AXL - American Axle & Manufacturing Holdings: Unconvincing EV Transition

2023-10-26 21:26:15 ET

Summary

- AXL’s revenue has grown at a CAGR of 7%, although this does not reflect its decline in commercial relevance. The business is set to suffer from the EV transition.

- AXL’s margins have declined, owing to competitive pressures and supply-side concerns. We struggle to see the company returning to its pre-pandemic levels.

- AXL quarterly performance has been reasonable thus far, although we suspect a slowdown is ahead, driven by a sequential fall in light vehicle production growth.

- When compared to its peers, AXL’s performance is disappointing, with significantly lower growth and weaker commercial development.

- AXL’s valuation appears attractive, particularly its FCF, but when contextualized we are far from convinced. We still see scope for downside in the coming quarters.

Investment thesis

Our current investment thesis is:

- AXL’s commercial positioning is a major concern, primarily due to the expectation of a material shift in automotive production toward EVs in the coming decade. We suspect AXL’s growth will slowly grind to a halt, as we experience a “cross-over” in the coming years between LVP and EV production.

- Even if AXL is able to sufficiently transition its business model, we are not convinced by the current state of the business. Its balance sheet is bloated and requires continued deleveraging, restricting its ability to reinvest in innovation. Further, its organic growth rate, even beyond the production impact, appears mild. Investors seeking exposure to automotive parts may be better placed with others.

Company description

American Axle & Manufacturing Holdings, Inc. ( AXL ) is a leading global automotive supplier that designs, engineers, and manufactures driveline and metal forming technologies for automotive, commercial, and industrial markets. With headquarters in Detroit, Michigan, AXL operates across multiple continents, serving a diverse range of customers in the automotive industry.

Share price

AXL’s share price performance has been disappointing, losing over 60% of its value while the S&P 500 has made impressive gains. This is a reflection of the company’s declining financial performance and industry headwinds.

