AEP - American Electric Power Is A Solid Low-Volatility Buy (Rating Upgrade)

2023-12-03 03:21:23 ET

Summary

- American Electric Power enjoys solid growth in its sales, EPS, and dividends.

- It is engaged in strategic investments that are renewables-focused and will lead to further future growth.

- The combination of balanced prospects, manageable risks, and decent valuation makes the company a BUY.

Introduction

I have invested in the utilities sector since starting my dividend growth portfolio. This is an excellent sector for investors seeking stable income with stable growth and are willing to have lower total returns but with lower volatility. As interest rates peaking at around 5%, and the market is pricing interest rates to decrease in 2024, it may be an excellent opportunity to increase exposure to the sector.

While I believe the entire industry is attractive, American Electric Power ( AEP ) is exciting. I wrote about the company for the first time in 2016 and found it a BUY. Since then, it has been chiefly around HOLD due to the valuation. In 2020, during the pandemic, I analyzed the company while it was trading for 22 times its earnings.

Seeking Alpha's company overview shows that:

American Electric Power is an electric public utility holding company that engages in the generation, transmission, and distribution of electricity for sale to retail and wholesale customers in the United States. The company generates electricity using coal and lignite, natural gas, renewable, nuclear, hydro, solar, wind, and other energy sources. It also supplies and markets electric power at wholesale to other electric utility companies, rural electric cooperatives, municipalities, and other market participants.

Fundamentals

The revenues of American Electric Power have increased by 30% over the last decade, which equates to almost 3% annually. The company grows organically by selling to new clients, enjoying price hikes and higher demand. At the same time, it also engages in M&A activities when it sells and buys power plants to optimize its portfolio. It has completed selling its non-regulated portfolio to focus on the regulated business. In the future, as seen on Seeking Alpha, the analyst consensus expects American Electric Power to keep growing sales at an annual rate of ~3% in the medium term.

The company's EPS (earnings per share) has increased at a faster pace of 43% during the same decade. The company managed to achieve an almost 4% growth rate despite an increase in the number of shares. It can be attributed to changes in the portfolio that focused on more lucrative and profitable assets. In the future, the company, in the Q3 2023 conference call, also reaffirmed its projected long-term growth rate of 6% to 7%. Moreover, as seen on Seeking Alpha, the analyst consensus expects American Electric Power to keep growing EPS at an annual rate of ~5% in the medium term.

The company has been increasing the dividend annually since 2008 and hasn't reduced it for almost twenty years. Therefore, it looks like a reliable dividend. The current entry yield is attractive and stands at 4.4%, following the 6% increase in October. While the company pays a generous dividend, the payout ratio is 76.5%. This is a manageable payout ratio as the company is a regulated utility with a stable cash flow. Still, it means we are unlikely to see higher dividend increases than the company's EPS growth rate. Thus, investors should expect an additional ~5% increase in the medium term.

In addition to dividends, companies, especially cash-flowing companies, tend to return capital to shareholders via buybacks. Buybacks support EPS growth as the share repurchase plans reduce the number of outstanding shares. American Electric Power has seen its number of shares increase by 8% over the last decade. The increase results from negative free cash flow associated with the company's investments. It doesn't leave room for buybacks, and the company has to issue shares to finance growth.

