AMED - Amedisys And Option Care Health: High-Probability Merger Arb

2023-05-16 08:02:06 ET

Summary

- Infusion services provider Option Care Health is acquiring home healthcare provider Amedisys.

- The merger spread currently stands at 9%, implying a potential 18%+ IRR.

- The spread seems to exist due to uncertainty around OPCH’s shareholder approval.

- I expect the buyer’s equity holders to support the transaction given the target’s fair valuation as well as strong strategic rationale.

This is an interesting mid-cap merger arb that seems likely to satisfy all closing conditions and close. Home and alternate site infusion services provider Option Care Health (OPCH) is acquiring home and hospice healthcare provider Amedisys (AMED). AMED equity holders are set to receive 3.0123 shares of OPCH per each AMED. At current prices, the merger spread stands at 9%. The merger will require shareholder approvals on both sides as well as a regulatory go-ahead. The companies expect transaction closing in H2'23. Assuming a fairly conservative six-month closing timeline, the situation would deliver an IRR of over 18%. There is plenty of cheap OPCH borrowing for hedging.

The existing spread seems to exist due to uncertainty around the buyer's shareholder approval. OPCH investor reaction to the merger has been negative as indicated by a 16% share price drop upon the announcement. However, I believe that OPCH's shareholders are eventually likely to support the pending transaction given a few arguments:

- The acquirer seems to be getting a good deal from a valuation perspective. The merger values AMED at 10.7x EV/adjusted EBITDA multiple - slightly below the 11x-23x range for comparable home healthcare industry transactions. Moreover, the current offer comes in below AMED's historical EV/TTM adjusted EBITDA valuation range of 13x-36x.

- The merger is highly strategic for the acquirer, giving it a push into the secularly growing value-based home healthcare market. Aside from the potential vertical integration, the merger would allow OPCH to materially expand its geographical footprint and diversify its revenue base.

- OPCH's management has a good track record of completing and integrating value-accretive acquisitions/mergers.

Let's go through these aspects one by one.

AMED Business And Buyout Valuation

AMED provides home healthcare, hospital at-home, hospice, and acute-care services. The company houses a network of clinicians (20k as of Feb'23) as well as care centers (532). AMED's home health segment (61% of revenues) comprises nursing, physical therapy, and other services provided to patients in their homes. The hospice segment (35%) provides end-of-life care to seriously ill/injured patients. AMED generates a significant portion of its sales (76%) from government payers (i.e. government-managed Medicare and Medicaid programs).

OPCH's acquisition bid values AMED at 10.7x EV/2022 adjusted EBITDA. This valuation is below that of UnitedHealth Group's acquisition of home healthcare provider LHC Group (completed in Feb'23) valuing the target at 22.6x 2021 adjusted EBITDA. AMED and LHCG have compounded their revenues at a similar CAGR during 2019-2022 (4% for AMED vs. 3% for LHCG). The companies have also displayed similar adjusted EBITDA margins, reaching 12% and 14% for LHCG and AMED respectively in 2021. Another data point here is Humana's acquisition of the remaining 60% stake in Kindred At Home back in 2021 at 11x 2021E EBITDA. Worth noting that Humana acquired the remaining stake at a price that was pre-agreed back in 2018, with industry participants describing the 2021 acquisition as a "relative steal" for Humana. While financial disclosures for Kindred At Home have been limited (co-owned by two PE firms and Humana from 2018 through 2021), AMED and Kindred At Home both compounded their adjusted EBITDA at 20-21% annual clips during 2017-2021. Other industry acquisitions include BrightSprings Health Services' merger with Abode Healthcare (announced in Feb'21, 15.5x EV/EBITDA) and Thomas H. Lee Partners' acquisition of Care Hospice (Oct'20, 15.0x).

The current multiple is also below where AMED used to trade historically. In 2016-2021 period, the business was valued at 12.6x-35.7x TTM adjusted EBITDA multiples. However, worth noting that AMED's larger peer EHC currently trades in line with the company on 2022 adjusted EBITDA. While AMED has grown at a slightly faster clip during 2019-2022, EHC has boasted higher adjusted EBITDA margins (19% in 2022 vs 13% for AMED).

