AEP - American Electric Power: A Great Utility To Boost Passive Income

2024-01-03 01:36:01 ET

Summary

- American Electric Power is the largest utility holding in my portfolio.

- The electric utility narrowly missed the analyst revenue consensus in the third quarter but topped the analyst consensus for operating EPS.

- American Electric Power enjoys an A- credit rating from S&P on a stable outlook.

- Shares of the electric utility appear to be priced 14% below fair value.

- American Electric Power could be primed to outperform the S&P in both the coming two and 10 years.

The utility sector is well known for its ability to pay reliably growing, above-average dividends to shareholders. On its face, it isn't hard to understand why.

For one, water, electricity, and natural gas are likely never going to face the risk of becoming technologically obsolete. Second, basic utility services are a prerequisite to living a high quality of life. Thus, the demand for these services is steady no matter what is going on with the economy. Third, population growth should translate into even higher demand for utility services moving forward. Fourth, regulated utilities are generally able to charge higher rates over time for their services. This is a formula for consistent growth in revenue and earnings, which is what supports rising dividend payments from utilities.

I'm going to be revisiting the largest utility in my portfolio, American Electric Power ( AEP ), which I believe remains a buy. The electric utility comprises 1.1% of my individual holding portfolio. For the first time since September 2023 , I will highlight AEP's recent operating results and valuation to back up my buy rating.

{kind=link}

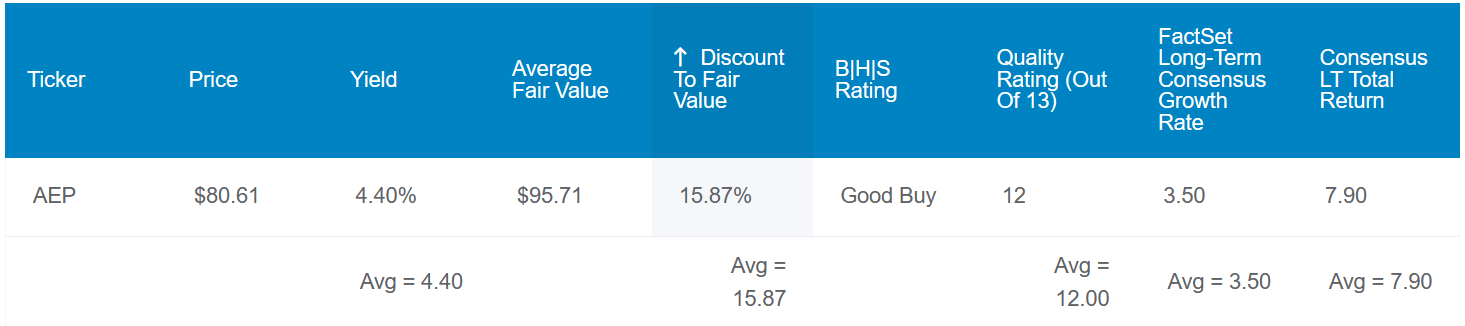

AEP's 4.4% dividend yield clocks in 50 basis points above the 3.9% yield of the 10-year U.S. treasury. Not to mention that its starting income is approximately triple the S&P 500's ( SP500 ) 1.5% yield.

