AEP - American Electric Power: Buy This Dividend Giant Before Everyone Else Does

2023-10-25 08:10:00 ET

Summary

- American Electric Power is one of the largest utilities in the U.S. serving 5.6 million customers across 11 states.

- AEP has underperformed the market in the past year due to concerns about inflation and customer demand.

- Despite these challenges, AEP has strong profitability and growth prospects, making it an attractive investment with a high dividend yield.

It's not easy being a contrarian investor, as friends and acquaintances at a cocktail party would probably be more interested in hearing about your investment in Nvidia ( NVDA ) than about boring utilities, especially when they are so far down in price over the past 12 months.

This brings me to American Electric Power ( AEP ), which I last covered here back in February with a 'Buy' rating, reflecting its strong positioning and potential benefits from its renewable energy transition. In this article, I discuss why now may be a terrific time to open a position on the stock for durable 'all weather' income at a value price and a historically high yield, so let's get started!

Why AEP?

American Electric Power is one of the largest investor-owned utilities in America, serving 5.6 million customers across 11 states. It has the largest transmission network in the nation, spanning 40K miles, and generates 25K MW of electric power, including 7.1K from renewable energy.

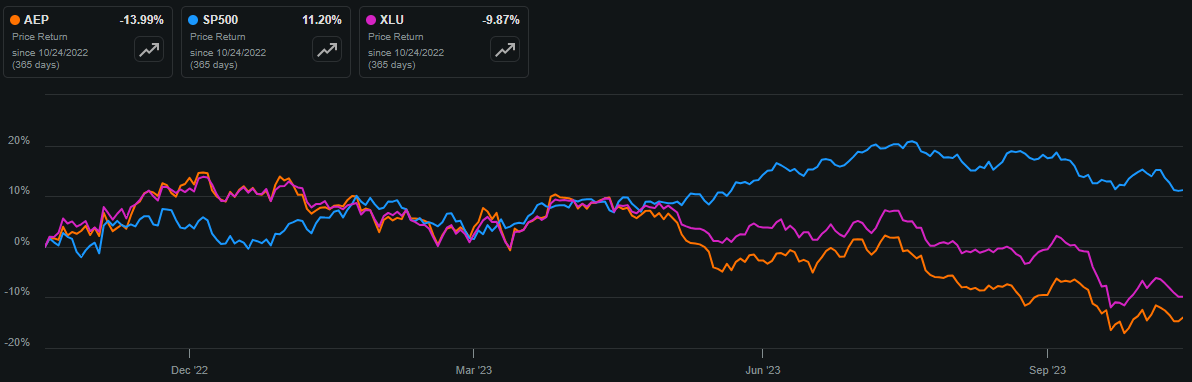

Those who follow AEP know that it hasn't been immune to the downturn in utility stocks over the past year, as the market has fallen out of favor with slow-growing and capital-heavy utility stocks. This is reflected by AEP's 21% share price decline since my last piece in February. As shown below, AEP has underperformed both the S&P 500 ( SPY ) and the Utilities Select Sector SPDR ETF ( XLU ) over the past 12 months.

