more exposure on the healthcare packaging side. I prefer AMCR's healthcare exposure to SON's industrial exposure.

Bottom Line

I will readily admit that I do not know how long it will take for AMCR to right the ship, rebuild its margins, and see normal revenue growth again. It may take longer than I currently assume.

But I am fairly confident in my thesis that as inflation cools, two things will happen:

- Consumer packaged goods unit volume will turn positive, giving a boost to AMCR's sales

- AMCR's prices will increase faster than raw materials costs

These headwinds are temporary. Meanwhile, the long-term tailwinds from exposure to healthcare products, R&D spending, and other faster-growing product categories are indefinite.

Meanwhile, AMCR's dividend yield of ~4.9% is attractive, given the company's defensive qualities and likelihood to grow the dividend at a mid-single-digit pace over the long run.

I am now looking to buy back into AMCR stock as soon as possible.

For further details see:

Amcor's Headwinds From Inflation And Rising Interest Expenses Are Temporary