AMRC - Ameresco: Capital-Hungry Business Throwing Off No Cash Flow To Shareholders

2023-11-29 03:05:41 ET

Summary

- Ameresco is facing difficulties in the renewable energy sector due to high rates, inflation, and construction slowdowns.

- The company's revenue model is lumpy and lacks returns on capital or free cash flow for future growth.

- AMRC's stock is not recommended for the long account in my opinion, due to its capital-hungry business model and no FCF per share.

Investment brief

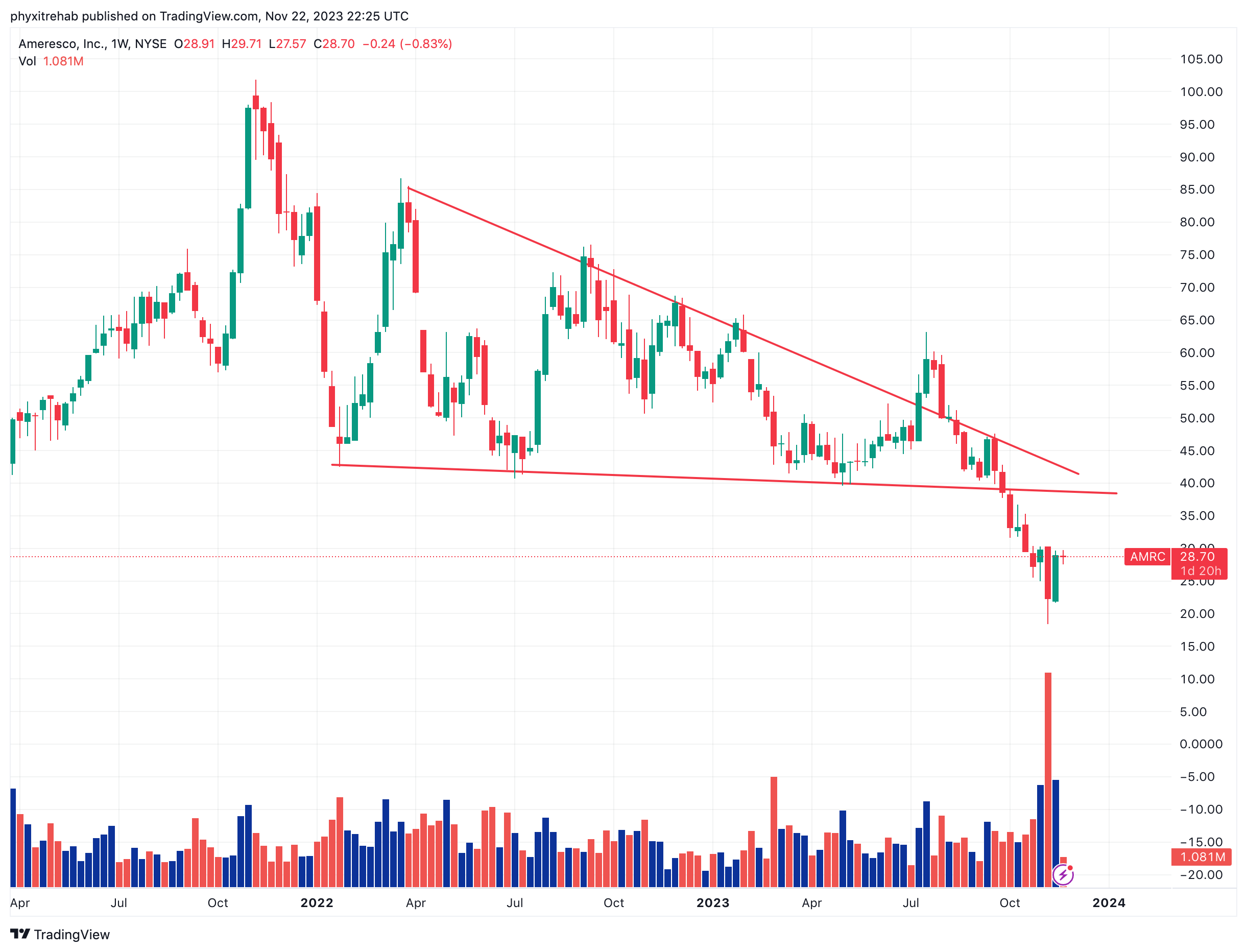

Persistently high rates, sticky inflation, and a slowdown in construction rates aren't the pillars of growth for the renewable energy sector. That in mind, it isn't surprising that investors continue to forecast a period of difficult business for Ameresco ( AMRC ) with its stock price nudging 52-week lows within the last month of trade (Figure 1). The company, that develops renewable energy projects to help companies transition to alternative energy sources, has a noble business model. But in my opinion, revenues are lumpy, and vary in size + nature. For instance, the top-line split is 1) project revenue, 2) energy assets, 3) O&M revenue, and 4) other. Per the 10-Q:

[R]evenues are derived principally from energy efficiency projects, which entail the design, engineering, and installation of equipment and other measures that incorporate a range of innovative technology and techniques to improve the efficiency and control the operation of a facility’s energy infrastructure;

this can include designing and constructing a central plant or cogeneration system for a customer providing power, heat and/or cooling to a building, or other small-scale plant that produces electricity, gas, heat or cooling from renewable sources of energy."

Following the extensive analysis presented here today investment in the company's stock is not recommended in my opinion. AMRC's ability to compound intrinsic value is hindered by:

(1). Capital hungry business model with no returns on capital or free cash flow to finance future growth,

(2). Macroeconomic environment (tight money, inflation, etc.,) forcing asset sales to maintain competitive position.

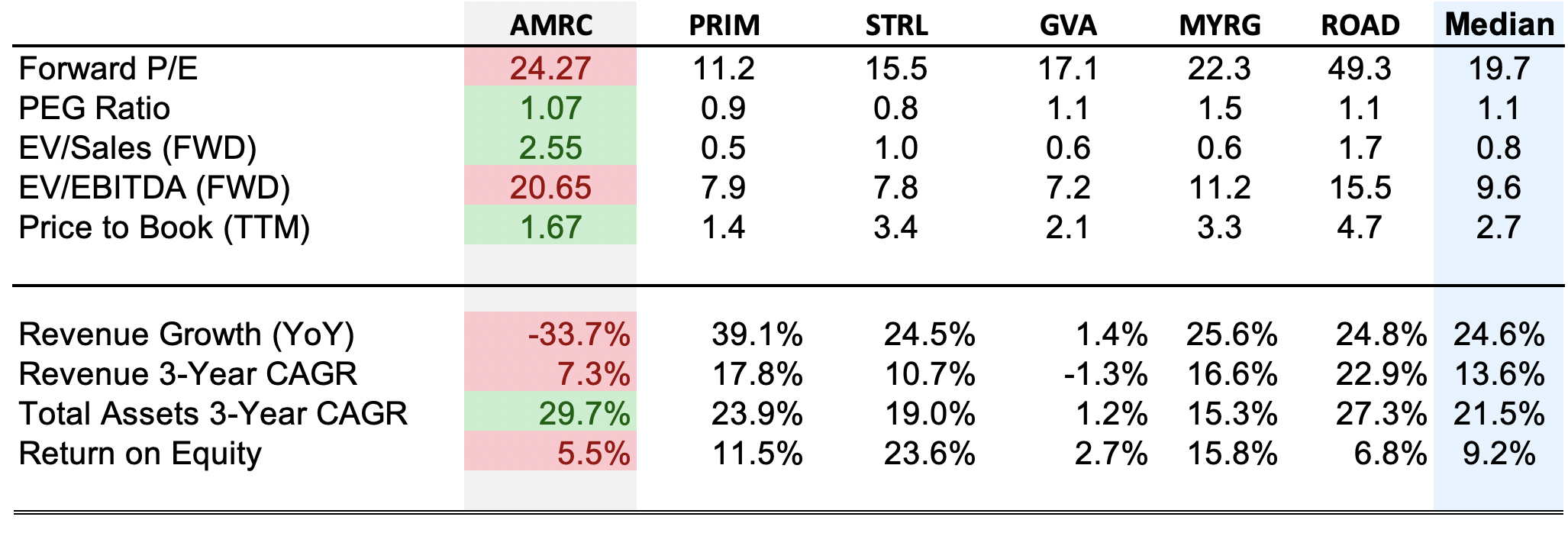

AMRC's offering does not differentiate on product or cost, and so far the ratio on profits to capital in the business has languished. Investors are asked to pay a 1.6x premium to book value, but for just 5.6% trailing rate of return on that equity.