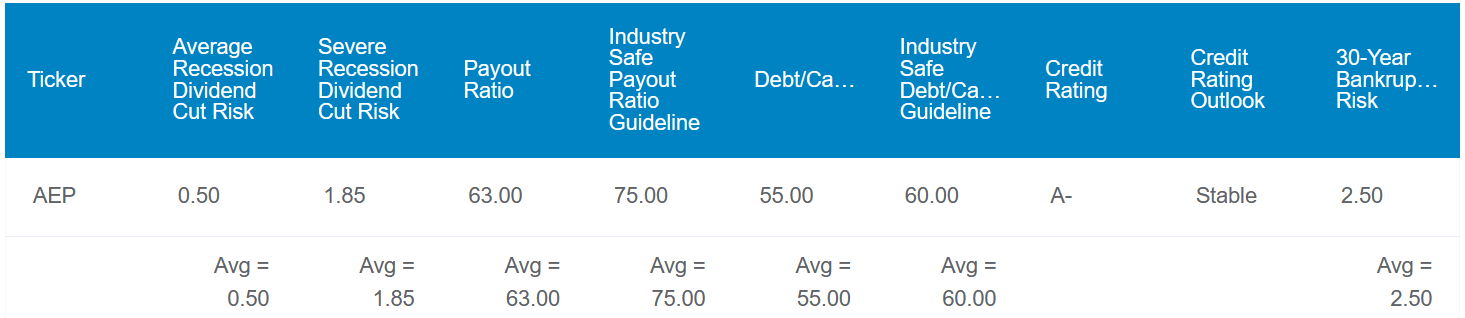

What makes this yield especially appealing is that it looks to be on a stable footing. This is because AEP's 63% EPS payout ratio is below the 75% EPS payout ratio that rating agencies consider safe for utilities.

Additionally, the electric utility's 55% debt-to-capital ratio is slightly less than the 60% that rating agencies prefer from utilities. These are some of the reasons why S&P awards an A- credit rating to AEP on a stable outlook. This implies that the electric utility faces just a 2.5% probability of going bankrupt in the coming 30 years.

