V - American Express: A Business Worth Owning For A Lifetime

2023-04-10 14:09:06 ET

Summary

- American Express has proven they have a resilient business model which is able to consistently grow and persist for long periods of time.

- Amex returns a tremendous amount of capital back to their shareholders which unlocks large shareholder value over the long run.

- They maintain a wealthy consumer base which allows for strong spending even during economic downturns and allows them to warrant a premium for their business.

Investment Thesis:

American Express ( AXP ) is a phenomenal business that investors should consider owning for a lifetime in our view. First, it is important to discuss Amex's business model and how it has proven to be strong as well as stand the test of time. American Express (Amex) is a global payments company which provides its customers with products and services such as credit cards, charge cards, and lending services to everyday consumers and businesses.

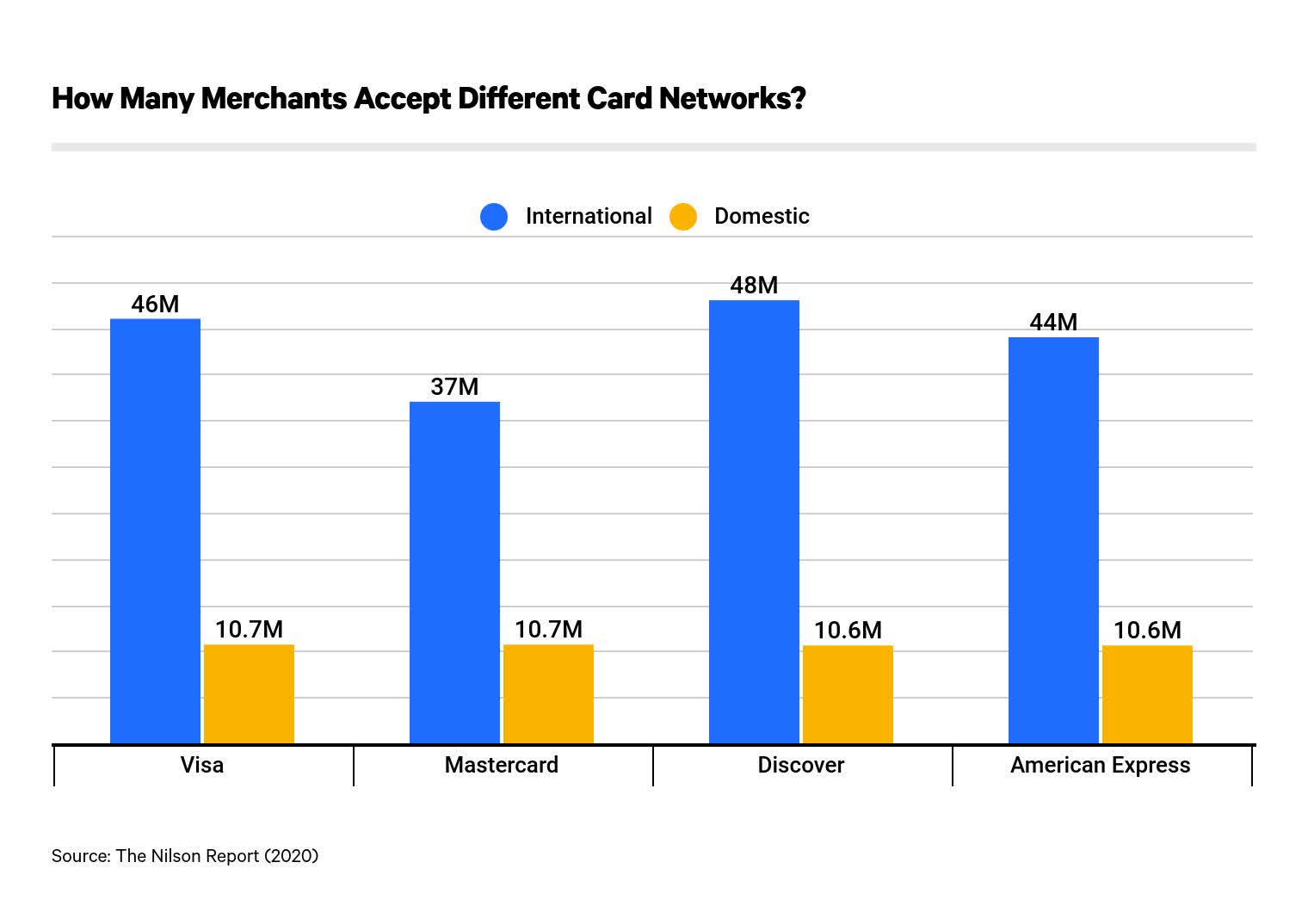

What makes Amex's business great is the toll booth nature where they are able to collect a small fee off billions of transactions while also having established themselves among wealthy consumers therefore allowing them to warrant a premium relative to other credit card companies. One example of this is that the average transaction on an Amex card is $141 compared to $80 and $75 for Visa ( V ) and Mastercard ( MA ).

