AMTB - Amerant Bancorp's Q2 Earnings: Promising Numbers But Challenges Loom

2023-07-24 11:36:31 ET

Summary

- Amerant Bancorp Inc. reported Q2 2023 EPS of $0.22 beats by $0.02, and revenue of $110.49M that beat by $13.38M.

- Despite promising numbers, the bank faces challenges including a contraction in key metrics and underperformance within the sector, which could impact its future prospects.

- The company's operational efficiency issues, contraction in ROA, ROE, and non-interest bearing deposits, and poor return on total assets lead to a "Hold" rating for its stock.

Thesis

In this article, I explore Amerant Bancorp Inc. ( AMTB ) Q2 2023 earnings figures that stand out with an EPS of $0.22 that beat by $0.02, and revenue of $110.49M that beats by $13.38M. However, I argue that despite these promising numbers, several underlying challenges, including a contraction in key metrics and underperformance within the sector, cast a shadow over the bank's future prospects

Company Profile

Amerant Bancorp Inc. provides an impressive portfolio of banking services and products both domestically in the U.S. and on an international scale.

In the realm of account options, their offerings span traditional checking, savings, business, and money market accounts, along with cash management services and the option of certificates of deposits.

When we drill down into the lending side of their business, there's a mix of commercial real estate loans, including both variable and fixed rate options.

And for the individual consumer, Amerant offers everything from automobile and personal loans, to loans secured by cash or securities, revolving credit card agreements as well as specialized services for high-net-worth customers – a comprehensive suite that encompasses trust and estate planning, brokerage and investment advisory services in the global capital markets, and wealth management and fiduciary services.

Amerant Bancorp's Q2 2023 Earnings Highlights

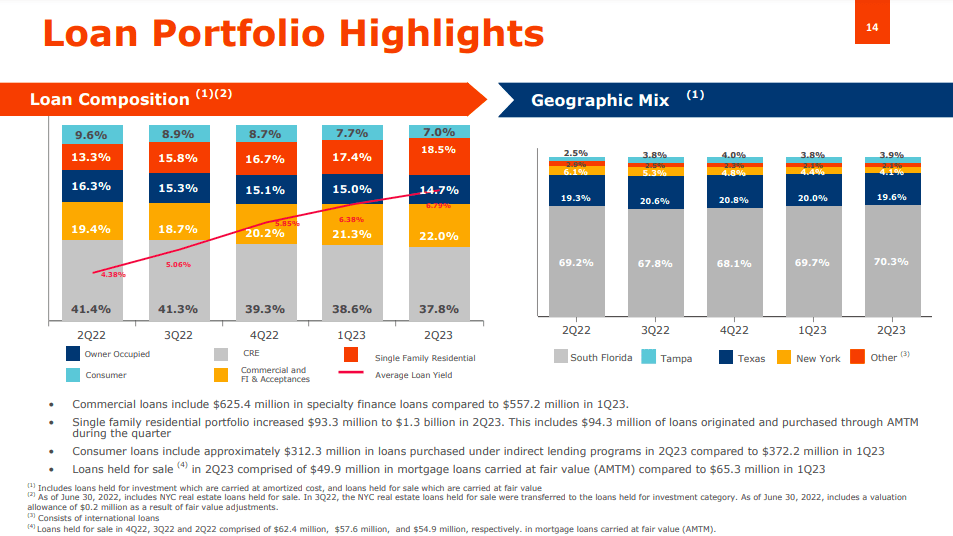

Amerant Bancorp exhibited moderate amplification in their loan portfolio. The overall expansion in loans climbed 1.4% , amounting to a sturdy $7.2 billion in the second quarter.

Amerant's Investor Presentation

{kind=link}

This upturn was primarily propelled by loan origination endeavors, notably within the realms of specialty finance and single-family residential mortgage. The specialty finance loans registered a growth from $557 million in Q1 to $625 million, while the residential portfolio burgeoned by $93 million to $1.33 billion.

When we shift focus to investment, Amerant Bancorp's Q2 balance for investment securities remained unaltered at $1.3 billion. Concurrently, the tenure of the investment portfolio has been stretched to 5.1 years, influenced by a rise in mortgage rates.