Financial analysis

{kind=link}

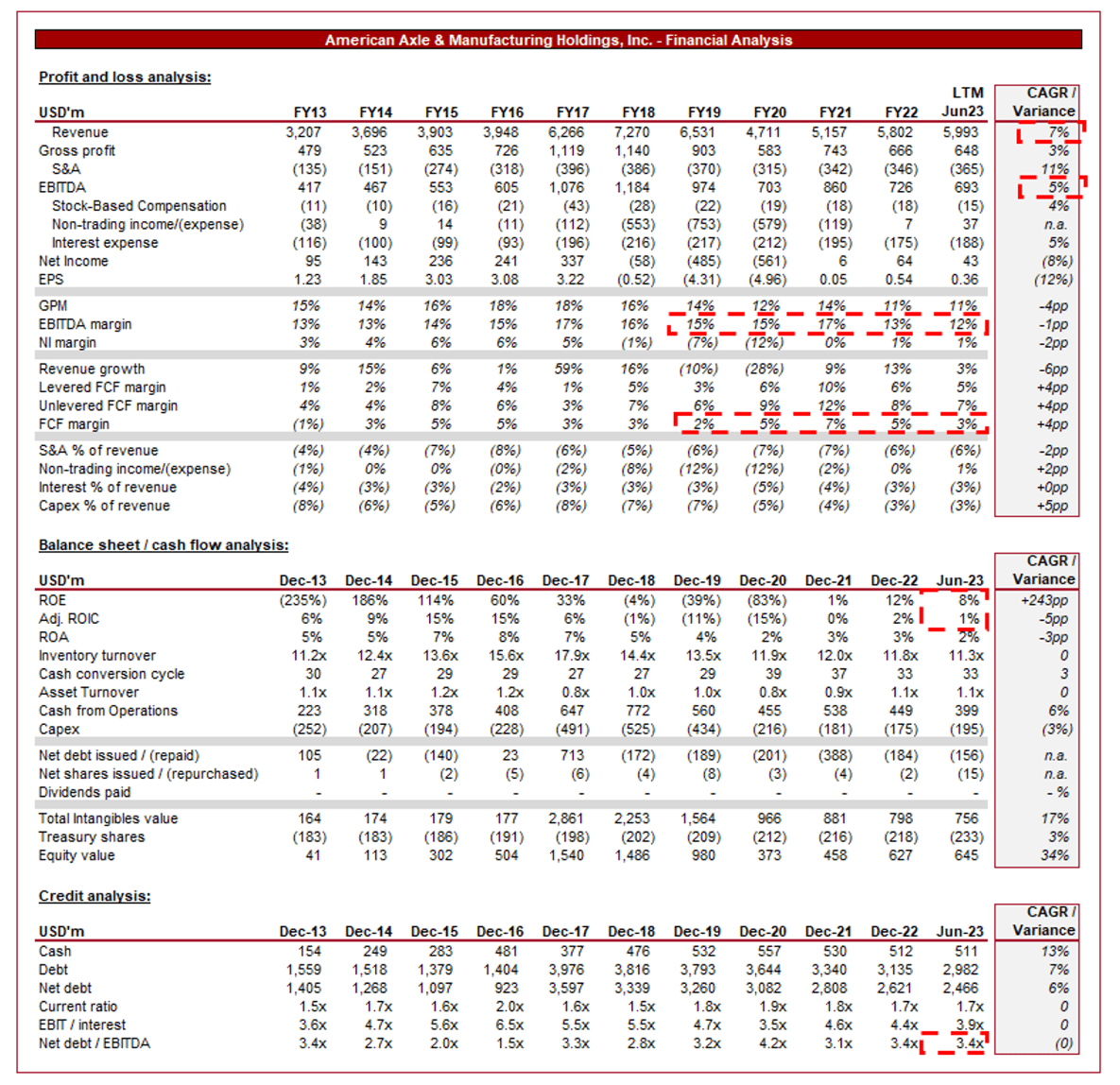

Presented above are AXL's financial results.

Revenue & Commercial Factors

AXL’s revenue development has been disappointing despite the +7% CAGR on the top line, primarily due to minimal organic growth and heavy weighting toward the acquisition of MPG .

