AXP - American Express: A Potential 'Forever Hold'

2024-01-17 01:34:15 ET

Summary

- American Express is a compounder, a stock that can grow at a higher-than-average rate for years and years.

- AXP has a high-moat business and is insulated from regulatory, monetary, and other risks.

- AXP has shown consistent growth in revenues and profits, has been buying back shares, and has outperformed the S&P 500.

- We expect these dynamics to continue well into the future due to the firm's strong competitive position.

- We rate AXP a "Buy".

In the world of stocks, there are many great public companies that have a solid return on invested capital, a strong set of products and services, and a competent management team.

However, there are comparatively few compounders - stocks that are able to grow at a higher-than-average rate for years and years, compounding an investment's capital many times over.

The difference may be difficult to spot at first, but it's there. Compounders are a different breed for a couple of reasons:

- They focus on demand for shares as well as supply of shares.

- They have high-moat businesses that go beyond having a solid offering.

- They are materially insulated from regulatory, monetary, and environmental threats.

American Express ( AXP ) is one such compounder.

Today, we'll cover the aspects of the company that make it extremely likely that it will outperform over time, as well as the present factors that make an investment in AXP stock at the current valuation a compelling investment idea.

If that sounds good, then let's get started.

What Makes A Compounder?

Like we mentioned, there are loads and loads of great public companies out there, but only a few should bear the title of "Compounder".

Many firms have great products, competent management teams, and solid competitive positions in their industries, but relatively few share all of the traits we discussed above.

First and foremost, companies that stand a chance of compounding an investment's capital over time need to focus on the supply and demand of their shares, something that is often overlooked by management.

Secondly , compounders need to have a solid moat. This goes beyond having a solid value proposition for their products or services - compounders need to be insulated from competition to the degree that they will have plenty of time to react disruptions in their industry.

Finally , compounders need to operate a business that offers asymmetric upside and removes risks from the equation. We're not talking about competitive risks; we're talking about macro risks. Consumer Sentiment, interest rates, the business cycle, natural disasters - you name it, the more risks a business is insulated from, the stronger of a case can be made for compounder status.

As an investor, once you've identified a compounder, doing well in the markets is simply a matter of waiting to buy it at the right price. That's what we think we have here today.

American Express's Advantages

For its part, AXP has all the hallmarks of a compounder, as we will outline.

The business grows continually, due to a strong offering, network effects, and efficiently run operations.

At the same time, AXP's financial results are self-hedging, to some degree, as the company continually makes money and grows revenue across business and rate cycles.

With few macro or competitive risks to worry about, AXP appears to meet all of the criteria we look for in a compounder.

Here's some more details to help flesh this idea out.

First, AXP has done well financially over time. The company's strong credit card franchise is entirely self-originated, which is unique. In most other arrangements, Banks ( JPM , BAC ) and card networks ( MA , V ) will unite to create an offer, with the bank taking on the credit side of the equation and the card network taking on the commission side of the equation.

This works out, because in the real world, the customer gets to access a line of revolving credit and make easy payments, the merchant pays the network a small fee to streamline their checkout process, and the bank gets to earn some fees and potentially interest on carried balances.

AXP takes this whole process and vertically integrates it with its own network, its own cards, and its own credit origination. This leads to lower margins than competitor networks like Visa and Mastercard, but higher nominal profits per user.

