AEO - American Eagle Outfitters Has Turned The Corner

2023-09-07 04:05:58 ET

Summary

- American Eagle Outfitters' stock is down after hours following its earnings report, presenting a potential trading opportunity.

- The report showed strong overall earnings, with flattish net sales but a 4% increase in comparable store sales.

- Gross profit and operating income saw significant improvements, leading to a turnaround in net income and earnings per share.

- Expect EPS revisions upward; turnaround confirmed.

We have traded American Eagle Outfitters (AEO) several times in the past and have loved the recent rally in the stock for a trade despite the pressure that we see coming for retailers. Shares are down after hours following the just reported Q2 earnings . We believe there is a trading opportunity that can stem from this selloff afterhours, but would like to see a retracement under $16 preferably. But that will not stop us from suggesting the specialty retailer is a buy.

The earnings, which we discuss here for our readers, were strong overall. In our opinion, the report did have some mixed components, and that has us hesitant to trade the name at current valuations, and as such prefer it lower. Long-term, we do see shares as a buy. While it has made for a good trade, as an investment, unless you were a buyer on the massive selloff and scooped shares this year, you have likely lost money. One way to potentially play the stock is through a buy-write strategy, but we think you need to let the stock retrace more before entry. There are a lot of things we like about the company, though some of the metrics are concerning, and we are especially cautious in this high rate environment which at some point is going to do some economic damage in our opinion. We also have student loan repayments coming. All things considered we rate shares a buy, but think traders need to wait for a breather in shares. Let us discuss the results.

When examining any kind of retailer, in any subsector of the space, in this case specialty retail, it's all about sales and margins. More specifically, we look at comparable sales. Well, net sales were about flat from a year ago at $1.2 billion, but nudged higher enough to set a new record for Q2. This was in line with the consensus estimates . Look no further than the comparable sales figure for why sales were flat. Well, comparable store sales were up 4%, which was solid. Interestingly, however, digital sales were weaker than anticipated, falling 7% from last year. This was a glaring weakness, but the positive store comps are welcomed.

We also mentioned the importance of margins. Despite flattish sales, gross profit is up. Folks, it was impressive. Gross profit ballooned to $453 million, a 22% jump compared to $370 million in Q2 2022 and reflected a gross margin rate of 37.7% compared to 30.9% last year. That is a strong 680 basis point improvement. Margin expansion was driven by lower markdowns thanks to management having much better inventory control and lower transportation and product costs compared to last year. Rising fuel costs are a risk going forward here though, so keep an eye on freight rates, it could be an issue going forward if energy does not retrace. Distribution and warehousing costs also softened, setting up the company for stronger profit.

Earnings power ramped up thanks to the good news on margins. Folks, operating income surged to $65 million, up from $14 million a year ago. Operating margin was 5.4% vs 1.2% a year ago. Truly strong here. Net income was $48.6 million, or $0.25 per share, versus a loss of $42.4 million, or -$0.24 per share a year ago. A real turnaround. EPS crushed estimates by $0.10 per share. This is a 66% beat versus the consensus level.

Moving forward, these are the items we'll look for. We look to see how sales will be. Comparable sales are key. In terms of valuation here, waiting to buy seems appropriate.

