AEP - American Electric Power: Buy This Utility For Income And Growth

2023-09-15 08:49:38 ET

Summary

- American Electric Power's operating EPS payout ratio should remain in the low-60% range in 2023.

- The company's revenue and operating EPS both fell in the second quarter due to macroeconomic headwinds.

- My inputs into the discounted cash flows model and dividend discount model show shares of the electric utility to be 16% undervalued.

- American Electric Power's 4.2% dividend yield and target.

What makes a dividend growth investing portfolio successful? The answer to this question is to arguably pick businesses that sell necessary goods and/or services to customers for which there is no substitute.

One such service that fits this description quite well is electric utilities. That is because most people couldn't live without electricity in economically developed countries. As one of the biggest publicly traded electric utilities around, American Electric Power ( AEP ) is one of the first that comes to mind. And it may also be one of the best. For the first time since May , let's refresh the reasons why.

A Safe and Competitive Starting Yield For The Current Environment

A good baseline as an income investor is to consider the risk-free rate (the 10-year U.S. treasury rate), which is currently 4.3% . The stability provided by U.S. treasuries is a major plus for investors. But for investors looking to grow purchasing power, this investment vehicle simply isn't going to cut it. That is why, with a 4.1% dividend yield, American Electric Power or AEP may be the better option for investors who can handle the risks.

First off, investors can be reasonably confident that the company won't be cutting its dividend anytime soon. AEP posted $5.09 in operating EPS in 2022. Using the $3.17 in dividends per share that were paid last year, this is a 62.3% operating EPS payout ratio. For perspective, that is well within the company's targeted operating EPS payout ratio of 60% to 70% (per slide 13 of 39 of AEP Q2 2023 Earnings Presentation ).

AEP has set $5.29 in operating EPS as its midpoint guidance for 2023 ($5.19 to $5.39 according to page 2 of 9 of AEP Q2 2023 earnings press release ). Assuming a Q4 dividend per share of $0.88, the company is slated to pay $3.37 in dividends per share this year. That works out to a 63.7% operating EPS payout ratio. Because this payout ratio is on the low end of its targeted range, I believe dividend growth could come in marginally ahead of operating EPS growth moving forward.

Considering that AEP anticipates 6% to 7% annual operating EPS growth (also sourced from slide 13 of 39 of AEP Q2 2023 Earnings Presentation), this is why I am reaffirming my long-term annual dividend growth rate of 6.25%.

Higher Interest Rates And Mild Weather Are Holding The Company Back

{kind=link}

AEP Q2 2023 Earnings Press Release

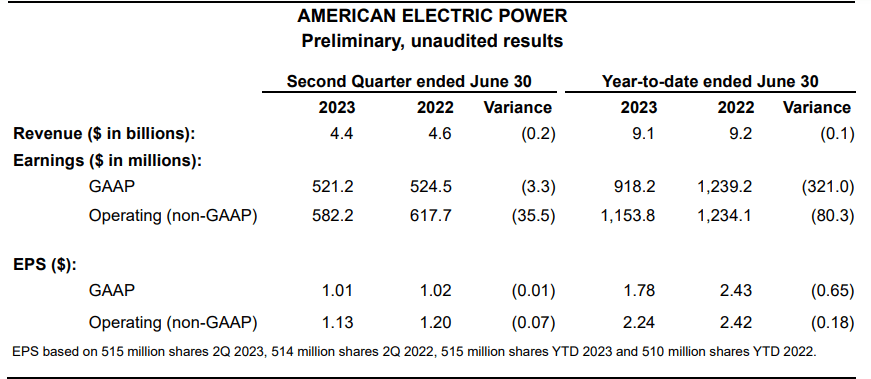

Sometimes, obstacles can impede the progress of even the best companies. That is what looks to have happened to AEP in the second quarter concluded on June 30. The electric utility's total revenue declined by 4.3% year over year to $4.4 billion during the quarter. More favorable weather in the year-ago period coupled with mild weather for the second quarter created the perfect storm: This is what led the company's total sale of kilowatt-hours (KWH) to decrease by 3.8% year over year to 91,029 in the quarter. That explains how AEP's topline contracted during the quarter.

The company's operating EPS moved lower by 5.8% over the year-ago period to $1.13 for the second quarter. Aside from the lower revenue base, AEP also faced higher interest expenses from soaring interest rates - - accounting for a $0.17 hit to operating EPS (details in previous two paragraphs sourced from AEP Q2 2023 earnings press release and AEP Q2 2023 Earnings Presentation).

With 40K miles of transmission lines (the most in the country) and 225K miles of distribution lines (one of the largest systems in the country), AEP holds the distinction of being an industry leader. As the company spends $40 billion on upgrading and expanding its infrastructure in the next five years, this should remain the case. That is what supports its underlying annual operating EPS target of 6% to 7% for the long term.