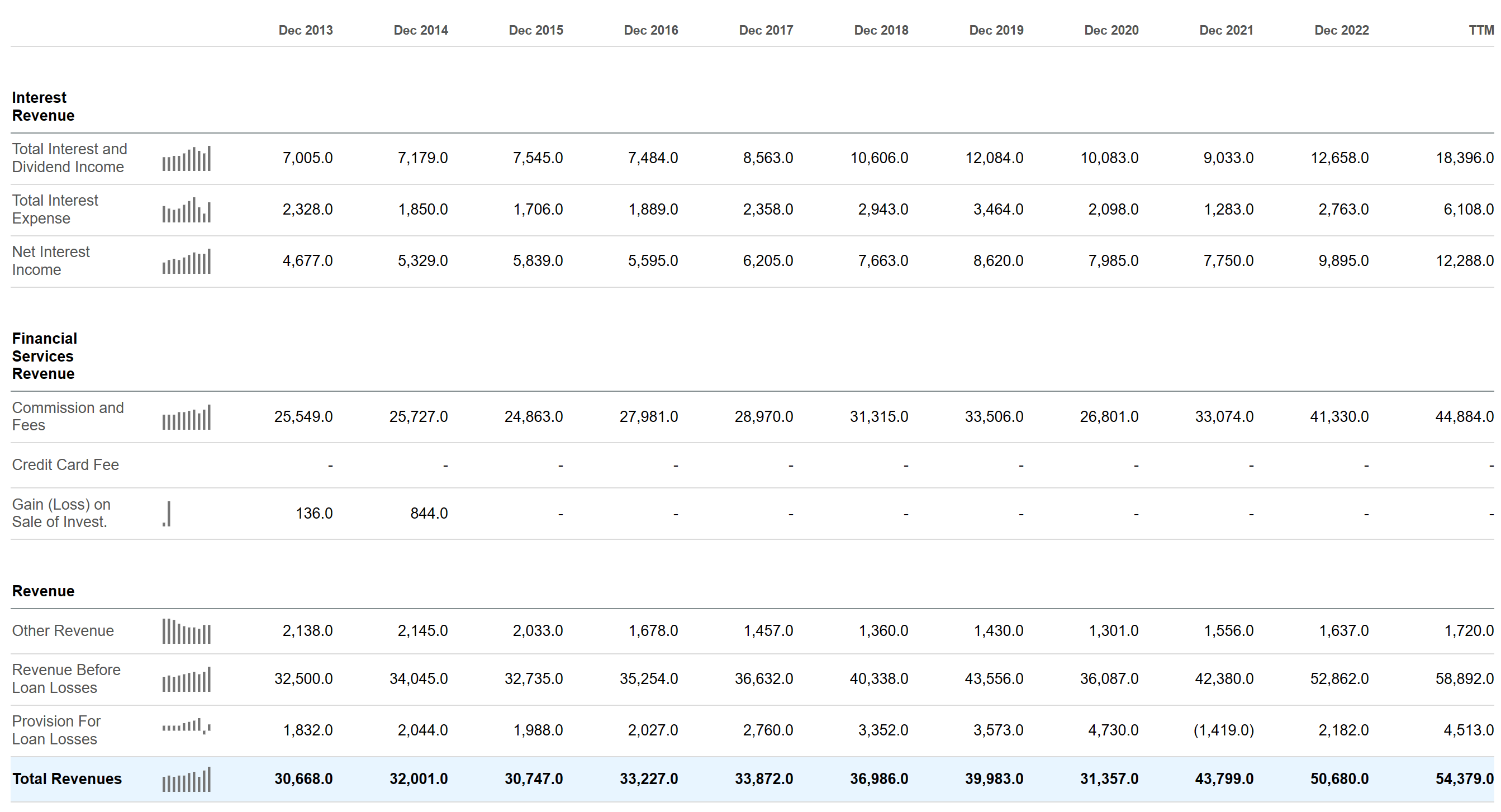

Functionally, AXP has grown revenues over time, from $30 billion to $54 billion over the last decade:

{kind=link}

This represents a compounded annual growth rate of 6%. On such a large revenue base, this is impressive growth. Average annual growth has been even better.

