SFM - American Assets Trust: A Quality REIT You May Want To Consider For The Back To Office Recovery

2024-01-17 13:00:00 ET

Summary

- American Assets Trust owns high-quality real estate in the San Diego area and other West Coast states like Washington and Oregon.

- AAT has faced challenges due to the COVID-19 pandemic, particularly in the office and multi-family sectors.

- Despite these challenges, AAT has remained resilient, raised its full-year guidance twice during the fiscal-year, and has a strong balance sheet.

- The REIT has traded as high as 20x FFO and could see a significant price increase if interest rates fall and businesses require workers back in the office.

- They also continue to focus on deleveraging its balance sheet, and expects to target a net-debt-to EBIDTA range of 5.5x in the foreseeable future.

Introduction

Last weekend I took a quick local trip here in the San Diego area and decided to stop off at a shopping center in Solana Beach, an upscale area north of the city. It contained a couple well-known stores like Sprouts Farmers Market ( SFM ), Marshalls, CVS Pharmacy ( CVS ), and Starbucks ( SBUX ).

I instantly looked up what REIT owned the shopping center, only to find out it was owned by American Assets Trust ( AAT ), a company I wasn't familiar with that owns a lot of the high-quality real estate here in San Diego area.

I was impressed by their growth and decided to delve deeper into the company, prompting this analysis. And in this article I discuss why this REIT may be a good play for long-term dividend investors willing to wait for the back-to-office recovery and lower interest rates.

Who Is AAT?

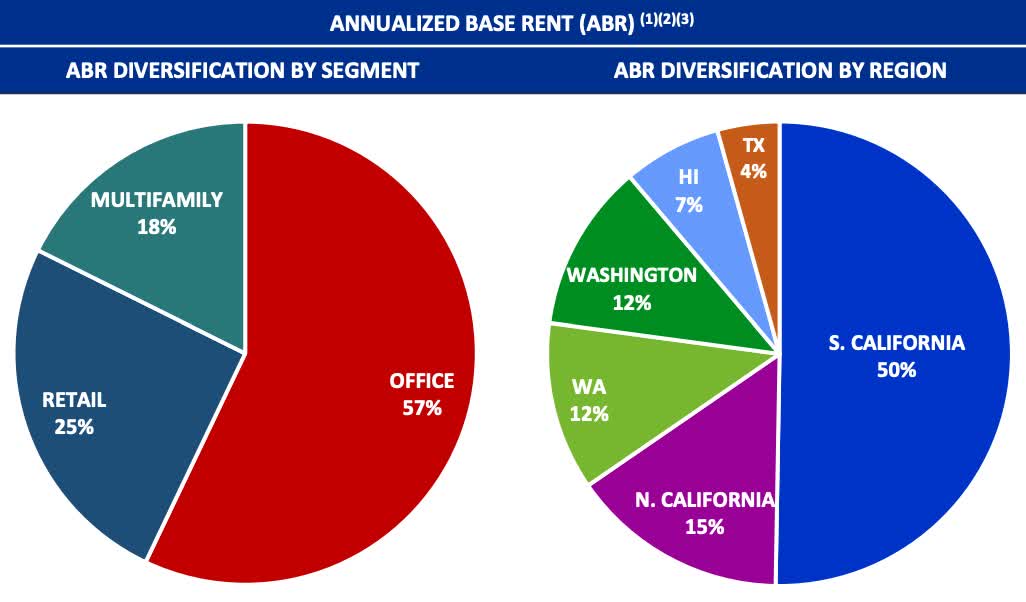

Despite being new to me, the REIT has actually been around for over a half of century and is headquartered here in San Diego. They own a lot of high quality real estate in high barrier to entry markets in Southern & Northern California, Washington, and Oregon. Most of their properties are here on the West Coast with the exception of properties in Texas and Hawaii. But a bulk of their properties are right here in the San Diego area, the country's most expensive city to live in.

They also own a well-known area in Honolulu, Hawaii, the Waikiki Beach Walk, a hotel and mixed-use retail center. I would visit the place almost every weekend when I was stationed on the island. It is a very touristy destination that attracts consumers because of its location between upscale shopping and the beaches. It also has a lot of popular restaurants nearby as well. Although the company is on the smaller side, the quality of their real estate is top notch.