Valuation

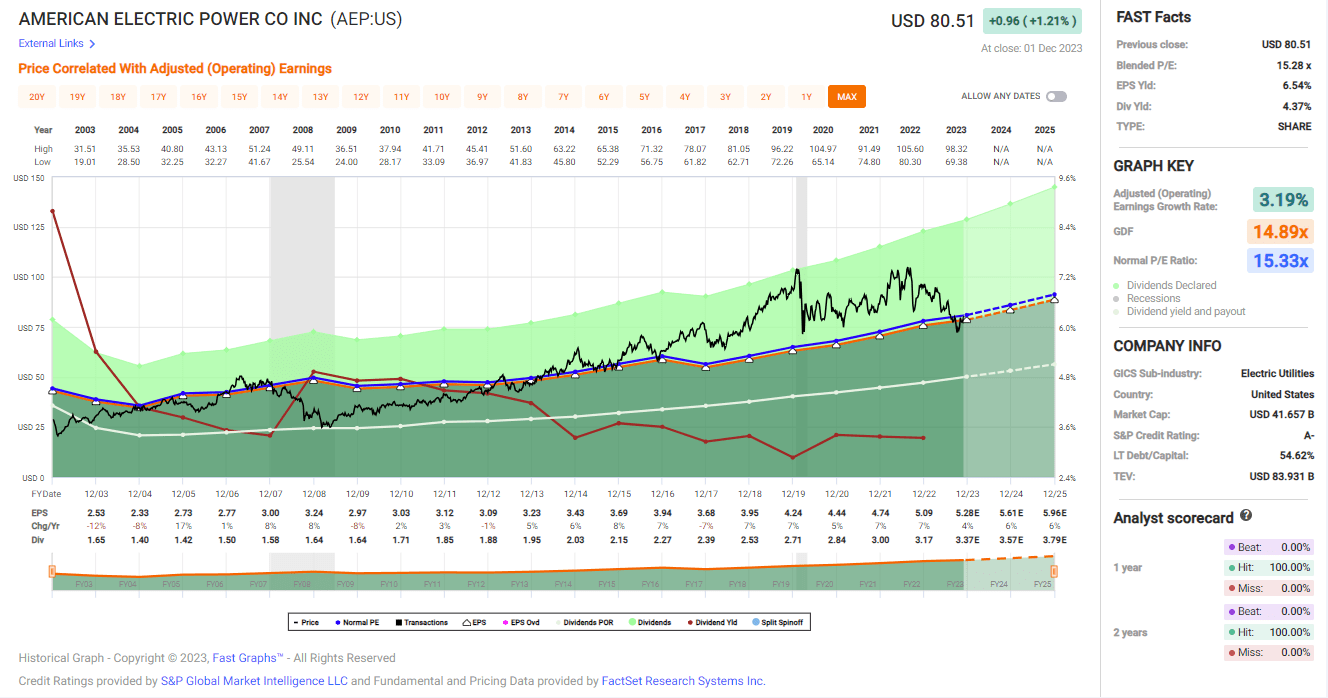

The P/E (price to earnings) ratio of American Electric Power stands at 15 when using the 2023 EPS forecast for the company. This is a similar valuation to the one I saw when I analyzed the company in 2016 and found it to be a BUY and 33% lower compared to the valuation in 2020 when I rated it HOLD. This is also close to our lowest valuation over the last twelve months. Therefore, the current valuation seems like a decent entry point to a solid, growing company.

The graph below from Fast Graphs shows that the company is at a decent entry point. The average P/E ratio of the company over the last two decades stands at 15.3. At the same time, the annual growth rate in the past 20 years was 3.2%. While the current valuation aligns with the historical, the EPS growth expectations are much higher, as the company forecasts 6%-7% annual growth over the long run.

{kind=link}

Opportunities

The most significant opportunity is the expansion of the renewable energy portfolio. The company is strategically investing $8.6 billion in regulated renewables over the next five years, with $6 billion already approved. These investments encompass significant wind and solar projects across various service territories, contributing to 2,364 megawatts. Progress in obtaining regulatory approvals for notable projects, such as the 995.5-megawatt portfolio for Public Service Company of Oklahoma ((PSO)) and the 999-megawatt portfolio for Southwestern Electric Power Company (SWEPCO), reflects a commitment to a sustainable energy future .

"We now have a total of $6 billion of the investment plan approved and an additional $800 million currently before commissions for approval."