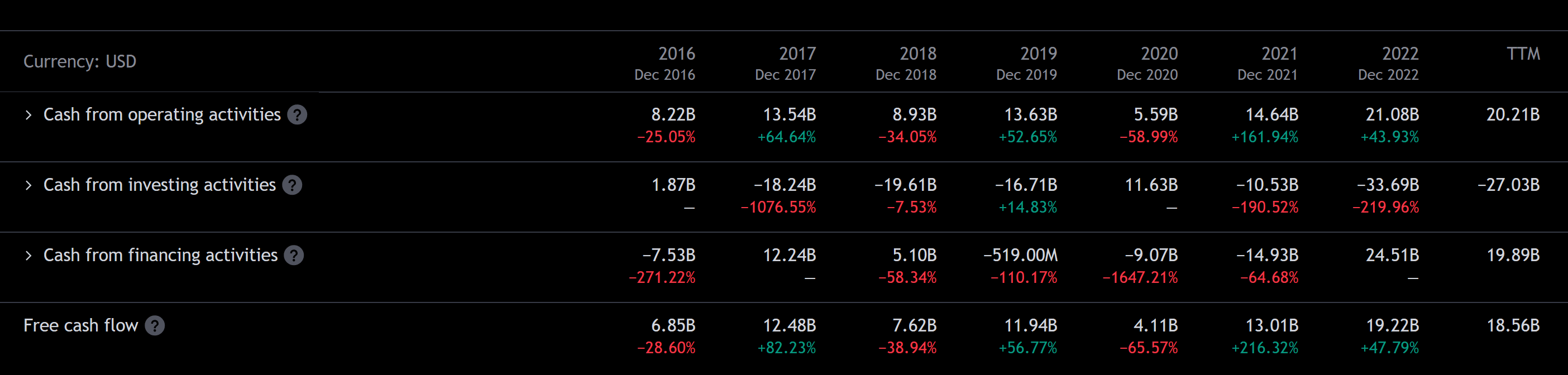

On the profits front, Free Cash Flow has grown from $6.5 billion in 2016 to $18.6 billion over the last twelve months, which represents a CAGR of 16.2%, higher than the revenue growth rate:

{kind=link}

This strong growth is largely a result of AXP's strong card network position, the company's ability to monetize its offerings better, and simple subscriber growth, which has steadily compounded over time:

{kind=link}

At the same time as AXP has grown revenues and profits (and thereby demand for AXP stock), they've also been shrinking the supply of shares over time.