Headwinds

Let's get down to business. Although the REIT sector has experienced quite a bit of volatility in lieu of rising interest rates, AAT has been down over the past few years. The main reason for this was the COVID-19 pandemic. And even though it started nearly 4 years ago, the REIT still has not recovered. And honestly it may take some time before they do.

But that doesn't mean it's a bad REIT. I actually think they're pretty solid and have held up well despite challenges. American Assets Trust has proved to be resilient, a testament to their management team as well.

But if you look back further than the last year, you'll see AAT is still in the red. In February the company was trading near $50 before the pandemic and has yet to recover.

One reason is the hybrid work from home schedule that many businesses have seemed to adopt. And with AAT deriving 57% of their annualized base rent from office properties, you can see why the share price has declined.

{kind=link}

But there does seem to be a glimmer of hope for REITs in the office sector. During Q3 earnings their COO addressed this:

Briefly on the office utilization front, a study by Resume Builder showed that 90% of companies plan to implement a return to office policies within the next 12 to 14 months with a meaningful amount of those companies also stating that they would threaten to terminate employees that don't comply. This, of course, comes as more and more CEOs contend that employee collaboration, engagement, mentorship, and productivity are clearly suffering without in-office presence.

If this happens and businesses mandate employees back into the office, then REITs like AAT will benefit. I can't say when but I do think in the next year or two office properties will be likely back to normal operations for most businesses. At the end of Q3 the office portfolio was 86.6% leased, down from 95% pre-pandemic. This is also down from 96% year-over-year. But management is very aware of office trends and expects this to tick up as more people go back to work in office.

AAT faced headwinds in their multi-family portfolio as well with vacancies and decelerating rent growth. But the REIT saw vacancies decline in the quarter with the return of college students. Furthermore, the decelerating rent growth was due to applicants not meeting their income and credit requirements. As I previously mentioned, San Diego is the most expensive city to live in and requires a substantial amount of income to live comfortably.

And with the city having a large number of college students, I can see why the REIT saw a decline. Especially with American credit card debt reaching an all-time high during the third quarter. Then there's also the general economic stress on consumers as well. But net effective rents for the multi-family leases are up 9% year-over-year.

Resilient Financials

The huge thing that stood out to me about American Assets Trust was despite the headwinds and challenges, the REIT has remained resilient, even raising full-year guidance twice! Once in the first quarter and again in Q3.

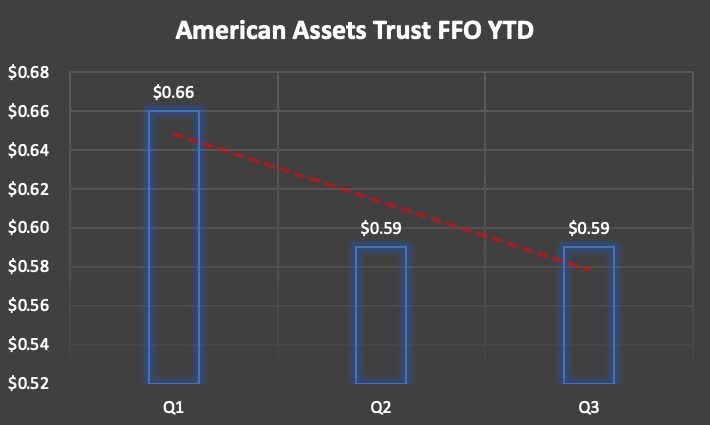

Management now expects FFO in a range of $2.36 to $2.40, up from $2.23 to $2.33. In the chart below, despite a decline from Q1 and FFO flat in the latest quarter, they comfortably out-earned their dividend of $0.33.

{kind=link}

Since Q1, FFO has declined over 10% but is fairly impressive considering the percentage of ABR the REIT collects from office properties and the economic environment. YTD, AAT has brought in FFO of a $1.84. Using their full-year guidance, I think it's safe to say Q4's FFO will be a minimum of $0.52. The consensus estimate is $0.55 although I expect FFO in a range of $0.55 to $0.62.

