AXP - American Express: Ongoing Growth Makes It Attractive

2023-12-05 07:49:57 ET

Summary

- American Express shares have risen 10% in the past year and 26% since my last article, and I see further upside potential.

- AXP is winning in the marketplace, attracting younger consumers and experiencing strong card growth while spending per card is also rising.

- The company's financial performance is solid, with increased spending levels, rising revenues, and positive operating leverage.

- While credit losses have risen, I expect recent stabilization to continue.

Shares of American Express (AXP) have been a solid performer over the past year, rising about 10%. Since I last wrote about the company in October 2022 , shares have returned 26%, justifying my buy rating. Given this run, now is an appropriate time to consider whether shares have further upside or if investors should take profits. Ultimately, I continue to view AXP as a strongly positioned premium franchise in the financial sector.

{kind=link}

In the company's third quarter , AXP earned $3.30, up by 34% from last year, with net income up 30% and the share count down over 2%. That leaves the company on track to earn over $11.50 this year, in keeping with my expectations. Importantly for the stock's outlook, management continues to target mid-teens EPS growth next year. Looking through the business's performance, that appears to be a credible outlook in my view.

First, it is important to highlight that the company is winning in the marketplace. So many legacy brands have struggled to remain relevant to a newer generation of customers. American Express, which has long maintained a premium brand, is a clear exception to this. Millennials and Gen Z account for 18% of spending growth and 60% of new consumer account growth. With its focus on travel-oriented benefits, younger consumers who often value "experiential" consumption have flocked to its platform.

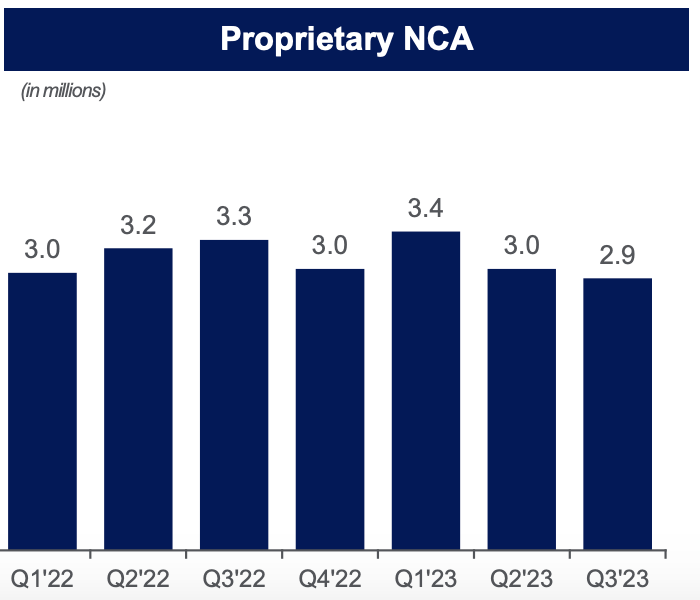

This has led to strong card growth. As you can see, below, the company has consistently been adding about 3 million new card accounts every quarter, with 2.9 million new cards in the quarter. As a consequence, cards-in-force rose by 5% from a year ago to 138 million. Due to price increases and customer migration to premium cards, the average fee per card rose by 13% to $93. AXP is winning new clients while also raising prices, a testament to the appeal of its product.

{kind=link}

Importantly, its customers are using their cards. Network volumes rose by 7% to $420 billion. With 5% card-count growth, the company is seeing about 2% per-customer spending growth. Average basic card member spending was $6,000 in the quarter. For the year, spending should be about $24,000, in keeping with its higher-end customer base, a key strength I will speak to in greater detail below. I view it as a positive that volume growth is being driven more by card count growth than by an unsustainable pace of per-capita spending growth.