In my opinion, these factors don't stack up. When you compare AMRC vs peers in comparative statistics, the company is priced below peers. But it lags in quality measures too. With 30% CAGR asset growth in 3 years, one would expect to see positive sales growth and a higher ROE.

With the company still priced at 24x forward earnings, my investment cortex is shouting to avoid this one, even, with such a sharp selloff. Net-net, I rate AMRC a hold for factors raised here in this report.

Figure 1.

{kind=link}

Figure 1a.

Source: BIG Insights, Seeking Alpha

{kind=link}

Critical investment facts supporting the hold thesis

On examination, the very nature of the company's revenue model broadens the distribution of potential outcomes compared to other industries. There are two obvious headwinds that lead to the one outcome—there's no cash falling through. Namely:

(1). Delays / backlogs:

This is an industry notorious for delays in produced work for factors beyond control. Given (i) the current state of construction markets, (ii) macroeconomic pressures, (iii) overspill of supply chain backups, and (iii) weather, the rate of project completion is slow.

For ARMC, its customers are taking longer to start work, causing a puddle of awarded projects not converted. Supply chain issues also persist, in getting its hands on more complex components. Whereas it would have taken 1–2 years on schedule, the company is looking as long as 3 years completion on a $100mm sized project.

(2). Capital intensity + economic value:

One of the major problems in energy markets that renewables has failed to solve is the issue of returns on invested capital. This is a capital-hungry industry with high reinvestment needs. Providers of capital to the company (creditors, equity holders) expect to see a return on their assets employed to run the business. Profits should therefore be assessed against the capital employed to generate them. A high ratio of profits to capital invested means the company:

- Produces cash flow that can be reinvested for growth and remain competitive,

- Can commit cash to growth, without jeopardising owner earnings/FCF, and vice versa (throw off cash to investors without hurting growth).

- This way, corporations can reinvest cash flows into growing the enterprise, 1) increasing FCF per share, and 2) compounding shareholder wealth.

Energy markets in general are challenging because there is no differentiation on product (energy) or price (set by the market). Profits are low relative to assets. Some low-cost producers survive on efficiency. The ancillary operators, like AMRC, offer unique exposure to market segments, however often run into the same troubles, with (i) no returns on capital, and (ii) no free cash flow to stay competitive.

AMRC has not been FCF positive since 2020, and only produced $80mm since 2019. It is particularly susceptible because:

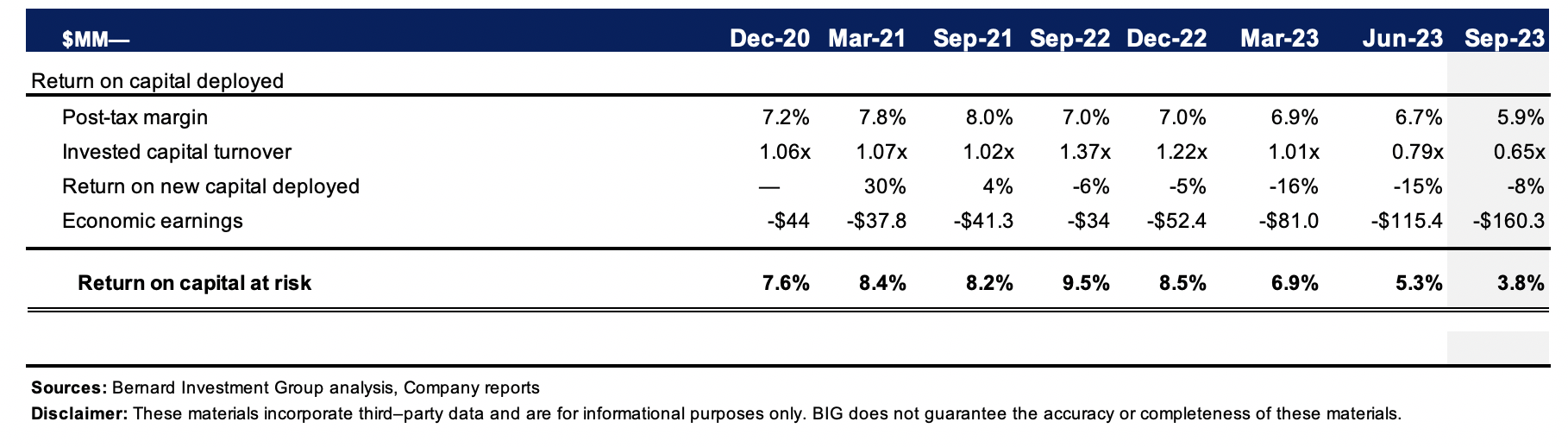

- The company's post-tax margins are thin, <9% on average and 5.9% last quarter (Figure 2). Any slowdown in business will suffocate earnings growth in my opinion. This is interesting. You would expect to see AMRC outperforming at the margins if the market liked its offerings. Many other players in the renewables value chain do have high relative margins in my experience. For AMRC, it appears there is no consumer advantage, and no cost differentiation.

- Pace of sales produced on investments is slow. Capital turnover is trending lower, at 0.65x last quarter from highs of 1.37x in 2022. Clear indication the investments made in the business aren't yet productive, a reflection of the delays and longer cycles.

Figure 2. There is no consumer advantage, and no cost differentiation

{kind=link}

To me this is critical. It suggests (1) the company's pace of sales is slowing, at (2) lower margins. To justify a 20-24x multiple I would expect to see at least one of these two creeping higher, so there is a dislocation in price to value in this regard.