{kind=link}

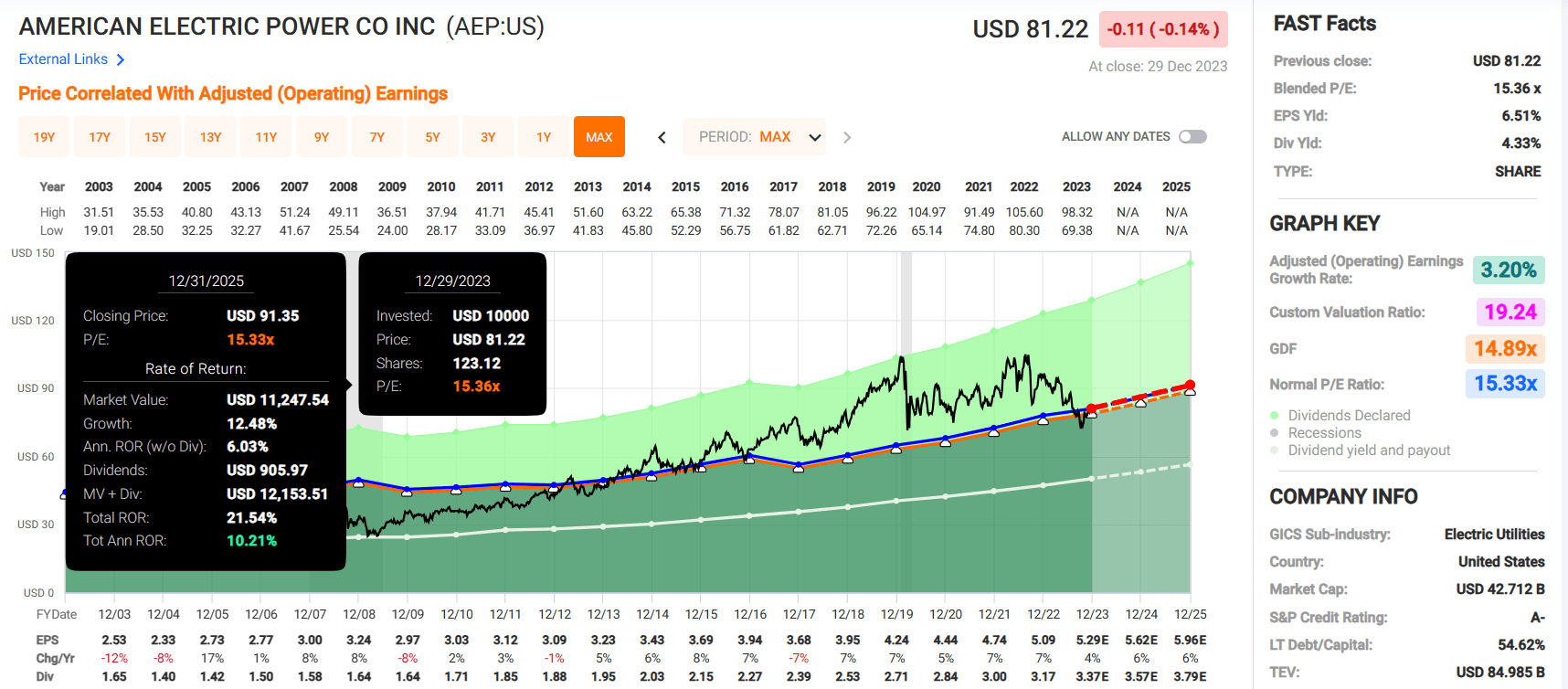

Fundamentals aside, another characteristic that I like about AEP is its current valuation. If historical dividend yield and P/E ratio are any guide, shares of the electric utility are each worth $96. Compared to the $82 share price (as of January 2, 2024), this suggests that AEP is trading at a 14% discount to fair value.

If the electric utility reverted to fair value and met the analyst growth consensus, here are the total returns it could generate in the next 10 years:

- 4.3% yield + 3.5% FactSet Research annual growth consensus + a 1.5% annual valuation multiple boost = 9.3% annual total return potential or a 143% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Operating Earnings Surged In The Third Quarter

{kind=link}

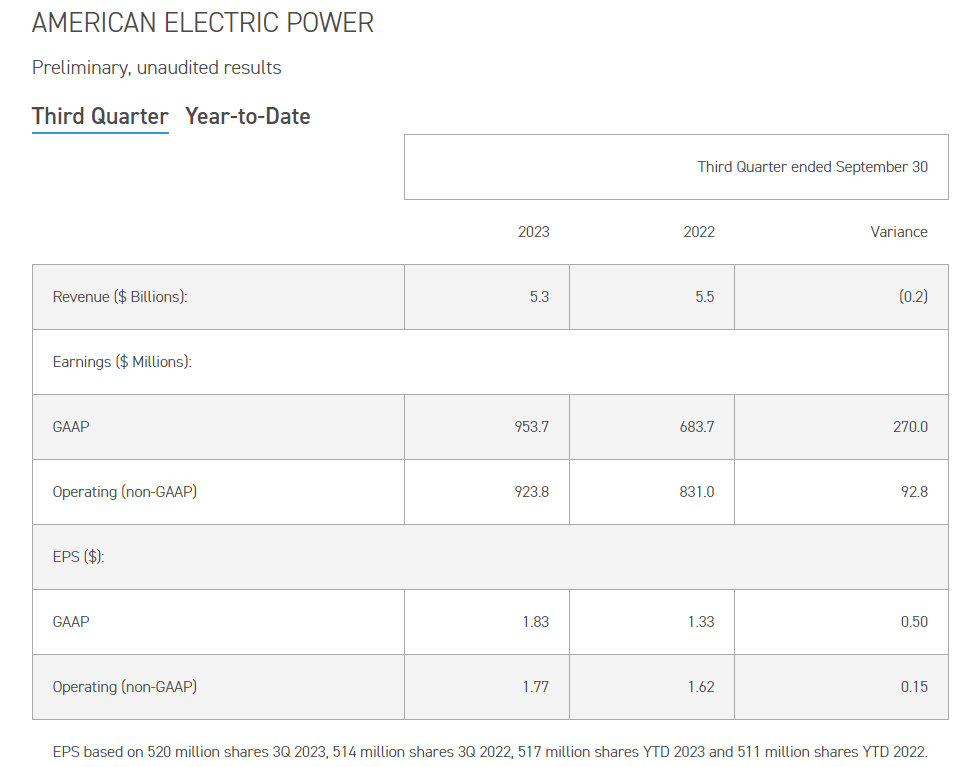

In early November of last year, AEP shared its financial results for the third quarter ended September 30. The company's total revenue fell 3.3% over the year-ago period to $5.3 billion in the quarter. For context, this missed the analyst consensus by $80 million .

