AMED - Amedisys: We Are Still Neutral Reiterate Hold

Summary

- Amedisys delivered a mixed set of Q4 numbers, with upsides vs consensus.

- In more detail, growth was inconsistent across key divisions and further down the P&L.

- Returns on capital below the hurdle rate remain as a key tension point.

- Looks overpriced at 26x earnings. Rate hold.

Investment summary

After extensively reviewing its Q4 results, our appraisal on Amedisys, Inc.'s (AMED) equity remains a hold. Since our last publication, the stock has caught a bid, yet, our observations of the company's financials remain unchanged. As noted last time, the " dominance of goodwill 'assets' on the balance sheet " still remains a concern, as we noted goodwill still comprised ~116% of the company's book value at the end of Q4. Added to that, sequential economic losses (i.e., ROIC<cost of capital) eroded shareholder value over the 12 months, coupled with the company's negative growth rates.

Reiterate hold at 19x P/E, in line with sector multiple.

Fig. (1)

{kind=link}

AMED Q4 results analysis

Turning immediately to the numbers . Top-line revenue growth of 50bps YoY came into $562mm on adj. EBITDA of ~$60mm, down 830bps YoY. It pulled this down to earnings of $31.7mm, or $0.97 per share, both numbers also down on the same time last year. Having reviewed the divisional and operational highlights, our key takeaways are as follows:

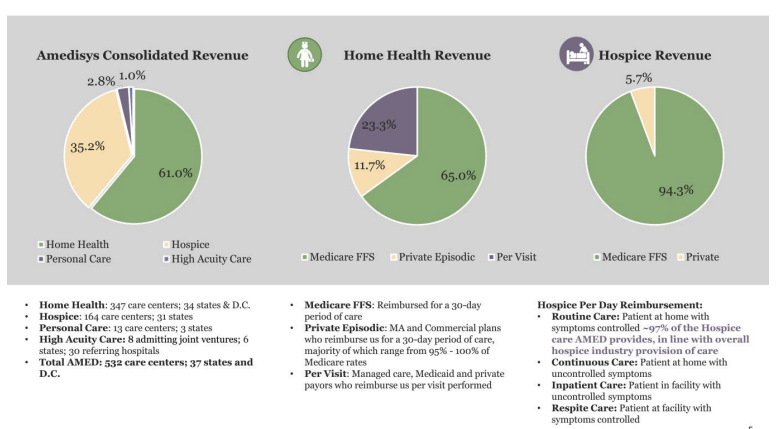

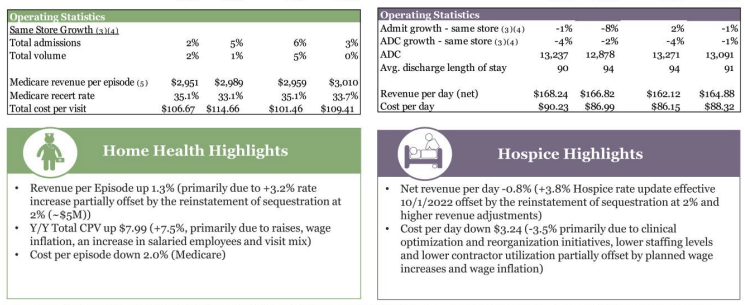

- Top-line sales attributed to its home health ("HH") segment, contributing 61% of total turnover, lifted to $342mm, underlined by growth in non-Medicare revenues. HH revenue per episode gained 130bps YoY from a 3.2% rate increase, balanced by a 2% sequestration headwind. Total admissions were up 8.3% YoY to 94,365, on total volumes of ~138,000. Looking deeper, the cost per visit gained 6.5% YoY to $114, driven by raises in clinical manager and clinician costs per visit. In total, there were ~1.7mm visits, down 480bps YoY.

- Related to 1), HH same-store growth came into 5%, pushed up by the Medicare revenue per episode, with the medicare recertification rate down 200bps YoY. Related to the HH G&A line, corporate expenses were $89mm or 26% of turnover, excluding acquisitions of $3mm.

- Hospice segment revenues pared back $7mm YoY to $197mm on a 48% gross margin, a decompression of ~100bps from Q4 FY21'. The bolus of hospice revenue stemmed from Medicare FFS. It recognized quarterly core hospice EBITDA of $44mm at a 22% margin. For the full year, the division's EBITDA clipped back 325bps to $166mm.

- Same-store admissions for the hospice business were down 8% YoY coupled with a 4-day increase in the average discharge length of stay. Subsequently, net revenue per day was down ~$2mm to $166mm on an $87 cost per day.

- Perhaps the key highlight from the quarter was the firm's decision to divest its personal care division to HouseWorks LLC. HouseWorks provides personal care services to ~75 home care agencies across several jurisdictions in the U.S. Financials of the transaction weren't immediately disclosed, but it is expected to close in Q2 this year.

- In extension, from 5), AMED also advised it signed a partnership with BlueCross BlueShield in Tennessee to provide at-home palliative care services, leveraging its newly acquired Contessa platform in the process.