(Julia Sloat- Chairman, President & CEO, Q3 2023 Conference Call)

Another opportunity is the simplification and portfolio derisking as the company sells unregulated assets. Ongoing efforts are directed at streamlining and derisking the business through portfolio management and asset sales. The recent completion of the sale of a 1,365-megawatt unregulated renewables portfolio is part of this strategy. The company is actively divesting non-core assets, including retail and distributed resources businesses, with proceeds to reinforce the regulated industry and manage the balance sheet .

"This quarter, we made progress on our ongoing efforts to simplify and derisk our business profile through portfolio management."

(Julia Sloat- Chairman, President & CEO, Q3 2023 Conference Call)

Lastly, the company is also poised to enjoy economic development and commercial load growth. The company is observing a robust increase in commercial load, primarily driven by Ohio, Texas, and Indiana data centers. The notable 7.5% growth in commercial load during the third quarter shows the success of ongoing efforts to facilitate economic development. The company must find growth paths in Texas, which enjoys favorable demographics, and its slower-growing areas, such as Ohio. This aligns with a broader strategy to attract projects, contributing to sustained commercial load growth, and it allows it to provide energy to the client's business needs.

"We expect the pace of year-over-year growth in our commercial load to moderate some in 2024 as new projects work their way through the queue."

(Chuck Zebula, EVP & CFO, Q3 2023 Conference Call)

Risks

When you're a regulated utility whose prices are decided by regulators, regulatory and legislative challenges are always a dominant risk. Challenges related to closing the authorized versus earned Return on Equity gap persist across service territories. With an ROE of 8.7% in the third quarter, impacted by weather factors, the company acknowledges the need for continued focus on regulatory and legislative initiatives. Balancing federal, state, and customer preferences is crucial in navigating the complexities of regulatory landscapes .

"Closing the gap will remain a primary focus into 2024 as we take federal state and customer preferences top of mind, along with meeting the needs of our communities."

(Julia Sloat- Chairman, President & CEO, Q3 2023 Conference Call)

The company has to deal with the risks of climate change and weather sensitivity while dealing with higher rates, making it more expensive to borrow flexibly. Acknowledging the impact of rising interest rates and a prolonged higher interest rate environment, the company emphasizes the importance of managing business operations within this context. The flexible business plan is designed to deliver on financial commitments while considering variables such as mild weather in the year's first half. Proactively managing economic development, load outlook, and operating and maintenance activities is vital in addressing potential challenges .

"We have a flexible business plan that allows us to deliver on our financial commitments while considering mild weather in the first half of the year and the higher for longer interest rate environment."

(Julia Sloat- Chairman, President & CEO, Q3 2023 Conference Call)

Another risk American Electric Power deals with is fuel cost recovery and the challenges associated with the associated regulatory proceedings. The management of fuel cost recovery remains a top priority, with the company actively engaged in regulatory proceedings, particularly in cases like fuel recovery in West Virginia. The shrinking deferred fuel balance across vertically integrated utilities totaling $1.2 billion as of the end of the third quarter underscores efforts to balance cost recovery with customer impact. Engaging stakeholders and navigating regulatory processes are crucial in resolving fuel recovery cases and ensuring financial stability.

"The management of fuel cost recovery is a top priority with AP's deferred fuel balance across our vertically integrated utilities shrinking sequentially and totaling $1.2 billion as of the end of the third quarter of this year."

(Julia Sloat- Chairman, President & CEO, Q3 2023 Conference Call)

Conclusions

To conclude, the company is a solid pick in the realm of utilities, consistently demonstrating growth and a commitment to shareholders through steady dividends. Noteworthy initiatives, like substantial investments in renewables, reflect a forward-thinking approach, and its focus on regulated assets will increase resilience. Moreover, the company is trading for what I believe to be an attractive valuation.

Despite acknowledged risks, the Q3 2023 conference call offers insights that increase my confidence, making the company's shares a decent prospect for those seeking a blend of reliability and growth, fittingly characterized as a solid BUY. If the company executes well, investors will enjoy a 4% dividend and a 6%+ growth rate.

For further details see:

American Electric Power Is A Solid, Low-Volatility Buy (Rating Upgrade)