Across spending categories, we are seeing divergences across categories. Travel and entertainment spending remains extremely powerful; it was up 13% with the US consumer up 13%, US business up 6%, and international up 20%. There is really little evidence of the surge in travel since the end of pandemic-era restriction coming to an end. While US consumer spending continues to be solid, total small and medium-sized businesses spending was up a more modest 2%--this accounts for 83% of its US corporate business. Many small businesses have faced inflation and wage-cost pressures on their business, which has soured their outlook for many months . With some of these pressures moderating, I do not expect spending to turn down from here, though I would continue to expect US consumer growth to be stronger. One other bright spot continues to be international, where growth was 15% due to increased foreign travel.

Thanks to increased spending levels, discount revenue rose 7% or $520 million to $8.4 billion-these are the fees the company earns from merchants on each transaction. That was nearly a third of the company's revenue growth, while card fees rose 20% to $1.85 billion thanks to the factors described above. AXP is also generating this growth in a cost-effective way. For instance, while card revenue rose 20%, business development rose by 17%. While spending rose by 7%, rewards costs rose just 6%. Each dollar of expense spending is driving more than a dollar of fee revenue, pointing to positive operating leverage.

Aside from higher customer counts, we are seeing more customers carry balance on cards, in keeping with the rise in credit card debt seen over the past couple of years. Loans and receivables rose to $183 billion, up 15% from last year. Because of higher balances and higher rates, net interest income of $3.4 billion was up 34%, driving half of the company's revenue gains. AXP earned an 11.7% average rate on loans, up 90bp from last year, as credit card loan rates do not move as quickly as the fed funds rate historically.