AEP believes that through a combination of (mostly) debt issuances and equity issuances, its debt-to-capitalization ratio will stay in the 60% range in the years ahead. Along with a qualified pension funding ratio of 102% in the second quarter, this backs up the argument that AEP is a financially sturdy business (info in prior two paragraphs according to AEP Q2 2023 Earnings Presentation).

Risks To Consider

All things considered; AEP is holding up well. However, the utility still faces risks.

After the inflation data that was reported for August 2023, it's worth noting that some downside could still be ahead for AEP. This is because even with interest rates as high as they currently are, inflation still came in at 3.7% for last month - - well above the Federal Reserve's 2% target. That came in higher than the 3.6% rate that analysts were expecting. Sure, progress is being made at taming inflation. But based on these results, it appears as though interest rates may need to go a bit higher and stay there for a while longer.

Besides the higher interest rates that will pressure AEP's profits further in the near term, this also raises the risk that a worse-than-expected recession could materialize. That could temporarily reduce the demand from commercial and industrial customers.

Now Is A Buying Opportunity

Sitting over 20% off its 52-week-high, shares of AEP seem to be at least somewhat cheaply valued. As evidence of this claim, let's take a look at two valuation models.

{kind=link}

Money Chimp

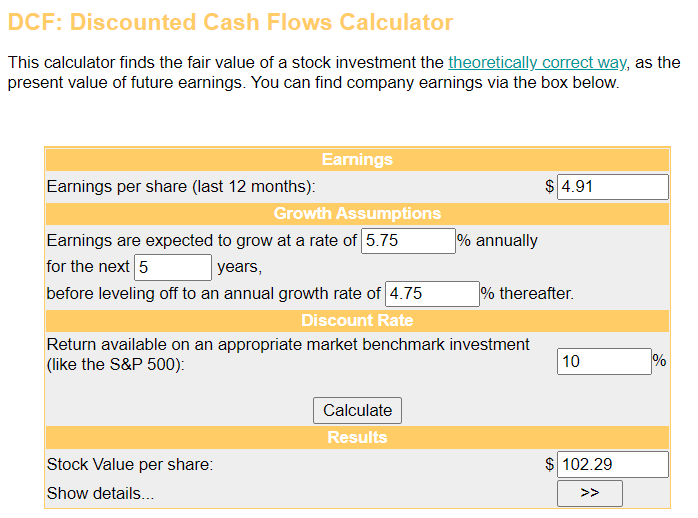

The first valuation model that I will deploy to value AEP's shares is the discounted cash flows model or DCF model. This valuation model is comprised of three inputs.

The first input for the DCF model is the trailing 12 months of operating EPS. For AEP, the company has generated $4.91 in operating EPS in the last four quarters.

The next input in the DCF model is growth predictions. Building in a slight margin of safety, I will use a 5.75% annual operating EPS growth rate for five years and a slowdown to 4.75% annually in the years that follow.

The final input for the DCF model is the discount rate. This is another way of saying the annual total return rate. My required annual total return rate is 10%.

Plugging these inputs into the DCF model, I get a fair value of $102.29 a share. That indicates shares of AEP are trading at a 21.3% discount to fair value and offer a 27.1% upside from the current price of $80.50 a share (as of September 14, 2023).

Investopedia

The other valuation model that I'm going to use to estimate the fair value of AEP's shares is the dividend discount model. This valuation model also has three inputs.

The expected dividend per share is the first input in the DDM. AEP's annualized dividend per share is currently $3.32.

The cost of capital equity or annual total return rate is the second input for the DDM. I will use 10% for this input.

The annual dividend growth rate is the third input in the DDM. I'll assume a 6.25% annual dividend growth rate for AEP.

Using these inputs for the DDM, I arrive at a fair value of $88.53 a share. This means that shares of AEP are priced 9.1% below fair value and could provide a 10% capital appreciation from the current share price.

Blending these two fair values, I compute a fair value of $95.41. That suggests that AEP's shares are trading at a 15.6% discount to fair value and could have an 18.5% upside from the current share price.

Summary: An Income, Growth, And Total Returns Trifecta

AEP is likely just weeks away from announcing another dividend increase. Given the company's viable operating EPS payout ratio and healthy growth potential, it should have many more years of dividend growth left in its future.

Topping it off, shares of AEP could be undervalued by around 16% at the current share price. Due to the risk of further downside from additional interest rate hikes, the stock isn't yet a strong buy. But it's not a bad buy for investors seeking a mix of yield, growth, and total returns.

For further details see:

American Electric Power: Buy This Utility For Income And Growth