BOOT - American Eagle Outfitters: Navigating Retail Dynamics With Strategic Initiatives And Brand Strength

2023-10-13 09:00:00 ET

Summary

- AEO is a leading global specialty retailer known for its high-quality clothing and accessories.

- AEO's brands, including Aerie, have shown impressive growth and resilience in the retail sector.

- The company's recent performance, strategic inventory management, and innovative product launches position it for sustained growth.

Summary

American Eagle Outfitters (AEO) is a leading global specialty retailer known for offering high-quality, on-trend clothing, accessories, and personal care products. As a staple in the casual apparel sector, AEO primarily caters to the teen and young adult demographics. The brand has garnered acclaim for its denim collections, which seamlessly blend comfort, style, and innovation. Beyond its mainline offerings, the company also champions Aerie, a lingerie and activewear brand celebrated for its body positivity campaigns and inclusive sizing. By adeptly combining brick-and-mortar retail with a strong online presence, AEO ensures it remains relevant and accessible, continuing to resonate with its loyal customer base amidst the evolving retail landscape.

Business overview

The company emerges as a beacon of adaptability and resilience in the ever-evolving retail sector. The brand's recent performance, which highlights its strategic expertise in inventory management and innovative product launches, highlights its potential for sustained growth. Aerie, a subsidiary brand, has been particularly noteworthy, showcasing impressive growth trajectories. Furthermore, the American Eagle [AE] brand continues to resonate with consumers, amplifying its market presence. Financial indicators, combined with a favorable valuation from a DCF model, highlight AEO's robust financial health and promising future. This valuation is anchored in AEO's historical performance, its post-pandemic recovery, and its alignment with market expectations. As AEO continues to harness its brand strength and execute strategic initiatives, it is well-positioned to capitalize on upcoming opportunities in the retail landscape.

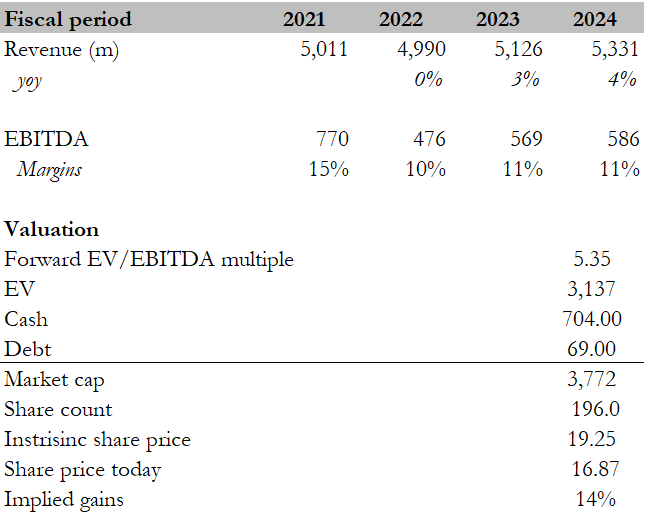

From 2017 to 2022, the company displayed a blend of resilience and adaptability. Revenue saw steady growth until 2019, with a 6% rise in 2018 and 7% in 2019. However, due to difficulties in 2020, including the COVID-19 pandemic and global economic disruptions, there was a 13% decline. Impressively, 2021 marked a robust recovery with a 33% revenue surge, stabilizing in 2022 with no growth due to tough comparisons. The six-year revenue CAGR stands at 5%.

On the profitability front, the EBITDA margin remained consistent at 13% for 2017 and 2018, dipped to 11% in 2019, and sharply declined to 5% in 2020. Yet, 2021 saw a remarkable rebound to 15%, moderating to 10% in 2022 due to tough comparisons. The average EBITDA margin over this period was 11%.

Investment thesis

AEO has recently presented its second quarter results, which show promise and demonstrate the brand's adaptability in a challenging retail environment. A pivotal highlight was the back-to-school shopping period, where both of AEO's brands, AE and Aerie, made a significant impact on consumers. In the second quarter, AEO announced a record revenue of $ 1.2 billion , marking an increase from the previous year.

Aerie, a standout brand under the AEO umbrella, showcased remarkable momentum. The brand's revenue surged by 2% in the second quarter, boasting an impressive operating margin of 15.1% . This growth trajectory is attributed to an improved markup strategy and a reduction in markdowns. Such strategic pricing and inventory management decisions have fortified Aerie's position in the market, emphasizing its potential for future growth.

