AEE - Ameren: Electric Utility Offers A Very Attractive Investment Proposition Today

Summary

- Ameren Corporation is a fairly large electric and natural gas utility that serves the city of St. Louis and most of the state of Illinois.

- The company enjoys remarkable financial stability, which should be very attractive today considering the strain that the economy is inflicting on household budgets.

- The company is positioned to provide its investors with an average annual return of 9% to 11%, which is quite attractive for a utility.

- The company has an attractive balance sheet and will likely increase its dividend within the next few weeks.

- Ameren Corporation boasts a very reasonable valuation and could prove a worthy addition to a portfolio today.

Ameren Corporation ( AEE ) is a regulated electric and natural gas utility serving customers throughout Missouri and Illinois. The utility sector in general has long been among the favorite holdings for conservative investors, such as retirees. There are some very good reasons for this, as most of these companies enjoy remarkably stable cash flows and high dividend yields. Ameren Corporation is certainly no exception to this, as its third quarter results showed its general stability.

Admittedly, though, the company’s 2.60% current yield is a bit lower than we really want to see from a utility, but Ameren has a long history of raising its dividend over time, so it is likely that the yield-on-cost will improve in the very near future. As some readers might recall, I have discussed Ameren before, but that was nearly six months ago, so the company has had a few developments since then. Our overall thesis still has not really changed, but the company does look slightly more expensive today, and it is always important to get an update on its financial condition.

About Ameren Corporation

As stated in the introduction, Ameren Corporation is a regulated electric and natural gas utility that serves the St. Louis Metropolitan Area as well as most of Illinois:

Ameren Corporation

Although this is a fairly large geographic area that includes a few major cities, the company serves fewer customers than might be expected. This is because the company’s service area notably does not include the city of Chicago, and much of Illinois is rural apart from that city. Ameren still manages to include 1.2 million electric and 100,000 natural gas customers within its reach, however.

The fact that the company is primarily a provider of electric service is something that some readers might find appealing. After all, for the past several years, we have been hearing about “electrification,” which refers to the conversion of things that are powered by natural gas or other fossil fuels to the use of electricity instead. One of the areas that are targeted for conversion is space heating, which is the primary use of natural gas. As such, natural gas utilities might be considered to be on the way to extinction. The fact that Ameren primarily provides electricity could be thought of as a good thing for this reason.

However, as I have explained in many previous articles (see here ), this belief is unlikely to play out the way that proponents of electrification expect. Nonetheless, there is one big advantage to primarily providing electricity. As just mentioned, the biggest use of utility-supplied natural gas is for space heating of homes or businesses. That is something that is needed in the winter months, but not so much during the summer. As such, natural gas utilities tend to see their operating cash flows increase dramatically during the fourth and first quarters of the year and then report much weaker numbers during the summer months. Electricity does have higher consumption during the summer due to the demands of air conditioners, but its consumption is much more balanced throughout the year. Thus, electrical utilities like Ameren should enjoy pretty stable cash flows over the course of a year.

We can, in fact, see this by looking at the company’s quarterly operating cash flows. Here they are for the past eleven quarters:

{kind=link}

One thing that we do notice is that the company’s numbers tend to spike during the third quarter of the year. This is largely due to the additional electric consumption that occurs during the summer months due to air conditioners. When we compare each quarter to the same quarter in the prior year, we can see a remarkable amount of stability along with some growth. In fact, even the pandemic during 2020 had a negligible impact on this characteristic.

The biggest reason for this is that most people consider electricity and natural gas service to their homes and businesses to be a necessity for modern life. Indeed, in many ways, it is, since governments offer assistance to low-income people that cannot afford their utilities and it is often illegal to turn off utility service during certain months of the year. As such, most people prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. This is something that could be very important today.

As I pointed out in a recent article , the inflationary environment that we are currently in has strained the budgets of many households. It has now gotten to the point that 81% of Generation-Z members and 77% of Millennials have either seriously considered or have actually taken on second jobs simply to pay their bills. In addition, the economy is widely expected to enter into a recession in the near future, which tends to result in people having a much lower discretionary income. Thus, it may make sense to hold companies that can weather this with ease. Ameren fits this bill perfectly.

Naturally, as investors, we want to see more than just stability. It is critical that any company in our portfolios deliver long-term growth. Ameren Corporation is very well-positioned to do this. The primary way that Ameren will be generating growth is by expanding its rate base. The rate base is the value of the company’s assets upon which regulators allow it to generate a specified rate of return. As this rate of return is a percentage, any increase in the rate base enables the company to increase the prices that it charges its customers in order to earn that specified rate of return.