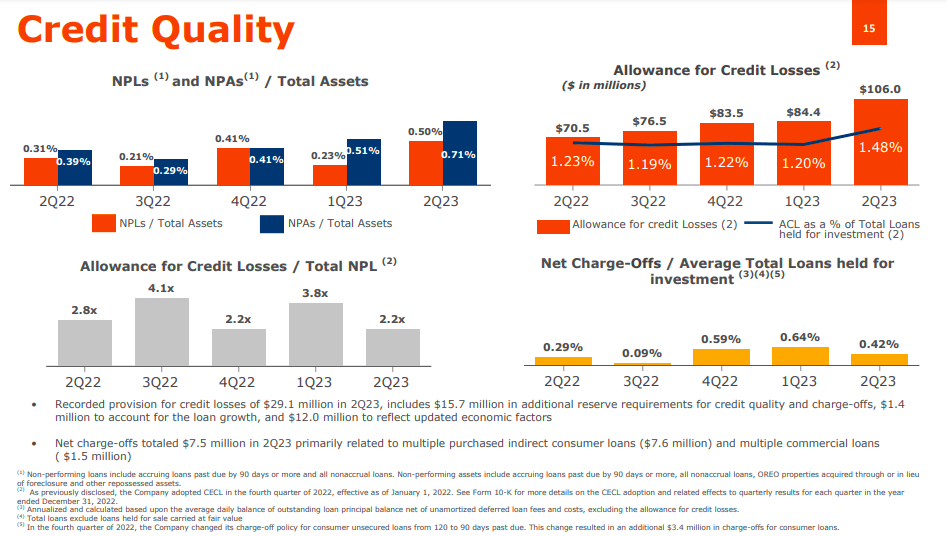

The allowance for credit losses escalated to 1.48%, up from 1.2% in the first quarter. This trend underscores an amplified provisioning for loan loss, instigated by dynamics such as economic forecast revisions and charge-offs. By the end of Q2, the allowance for credit losses (see chart below) accounted for a substantial $106 million, a noteworthy leap of 25.6% quarter-over-quarter.

Amerant's Investor Presentation

{kind=link}

Nevertheless, the financial landscape wasn't entirely bathed in positive light. The efficiency ratio along with return metrics, ROA and ROE, contracted this quarter due to escalating provision and non-standard charges. The efficiency ratio was pegged at 65.6%, up from 63.7% in the preceding quarter, with ROA and ROE measuring 0.31% and 3.92% respectively.

Moreover, consumer loans in Q2 shrunk by 8.5% quarter-over-quarter, settling at $503 million, and the ratio of non-performing loans to total loans escalated to 65 basis points, an ascent from 31 basis points in the last quarter. According to management, this uptick is chiefly attributable to further downgrades of a loan in New York City and a commercial loan.

The net interest income saw a marginal upswing of 1.9%, culminating at $83.9 million for Q2. However, the net interest margin underwent a shrinkage, dropping by 7 basis points quarter-over-quarter to 3.83%.

And finally, the bank successfully navigated the transition from LIBOR to SOFR, modifying approximately 390 loans with a cumulative balance of nearly $1.1 billion, reaffirming the bank's resolve to adhere to market norms.