If there isn't a good reason behind a topline decline, that's usually a red flag for me. The good news is that I believe AEP's dip in revenue to be acceptable for the circumstances. That is because mild weather was what weighed on the company's revenue during the third quarter.

Total weather-normalized retail sales volumes edged 2.1% higher year-over-year for the quarter. This was largely driven by a 7.5% growth rate in weather-normalized commercial sales in the quarter, which was made possible by new data centers in AEP's service areas. A 0.6% increase in weather-normalized residential sales was another contributing factor to total weather-normalized retail sales volume growth during the quarter. Growth within these two customer groups was only partially offset by a 1.1% decrease in weather-normalized industrial sales (details sourced from page 13 of 223 of AEP's 10-Q filing ).

AEP's operating EPS climbed 9.3% higher over the year-ago period to $1.77 for the third quarter. That topped the analyst consensus by $0.07. The slightly lower demand for electricity in the quarter was more than countered by a 13.2% drop in total operating expenses to $4 billion. This was the result of lower purchased electricity and fuel expenses and operating expenses. The company's higher operating income was only partially offset by higher interest expenses stemming from elevated interest rates.

Moving to the balance sheet, AEP is financially healthy. The company's interest coverage ratio through the first nine months of 2023 was 2.4. This is an okay interest coverage ratio for a regulated utility. That's especially true when considering that interest rates are still near their highest levels in 15 years. As interest rates come down and AEP's earnings grow, its interest coverage ratio should improve. The company's pension program was also 100% covered as of the third quarter (info according to slide 42 of 86 of AEP's 2023 Factbook ).