Average value of transactions per credit card (Statista: The Nilson Report)

Notoriously, Amex has charged higher fees on their cards relative to others which has led to some businesses not accepting their cards. Fortunately, in recent years the gap in fees between the major credit providers has closed leading to broader acceptance of Amex credit cards. Furthermore, Amex also has a unique closed loop network where they maintain direct relationships with their card members (as issuers) and merchants (as acquirers) whereas their primary competitors of Visa and Mastercard do not do so.

{kind=link}

Another primary selling point for the stock is the resilient nature of the business as well as continued growth. Overall, credit card businesses are typically subject to regular economic fluctuations yet Amex is quite different. Due to the wealthy nature of Amex's clients, their earnings are typically not materially impacted by economic downturns as wealthier individuals tend to be impacted less by economic downturns. This is reflected with their revenues growing 25% in 2022 as well as guidance towards 15-17% revenue growth going forward.

Evidently, American Express has a phenomenal core business which is poised for strong growth going forward and has also proven to be strong during harsh times. As a result of this, not only can the business warrant a high multiple, but it also makes it a strong candidate to own for virtually a lifetime.

Prioritization of Shareholder Value:

Amex's core business is a strong selling point of the stock, yet, their strong prioritization of shareholder value has historically been one of the strongest factors driving returns. Famously, Buffett initially bought a 10% stake in Amex from the 1960's through 1990's, yet, he now own 20% of American Express without buying a single additional share. Why? Their extremely aggressive share buybacks. One of my favorite things to see in companies that I own are large share buybacks. Not only are buybacks more tax efficient than dividends, but when businesses buy back shares at undervalued prices, they are retiring shares at lower prices than they will be in the future thereby furthering the effects of their investments relative to a simple dividend. Besides the share buybacks, Amex also provides a dividend with a yield of 1.5% and is continuing to rapidly increase it. Just this past year, Amex raised their dividend by an additional 15% while also authorizing the repurchase of 120 million shares which accounts for roughly 16% of their market cap.

Amex shares outstanding (investor place)

Clearly, Amex returns a tremendous portion of their capital towards shareholders while also investing capital to grow their core business at a steady rate.

Growth Trajectory:

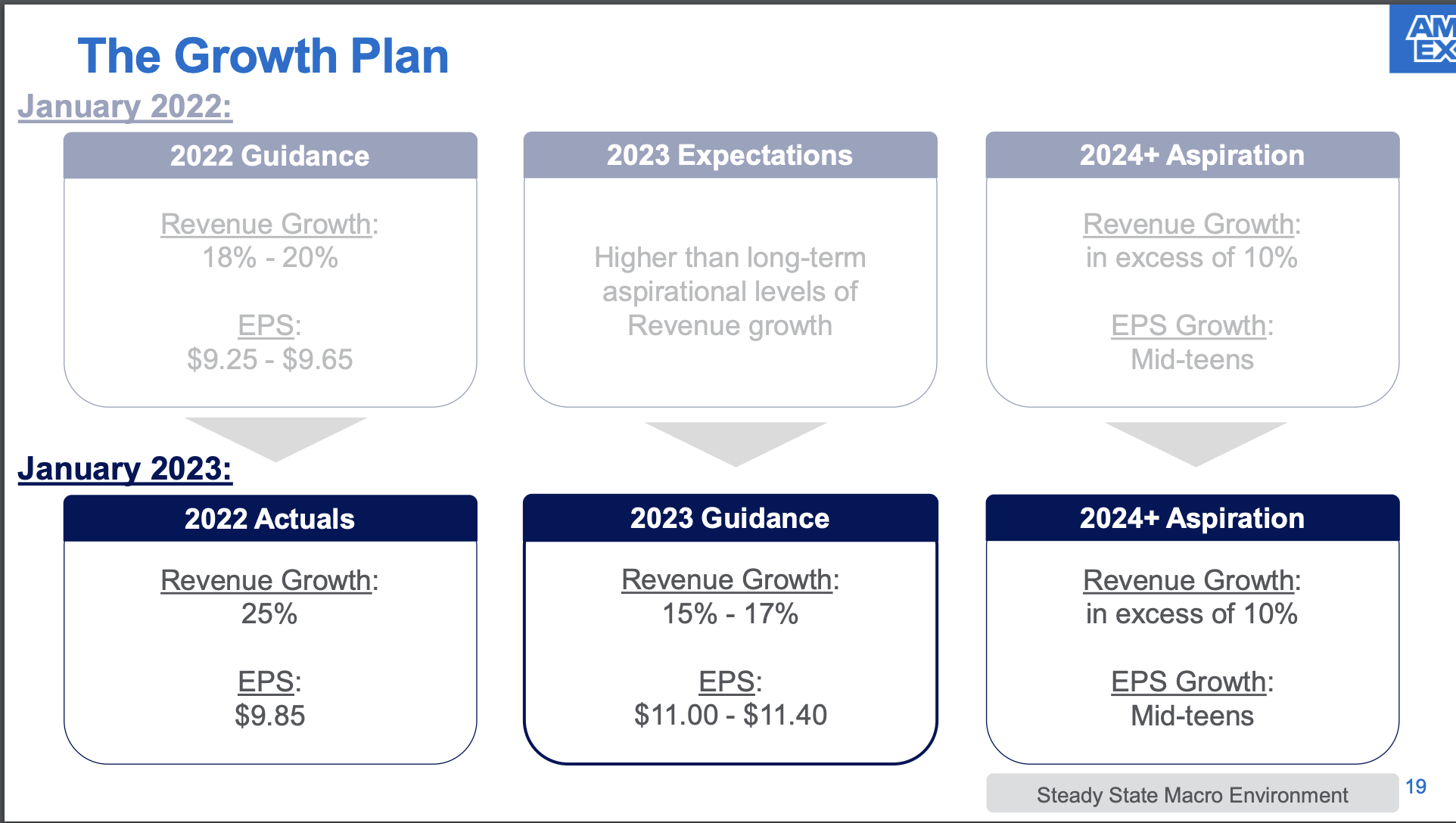

Although American Express is an extremely established and developed business, their growth is surprisingly rapid and persistent. As previously noted, Amex surpassed their revenue growth guidance to deliver 25% top line growth and is projecting 15-17% growth for the next year. This high teens growth is phenomenal for a developed business that is trading at 14 times forward earnings and trailing price to free cash flow of 6. Furthermore, they are also guiding for long term revenue growth in excess of 10% as well as mid-teens EPS growth.

Amex Guidance - Investor Relations (American Express Investor Relations)

{kind=link}

In order to achieve their growth projections, Amex is focusing on four key growth strategies.

First, Amex plans on continuing to expand the benefits they provide to their consumers in order to expand their leadership in the premium consumer space. American Express has notable partnerships with Delta Airlines, Marriott, and Hilton to name a few which allow them to offer large benefits to their premium consumers thereby allowing them to maintain their wealthy consumer base.

Then, Amex wants to focus on furthering their position in the commercial payments space and expanding their offering in banking and finance. Essentially, Amex has a small banking arm where they offer savings accounts, CD's, and lend money which is often pointed to as the reason they are valued much cheaper relative to their credit card peers. Within their banking division, Amex tends to loan to their wealthy customer base therefore they have a very strong loan book.

Third, American Express wants to continue enhancing the advantages of their closed loop network by working closely with merchants to strengthen the value they provide and offer additional services. The reason that Amex has been able to charge higher fees than other credit providers is because they operate under the philosophy that merchants should pay a premium in order to unlock their premium consumer base. By continuing to enhance their relationship with merchants, it allows for continued broad acceptance of their cards paired with strong fees.

Lastly, they want to continue expanding their role in their customers' digital lives by offering additional digital services. Evidently, Amex's growth strategies are working as they continue to deliver rapid top and bottom line growth.

Valuation:

Now that we have noted the primary components of the business, it is crucial we value it in order to determine what we should pay for the business. Due to Amex's banking division, valuing the business can become slightly more complicated, yet I believe that utilizing a simple DCF model would be adequate in order to determine its value.