(3). Shareholder value taking its time

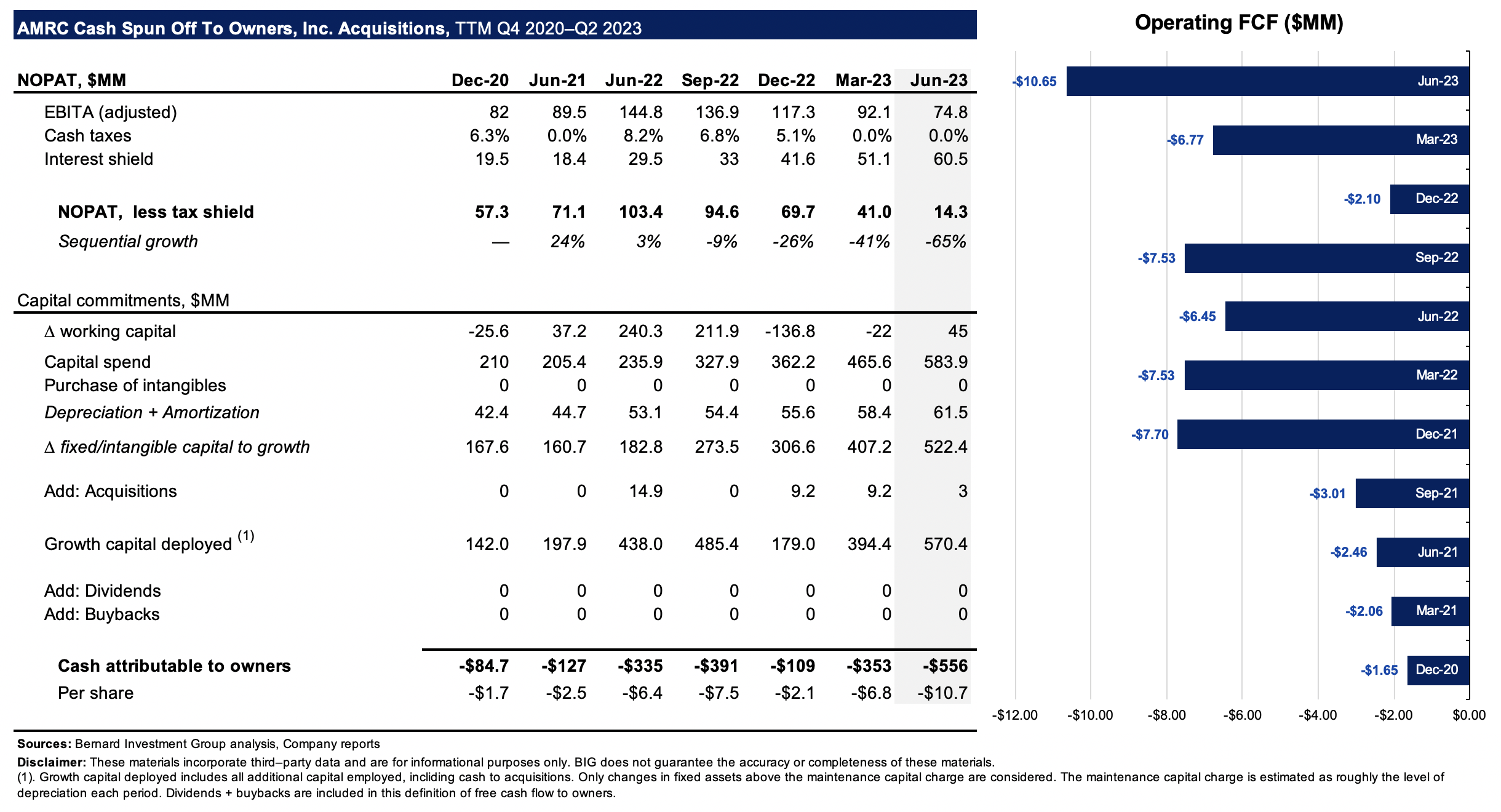

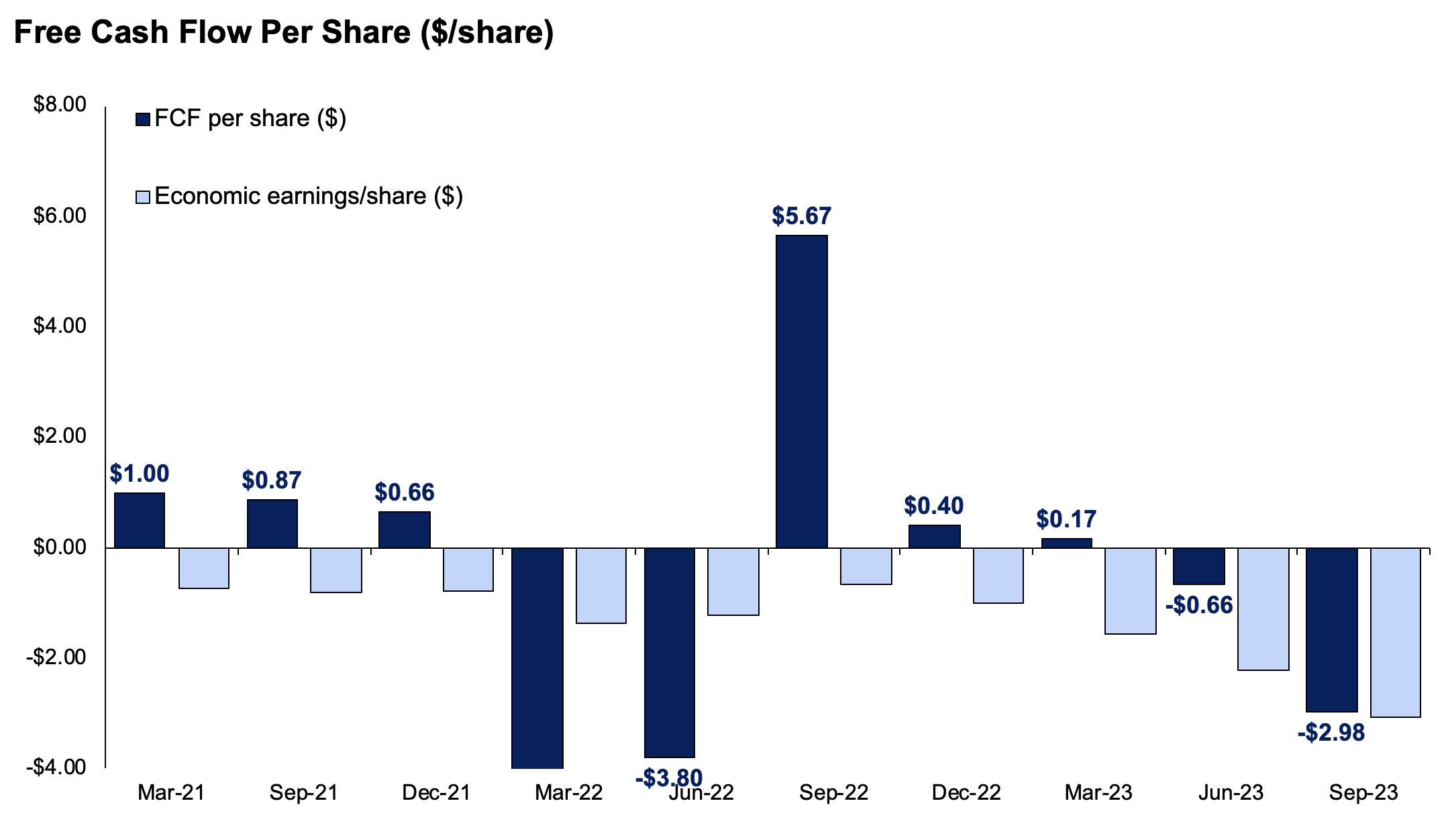

More direct value should be seen as well. A nuanced breakdown of AMRC's free cash flow to equity seen in Figure 3. It is calculated as net operating profit, less cash taxes and the interest shield, less investments made for growth. Only investment above the maintenance capital charge is considered to be an investment for growth. The maintenance capital charge is approximated as the level of rolling depreciation (note: all figures on rolling TTM basis) .

Three critical observations standout:

- Earnings produced on AMRC's capital are trending lower—$14.3mm last period vs. highs of $103mm in 2021,

- AMRC is investing heavily to growth initiatives: $142mm in 2020, up to $570mm in Q3 2023,

- FCFE outflows have been deepening for the last 3 years, to $556mm in the last 12 months.

The company has $108mm in cash on hand, around $1Bn in liquid assets when factoring in receivables and so forth. But there is no uncertainty it won't raise additional cash, by what route, nor at what valuation. This is critical information to consider. How this looks for investors in FCF per share, and economic losses per quarter, is seen in Figure 4.

Figure 3.

{kind=link}

Figure 4.

Source: BIG Insights, Company reports

{kind=link}

Q3 earnings insights

Much of what's been described above was on show in the company's Q3 numbers.

According to the CEO, " We are very disappointed". What stood out for me was management's language on capital and asset management going forward. It said it " will look to sell assets"; acknowledging the difficulty of such a high capital intensity, low productivity/profitability scenario. It continued:

[W]ith higher interest rates, we're starting to see a little bit of challenge in the levered IRR targets that we have. And as you know, some of these assets take a while to sort of make their way through the asset and development metric into something that's in operation."