{kind=link}

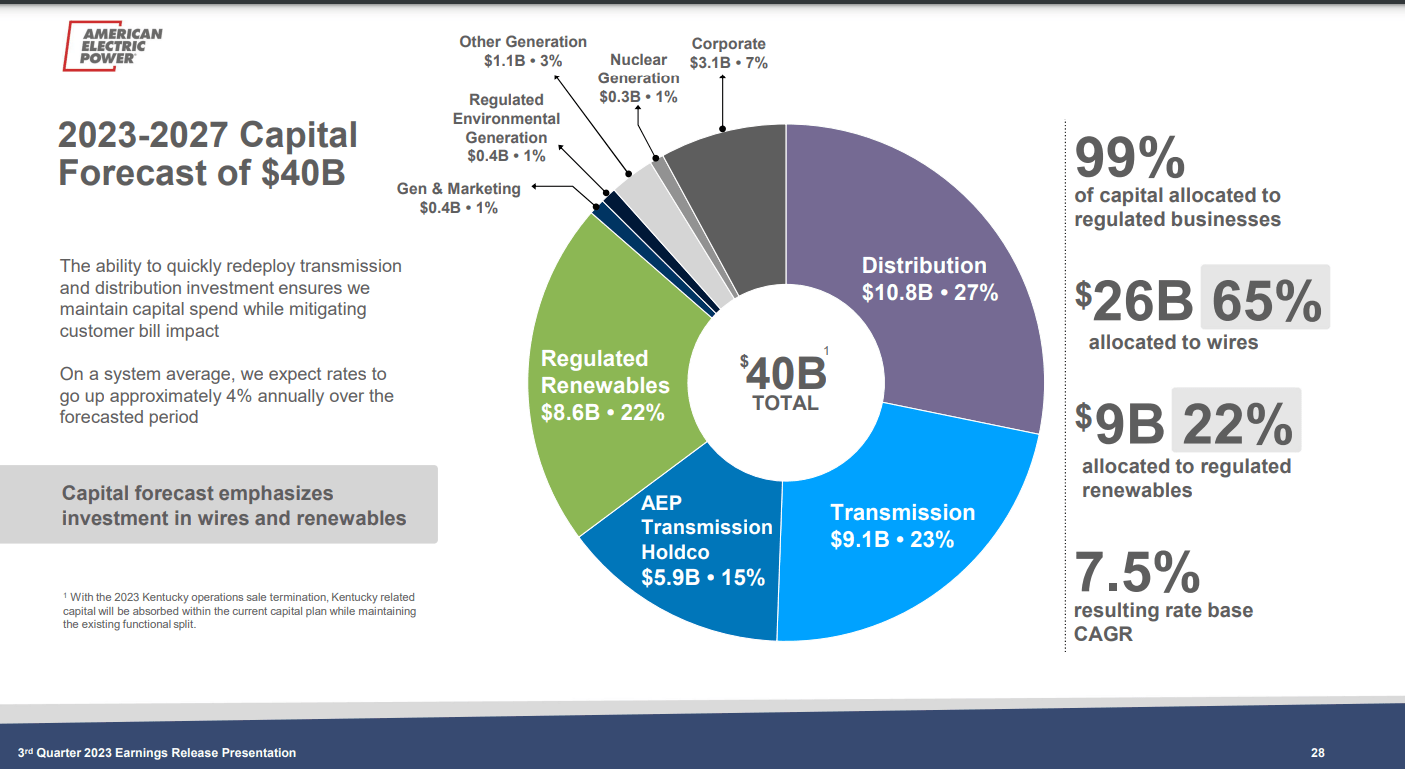

For these reasons, AEP should have little difficulty funding its $40 billion capital spending forecast for 2023 through 2027. This ambitious capital spending program will be split between distribution, transmission, the AEP Transmission Holdco, regulated renewables, and other spending. The company anticipates that this should fuel 6% to 7% annual operating EPS growth in the years to come.

The Safest Dividend Is The One Just Raised (By 6%)

As I expected, AEP raised its quarterly dividend per share by 6% to $0.88 last October. In the last five years, the company's quarterly dividend per share has increased by 31.3% . In the next five years, I believe dividend growth should be like the last five years.

This is because analysts are projecting that AEP will post $5.28 in operating EPS in 2023. Against the $3.37 in dividends per share paid in 2023, that is a payout ratio of just 63.8%. For more perspective, this is well within the company's 60% to 70% targeted payout ratio range (slide 6 of 41 of AEP's Q3 2023 Earnings Presentation).

Risks To Consider

AEP is a quality utility, but it still faces risks that must be weighed against the rewards of a potential investment.

The same regulated nature that makes AEP interesting is also what could make it concerning. That's because there is the possibility that public utility commissions may not approve adjustments to rates related to capital improvements and additions. If this were to happen, the company's operating results could be negatively impacted in affected markets. Fortunately, AEP's operations are scattered throughout 11 states in the U.S. So, any single unfavorable regulatory outcome won't completely crush its growth prospects.

Another risk to AEP is the potential for its projects to be delayed and/or to experience cost overruns. If this were to happen, the company's growth profile could be hurt.

Lastly, AEP owns the Cook Plant, which is made up of two nuclear generating units. If this asset were to have a major incident, the impact on the surrounding area could be devastating. Such an event could result in damages beyond the extent of AEP's insurance coverage, which could hurt AEP's financial position.