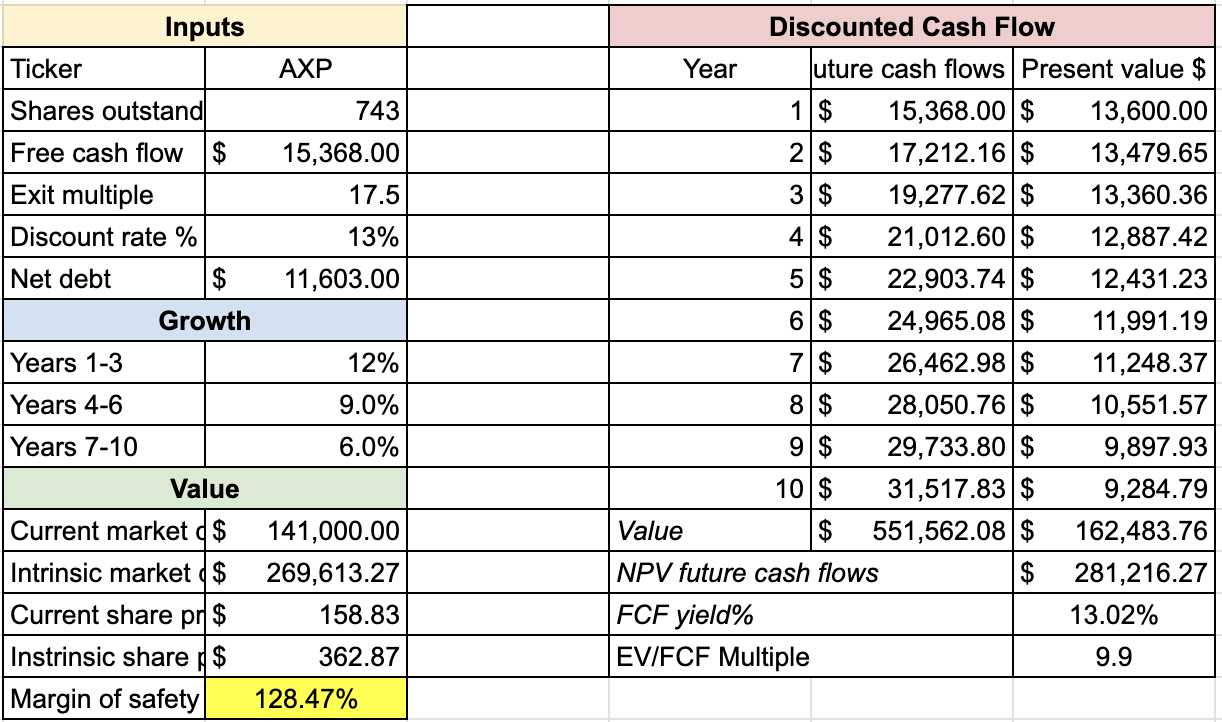

For this DCF model, we will subtract net debt from their value ($11,603 million), assume 12%, 9%, and 6% growth for the next 10 years which is in line with their guidance, and assign a multiple of 17.5 due to the extremely high quality and fast growing nature of the business.