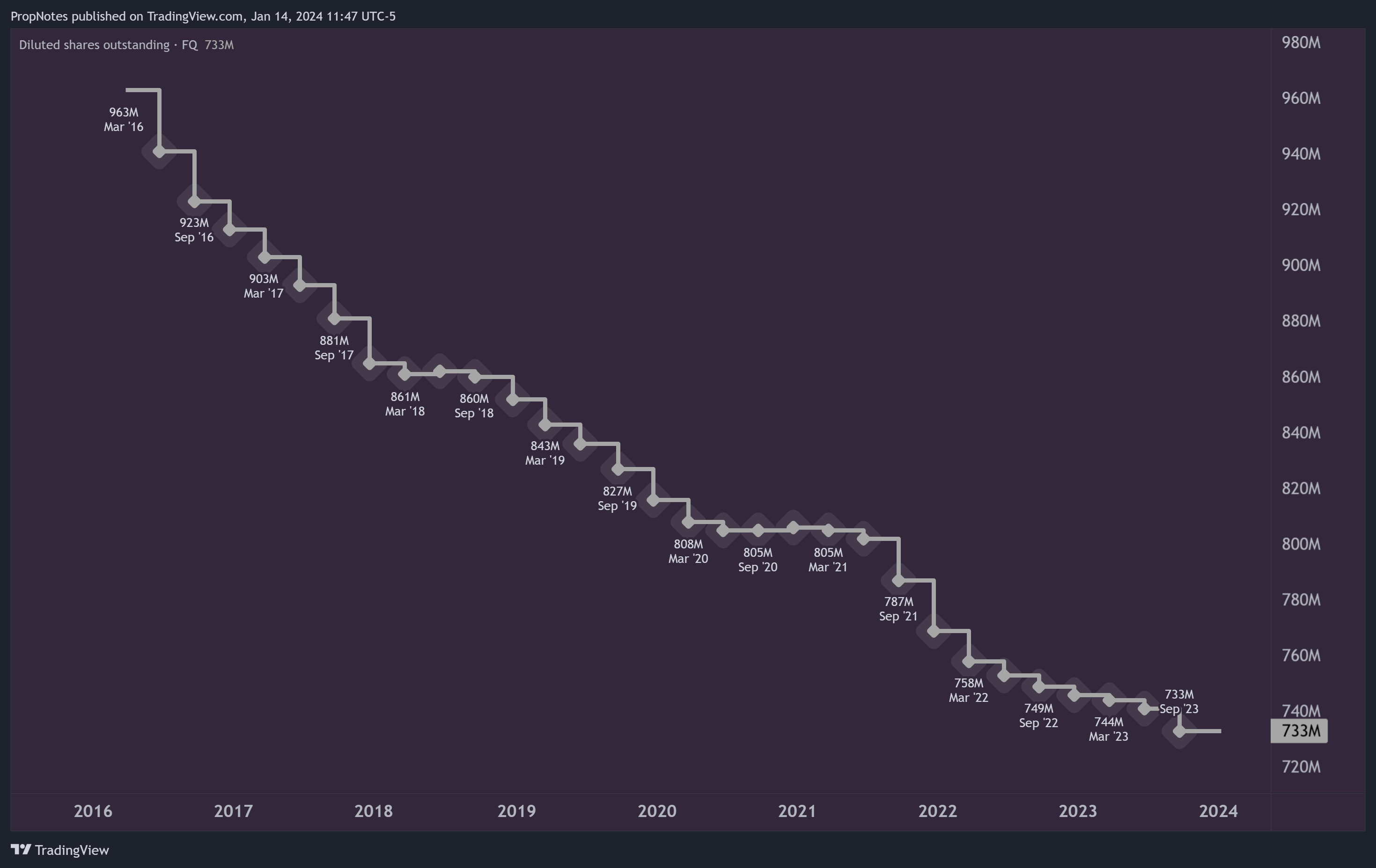

Since Q1 2016 AXP has repurchased over 21% of the company's diluted outstanding supply; more than 200 million shares worth:

{kind=link}

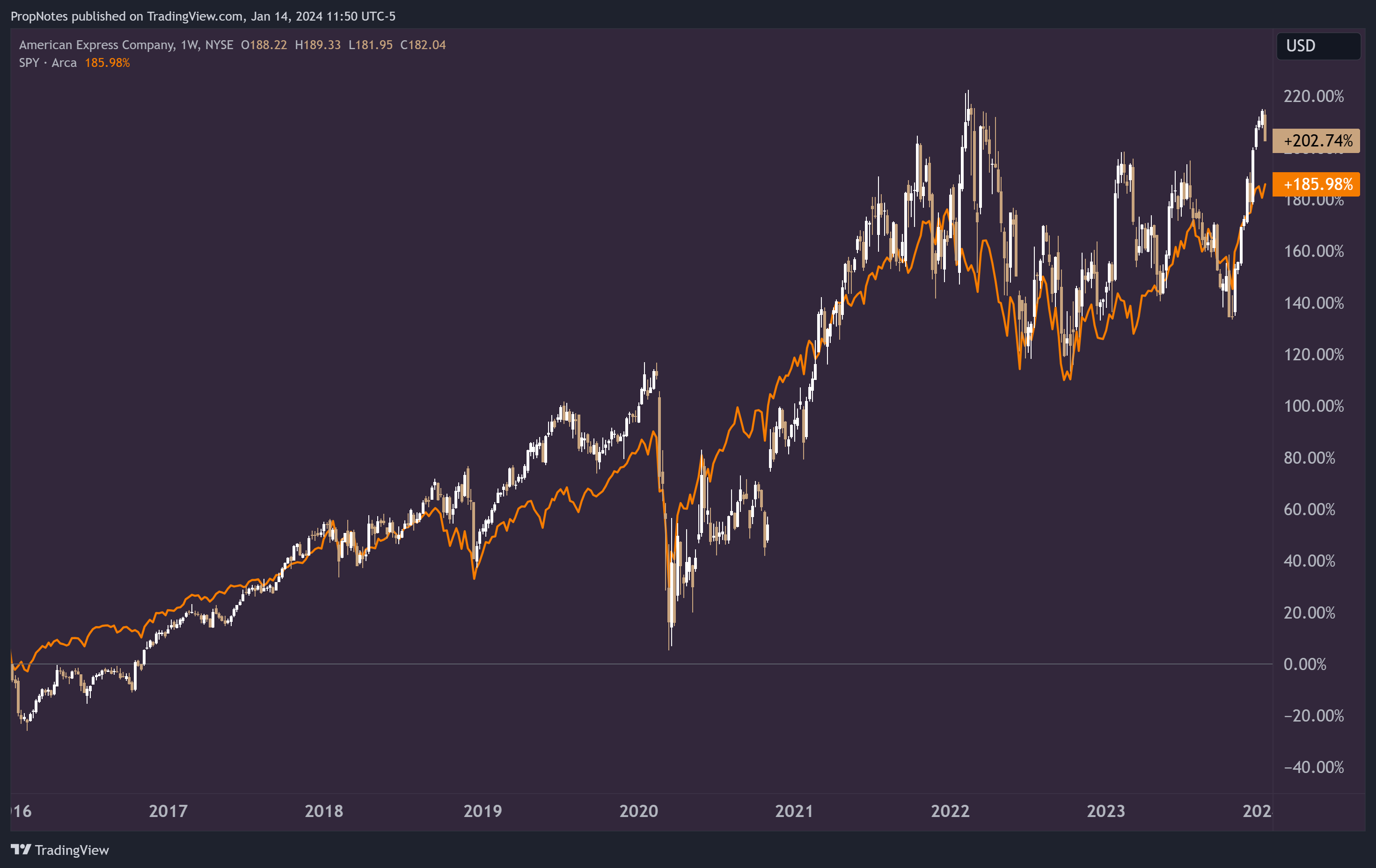

This combination of increasing demand for shares and a dwindling supply has resulted in total returns for AXP shareholders of more than 200% since 2016, which has outpaced the S&P 500 by more than 20%:

{kind=link}

For what some may perceive to be a 'sleepy' financial company, this may be surprising.