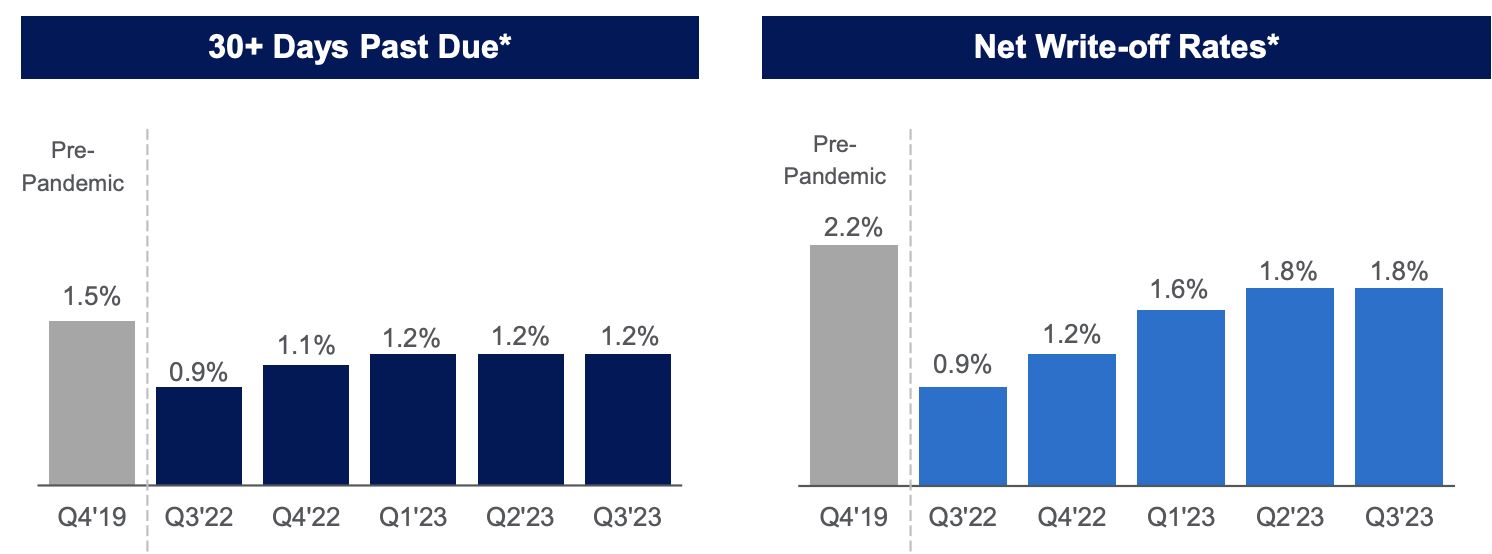

While higher balances do drive more net interest income, they can contribute to higher reserves, and credit quality is a concern for the sector. Provisions for credit losses rose 58% to $1.2 billion. First, I think it is important to highlight that even with this provision increased profits rose by 34% because of the growth in the business, and the still relatively strong credit quality AXP has. AXP built $321 million in reserve from $387 million last year, but there were $912 million in write-offs from $391 million last year. While delinquencies and charge-offs have risen relative to 12-18 months ago, they actually are still better than pre-COVID. They also have been stabilizing. Remember, when you consider that AXP earns 11% interest on its cards, a 1.8% write-off rate is easily funded by interest margin.

{kind=link}

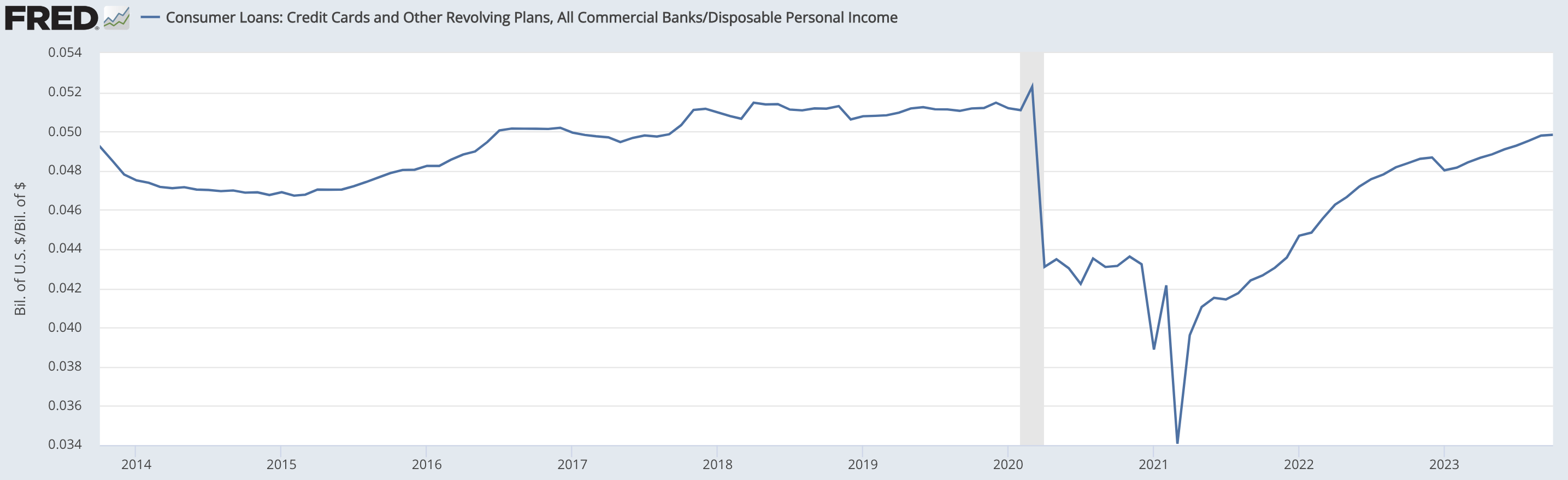

My view is that we are likely to see charge-offs and reserves persist around current levels, but that we are not likely to see substantial further deterioration. This is because results are really returning to more of a "normal" level after government stimulus kept losses unsustainable low post-pandemic. This is consistent with the fact that relative to income, credit card debt has been rising, but it actually remains below pre-COVID levels. I also view it as a positive that over 70% of revolving growth comes from tenured, not new, customers. These are consumers whose creditworthiness AXP is quite familiar with.

{kind=link}

After this quarter's build, American Express has $5 billion in reserves, or about a 2.7% ratio of allowance for credit losses relative to loans and receivables. This provides 225% of 30+ day delinquencies. I like to see this metric at least at 250%, and AXP management has said that it expects ongoing builds for several quarters. I would expect to continue to see $300-$350 million quarterly builds over the next year, which should keep credit costs around $1.2 billion per quarter. In other words, AXP is likely to have credit costs stay near current levels, rather than rise further, or fall back to 2022 levels.