{kind=link}

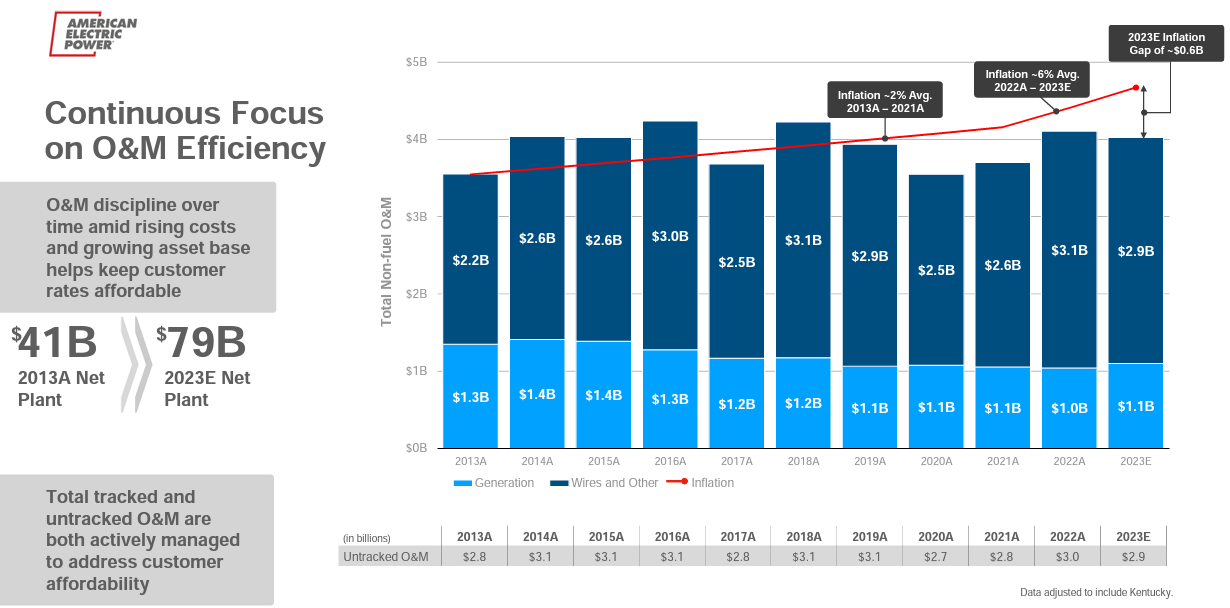

Inflation has weighed heavily in investors' psyche over the past year, and that's spilled over into sectors that are labor and capital intensive such as utilities. Those concerns for AEP, however, may be overestimated, considering that the company has a strong track record for capital efficiency. This is reflected by O&M (operating and maintenance) costs that have stayed more or less the same over the past decade, despite going through periods of higher inflation in recent years, as shown below.

{kind=link}

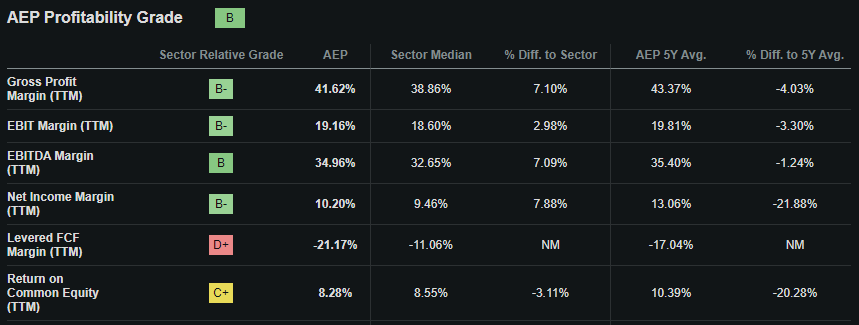

Plus, AEP's operating efficiencies relative to its utility sector peers has helped it to earn a 'B' grade for profitability. AEP produced healthy Net Income and EBITDA margins of 10.2% and 35% over the trailing 12 months, respectively, sitting above the sector medians, as shown below.

{kind=link}

Nonetheless, inflation appears to have weighed on AEP's residential and industrial customers, as their electric loads declined during the second quarter. This was partially offset by increased loads by commercial customers, which saw 8% YoY load growth in the first half of the year. This was a contributing factor to the $0.07 YoY decline in AEPS second quarter earnings per share to $1.13.

While inflation has remained sticky in the near-term, customer usage patterns could normalize over time as wage-growth tends to lag CPI growth by a couple of quarters. This is supported by a recent survey by Bankrate last month, showing that wage growth is closing the gap to the growth in price of goods. Plus, management doesn't appear to be fazed by near-term results, as it reaffirmed its full-year EPS guidance for $5.29 at the mid-point, and its 6% to 7% long-term annual growth target.

Looking forward to Q3 results and beyond, I wouldn't expect much surprises, considering that inflation pressures have eased . AEP should also be able to support its 6-7% annual EPS growth target, as nearly all of its $40 billion capital spend plan through 2027 is expected to go towards regulated investments.