Business Model

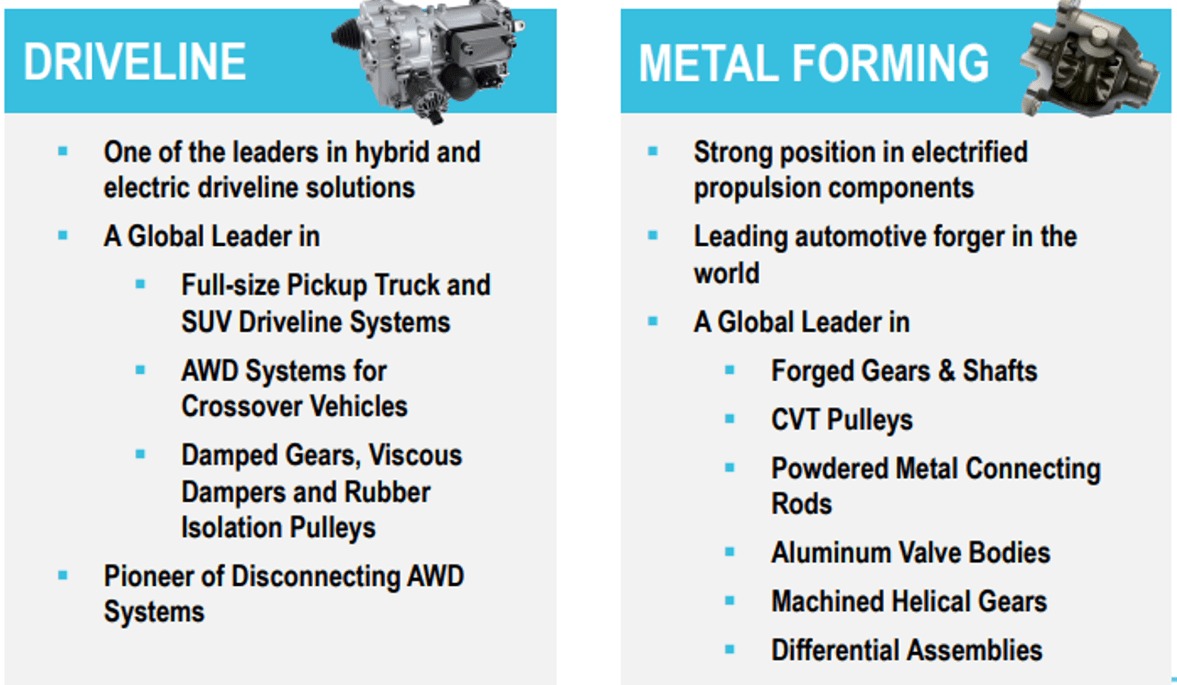

AXL manufactures a broad range of driveline and drivetrain systems, including axles and power transfer units, catering to various vehicle types, including SUVs, trucks, electric vehicles, and commercial vehicles. It collaborates closely with automotive manufacturers during the design and development phase, creating tailored and scalable solutions. Additionally, AXL provides aftermarket services, including replacement parts. This additional revenue stream enhances customer satisfaction and loyalty, while boosting its non-cyclical revenue capabilities.

The company has developed a strong reputation within the market globally, owing to its market-leading products that in many cases are noticeably superior to its peers’ alternatives. This has allowed AXL to create relationships with several leading OEMs globally.

Products (AXL)

{kind=link}

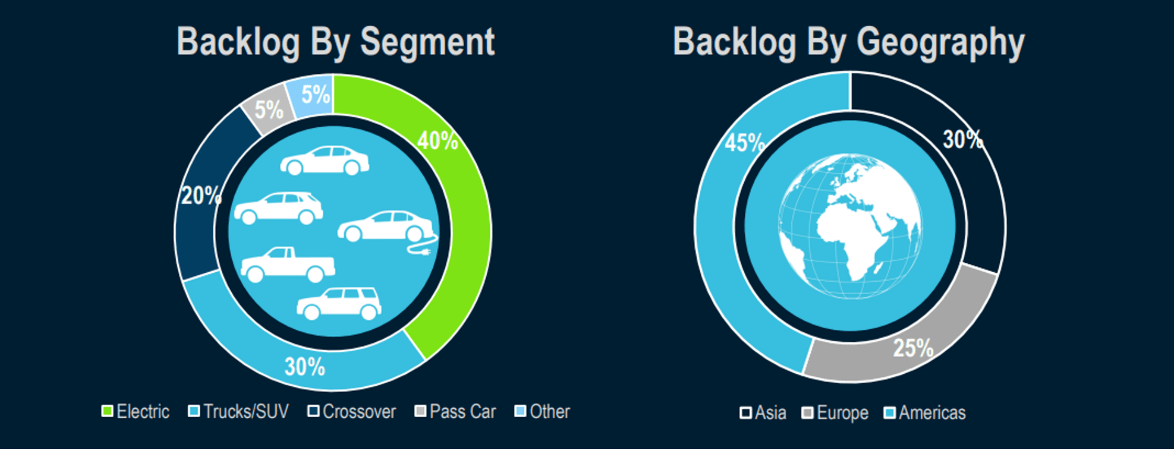

AXL operates manufacturing facilities and engineering centers globally, allowing it to efficiently serve clients across all key regions by adapting to local demands and regulations. When assessed by Backlog, the company’s business by region is broadly equal between Asia, Europe, and the Americas. This is a reflection of its market-leading technology in the traditional ICE-powered market. Most recently, the company has own multiple contracts with OEMs in Europe and China.

Backlog (AXL)

{kind=link}

AXL has invested significantly in R&D (which is one of the reasons for its margin erosion), with a current focus on innovative technologies in the EV space, such as electric driveline systems and lightweight materials. AXL is committed to lightweight components and electric driveline systems, contributing to the fuel-efficient objectives of OEMs. This is a critical requirement for the business in order to ensure it stays competitive in the evolving automotive industry that appears to be undergoing an unstoppable transition to electric only.

We are currently unconvinced by AXL’s transition efforts. Despite the industry being in a rapid upswing and production accelerating, only 40% of AXL’s backlog is currently weighted toward EVs. Further, the company has yet to develop a key advantage over its peers that would allow for a market-leading position in a similar vein to its current position. This is compounded by the risk of OEMs producing comparable products for EVs in-house. Realistically, AXL will be a strong market participant but we believe there is significant risk associated with replicating its existing business. We believe the broader LPV production slowdown as weighting moves toward EVs is going to be a major concern for the company as it loses on the ICE side and faces greater competition on the EV side.