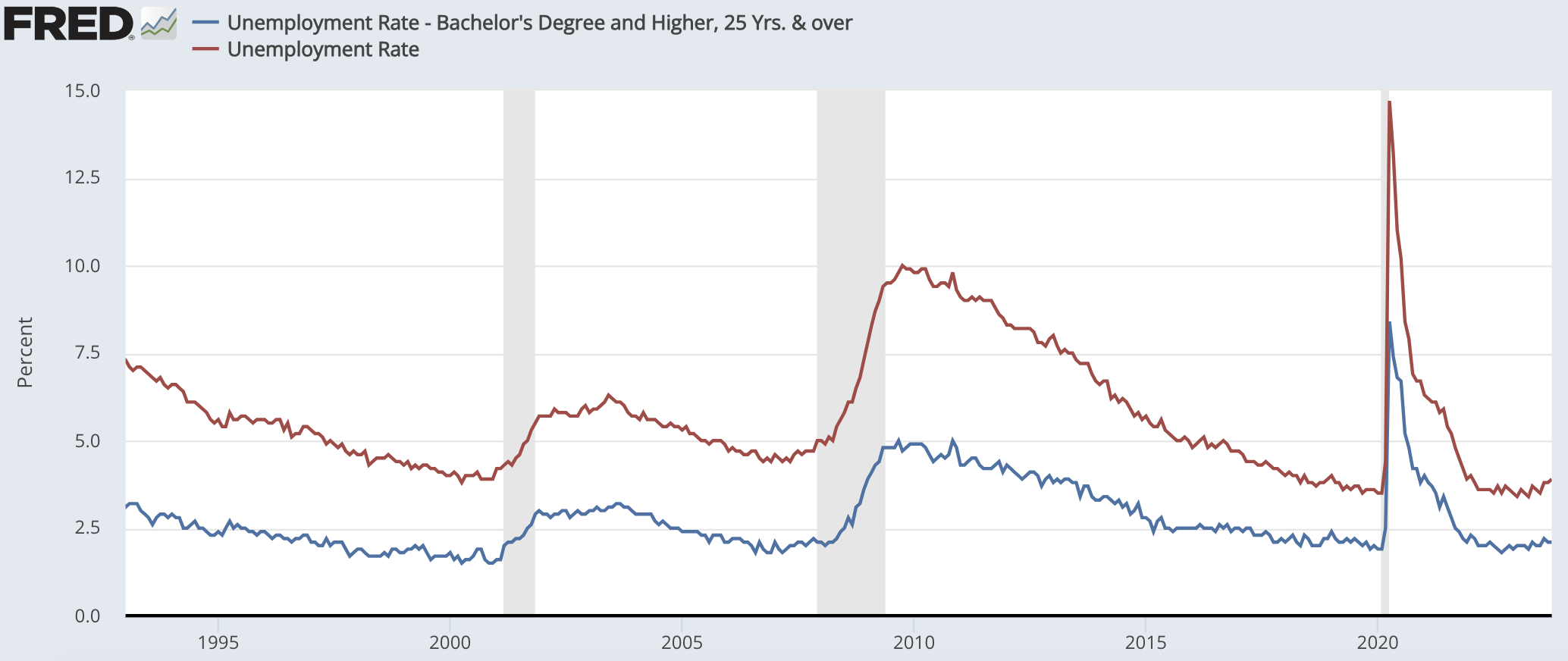

One reason I view AXP's loan book constructively is the nature of its customer base. It caters to higher-income consumers in general, as evidenced by their spending level. These consumers tend to be more resilient. As you can see below, for instance, college-educated unemployment is structurally lower than total unemployment, and it rises much less during recessions. It is hovering around 2% now. With a solid labor market and a customer base less likely to lose a job, AXP should continue to see fairly low defaults.