The usual way that a utility increases the size of its rate base is by spending money on upgrading, modernizing, or even expanding its utility-grade infrastructure. Ameren Corporation is planning to do exactly this, which it unveiled a year ago in its five-year spending plan. Over the 2022 to 2026 period, Ameren is planning to invest $17.3 billion into its infrastructure:

Ameren Corporation

I will admit that I would have preferred that the company provide its planned investment for each of the five years as some of its peers do but Ameren has not publicly provided this information. The company has also not provided any information about its 2027 capital investment plans, although it likely will provide an updated five-year plan in a few weeks when the company announces its fourth-quarter earnings results. Overall, the company’s investment plan should be sufficient to grow its rate base at a 7% compound annual growth rate over the period, which will take it from $21.1 billion at the end of 2021 to $29.6 billion by the end of 2026:

Ameren Corporation

At this point, we may see some readers point out that this growth is far less than the amount of money that the company is actually investing. That is certainly true, and it is expected. One reason for this is that some of the new assets that the company will be buying are intended to replace existing assets. Once these existing assets are replaced and retired, their residual value is then removed from the rate base. That offsets some of the company’s capital spending.

In addition to this, the value of the assets that the company owns is constantly going down due to depreciation. This means that something that the company purchases in 2022 will be worth less and have a lower impact on the rate base in 2026. The company thus needs to spend enough to overcome this process and still grow the rate base. Ameren’s current spending plan should accomplish this and grow its earnings per share at a 6% to 8% rate over the projection period. When we combine this with the company’s current dividend yield, we get a total average annual return of 9% to 11%, which is quite respectable for a conservative utility stock.

We actually saw this growth play out in the most recent quarter. During the third quarter of 2022, Ameren reported total revenue of $2.223 billion, which represents a 28.50% increase over the $1.730 billion that the company reported in the prior year's quarter. We also saw the company report earnings per share of $1.75 compared to $1.65 in the prior-year quarter. That is a 6.06% increase, which is right in line with the projections that we just made. We should be able to expect similar performance during the fourth quarter as well as going forward.

Financial Considerations

It is always important to look at the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is typically accomplished by issuing new debt in order to repay the maturing debt, which can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a decline in cash flows may push a company into financial distress if it has too much debt. Although utilities like Ameren Corporation tend to enjoy remarkably stable cash flows, this is still a risk that we should not ignore.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio essentially tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us how well a company’s equity will cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, Ameren Corporation had a net debt of $14.946 billion compared to $10.330 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.45, which is a slight increase over the 1.43 ratio that the company had the last time that we reviewed it. It still compares pretty well to its peers though, which we can see here:

| Company |

| Net Debt-to-Equity Ratio |

| Ameren Corporation |

| 1.45 |

| DTE Energy ( DTE ) |

| 2.22 |

| Public Service Enterprise Group ( PEG ) |

| 1.49 |

| Eversource Energy ( ES ) |

| 1.41 |

| Entergy Corporation ( ETR ) |

| 2.14 |

| CMS Energy ( CMS ) |

| 1.81 |

This is something that is quite nice to see, and it confirms my earlier statement that Ameren Corporation’s financial structure is quite reasonable for a utility. As we can see, it is either in line with or better than its peer group on this metric. This tells us that the company is almost certainly not employing too much debt in its financial structure and therefore its debt does not represent a particularly outsized risk. Overall, investors should feel reasonably comfortable here.

Dividend Analysis

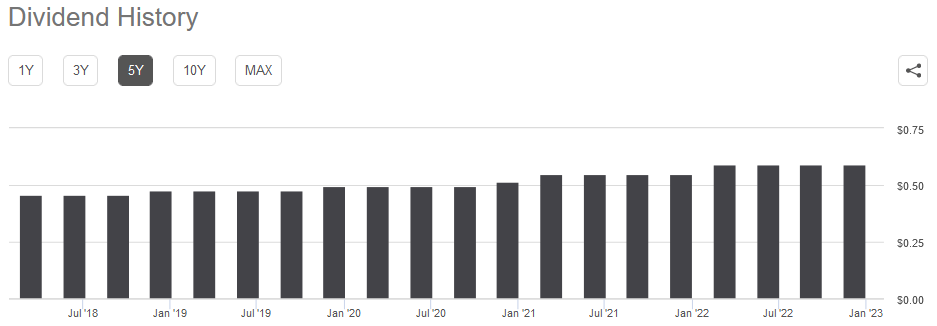

As stated in the introduction, one of the reasons why investors purchase shares of utility companies like Ameren Corporation is because of the fairly high dividend yields that they tend to possess. Admittedly, Ameren’s yield of 2.60% is not nearly as high as some other utilities but it still beats the 1.60% yield of the S&P 500 Index (SP500). Perhaps more importantly, Ameren Corporation has a long history of increasing its dividend on an annual basis:

{kind=link}

The fact that the company normally increases its dividend in conjunction with its fourth-quarter results means that we can likely expect a dividend increase in a few weeks. This means that the yield-on-cost will be quite a bit more than 2.60% in very short order for someone that buys the company’s stock today. In addition to this, the fact that the company consistently increases its dividend is nice during inflationary times such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it seem that we are getting poorer and poorer with each passing year. The fact that the company increases the amount of money that it pays us each year helps to offset this effect and maintains the purchasing power of the dividend that we receive.

As is always the case though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to find ourselves the bag-holders of a dividend cut, since that would both reduce our incomes and almost certainly cause the share price to decline.

The usual way that we judge a company’s ability to maintain its dividend is by looking at its free cash flow. The free cash flow is the amount of money that is generated by a company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that is available to do things that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the third quarter of 2022, Ameren Corporation reported a negative levered free cash flow of $486.3 million. This is obviously not enough to pay any dividend but the company still paid $152.0 million to its investors. This is something that certainly may appear concerning at first glance.

However, it is not unusual for a utility to finance its capital expenditures through the issuance of equity and especially debt. The company will then pay its dividend out of its operating cash flow. This is due to the incredibly high expenses involved in constructing and maintaining utility-grade infrastructure across a wide geographic area. During the third quarter of 2022, Ameren Corporation reported an operating cash flow of $727.0 million. This was more than enough to cover the $152.0 million in dividends that it paid out and still leave it with a substantial amount of money left over. Overall, it appears that Ameren is having no particular difficulty maintaining its dividend.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like Ameren Corporation, one metric that we can use to value it is the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few companies that have such a low ratio today, particularly in the slow-growing utility sector. Thus, the best way to utilize this ratio is to compare Ameren’s valuation to that of its peers and see which firm offers the most attractive relative valuation.

According to Zacks Investment Research , Ameren Corporation will grow its earnings per share at a 6.86% rate over the next three to five years. This is within the 6% to 8% range that we projected earlier based on the company’s rate base growth and it is also in line with the 6.06% year-over-year growth rate that the company reported in the most recent quarter. Thus, the Zacks estimate seems pretty reasonable. This gives Ameren Corporation a price-to-earnings growth ratio of 3.03 at the current price, which is a bit higher than the 2.99 ratio that the stock had when we last looked at it back in July. Here is how Ameren Corporation compares to its peers:

| Company |

| PEG Ratio |

| Ameren Corporation |

| 3.03 |

| DTE Energy |

| 3.21 |

| Public Service Enterprise Group |

| 5.58 |

| Eversource Energy |

| 3.01 |

| Entergy Corporation |

| 2.69 |

| CMS Energy |

| 2.56 |

Ameren Corporation’s valuation compares to its peers in a similar way to the last time that we looked at the company. The big surprise here is that Eversource Energy now appears to be a bit cheaper than Ameren despite previously being much more expensive. That may have to do with that company considering getting out of the offshore wind business, which is a bit of a disappointment for those investors that are interested in renewables. Entergy and CMS Energy are also both substantially cheaper than Ameren, but both of those companies have significantly higher leverage, as we saw earlier. As higher debt corresponds with higher risk, Entergy and CMS Energy are cheaper for a reason.

Overall, Ameren Corporation appears to be offering a very good balance between risk and reward here and its valuation looks fairly attractive in that light. It may therefore be worth considering for a portion of your investment dollars.

Conclusion

In conclusion, Ameren Corporation is a somewhat sleepy electric and natural gas utility that still appears capable of greatly rewarding its investors. The company is positioned to deliver an attractive 9% to 11% total annual return over the next few years and will likely increase its dividend in a few weeks. The company also sports a very attractive balance sheet and a reasonable valuation. Overall, Ameren Corporation might be worth considering today.

For further details see:

Ameren: Electric Utility Offers A Very Attractive Investment Proposition Today