The auto parts industry is expected to experience a continuation of its recent uptick in growth, with a CAGR of 6.3% into 2032 . AXL faces competition from and operates alongside, several key parts players, including GKN Automotive, Magna International (MGA), Dana Incorporated (DAN), Autoliv (ALV), and Genpact (G). This growth trajectory will be driven by strong demand from the APAC region, as producers in China (in particular) seek to take advantage of their strong EV innovation to penetrate the global automotive industry. Furthermore, technological development and innovation will have a material impact on consumer spending, as the ability of automakers to differentiate will increase. We struggle to see AXL meeting this growth rate, as it has yet to sufficiently tether its growth to the EV segment while facing the downside issues.

Margins

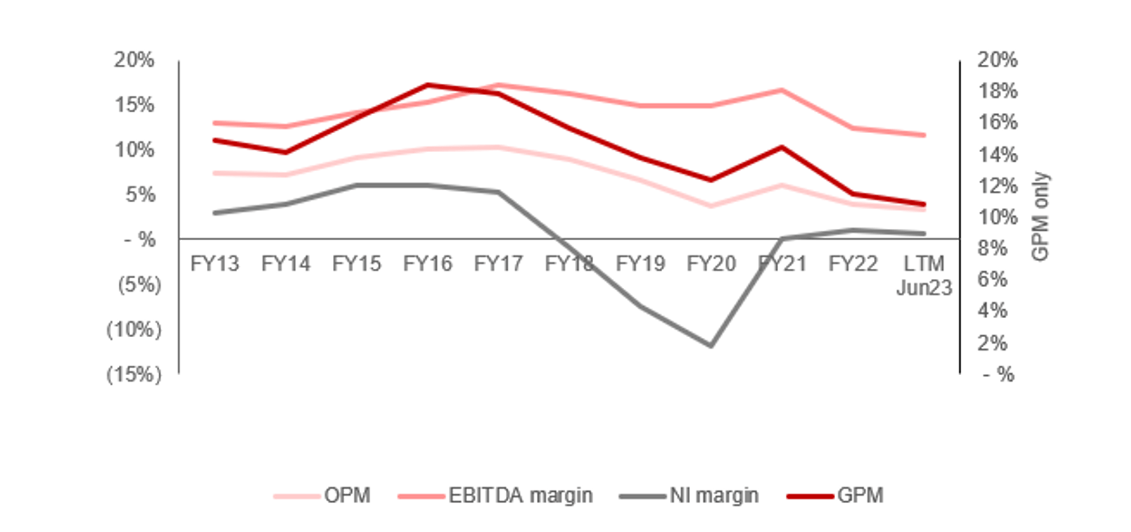

{kind=link}

AXL’s margins have trended down during the last decade, particularly in the post-FY16 period. This is a disappointing development given the significant increase in scale following the acquisition of MPG. The company has been unable to deliver on the synergies and cost savings expected on a normalized basis. The positive for AXL is that its pre-pandemic level (above NI) was strong, with much of the recent decline attributed to macro/industry conditions (supply chain issues contributing to reduced production).

Quarterly results

AXL’s recent performance has been respectable given the current macro environment, with revenue growth of +26.6%, +12.8%, +4.0%, and +9.2% in its last four quarters. In conjunction with this, margins have continued to slide, with an LTM EBITDA-M of 12%.

The company’s growth performance is respectable, however, looks to be achieved through negative pricing action and continued inflationary pressure, contributing to a decline in EBITDA since FY22. We are generally not supportive of such actions, as in highly competitive industries such as this, the ability to subsequently win back margins can be difficult. We attribute this to AXL’s declining competitive positioning.

Key takeaways from its most recent quarter are:

- Management attributes continued margin pressures to inflationary headwinds and labor availability. This is likely a reflection of the wider post-pandemic trend of higher labor churn as pay increases have been sought. This said, we have seen a clear normalization of this trend which implies AXL is potentially under-compensating its staff.

- The company is still working toward establishing a “technological foundation” within the electric component industry, a concerning indictment of its lack of development thus far. The business remains reliant on its traditional ICE-powered vehicle segment.

- R&D spending is expected to sequentially increase as greater financial focus is committed to electrification growth opportunities.