Revenue has impressively increased quarter-over-quarter growing from $107.75 million to $111.2 million in the third quarter. So, despite FFO being flat, revenue has continued to climb more than 3% in the first 9 months. AAT is a small, but mighty REIT with an experienced management team. And I expect them to continue marching forward.

Furthermore, since the pandemic when AAT was forced to cut the dividend temporarily, the REIT quickly got back to business and has not only recovered, but grown the dividend since then from $0.20 to their current. And this is well-covered by a conservative, low payout ratio of roughly 56%. So, the company has ample room to continue growing their dividend for the foreseeable future.

Strong Balance Sheet

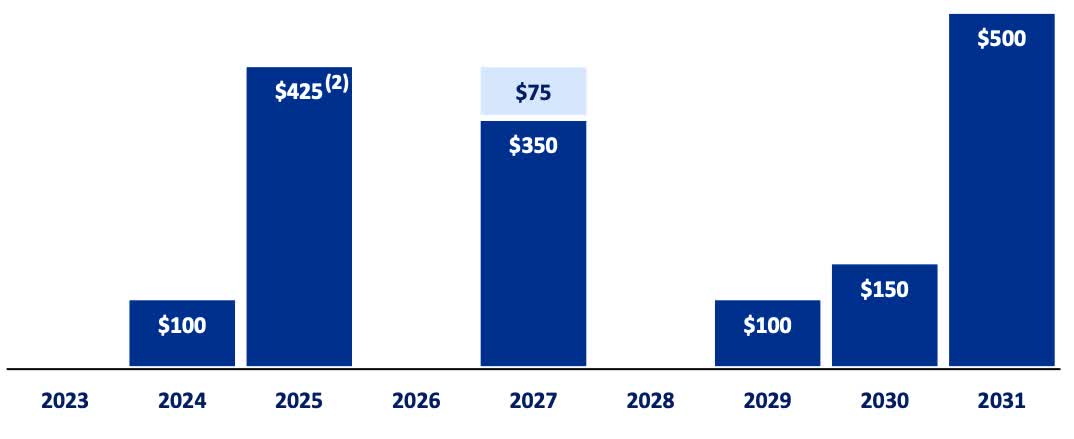

AAT does sport investment-grade ratings from all three major agencies with a BBB- from S&P. Their debt maturities are also well-laddered with only $100 million due this upcoming July. They do, however, have a substantial amount due next year with $425 million, in which the company anticipates refinancing.

{kind=link}

AAT had $490 million of available liquidity on its balance sheet with $90 million in cash & cash equivalents. One thing I would like to see from the company is them lower their net-debt-to EBITDA ratio of 6.6x. Although REITs use debt to fund growth due to the business model, I typically like to see this in a range of 5.5x or lower.

A ratio below 5x is even better. One reason why I like Agree Realty ( ADC ) so much is the company's fortress balance sheet and net-debt-to EBITDA ratio of just 4.5x. Before the pandemic in 2020, their net-debt-to EBIDTA was 5.6x and AAT's management addressed this during their latest earnings stating they planned to get back to this level targeting a range of 5.5x or better in the near future. This is something I will be keeping a close eye on in the coming quarters.

Is It A Buy, Hold, Or Sell?

Because of the headwinds from the economic environment and the office properties the REIT holds in its portfolio, the stock is currently undervalued in comparison to their 5-year average P/FFO ratio of 18.7x. Over the years the stock has traded more than 20x FFO. Additionally, their forward P/AFFO ratio of 14.15x is currently below the sector median and they currently have a price-to-book ratio of 1.2x.