{kind=link}

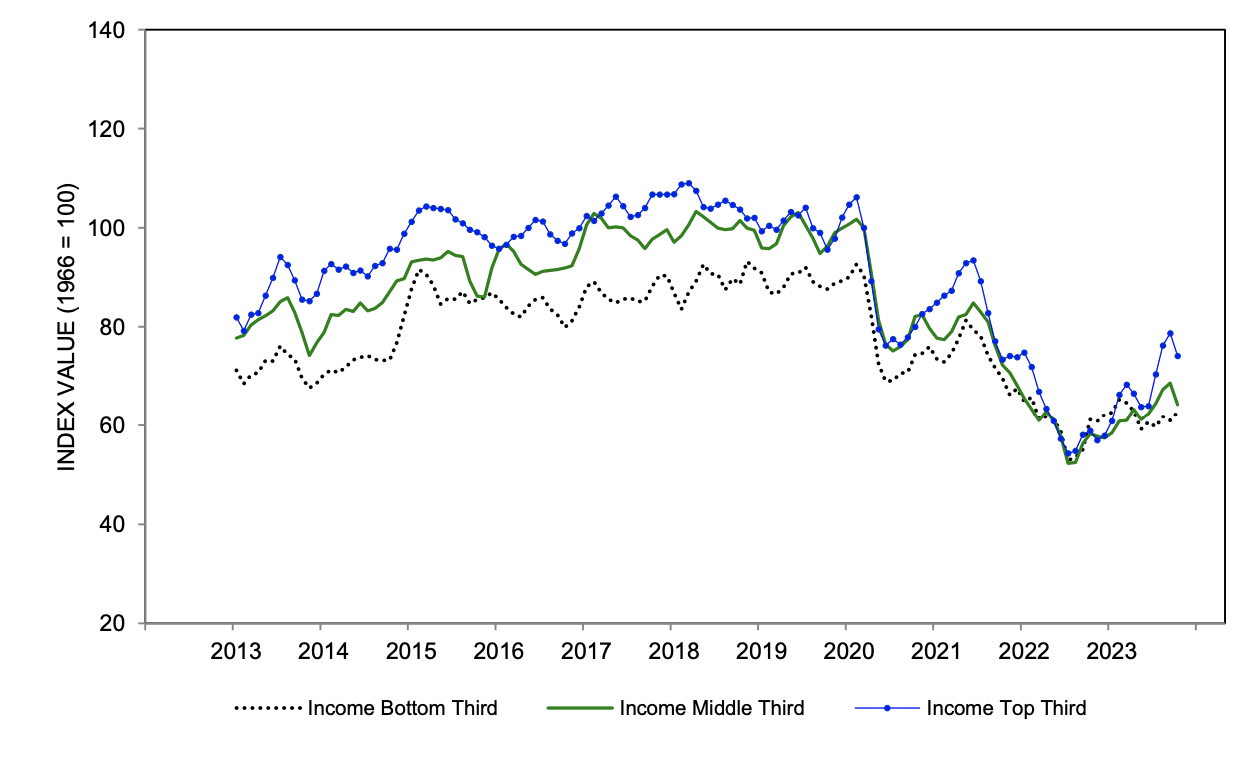

Much has also been made of weak consumer sentiment. However, I would note that consumers with top-third incomes feel meaningfully better than overall consumers. No consumer group is pleased with the current conditions, of still-high prices and elevated mortgage rates, but higher-income consumers feel better, which is consistent with AXP's spending trends.