Looking ahead, we suspect the company will face a revenue slowdown, owing to the broader macro environment. The automotive industry has boasted resilience thus far, primarily due to the unwind of supply chain issues contributing to unmet demand being fulfilled. This offsetting impact is rapidly subsiding. As the following data illustrates, LVP is forecast to decline in the coming quarter, driven in large part by the Chinese market. We suspect this will begin impacting other regions too by the end of the year.

For these reasons, we believe revenue will decline in the coming quarter, although likely not substantially so. It is critical for AXL to protect its margins, although we are again hesitant of this.

Production (S&P Global Mobility)

{kind=link}

Balance sheet & Cash Flows

AXL has maintained a bloated balance sheet since its acquisition of MPG, with ND/EBITDA exceeding 3x since Dec17. We do not consider the current level concerning, as its interest coverage is borderline reasonable (as evidenced by historical levels). This said, its inability to rapidly deleverage is a concern and will mean cash continues to be tied up rather than distributed to shareholders.

Speaking of cash flows, AXL’s FCF margin has struggled to improve, operating significantly below the company’s EBITDA margin. This said, as it moves directionally with profitability, its cash flow generation is now highly unattractive and problematic for its long-term objectives.

The company’s ROE profile compounds criticism of its operating performance. AXL’s profitability has been highly volatile, with no genuine scope for normalization due to the commercial concerns ahead. This makes it incredibly difficult to forecast the level of future investor returns through earnings.

{kind=link}

Outlook

{kind=link}

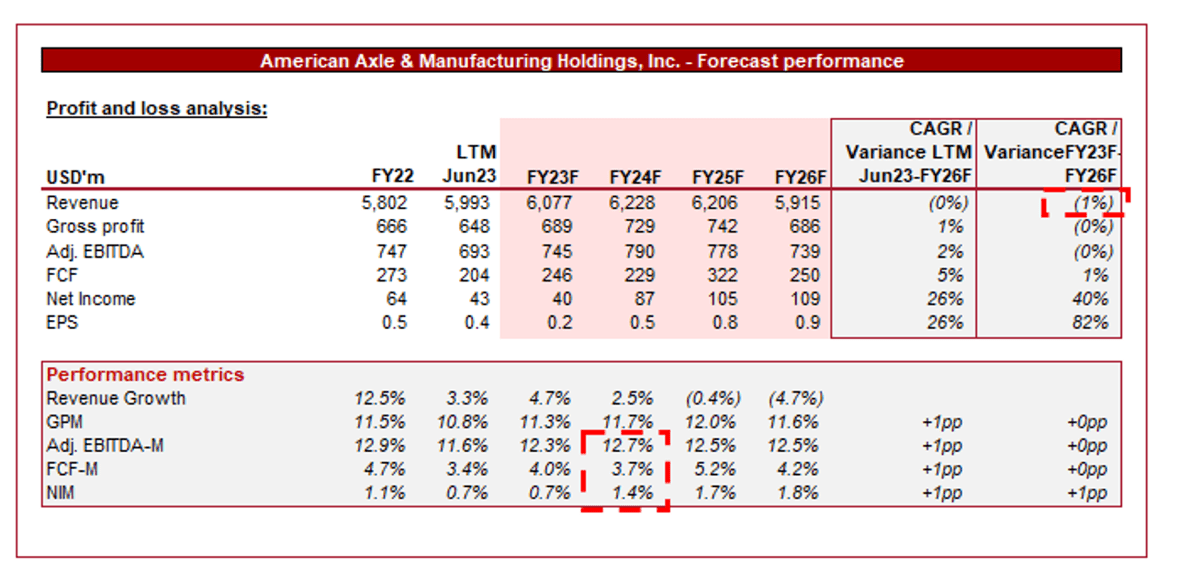

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a worsening of its commercial position, contributing to a stagnation of revenue into FY26F. In conjunction with this, margins are expected to remain broadly flat, although slightly improved from the current LTM levels.

We are supportive of the assumptions made. We are completely unconvinced by the technological developments currently underway, contributing to a reliance on traditional ICE-powered vehicles. Due to this, the expectation is that as production transitions toward EVs, revenue growth potential will rapidly diminish. It is worth highlighting that the company could successfully innovate itself out of this mess and is trying its best to do so, but based on the current evidence, we are not confident.