Strategic Rationale

OPCH operates in the home and alternate site infusion services market. The services provided by the company include the administration of intravenous medications, nutrition, and other treatments. Infusion is provided in patients' homes as well as in OPCH's network of pharmacies and stand-alone ambulatory infusion suites. OPCH is reimbursed for the cost of pharmaceuticals and the cost of services (such as nursing and therapy). The majority of the company's revenues (88%) come from contracts with private payers, such as managed care organizations and insurance companies. The remaining revenue share (12%) is from services that are directly reimbursable through government-run health insurance programs, such as Medicare. 70% of OPCH's infusion services revenues come from chronic therapies while the remainder of revenues is attributable to acute therapies.

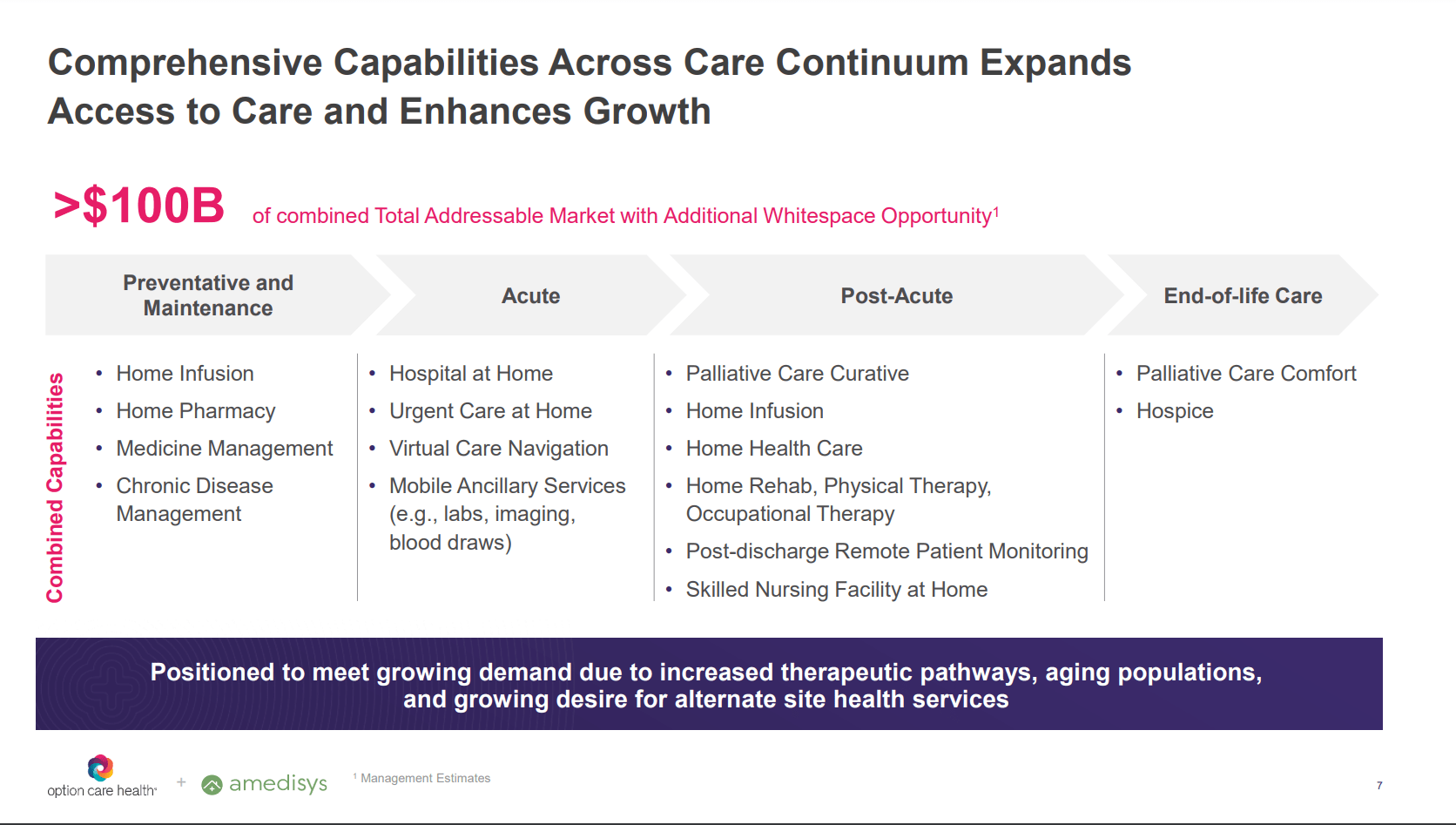

The potential transaction would have a strong strategic angle given the complementary businesses of AMED and OPCH. The merger would expand OPCH's healthcare infusion service offerings with a range of acute, post-acute, and end-of-life care services (see below), allowing the combined entity to operate a single provider of these healthcare services. Importantly, this vertical integration is expected to give the company a strong push toward the value-based care model where healthcare providers are paid based on healthcare outcomes as opposed to the services provided. Value-based care service market is expected to grow rapidly in the upcoming years driven by a secular shift from the traditional fee-for-service model due to lower resulting healthcare costs to patients. The industry has seen the entry of a number of players, including large healthcare insurers CVS Health and UnitedHealth Group, which have scooped up value-based home healthcare providers. The combined OPCH-AMED, due to its larger scale ($6.2bn in combined 2022 revenues) and presence along the entire home healthcare service continuum, would be able to better compete in the market to attract customers, such as health systems, health plans, and government agencies (see quotes from the management teams below).

From AMED's CEO during the merger conference call ( requires registration ):

We have conversations with health plans, health systems, referral sources all the time about what John just said. Is there a way that we can bundle these services together into a commercial contract for simplicity and efficiency at the local level to deliver care or at the -- at health plan level around value-based arrangements. And so, what we've done here over time is we're able to put all of our services together in a more comprehensive care delivery platform, and that should enable us to engage with our health plan partners in a way to bring them value, but also bring some for our patients and the organizations.

From OPCH's CEO during the recent BofA Securities Health Care Conference 2023 :