{kind=link}

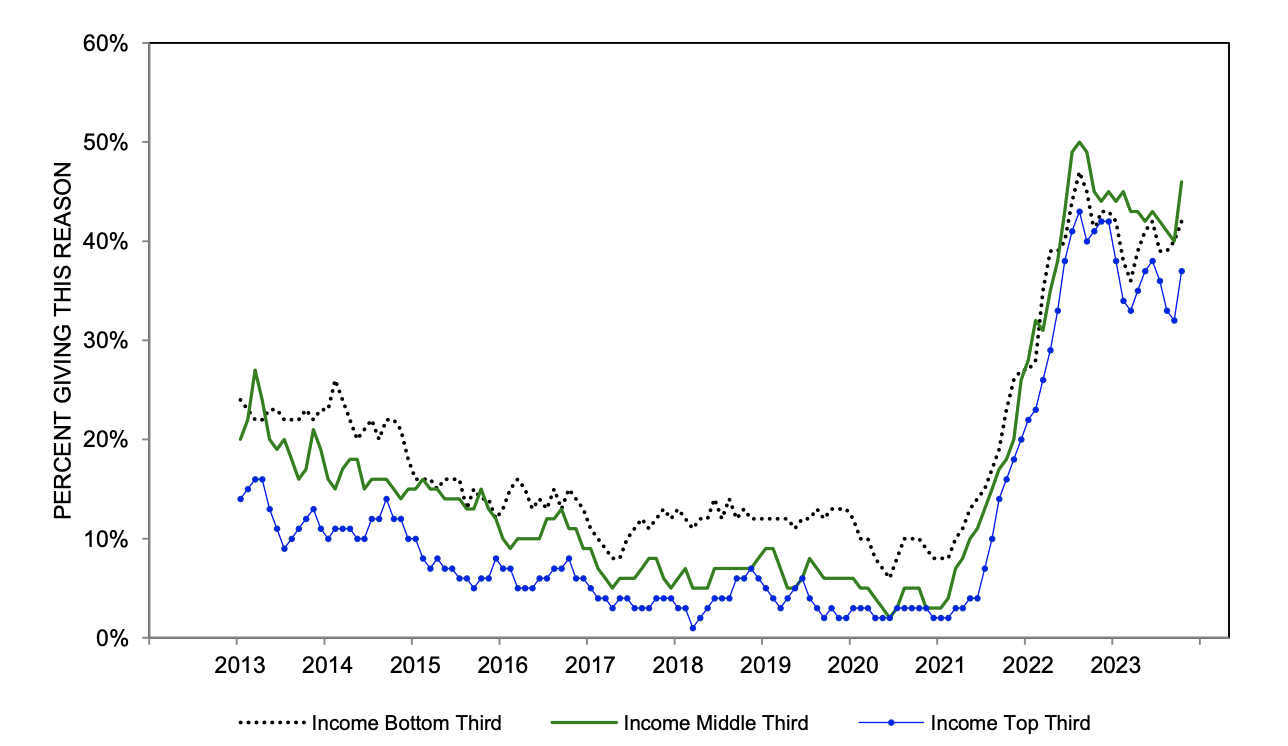

A reason for this is that higher-income consumers are less bothered by higher prices. While a large share of every income group says inflation has worsened their financial position, this has been less the case for higher-income consumers, in part because basic necessities like food and energy are a lower share of their spending mix.

{kind=link}

With its core customer base, AXP is relatively well positioned for credit losses to not rise substantially further, particularly as a recession appears less likely. The company also has a solid balance sheet. Its tier one common equity ratio is at 10.7%, up 10bp from last year, in keeping with its 10-11% target. This has come even as it has grown its business while reducing its share count by 2% and paying a 1.4% dividend. I would look for the company to allocate all incremental capital not needed to support business growth to shareholders.

Just given a higher starting card count and more loan balances, AXP is poised to generate about 7% growth next year if spending and card growth are flat. However, we are seeing the company continue to deliver underlying growth. Assuming modest pricing gains, 2-4% spending growth, and 3-5% customer growth, alongside balances that rise at a slowing pace, AXP should be able to deliver $12.75-13.00 in EPS, holding credit costs roughly flat. That should leave it with about $6-6.5 billion in capital return capacity, or about a 5% rate.

AXP is a premium franchise with a 5% capital return yield, yet it is trading at 13.5x earnings. American Express is one of the few quality growth companies in an increasingly commoditized industry, and at this valuation, it is compelling. I continue to view 15x earnings as a reasonable estimate, pointing to an upside past $192. With over 10% return potential, I would stay long AXP. Given its positioning, it remains a good opportunity for long-term investors.

For further details see:

American Express: Ongoing Growth Makes It Attractive