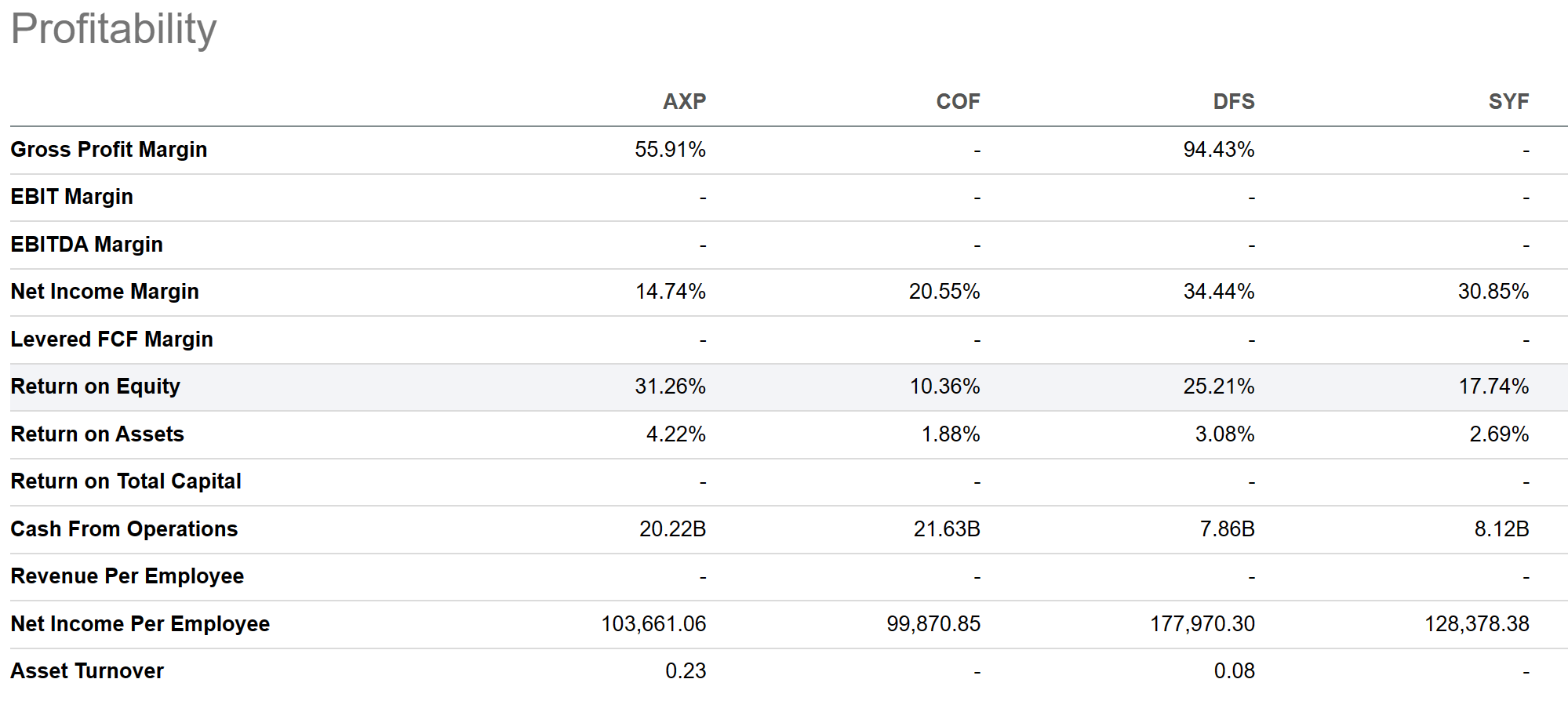

When looking at peers, however, it's clear that there's nothing sleepy about AXP's ability to make money, as the company sports a peer-group-leading 31.3% ROE, and more than 4.2% ROA:

{kind=link}

This is due to the fact that as one of four major card network operators globally, AXP's competitive position is extremely robust.

Finally, AXP's revenue base is somewhat self-hedging from an inflation/business cycle perspective. As rates (and thus NIM's) go down, AXP earns more from card fees and transactions as people get out and participate more in the economy.

As rates go up and the company sees reduced payment volume, NIMs increase, thus hedging the business's revenue streams. You can see this dynamic on the financial statement we included above. This is one of the core reasons that AXP has been able to compound an investment's capital without much disruption in the way that it has.

Why Now?

All of this is good to know, but what makes now the right time to invest in AXP stock?

In short, AXP is trading at a good price, and could be on the cusp of regaining momentum following a long period of lagging the market. Let's break these two components down.