Payers are really starting to change their view around focusing around total cost of care whether you want to call that value-based reimbursement or other models. We know that the reimbursement model will be changing over time and thinking about what we need to do to provide broader services with that.

From OPCH's CFO during the recent BofA Securities Health Care Conference 2023:

It's hard to really define value-based in a clear way, but we know it's evolving. We know the total cost of care is something that is front and center that needs to be dealt with and having the ability to think more broadly, not just on the infusion event, but on the total patient care and being a bigger part of that care plan, we think allows us to have a stronger voice in that process in a better position in order to be part of the change that's coming.

Amedisys and Option Care Health Merger Investor Presentation, May 3, 2023

{kind=link}

Aside from the potential shift to value-based care, the merger would allow OPCH to significantly expand its geographical footprint from 163 sites currently to 674 by adding AMED's locations where infusion services could potentially be offered. The merger parties have noted that there has been a significant overlap between the patients of both companies - a quote from AMED's CEO during the merger conference call:

In our home health and our hospice business, we have a pretty good density of patients who need the services that Option Care provides, and vice versa with Option Care providing infused services for folks who consume home health and hospice, and of course, the high acuity, which was one of the ones that we outlined. So I think there's a fantastic opportunity between both organizations to increase the health outcomes for the patients we have by combining our services, let alone the ability to develop, recruit, and retain an 18,000-plus clinician workforce. That's pretty exciting.

Another strategic benefit of the merger comes from different payer mixes for both companies as OPCH's customers are mostly private commercial payers compared to primarily government entities for AMED. The merger is expected to diversify OPCH's revenue base as well as potentially allow for cross-selling opportunities, including providing home healthcare services to OPCH's primarily Medicare Advantage (i.e. health plans offered by private companies) customers. The companies have guided for synergies reaching $75m in annual incremental EBITDA by year three after transaction closing, comprised of $50m in cost savings and $25m in incremental sales. This compares to $622m in combined adjusted EBITDA printed in 2022. Worth noting that since 2021 both companies have been in a partnership whereby Amedisys' personnel provided infusion services to COVID-19 patients. OPCH's management has mentioned that recently the company has been in another partnership with AMED's hospital at-home arm Contessa Health.