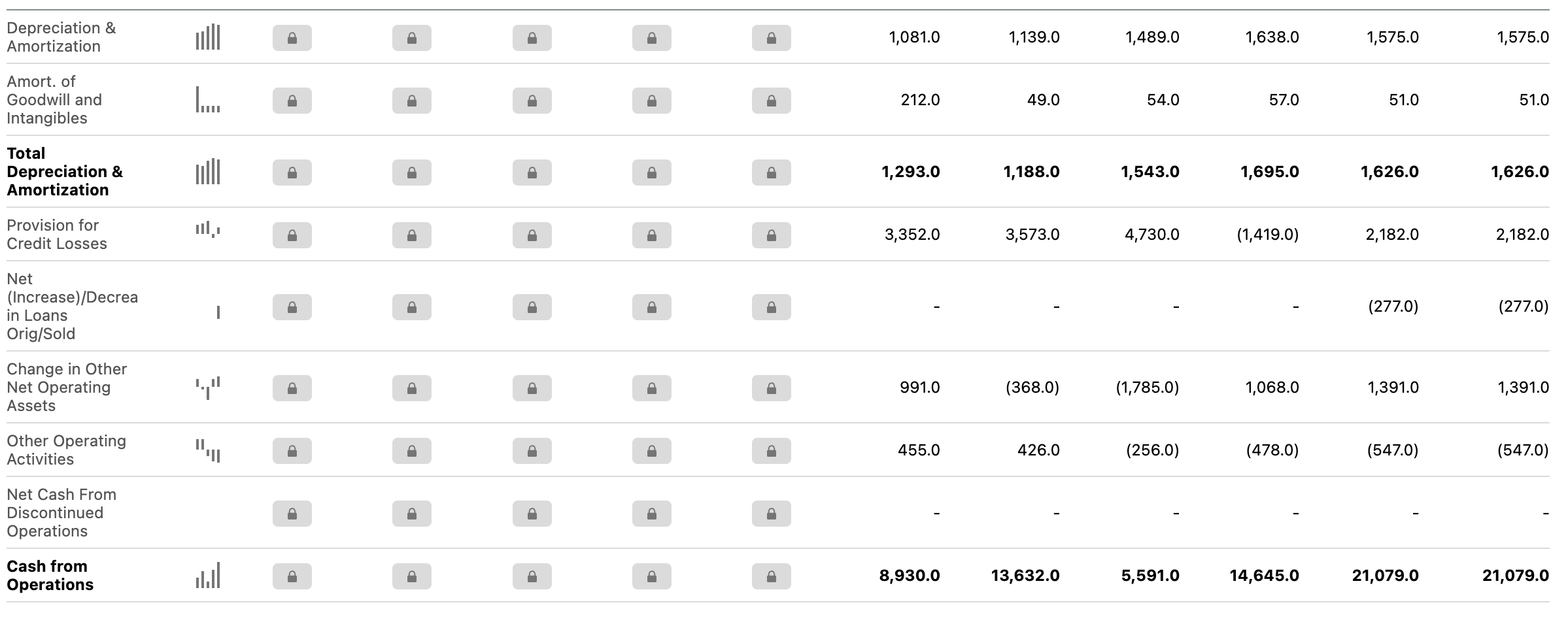

Then, in regards to profitability, it becomes slightly harder to assign a proper number. Under Amex's midpoint guidance for EPS of $11.20 a share, they would have 8.3 billion in profit, yet, they had roughly $21 billion in operating cash flows and just $1.8 billion in capex. The reason for their extremely high cash flows is partially a result of the nature of the business and a large increase in accounts payables & other liabilities which was reflected in their cash flow statement as $8,815 million was added back. Evidently, their cash flow cannot be sustained at $21 billion a year therefore if were to take the previous year's change in accounts payables & other liabilities ( $5,539 million) and substitute that in for a more normalized number, we would be left with $17,224 in operating cash flows.

{kind=link}

To calculate free cash flow, we would subtract their $1,856 million in capex to arrive at $15,368 million. Lastly, I utilize a discount rate of 13% for three main reasons.

1) I want to beat the market

2) I want to be compensated for the time I put towards research

3) By utilizing a discount rate that is above what the market does, it builds in an extra margin of safety as even if the stock underperforms my expectations, the returns would likely still be adequate.

Rasoli Research - AXP DCF model (Rasoli Research & Seeking Alpha Financials)

{kind=link}

Evidently, American Express appears tremendously undervalued at its current prices and poised to deliver market beating returns in the future.

Risk Factors:

Although Amex does appear to be extremely undervalued and maintain a strong business, there are some short term risks present.

Macroeconomic Environment:

The current macroeconomic environment is daunting and continues to poise short term troubles for all kinds of businesses. With the recent collapse of Silicon Valley Bank (SVB) and widespread trouble among regional banks such as First Republic ( FRC ), it has raised questions about an upcoming recession and its severity. Although we did enter a technical recession a few months ago when there was two consecutive quarters of GDP decline, overall employment was not impacted and the effects to the economy were minimal. With the recent collapse and damages to regional banks, if the economy were to enter a severe recession, Amex's earnings would likely be hurt as their wealthy consumer base would also be impacted by a recession of large magnitude. Furthermore, although Amex typically does lending to prime consumers, the profitability of their banking division could also be impacted. Overall, these are short term concerns which could impact Amex's earnings power yet over the long run the validity of their business remains constant.

Final Thoughts:

American Express has proven itself to have a strong business model due to the wealthy nature of their consumer base and ability to collect consistent fees with their credit card base. Over the lifetime of the business, Amex has delivered phenomenal shareholder value by returning a tremendous amount of capital to their shareholders in the form of share buybacks and dividends. Furthermore, they have been able to consistently beat their guidance and continue to grow their top and bottom line at a rapid clip through recent economic uncertainty. Overall, American Express presents itself as a great investment for the base of a portfolio and to own for a lifetime as it appears likely to deliver outsized returns with minimal risk.

For further details see:

American Express: A Business Worth Owning For A Lifetime