Margins assumptions also appear reasonable. As a market-leading business, it is unlikely to see a material change, with scope for some improvement coming from supply chain improvements.

Industry analysis

Auto Parts and Equipment Stocks (Seeking Alpha)

{kind=link}

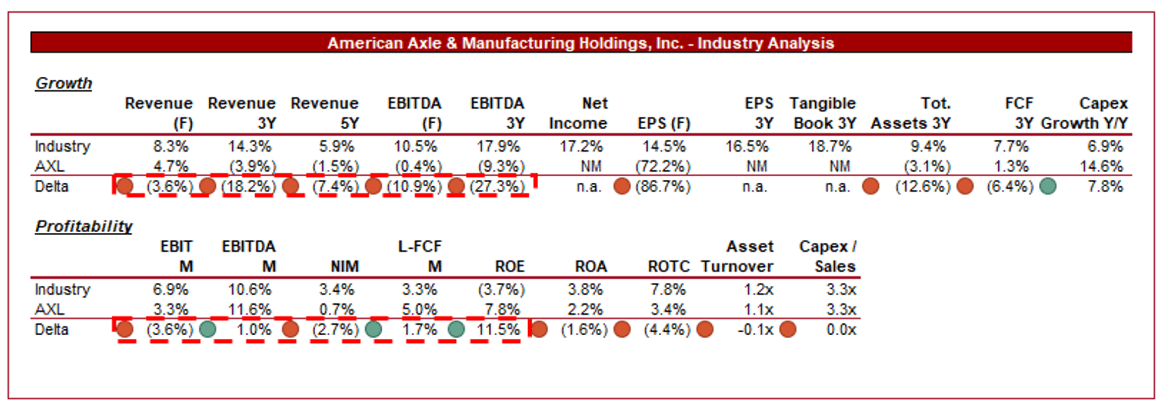

Presented above is a comparison of AXL's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

AXL’s performance is disappointing relative to its peers. The company’s growth has lagged its peers across every time frame, in both revenue and profitability. This is a reflection of slowing light vehicle production growth in favor of more EVs, as well as its declining commercial standing.

The company’s margins are slightly better, with an EBITDA-M and FCF outperformance. This said, this is a reflection of its historical business model, which does not translate well into how the market is transitioning. Although margins are unlikely to be affected in the coming 5 years, beyond this we could see greater pressure.