OPCH's Acquisition Track Record

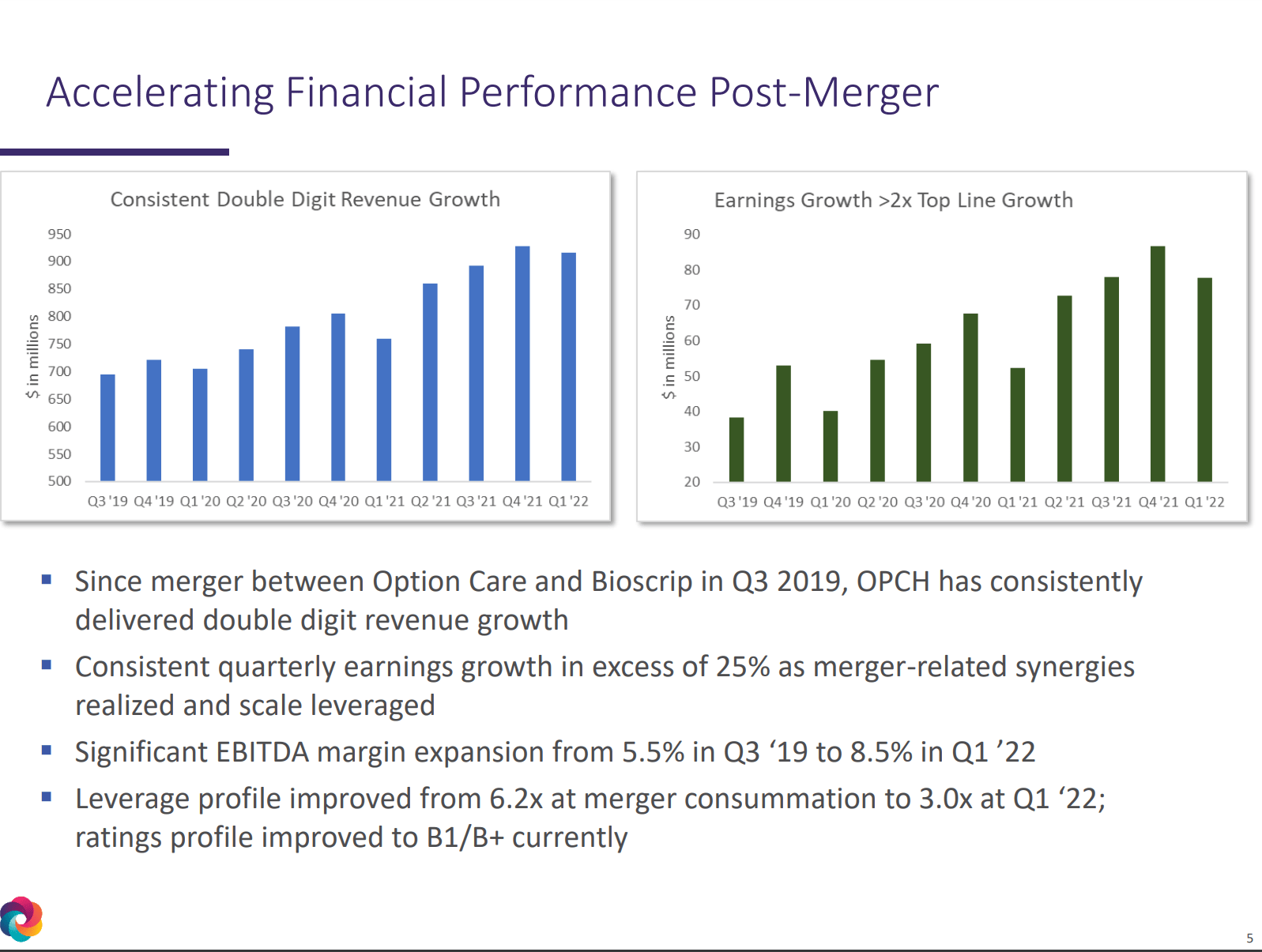

What also gives confidence in a successful merger implementation/integration is OPCH's track record of value-accretive acquisitions. OPCH is a serial acquirer with a number of mergers completed in recent years, including BioScrip (reverse merger performed in 2019), BioCureRX (acquired in 2021), Infinity Infusion Nursing (2021), Wasatch Infusion (2021) and Specialty Pharmacy Nursing Network (2022). OPCH's reverse merger with BioScrip combined two of the US's largest independent infusion services providers. The merger was eventually successfully integrated as displayed by the combined entity's consistent revenue growth and increasing EBITDA margins since the merger closing (see below). OPCH's share price has risen over 100% since the BioScrip reverse merger was completed.