Given the company's investments haven't yielded adequate returns or cash flows (as discussed), this might be a sensible move.

The company also lowered its FY'23 guidance. It calls for revenues of $1.35Bn vs. $1.55Bn previous, adj. EBITDA of $165mm vs. $220mm and earnings of $1.20/share, well behind the $1.90 forecast in Q2. It expects to place 120–130MWe of energy assets in service, higher than the previous forecast of 80–100MWe.

As to the quarter, takeouts were balanced. They include the following:

Positives—

- Record backlog: Ended the quarter with a record total project backlog of $3.7Bn. Sequential increase of 14%, and a notable 41% increase compared to last year. Need to question this is demand-driven, or a function of poor efficiency.

- Pipeline robust: Added $700mm in new project awards during the quarter. YTD awards stand at $1.7Bn, more than double the previous year's level. All of this is supported by a 35% increase in proposal activity.

- Operating energy asset visibility: Operating energy asset visibility is approximately $2.3Bn. Represents both contracted revenue and a conservative estimate of lifetime uncontracted R&G revenues.

- Asset development and construction: Added >50MWe of assets in development in Q3. Ended the quarter with c.600MWe of assets in development and construction. Reflects a 30% increase from the 460Mwe at the end of previous year.

The company says these metrics give it visibility to over $7.2Bn of future revenue, which could be a tailwind. Question remains—when.

Negatives—

- Financials: Q3 revenues came to $335mm and fell short of projections, influenced by 1) project delays and 2) asset downtime. It booked adj. EBITDA of $43.3mm for the quarter. Despite challenges, energy asset revenue grew by 6%, propelled by an expanded portfolio of operational assets. The O&M business sustained a consistent quarter, realizing a 4% growth. The company is highly leveraged, at 8.3x debt-to-EBITDA. Likely a function of its poor economics and ability to produce cash flows on investments. With the new guidance, management projects the leverage ratio for 2024 to hover around 8x.

