BA - Amedeo Air Four Plus Limited: Airplane Lessor With A 15% Yield

2023-05-30 00:34:47 ET

Summary

- Amedeo is a self-managed fund offering quarterly distributions from leasing a small portfolio of wide body airplanes.

- Amedeo has a 15% yield.

- While possibly attractive, there are some risks that should be kept in mind when assessing Amedeo for investment.

Generally, when looking at investments opportunities, investors but also many analysts stick to the bigger names. Consequently, that leaves big names too much in the spotlight and potentially overvalued while smaller names remain underexposed and undervalued. It’s something that I have seen quite often in the aerospace supply chain. However, one company for which this theory does not hold is Amedeo ( OTCPK:AMDOF ).

A Low Price, Even Lower Volume

One reason why I am not quite charmed by Amedeo is that it is a stock that trades OTC in the Pink Tier or better said there is a lack of trading. The stock trades below $1 which increases the probability of volatility and ability to sell and buy at stable prices. This is even more amplified by the low volume. There seems to be no continuous market making with the last trade price quoted being from the 20 th of March. Apart from that OTC stocks often have different reporting standards which can make following the fundamental performance of the company harder. All, with all I would say if you really do want to invest in Amedeo consider doing it via the ordinary shares registered in London.

Amedeo Is A Higher Risk Name

Besides the risks of the low price and the low volume, the business itself is one that I consider rather risky. Amedeo specializes in acquiring, leasing and selling aircraft. The fund seeks to use the net proceeds of placings and/or other equity capital raisings, together with debt facilities (or instruments), to acquire aircraft which will be leased to one or more major airlines.

That itself not what I see as a risk as Amedeo is basically in the business of acquiring airplanes and leasing them to airlines and as you know I have buy ratings on AerCap ( AER ) and Air Lease Corporation ( AL ). What I am not a big fan of is Amedeo’s addiction with the Airbus A380 ( OTCPK:EADSF ).

{kind=link}

Years ago, when Amedeo was still known as Doric Lease Corp., the company ordered 20 Airbus A380s without any lease customers. Subsequently, the company tried to pitch the business case for the Airbus A380 to anyone who wanted to hear but not so much with airlines as airlines already had seen that the Airbus A380 is a great airplane when you are able to fill it but if you don’t, then from economics perspective the A380 is an awful plane that cannot efficiently be used on point-to-point networks and does not allow for incremental capacity additions. As the Airbus A380 production program was nearing its end and Amedeo had found no parties interested to lease the airplanes, Airbus and Amedeo agreed to cancel the order. At the time the company already owned 18 Airbus A380s via sale-and-leaseback arrangements, but with demand for the superjumbo being extremely low that exposure with the eye on value retention has been a risk. Even more so given that plans from Doric Aviation, a different company that also owns A380s, to offer A380s for ACMI operations has been a failure given the A380 virtually no chances on a life with a second operator.

Currently, the company still owns six Airbus A380s on lease to Emirates. Furthermore, it owns two Boeing 777-300ERs ( BA ) on lease to Emirates as well and four Airbus A350-900s on lease to Thai Airways. That already highlight another two risks. The first one is the lack of diversification of lessees and a subitem of that is the exposure to Thai Airways. Thai Airways filed for bankruptcy during the pandemic and defaulted on lease payment. The lease agreement was restructured through January 2023 as power by the hour contracts. By now, the payments are occurring at industry standard terms but it perfectly demonstrates the risk for Amedeo having a non-diversified lessee pool.

Secondly, the lack of scale in combination with the exposure to the Airbus A380 could make financing at attractive rates very challenging especially in a higher interest rate environment as we see it today. Subsequently, this means that expanding the pool of airplanes can be a challenging holding Amedeo in a gridlock.