William Blair 42nd Annual Growth Stock Conference, June 7, 2022

{kind=link}

OPCH And AMED Shareholders

Given the strong strategic rationale, fair valuation of the target, and the management's track record of pursuing and integrating value-accretive acquisitions, I expect OPCH equity holders to approve the merger. OPCH's shareholder base includes a number of institutional shareholders, including BlackRock (11%), Vanguard (9%), and Fidelity Investments (8%). 6% is owned by Walgreens Boots Alliance.

Likewise, AMED shareholder approval seems likely as all-stock merger consideration allows the target shareholders to participate in the upside of the combined company. While the transaction appears to value AMED at a fair-to-low adjusted EBITDA multiple, I do not expect any pushback from the target's equity holders. Importantly, AMED's business and the broader home healthcare space have been facing planned and anticipated cuts ( here and here ) to reimbursement for government-managed Medicare home healthcare services. Given AMED's reliance on Medicare reimbursements, this might negatively impact the company's top line going forward. In this context, the merger, which would diversify AMED's revenue base with a number of private commercial customers, seems to be a strategic move. AMED's shareholder base includes a number of institutional investors (40% combined stake), including JP Morgan Chase (owns 5%), BlackRock (13%), Wellington Management (9%), Vanguard (10%), and Ameriprise Financial (3%). AMED's management owns 2%.

Regulatory Outlook

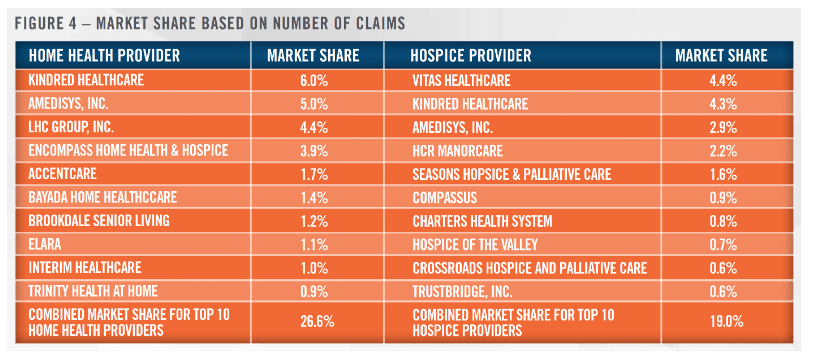

I do not expect the transaction to face any regulatory pushback. Admittedly, AMED and OPCH are among the largest players (by market shares) in the home healthcare and infusion services markets in the US respectively. OPCH is the largest independent infusion services provider in the US, with a 21% market share as of 2021. OPCH's largest competitors CVS Health ( CVS ) and UnitedHealth Group ( UNH ) captured 17% and 16% of the market in 2021. Meanwhile, AMED was the second-largest home healthcare provider in the US as of 2020 with a 5% market share.

Having said that, any regulatory opposition to the deal seems unlikely as AMED and OPCH operate in different industries. While home health care comprises a range of services, including wound care, medication management, physical therapy, and others, infusion services are primarily focused on the administration of intravenous medications. Moreover, a part of OPCH's services is provided outside of patients' homes, i.e. in alternate sites, such as ambulatory infusion centers and physician offices. Another important aspect here is that the home healthcare market in the US is highly fragmented. In 2020, the largest industry player Kindred held an insignificant 6% market share while the portion of the market captured by the ten largest providers stood at only 27%. What gives added confidence in a successful regulatory go-ahead is the precedent of UnitedHealth Group's above-mentioned acquisition of home healthcare provider LHC Group. Both UnitedHealth Group and LHC Group occupied market shares similar to those of OPCH and AMED in the infusion services and home healthcare markets.

Worth noting that OPCH's management has been confident about securing the required regulatory approvals - from the merger conference call :

Yeah, as you'd imagine, obviously there's the HSR in the regulatory process and as you'd expect with two healthcare services organizations, there are commensurate regulatory filings across the country. But again, as John highlighted in his comments, we have a high degree of conviction that we should be able to close this before year-end.

{kind=link}

Conclusion

The ongoing AMED-OPCH merger presents an interesting event-driven investment opportunity. The merger spread seems to be explained by uncertainty surrounding the acquirer's shareholder approval. However, given fair-to-low valuation, strong strategic rationale, and OPCH management's good track record of mergers/acquisitions, I believe the risk is minimal. At current price levels, the situation potentially offers an IRR of over 18%.

For further details see:

Amedisys And Option Care Health: High-Probability Merger Arb