Performance

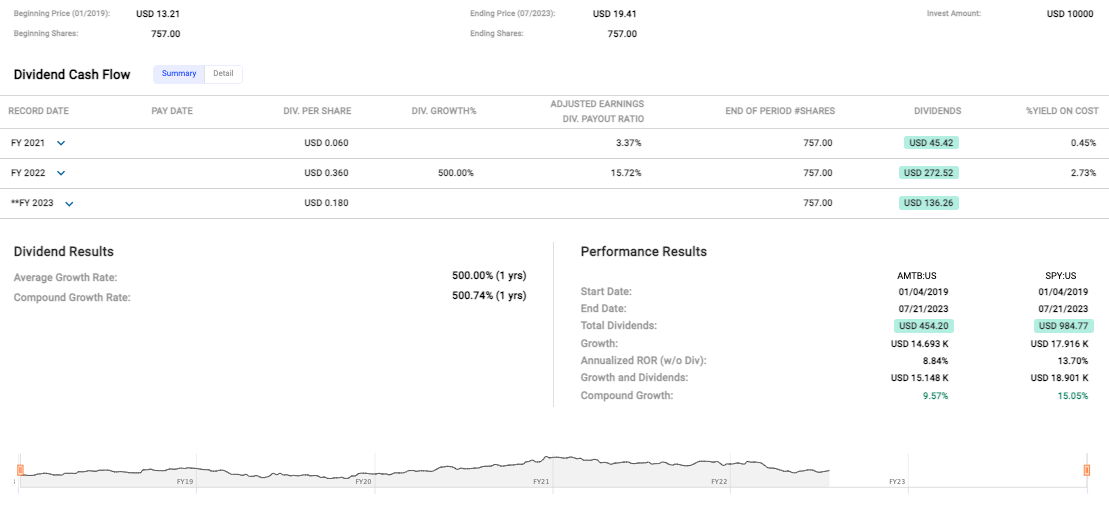

In terms of share price appreciation, it's commendable that Amerant has grown its stock price from USD $13.21 in 2019 to USD $19.41 in 2023. A hypothetical investment of USD $10,000 (see data below) would have grown to USD $14,693 during this period, translating to an annualized rate of return (without dividends) of 8.84%. However, when we bring the S&P 500 Index (SP500) into the picture, we see it has outperformed Amerant with a 13.70% annualized return over the same period.

{kind=link}

Even considering the compound growth (including dividends), Amerant delivered a respectable 9.57%, but again, the S&P 500 far outstripped this with a return of 15.05%. So, from a comparative perspective, Amerant's performance seems to have been somewhat lackluster.

Valuation

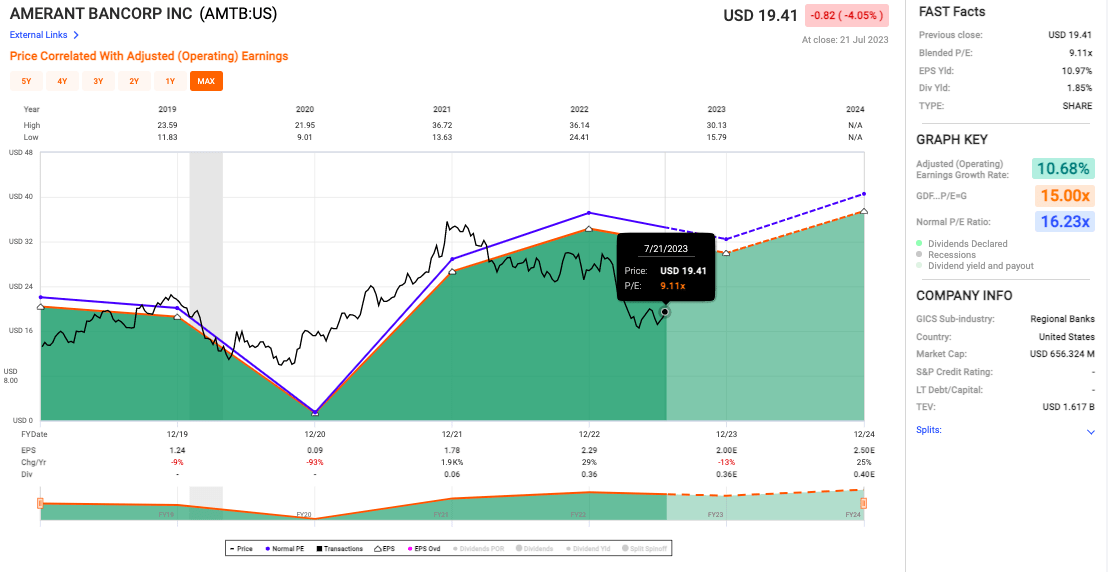

Considering that the blended Price/Earnings (P/E) ratio which is 9.11x, which is materially lower than the "normal" P/E ratio of 16.23x, could be indicative of undervaluation. And when we move on to the earnings yield (EPS yield) - it's standing at an attractive 10.97% signifying a potentially solid return on investment.

{kind=link}

Adding to that, we can see an adjusted (operating) earnings growth rate of 10.68% which is a sign of strong performance and suggests the company could be well positioned to continue delivering growth moving forward.