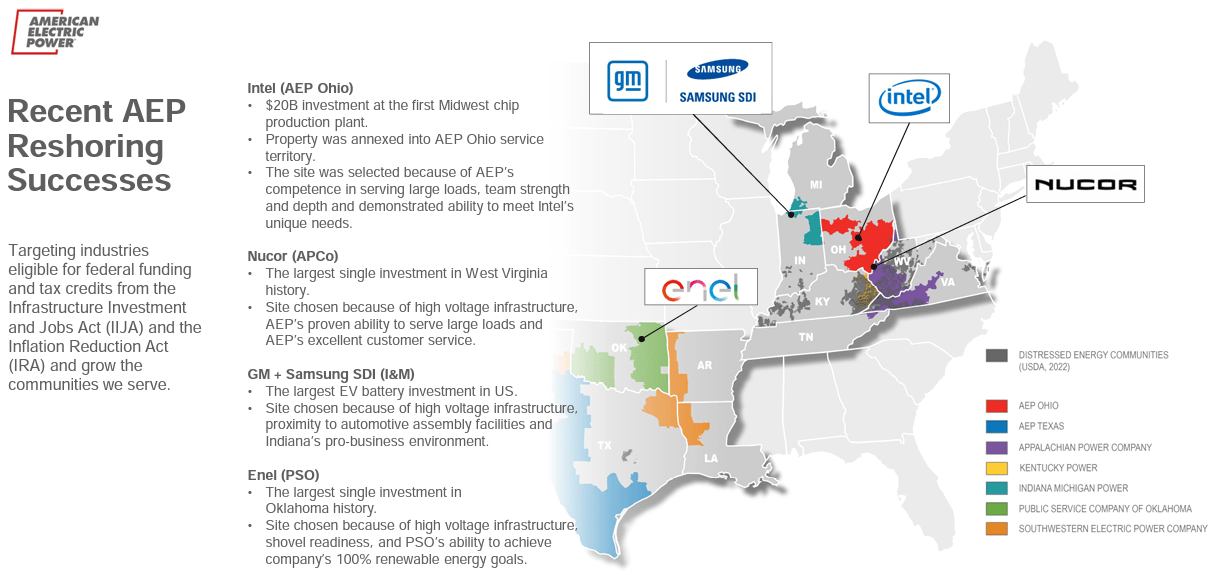

Plus, growth trends in AEP's markets are expected to add 77K jobs in the near-term. This includes the potential impact from domestic investments and re-shoring of manufacturing activities back to the U.S. Examples are the $20 billion investment by Intel ( INTC ) to build 2 leading-edge chip factories in Ohio as part of its push to buildout domestic foundries, along with manufacturing investments by steelmaker Nucor ( NUE ), GM ( GM ), and Samsung ( SSNLF ), as shown below.

{kind=link}

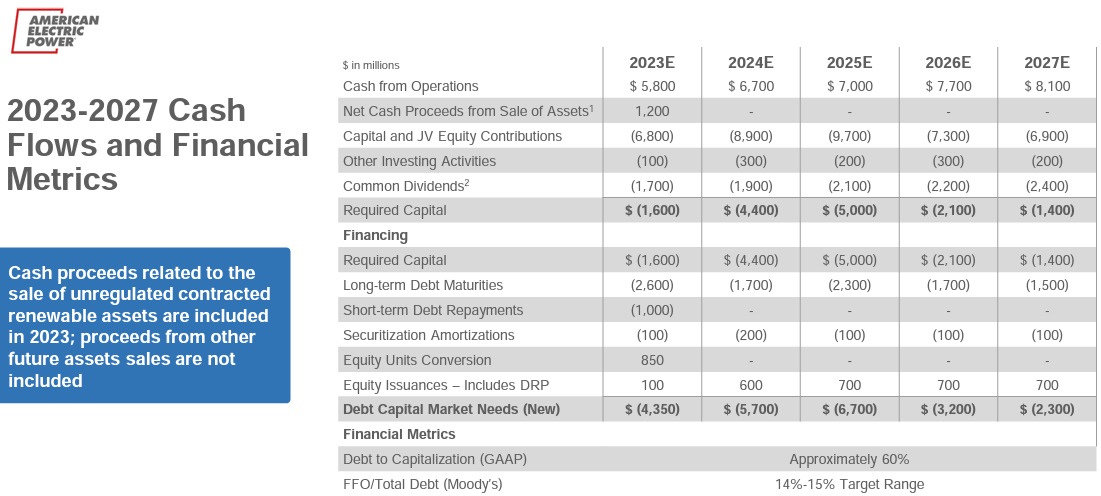

Risks to AEP include potential for a warmer than expected winter season, which may mute customer demand. Plus, it has funding needs to support its capital investment plan. This may result in higher interest expense in the current higher-for-longer environment. As shown below, AEP will require $2.3 to $6.7 billion in debt capital funding annually between now and 2027.

{kind=link}

It's worth noting, however, that the above projections don't include potential asset sales, including that of AEP's unregulated renewable energy assets that could materially decrease its external capital needs. AEP also carries a strong balance sheet with an A- credit rating from S&P to weather near-term impacts from higher interest rates, with a targeted FFO/Debt ratio of 14-15% that sits above the 11% thresholds set by Moody's and S&P. AEP also has strong $3.07 billion of liquidity consisting of $305 million in cash and with the balance in availability in revolving credit facilities.