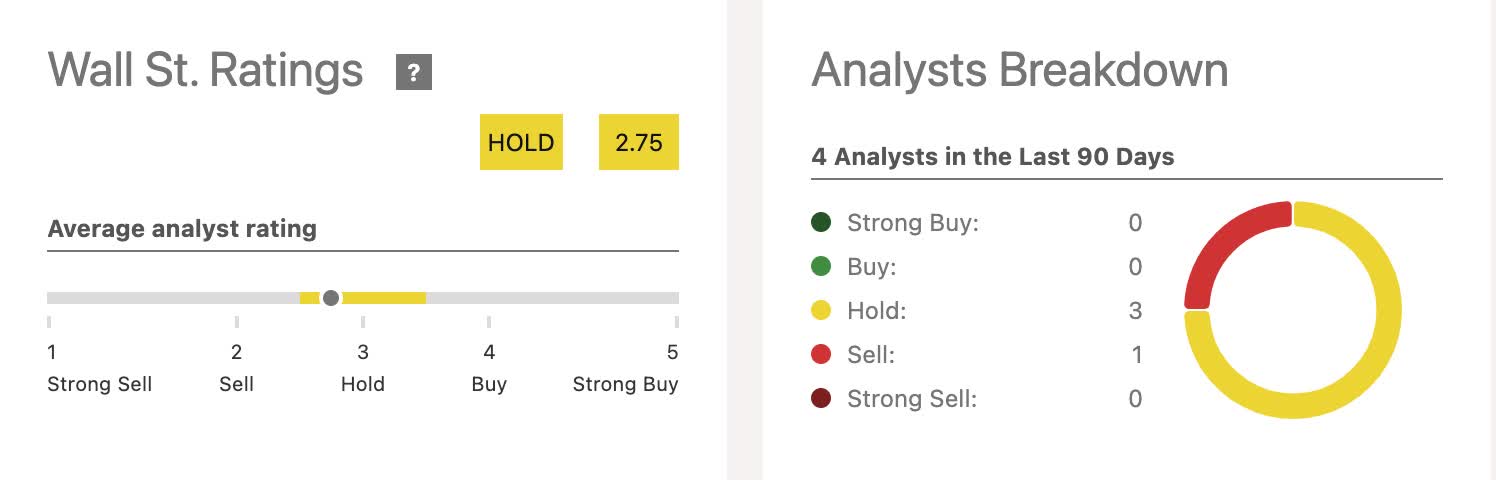

So, if you believe in the office property recovery and have a positive long-term outlook for the sector, then AAT may be a potential great long-term buy while you wait. Seeing how high they've traded in the past, this shows the stock's share price potentially has significant room to grow. However, Wall Street currently rates the stock a hold with a price target of $21.67.

{kind=link}

I think this is due to the uncertainty of the hybrid work environment. Although it is said businesses are going to require people back into the office, some are saying the hybrid environment is here to stay. Either way it will be a tough road ahead and the sector will likely not see a full recovery for the next year or two, if ever.

Risk Factors

Most readers know higher interest rates are not good for the REIT business model due to the significant amount of debt required to fund growth. And while I do think rates will decline this year, this will continue to plague AAT as well, on top of everything else the company is facing.

A risk of a recession would also hurt the company as they are currently battling vacancies. Even with their proved resilience, a recession would likely cause an uptick in vacancies as unemployment rates rise. Especially with a lot of their properties in nicer areas, this would only cause further tighter consumer spending as they look to cut costs.

With that, the multi-family segment would likely suffer the most. In Q3, occupancy rebounded from 70% in the second quarter to approximately 90% in Q3, but this could see a reversal in the wake of a recession.

Bottom Line

American Assets Trust is a smaller cap REIT that focuses on high-quality real estate in the Western part of the U.S. Despite headwinds in the sector ( VNQ ) and most of their revenue deriving from office properties, AAT has proven to be quite resilient in spite of an economic downturn and uncertainty on the office outlook.

They also managed to grow revenue, and although FFO declined from Q1, it has been steady over the last 2 quarters. Additionally, management raised guidance twice this year, further showing they're well-equipped to handle headwinds with precision. Even with a cut during COVID, the REIT quickly got back to growth and is comfortably out-earning the dividend with a very safe payout ratio of nearly 56%.

Furthermore, AAT has an investment-grade balance sheet with well-staggered debt maturities. Although I would like to see a lower net-debt-to EBITDA ratio, management is focused on deleveraging its balance sheet, bringing this down to a more comfortable range of 5.5x or lower. While the outlook for the normal back to work environment is cloudy and the REIT may face additional headwinds if we enter a recession, I think this lesser-known small cap REIT is a speculative buy.

For further details see:

American Assets Trust: A Quality REIT You May Want To Consider For The Back To Office Recovery