Summary: AEP Offers Value And Market-Beating Income

{kind=link}

{kind=link}

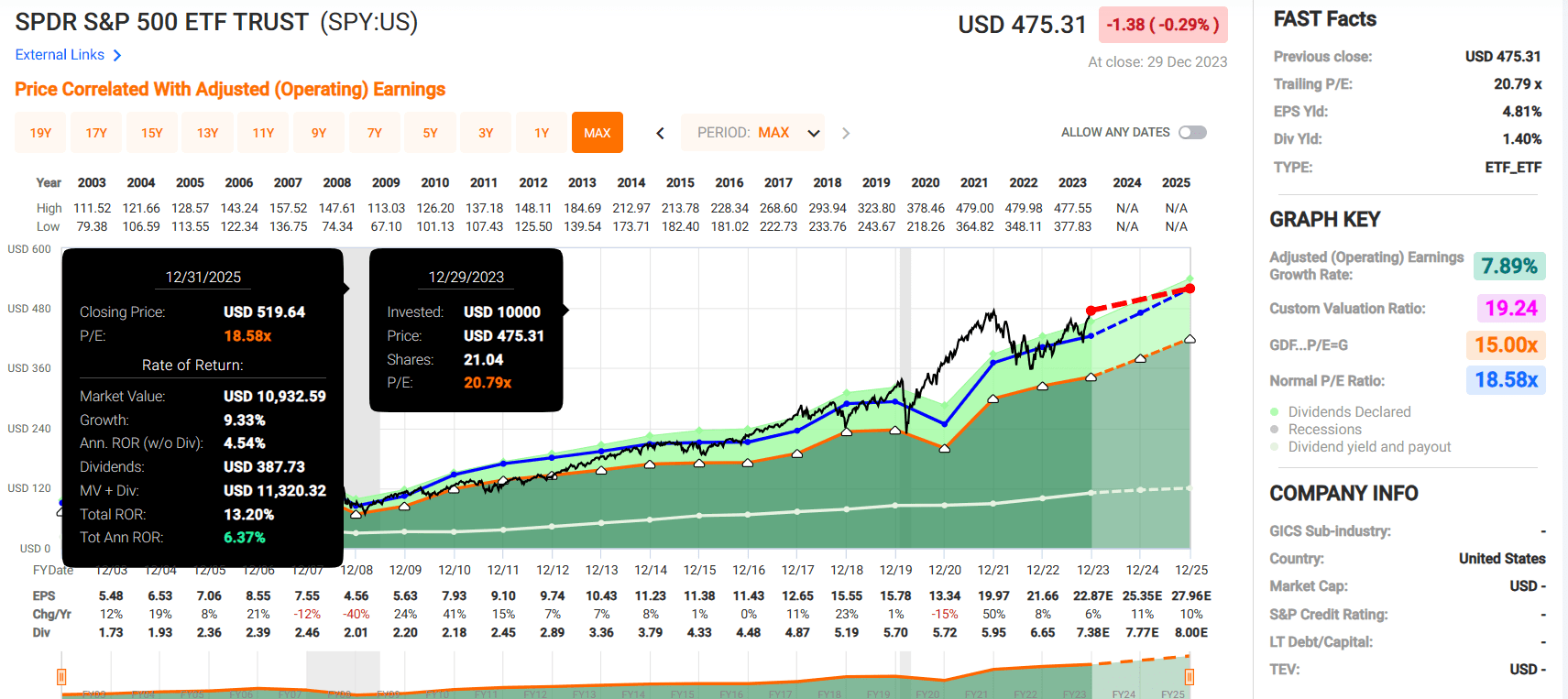

AEP's blended P/E ratio of 15.4 is trading about in line with its normal P/E ratio of 15.3. Assuming the company can grow as analysts expect and its valuation holds steady, it could deliver nearly 22% cumulative total returns through 2025. This would be 60%+ greater total return potential versus the 13% cumulative total return expected from the SPDR S&P 500 ETF Trust ( SPY ) during that time. That's why I am reiterating my buy rating on shares of AEP now.

For further details see:

American Electric Power: A Great Utility To Boost Passive Income