The 15% Dividend Yield Is There For A Reason

One thing investors might like is the fact that Amedeo pays a dividend. As a self-managed fund it is focused on returning value to shareholders through dividends and compulsory redemptions. It is structured much like a portfolio, which can be filled with airplanes and from which the proceeds are shared with shareholders. The distribution policy aims to return 8.25 pence per ordinary share in dividends and separately, when deemed fit the dividend can be altered or a compulsory redemption can take place. That can be the case when the company for instance sells airplanes or the business environment improves. Following the reversal from the Thai Airways contract structure to the more acceptable monthly rates, Amedeo bought back shares and increased its dividend from 6 pence per share per year to 7 pence.

The yield of 15% is high for several reasons. One reason is a positive and that is the dedication to returning value to shareholders. That is how managed funds work, but there are also some negatives. The compulsory redemption of shares can be seen as a negative to any upside the stock has as there is no way to refuse the redemption if you don’t agree with the terms. Furthermore, the company’s portfolio is not extremely attractive nor does it have an attractive scale which infuses risk. Next to that, while the company also considers increasing the portfolio size it might do so by raising equity through issuing shares and dilution is a very real possibility as the existing airplane portfolio does not make it extremely attractive to finance with debt and it should also be considered that the way the pool works is that investors finance the airplanes when possible and they also get the rewards shared with them.

Liquidation Risk For Amedeo

By 2029, the future of the fund will be reviewed and the way I am viewing things essentially by 2029 the fund is scheduled to close down in an orderly manner. In case that shareholders do not approve the wind up, airplanes can be re-leased with proceeds used for reinvestment in other airplanes and debt reduction. So, while the fund does not have a fixed life it does seem that if things go as expected by 2029 the fund will be shut down which also further reduces its appeal and risk for long-term focused investors. The undesired side effect this also has is that some investors are looking to disposing airplanes at present trying to pull shareholder returns forward. As an example, some investors are trying to persuade the fund to sell the Airbus A350-900s on lease to Thai Airways. That is the most future proof asset the fund has and it shows that due to the fund structure, there is a somewhat short term mindset that might not be beneficial to the operations of the fund.

Amedeo has extended the leases of the four airplanes leased to Thai Airways. The lease extension of the four Airbus A350s was already announced last year and is part of a broader lease restructuring for the leases with Thai Airways. In theory, this does not change any expectations for the fund to wind up or not. Typically, an airplane under lease has a higher value which could give Amedeo more distributable funds if it decides to sell the airplanes with leases attached. Since the airplanes are leased by Thai Airways, which is considered a riskier customer and still needs to pay deferred leases, it is unknown whether this is a positive or negative enhancement of the asset value. With the asset being leased to a higher risk customer with lease rent to be determined by the underlying value plus any premium, could increase the value in the sense that Thai Airways possibly pays a higher risk premium on its leases making the asset more valuable for lessors. Alternatively, parties could consider the risk too high which negatively affects the asset value. Overall, the Airbus A350s which also still have associated debt are difficult to assess. To shareholders, they might not be accretive until associated debt is extinguished.