{kind=link}

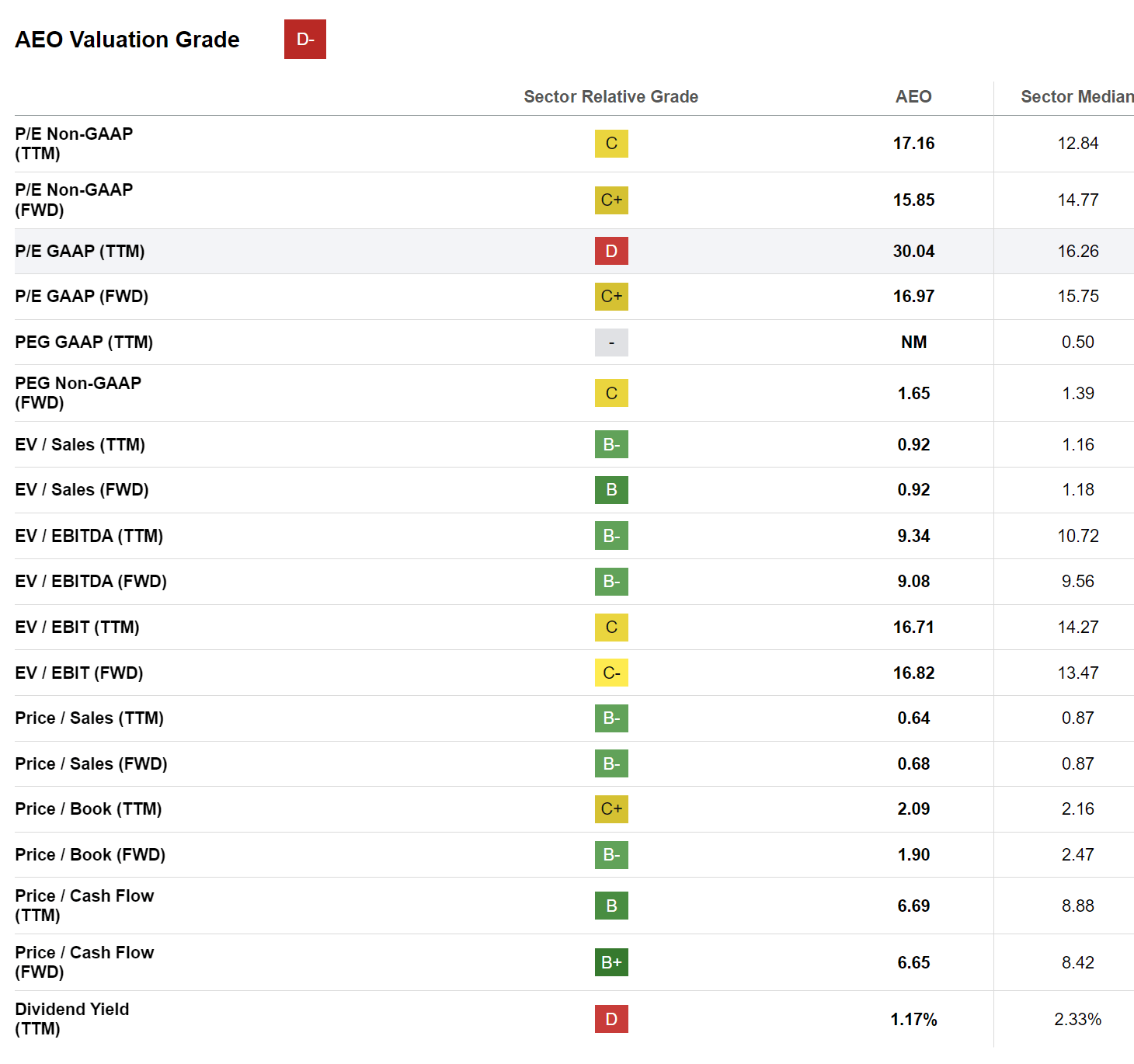

Overall, the rating is D on valuation. The FWD p/e is relatively in line with the market at 15.8X and with the sector median at 14.8X. We also think that on a price-to-cash flow basis, the stock is relatively attractive. The enterprise value metrics also are attractive, so nothing jumps out as overtly bearish, but it's not exactly screaming value. However, the growth is back, so you are paying a bit for that.

We think you see some EPS revisions on this quarter. This is because for the year, management now expects revenue to be up low single digits compared to last year, compared to prior guidance for revenue in the range of flat to down low single digits. Operating income is now expected to be in the range of $325 to $350 million, up from prior guidance of $250 to $270 million. We now think the company can earn $1.20 per share this year. That would be less than 14X earnings. Overall, we like what is going on here, but think you need to let shares pull back a bit, then do some buying.

For further details see:

American Eagle Outfitters Has Turned The Corner