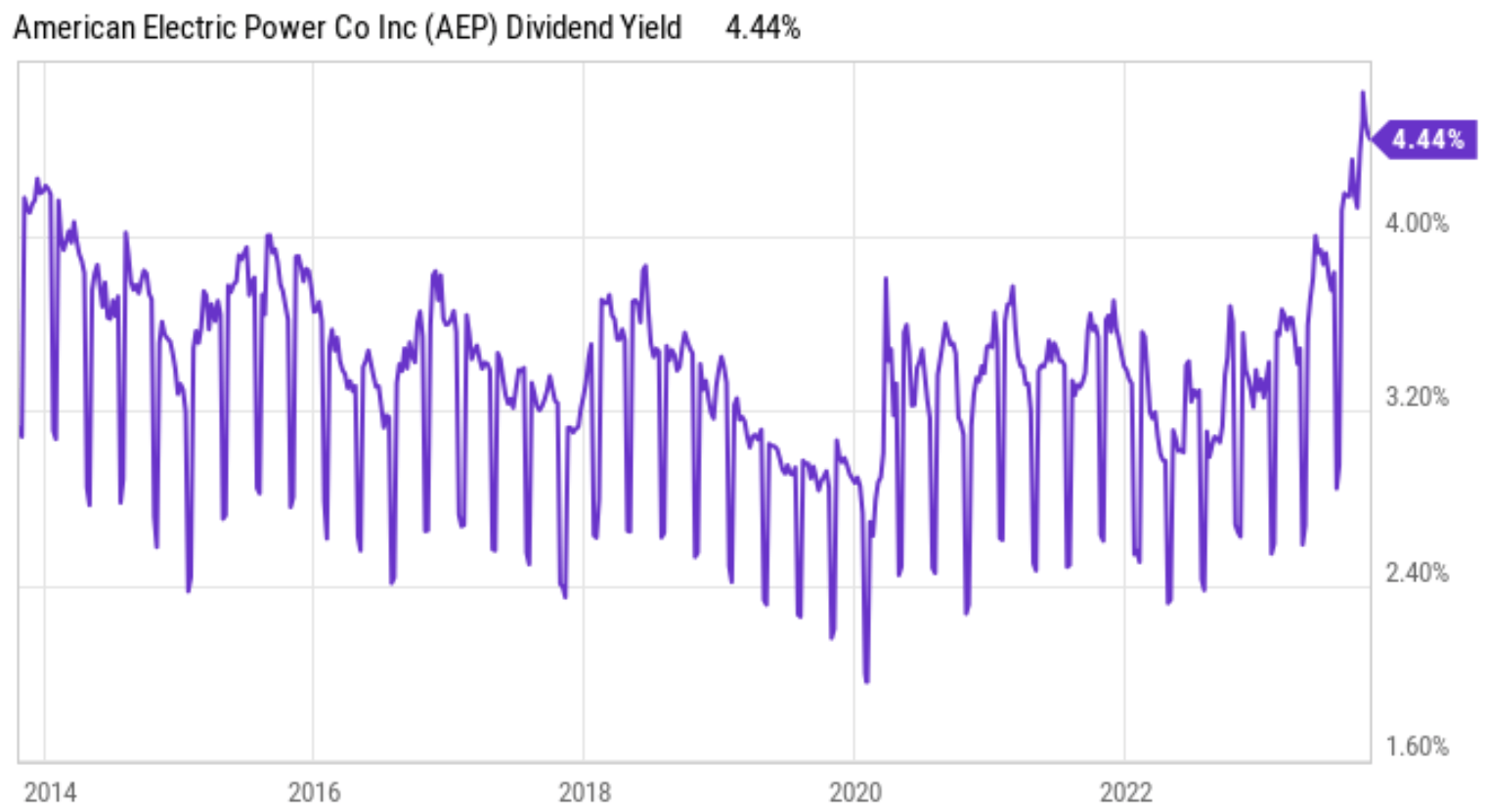

Meanwhile, AEP currently sports an attractive 4.7% forward dividend yield that's well-covered by a 67% payout ratio. Management seeks to grow the dividend at a 6-7% annual rate, in-line with the earnings growth target, and this is exemplified by the 6% dividend bump announced this week. As shown below, AEP's dividend yield currently sits at its highest point in 10+ years.