Fig. (2)

{kind=link}

{kind=link}

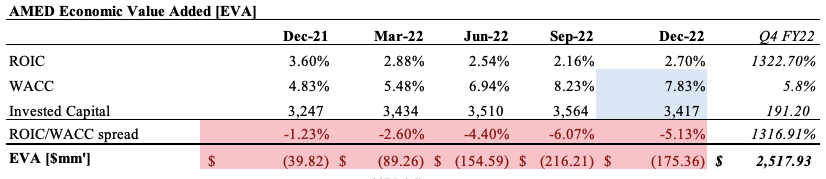

Returns on capital, profitability

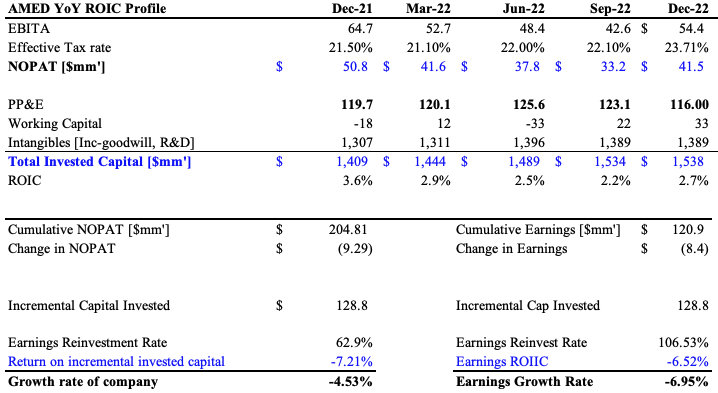

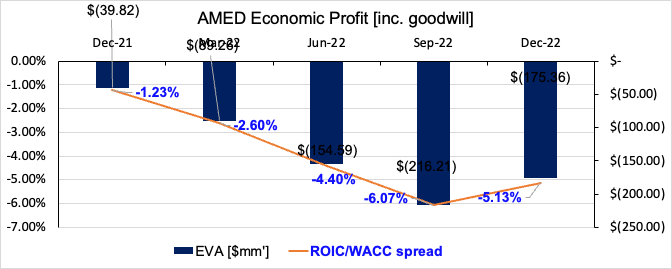

Key risks for value seekers are identified here. Intelligent investors will know that a firm creates future value (both corporate value and for its shareholders) when its ROIC is positive and exceeds the cost of capital - i.e., an economic profit. In that vein, AMED had a destructive period to value over the 12 months to Q4 FY22. It generated $204mm in cumulative sequential NOPAT, on a $9.3mm YoY decline in Q4 NOPAT. It invested a net $128.8mm in capital to generate these figures. The same analysis for earnings is observed in the bottom right of Figure 3. Three key findings spring to light:

- The incremental ROIC from Q4 FY21'-Q4 FY22' was negative 7.2% (a corresponding negative 6.5% earnings ROIIC).

- It reinvested ~63% of post-tax earnings to generate this negative rate of return.

- Alas, both NOPAT and earnings declined 4.5% and ~7% respectively.

Fig. (3)

{kind=link}

Added to that, it booked ~$32mm in quarterly net income, but this is an accounting reality. The economic reality tells a different story. In fact, since Q4 FY21', AMED recognized sequential economic losses, most recently at $175mm, or a negative 5.13% ROIC/WACC spread in the last quarter. In detail, this represents an erosion of value for equity holders and illustrates the hurdle AMED must overcome into the subsequent periods to reverse the situation. There are no major catalysts to recognize other than the personal care divestiture that may contribute to a reversal here. The company also guides $2.27Bn in top-line sales for FY23, behind a $2.36Bn consensus, on adj. EBITDA of $240mm at the upper range. Management also guided below consensus FY23 EPS at $4.36. However, if the economic losses deepen, we estimate this will clamp AMED's propensity for valuation upside looking down the line. Alas, AMED has some work to do to prove its sturdiness for the intelligent investor to add the stock into their equity risk budget.

Fig. (4)

{kind=link}

Fig. (5)

{kind=link}

Valuation and conclusion

In an inflationary and high-yield environment, paying >26x trailing earnings to buy AMED for no dividend income and tightening residual cash flows is an unattractive prospect, by estimate. This is also a premium to sector peers. Supporting this, the stock trades at ~3x book value, and >32x trailing cash flow. We believe the stock should trade closer to the peer's at 19x earnings, implying a FY23 price target of ~$83, baking in the compressed growth profile. This supports a neutral view but also gives headroom for multiple expansion this year.

Net-net, it was another period of lumpy growth for AMED, with inconsistent upsides observed throughout its financial statements. Looking in more detail, ROIC and forward guidance are key tension points investors have to navigate through with AMED this year. Supporting the above, the stock is richly priced at 26x earnings and the quant factor system rates it a hold. Reiterate hold.

For further details see:

Amedisys: We Are Still Neutral, Reiterate Hold