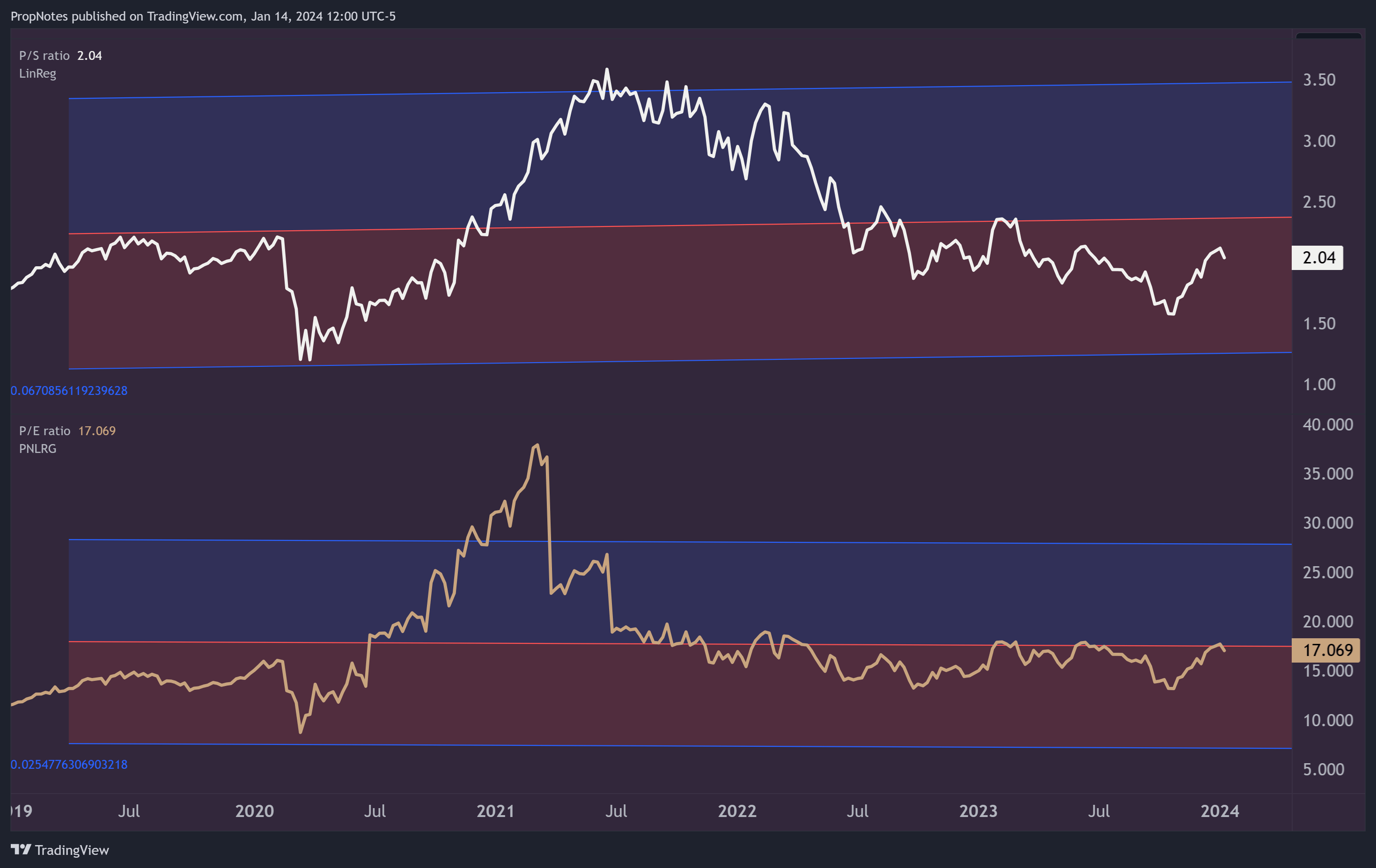

First off, AXP is well priced. It's not scraping the bottom of the barrel (which may even be concerning depending on the context), but it is trading at a lower sales and earnings multiple than its average over the last 5 years or so:

{kind=link}

On the top line, you can see that AXP is firmly in the red zone, which is the lower half of the company's standard deviation for revenue sales multiple since the start of 2019. This indicates that it could be a good time to invest, especially if AXP were to re-expand into its average long-run valuation paradigm.

On the bottom line, you can see that the company looks a little more reasonably valued from a net income perspective, trading right near the center of the linear regression.

While these aren't huge margins of safety from a valuation standpoint, it's rather difficult to find good companies at comparatively great prices barring some extreme market event, like Covid.

The good news is that it appears as though AXP's relative momentum is about to improve as well.