(Note: The following chart shows TTM yield. Forward yield is 4.7%)

{kind=link}

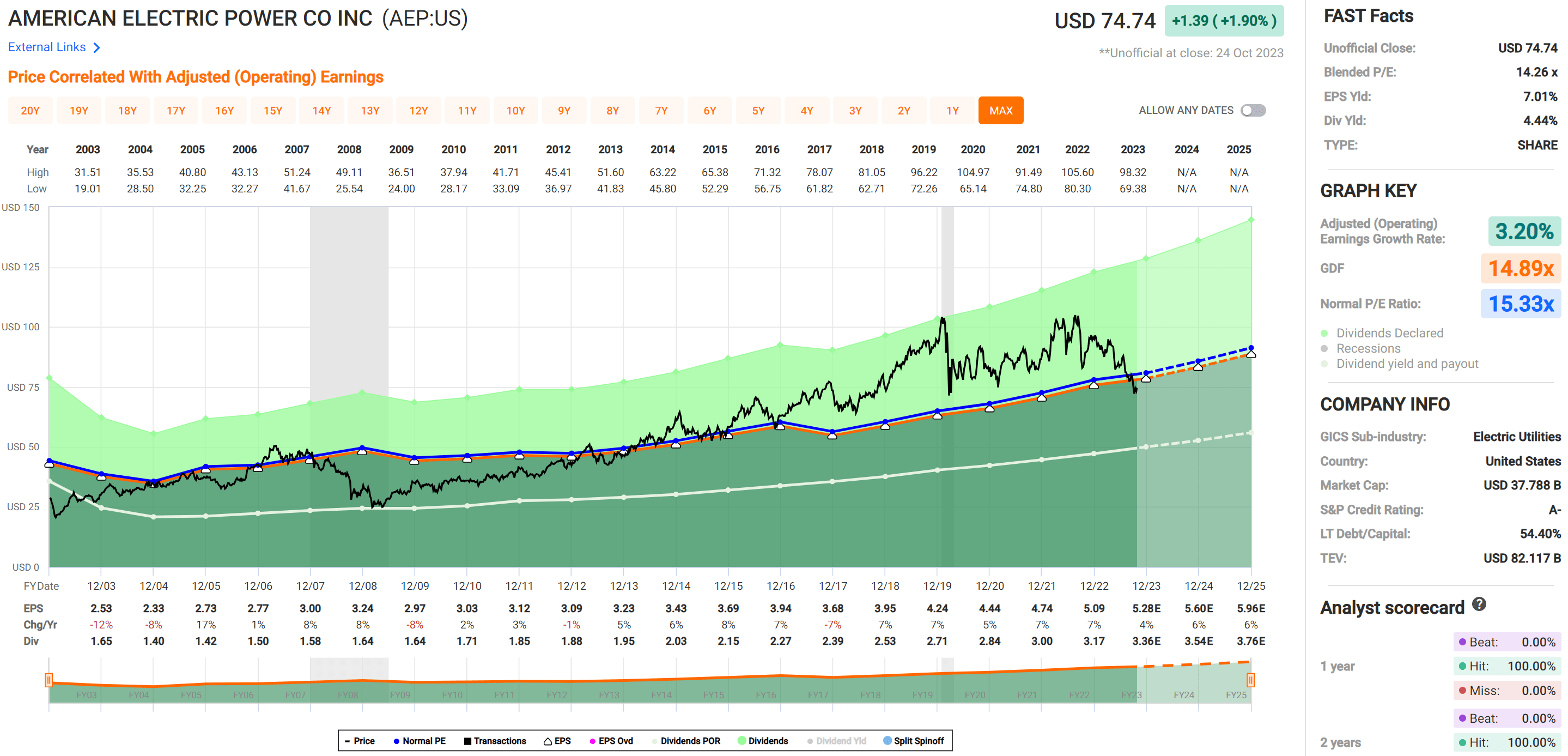

Lastly, I see value in AEP at the current price of $74.74 with a forward PE of 14.2, sitting below its normal PE of 15.3. While this doesn't scream bargain, it's worth considering that quality enterprises like AEP rarely go on sale unless if there is fundamentally broken with the business, and that's something that I simply don't see.

With a 4.7% dividend yield and 6-7% estimated long-term annual EPS growth, investors get potential 11-12% annual total returns. This outpaces the 9-10% historical annual total return of the S&P 500 with a far higher yield and far less potential volatility considering the regulated nature of AEP's earnings.

{kind=link}

Investor Takeaway

In conclusion, AEP appears to be a stable and well-managed utility company with strong cost management and growth prospects. While near-term inflationary pressures may have impacted customer demand, the company has a solid track record for maintaining capital efficiency and remains focused on long-term growth with investments in its regulated utilities. With a historically high dividend yield that was just raised and potential for annual total returns above market average, I view AEP as being a solid 'Buy' at the current discounted valuation.

For further details see:

American Electric Power: Buy This Dividend Giant Before Everyone Else Does