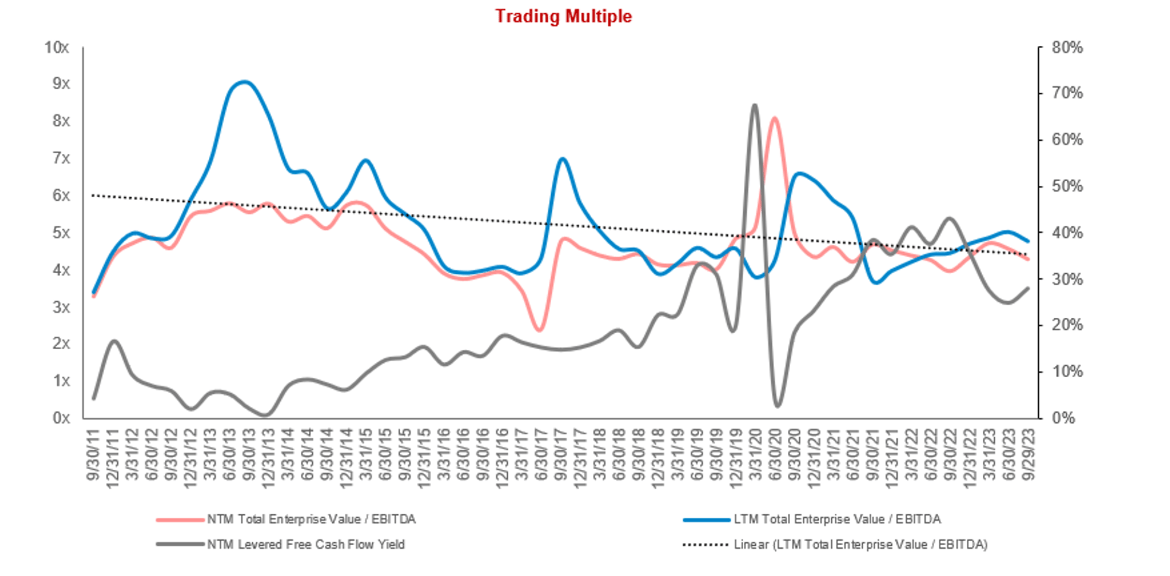

Valuation

{kind=link}

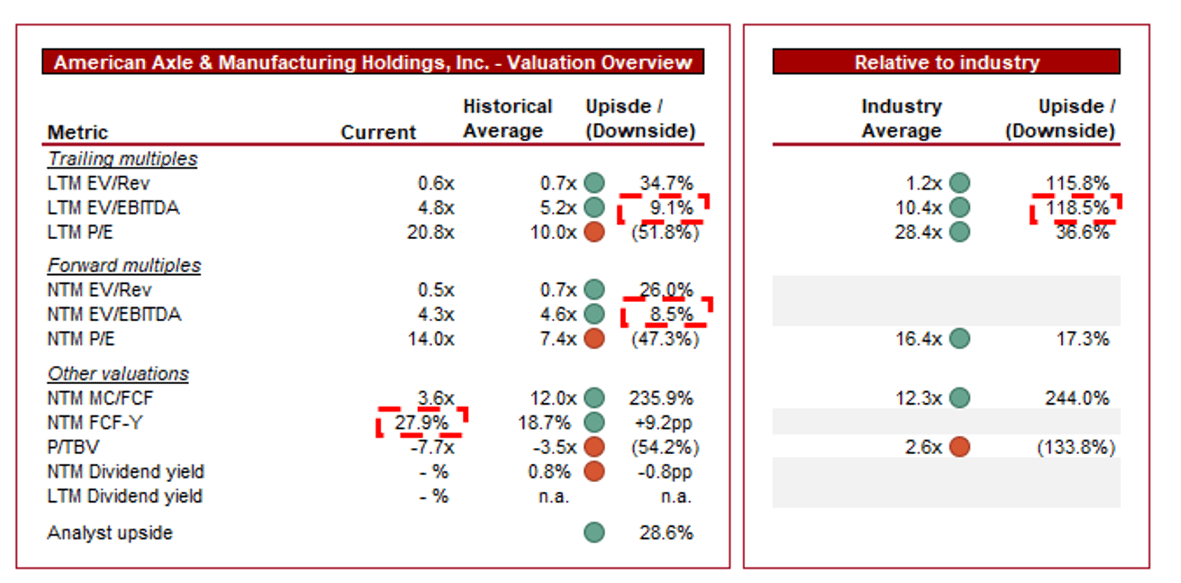

AXL is currently trading at 5x LTM EBITDA and 4x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, owing to the decline in the company’s financial performance and commercial attractiveness. At a low multiple, it appears investors have priced in the long-term concerns for an extended period, yet we still feel the current discount is not sufficient.

Further, the company is currently trading at a substantial discount to its peer group, with a 119% discount on an LTM EBITDA basis and a 17% discount on a NTM P/E basis. A discount is undoubtedly warranted in our view, reflecting the poor future outlook and weakness in growth thus far.

Risk-taking investors may see an opportunity with a depressed valuation such as this, particularly with an FCF yield in excess of 20%. This must be contextualized, however. Its average FCF yield is close to 20%, yet investors have seen almost none of it since FY13, with a substantial unconvincing acquisition and investment in electrification that has no evidence of future repayment.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The key risks to our current thesis (outside of innovating its way to a market-leading position) are:

- A rapid improvement in economic conditions. This would likely lead to an improvement in spending, allowing for production levels to stabilize before expanding.

- Delays in the EV transition . The UK recently announced it would delay the ban on traditional ICE-powered vehicle sales. Should this occur in other large markets, we could see a delay to our thesis and greater time for AXL to develop a suite of attractive products.

Final thoughts

AXL is facing significant threats to its business model, as the automotive industry transitions to EVs. The company is a leading player in the existing market, with strong relationships and deep expertise. For this reason, we do believe it will have some success in growing within the EV segment, however, we do not currently see it maintaining its existing relative position.

Compounding our negative views are the lack of distributions, poor performance relative to its peers, and the potential for weakening financial performance in the near term.

For further details see:

American Axle & Manufacturing Holdings: Unconvincing EV Transition