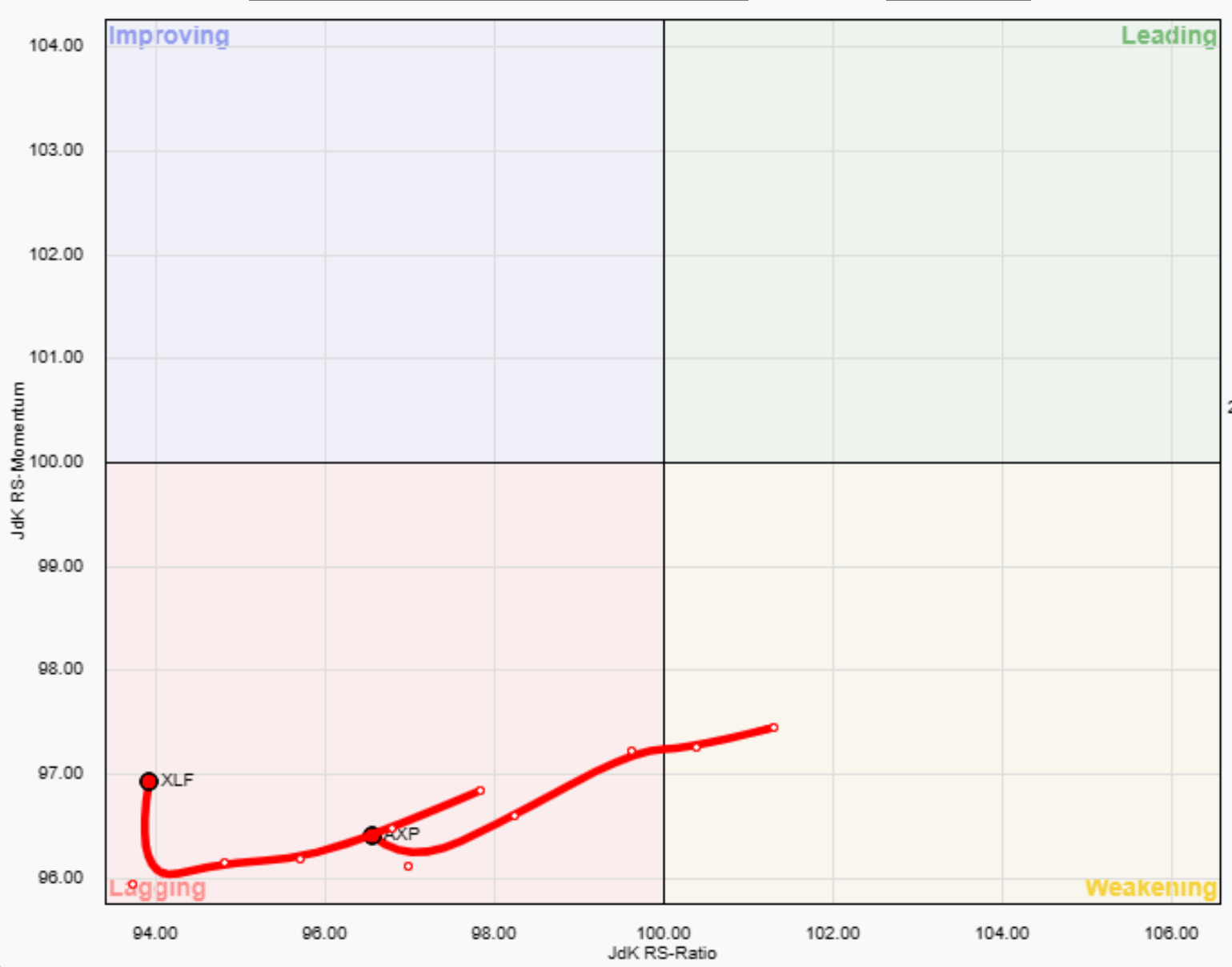

Based on the RRG measurement taken below, it's clear that AXP and the financial sector ( XLF ) at large is beginning to see some positive momentum, as they begin to head for the "Improving" category, turning away from their lagging downslide trajectory:

{kind=link}

In case you've never used an RRG before, it basically works like a clock. stocks and sectors rotate around the center in a clockwise fashion typically, with the 8:00-1:30 zone typically being the best time to allocate capital to an opportunity.

There's statistical outperformance proven to come from this tool as well when it comes to predicting returns one month out:

{kind=link}

It's true that AXP is in the "Lagging" sector, but this is important for two reasons. One, because XLF has actually shown the best relative performance (for some reason?) when lagging on a momentum basis. And two, because once it likely transitions to the improving and leading sectors over the next several quarters, it will likely also see improved performance as a result of the inherent function of the RRG.

Either way, AXP looks relatively well priced and set to improve momentum wise vs. the S&P, which could make it a great investment for the medium and long term.

Risks

There are some risks to our thesis; and here are the three key ones.

- Consumer Sentiment - While AXP is relatively insulated from almost all macro risks (including the consumer), as we've laid out when we talked about revenue hedging, there have been cases over the last few decades where consumer spending was impacted at the same time rates were low. Covid is a prime example of this, and in 2020, AXP's net income dropped from its average around $7 billion per annum to around $3 billion. The company still made money, but it was a big hit that caused the stock to crash. Keep an eye out for this - they're usually buying opportunities.

- Regulatory Risk - AXP isn't a 'big bank' in the traditional sense, so they usually get off relatively light when it comes to consumer protections, risk ratios, and other regulatory requirements that can hamper capital returns to shareholders. That said, they are still a big company in a relatively uncompetitive industry, and there is a risk that card networks could be targeted by Congress or the CFPB due to uncompetitive practices. This would be a longer-term profit headwind if it were to crop up, but it's far from a hot button issue at the moment.

- Earnings Releases - Finally, continued earnings releases from the company stand to add some volatility into the investment mix. Near term, AXP is set to release earnings on January 26th, which is less than two weeks away. This release looks to be more of the same, as management has largely beaten / met projections for the last few years, but releases can always cause volatility. Even if the numbers are good, there's no telling how the market will react to them. Needing to liquidate shares for whatever reason, especially near an earnings release, could lock in suboptimal prices going forward, which is a risk.

Summary

All in all, AXP is a great company that deserves consideration when it comes to investing your hard-earned capital.

The company has performed well due to its strong business position, solid management, and expense control, and the company stands to outperform into the coming years due to its relatively attractive valuation, improving momentum situation, and continued share buybacks.

Toss in a modest (but well supported) 1.3% dividend, and the bullish picture is complete.

We initiate coverage on AXP at a "Buy" rating.

Cheers!

For further details see:

American Express: A Potential 'Forever Hold'