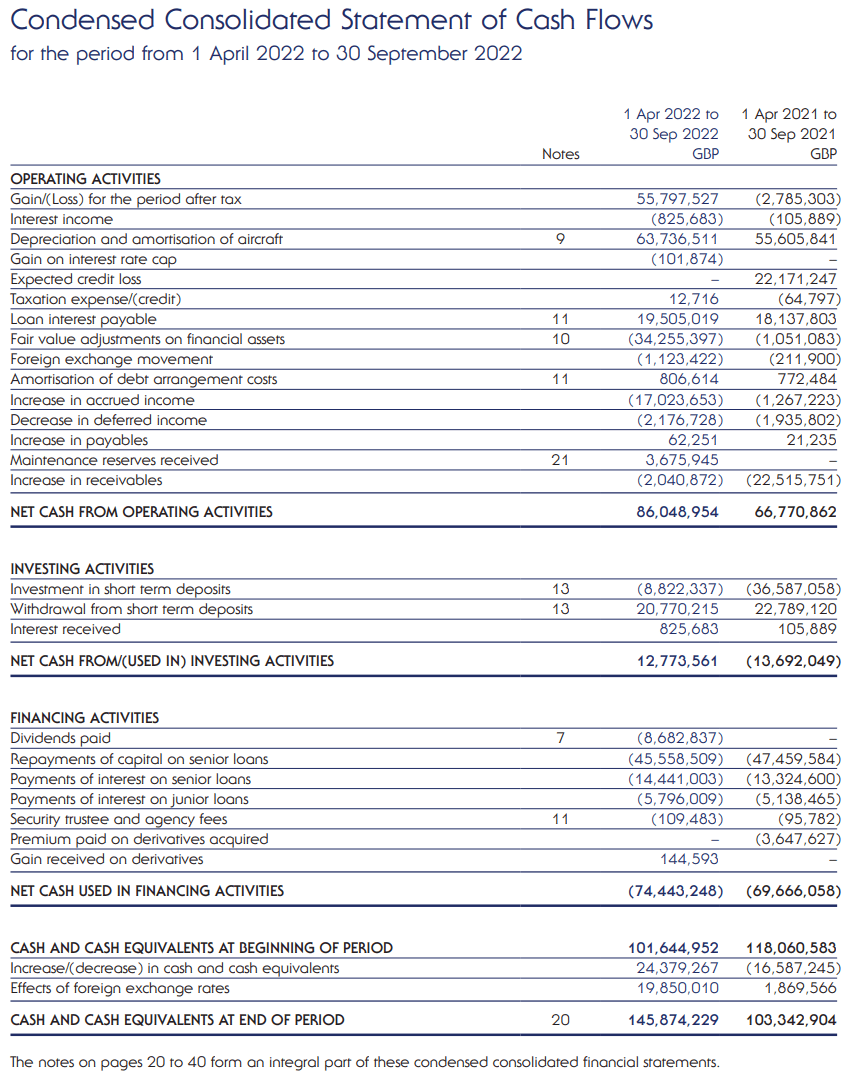

A Look At The Financials

I could analyze the P&L statement, but I think the cash story is more interesting to assess for the simple reason that the dividend and debt position are of interest. Whether one assesses the P&L or cash flow statement, what should be kept in mind is that Amedeo has not yet provided H1 2023 results, which in part include the return of Thai Airways to fixed month payments from January 2023. That makes both statements a bit less useful for forward projection.

{kind=link}

The most recent cash flow statement shows a 29% increase in operating cash and I would expect H1 2023 and H2 2023 both to be showing sequential improvement. Every six months, little over 50 million GBP goes towards debt reduction. At the end of September 2022, there was still 1 billion GBP in debt remaining. At the time the liquidation vote takes place, around half of the debt will still be on the balance. Roughly around 150 million GBP could be obtained from selling the 4 A350s, possibly around 80 million GPB in the low value scenario and another 100 million GPB. The actual values rely on many factors, but overall this would bring us to 330 million GPB of debt reduction from the sale of the airplanes. So, from airplane sales there would actually be no proceeds to shareholders since it does not even pay for the outstanding debt. The best path forward would be to keep the airplanes and continue leasing those to customers for the simple reason that it would make little sense to have the debt associated with the strongest assets in the portfolio removed by 2029 and then or before that time sell the airplanes because the point where the airplane is debt free is where the return for investment is in the best spot.

Conclusion: Amedeo Dividend Yield Is Not Necessarily Unattractive

I think Amedeo’s dividend yield is not necessarily unattractive, but there are portfolio and diversification risks that should be kept in mind. Furthermore, the way the fund is structured and scheduled there are additional pressures. Either way, I would mark the stock a hold but certainly not a buy. Furthermore, if Amedeo sounds attractive to you I would opt for the London-registered shares over the OTC pink tier shares which barely have any volume or market making.

For existing investors, I would think that a continuation of the company will be beneficial as the Airbus A350s will have better value for shareholders after the debts are reduced. I deem it unlikely that selling the airplanes earlier will be to the benefit of shareholders due to the debt associated with these airplanes.

For further details see:

Amedeo Air Four Plus Limited: Airplane Lessor With A 15% Yield