Risks & Headwinds

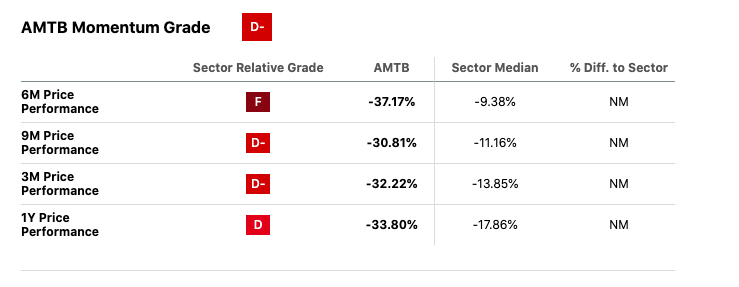

First off, looking at Seeking Alpha's Momentum Grade metrics (see data below), we find a 6-month price performance of -37.17% which signifies that the bank is far off the sector's already concerning median of -9.38%. And this underperformance isn't a recent phenomenon. Over 9 months, AMTB is still significantly behind its sector counterparts, marking a -30.81% performance. The data's downward momentum potentially hints at deeper structural issues within the company that aren't easily remedied by short-term market fluctuations.

{kind=link}

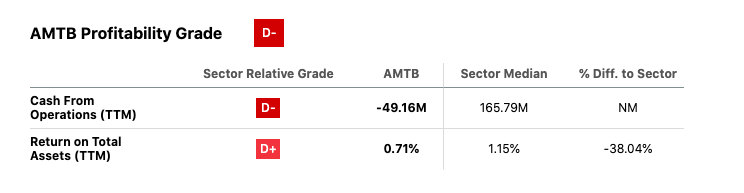

Furthermore, when comparing AMTB's cash from operations ((TTM)) with the sector's median, the situation worsens (see below). Amerant's trailing twelve months ((TTM)) cash from operations stands at a negative $49.16 million, while the median for other financial sector stocks is a healthier positive $165.79 million.

{kind=link}

Likewise, their return on total assets ((ROTA)) of 0.71% falls well short of the sector median of 1.15%. The return on assets figure is a significant metric, as it indicates how profitable a company is relative to its total assets. For AMTB, this underperformance suggests that they're not employing their assets as efficiently as their counterparts, which could point to poor investment decisions, misguided operational policies, or a lack of strategic vision.

When it comes to the bank's capital management, there's a palpable decrease in non-interest bearing deposits. These deposits, having slumped from 18.7% to 17.1% in the second quarter, spell out an unfavorable trajectory for the bank's cost management. Essentially, this implies a potential reduction in the bank's low-cost funding, a key backbone of their operations. Such a trend could, unfortunately, escalate the bank's cost of capital, affecting the ability to expand and invest. Along those lines, CEO Jerry Plush noted:

So I think where we are right now is we do believe that it's going to come in that solid 18 to 20 lower. We are going to grow. I mean, the view is we've got great pipelines on both sides of the balance sheet. But it is important to recognize that the key for us to keep our costs down is clearly to focus on non-interest bearing, so getting more relationship core operating accounts. And it's also to continue the growth and to really ramp up the growth in the international side because we see -- obviously, the advantage there is we can attract a lower cost and a very sticky deposit.

Lastly, shining a spotlight on the bank's operational efficiency, there's another potential obstacle emerging. Non-interest expenses, a core component of a bank's operational cost structure, have risen to 12% relative to the preceding quarter. This uptick may present a hurdle to the bank's net earnings, thereby impacting the overall profitability and possibly undermining the bank's financial health.

Final Takeaway

Given the operational efficiency issues, contraction in key metrics such as ROA, ROE, and non-interest bearing deposits, coupled with the bank's underperformance in the sector and its poor return on total assets, I would rate Amerant Bancorp stock a "Hold." While the company demonstrates promising growth in its loan portfolio and potentially undervalued P/E ratio, I believe that the observed trends present some serious concerns which need addressing before a "Buy" rating can be justified.

For further details see:

Amerant Bancorp's Q2 Earnings: Promising Numbers, But Challenges Loom