- Extended timelines are chocking cash flow. As mentioned earlier, the business hasn't generated free cash flow since 2020. It is facing added pressure as conversion of awarded projects into contracted backlog faces extended cycles. Customers aren't keeping to schedule, or implementing directives on time. So as mentioned, traditional construction schedules have elongated, and current assessments indicate construction periods exceeding 1.5 to almost 3 years.

- Energy asset downtimes. Its energy asset business faced difficulties in Q3. First, from downtime at select biogas plants, and second from delays in developing larger, intricate plants. Management's language on this is optimistic, but might need to be kept front of mind:

Where assets always incurred downtime and the levels we have faced over the last few quarters have been considerably greater than budgeted.

it's important to keep in mind that all of these profitable assets will be built. It's just taking longer than originally anticipated."

As mentioned, performance was balanced, with nothing remarkable on either side of the investment debate.

Valuation and conclusion

The intelligent investor simply cannot walk past the three major economic factors eroding AMRC's corporate value:

(1). No cash flow producing assets to finance growth and FCF per share,

(2). Minimal earnings compared to assets/capital employed in the business,

(3). Capital hungry economics that require all profits to be re-consumed to maintain any competitive position, rather than distribute for growth.

With those in mind, you're paying 24x forward earnings and 39x forward EBIT to buy AMRC today, and receiving an 8.5% cash flow yield for doing so (plus all the downside factors outlined). The company's growth outlook does not sport these kind of valuations either.

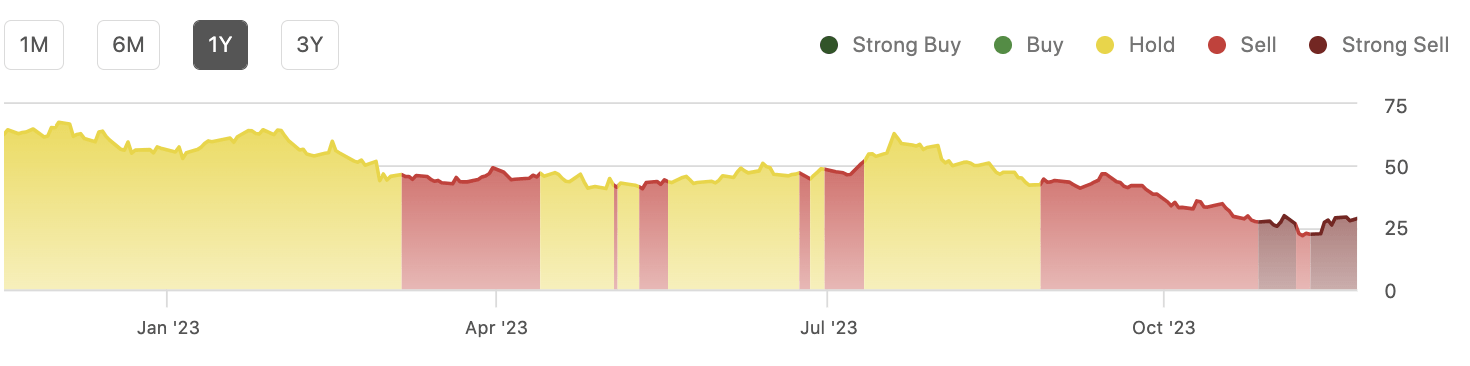

I can't wrap my head around AMRC trading at 40% and 155% premium to the sector respectively. The company does trade at 1.6x book value, but that is likely because you have poorly valued assets underneath the market value. My estimate is the company should trade closer to the sector median of 17x EBIT. I would also note to investors the quant system rates AMRC a sell, using a blend of objective factors in one composite. I would urge all to consider this in their reasoning as well.

{kind=link}

In short, after extensive analysis, my judgement on AMRC is there are more selective opportunities elsewhere. The market has done a fair job in pricing the company's outlook in my opinion. Soft business economics with a no growth, no cash flow duet is not something for my investment palate. With all facts raised here today, I rate AMRC a hold.

For further details see:

Ameresco: Capital-Hungry Business Throwing Off No Cash Flow To Shareholders