The introduction of cutting-edge products like AE77 and 24/7 further amplifies the AE brand's positive trend. These additions not only rejuvenated the brand's appeal but also expanded its consumer reach. In the latest quarter, both AE and Aerie were performing positively, a testament to AEO's proactive strategy of introducing fresh fashion and swiftly adjusting to high-demand items.

AEO's strategic approach to inventory management further bolstered its second quarter performance. By minimizing promotions and end-of-season clearance, the brand maintained its pricing integrity and equity. This strategy led to the second quarter's average unit retail [AUR] being among the highest in the company's history.

Financially, AEO stands on solid ground. The company reported a robust cash reserve of $175 million, an increase of $77 million from the previous year. This stellar second quarter performance prompted AEO to revise its annual outlook, now projecting growth in total revenue in the low single digits and an operating income of between $325 million and $350 million.

AEO’s second quarter performance, which was characterized by strategic inventory management, product innovations, and strong brand performance, solidifies its position as a compelling investment opportunity. The brand's agility in navigating market shifts, combined with its robust financial foundation, indicates a positive outlook for the company.

Valuation

I believe the fair value for AEO based on my DCF model is $19.25. This valuation draws from the company's historical resilience, particularly its robust recovery in 2021 and 2022 due to the recovery of the COVID-19 pandemic and the easing inflationary environment . Therefore, I anticipated 3% growth in FY23 and 4% in FY24. These projections are consistent with the company's historical CAGR and align with both market consensus and management's guidance. The sustained success of brands like Aerie, strategic inventory management, and the introduction of products such as AE77 and 24/7 further underpin this growth outlook. Given the exceptional performance across its brands, which have achieved impressive margins, I expect the EBITDA margin to align with its historical average.

{kind=link}

Peers include Boot Barn (BOOT) and Abercrombie & Fitch (ANF). The median forward EV/EBITDA multiple peers are trading at is 6.86x, the median EBITDA margin is 16%, and the median net margin is 5%. As for AEO, its forward EV/EBITDA multiple is 5.35X, its EBITDA margin is 16.59%, and it has a net margin of 3.87%. The factors that drive the lower valuation are, in part, due to its lower net margin compared to peers. Therefore, I believe its current multiple is fair. At its current multiple, implied gains are 14%. Therefore, I recommend a buy rating. Should AEO succeed in enhancing its net margins to align more closely with the median of its peers, there's potential for its valuation multiple to expand towards the peer’s median. This shift would pave the way for greater upside potential. Currently, AEO is on a promising trajectory, as evidenced by its effective inventory management and the strong margins exhibited by its brands in the recent quarter. It will be crucial to closely observe the outcomes of their strategic initiatives in the forthcoming quarters to gauge the initiative’s success.

Risk

While AEO has shown resilience with its inventory management and brand margins, there's a risk associated with its net margin, which currently lags behind its peers. If AEO strategies fail to expand its net margins or face unforeseen operational challenges, it might experience margin compression. This could lead to reduced profitability, potentially impacting its valuation and making it less attractive to investors compared to its peers. Additionally, any external market factors or increased competition that puts downward pressure on demand could further exacerbate this risk, such as persistent inflation.

Conclusion

AEO has demonstrated adaptability and resilience in its recent performance, reflecting its strength in a dynamic retail landscape. The brand's strategic initiatives, from inventory management to product innovation, have been pivotal in driving its success. Notably, the standout growth of Aerie and the continued positive trajectory of the AE brand underscore AEO's potential. Financially, the company's robust cash position and optimistic growth outlook further solidify its position. My DCF model values AEO favorably, a valuation rooted in the brand's historical financial resilience, especially its recovery in the post-pandemic phase. The projected growth rates, consistent with historical trends and market expectations, coupled with the brand's strengths, position AEO as a compelling investment proposition. As the company continues to leverage its brand appeal and strategic initiatives, it stands poised for a promising future in the retail sector. With these tailwinds, I recommend a buy rating for AEO.

For further details see:

American Eagle Outfitters: Navigating Retail Dynamics With Strategic Initiatives And Brand Strength