AXP - American Express Q4: Expect Decent Report But Stock Is A Hold

2024-01-15 07:09:00 ET

Summary

- American Express Company is expected to report impressive YoY EPS growth of nearly 30% and a 12.50% YoY jump in revenue for Q4.

- Expectations for Q4 earnings have been seesawing, with a downward trend in EPS estimates.

- Key things to monitor include record revenue, credit card metrics, international income, and a reduction in shares outstanding.

- I rate the stock a hold after a near 30% run since October 2023.

American Express Company ( AXP ) is set to report results for its Q4 and FY 2023, premarket on Friday, January 26th. Analysts expect the company to report GAAP EPS of $2.64 on the back of $15.95 billion in revenue. Should American Express meet the estimates, it'd represent an impressive YoY EPS growth of nearly 30% and a 12.50% YoY jump in revenue.

My most recent coverage on American Express was in July 2023, when I rated the stock a buy. Since then, American Express stock has returned 9% (including dividends) against the market's 4.50% return. With that background out of the way, let's now preview American Express' upcoming Q4 report on these parameters:

- Expectations heading into earnings.

- Historical surprise.

- Key things to look for.

- Valuation.

- Technical setup.

AXP Q4 Preview (Seekingalpha.com)

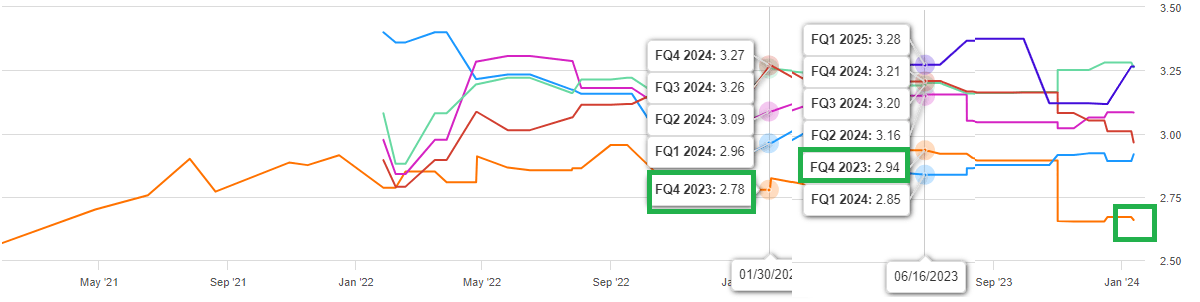

Seesawing Expectations, With A Downward Blip

Expectations have been seesawing as we head into the Q4 earnings report. Q4's EPS estimate has gone from $2.78 at the beginning of the year to $2.94 in June to $2.66 at present. It is also interesting to note that since October 2023, Q4's EPS expectation has gone down by nearly 8%. In addition, over the last 3 months, just 2/18 EPS revisions have been to the upside while 7/15 revenue revisions have been to the upside. This suggests there is a stronger belief in the company's revenue potential than profit potential.

{kind=link}

{kind=link}

Beat or Miss? Recent Trend Says It's A Coin Toss

American Express has beaten EPS estimates 10 out of the last 12 quarters and revenue estimates 8 out of the last 12 quarters. Worryingly for AXP investors like myself, the company has missed both EPS and revenue expectations in 2/4 most recent quarters. Earnings season in the financial sector is off to a mixed start as many big names ( here and here ) have beaten on EPS but missed on revenue. Will American Express continue the trend?

Key Things To Monitor

- American Express highlighted its 6th consecutive quarter of record revenue when it reported Q3 in October 2023. Will the company make it 7 in a row? I am willing to bet it does as the expectations are for $15.95 billion in Q4, with the holiday quarter typically being strong for consumer spending.

- November credit card metrics showed a return to seasonality as opposed to normalization from the pandemic era. On paper, this should help companies like American Express as, unfortunately, the pandemic affected the weak consumers disproportionately, leading to survival of the fittest. However, American Express reported a 58% jump in Provisions for Credit Losses [PCL] in Q3 2023 compared to Q3 2022. This number in Q4 should give us an indication of how confident Amex feels about the resilience of the economy and consumers.

AXP PCL (americanexpress.com)

- Even if you worry about US softness, American Express has enough clout internationally to at least cushion , if not entirely offset, the potential domestic pain. In Q3, international income more than doubled YoY to reach $387 million. Given this strength in Q3 2023, I am almost certain that Q4 2023 will show a significant jump in international income compared to the $15 million loss shown in Q4 2022 .

- Finally, American Express has slowly but surely been chipping away at its shares outstanding. Dating back to at least March 2021, AXP's share count has been going down every single quarter, for an overall reduction of 9% in that time period. I expect total shares to have gone down below 730 million when the company discloses its Q4 report. It may not seem like much on the surface but the 72 million reduction in share count since March 2021 means the company saves about $172.8 million in annual dividends (based on a $2.40 dividend per share).

{kind=link}

Valuation

- American Express stock is heading into earnings at a forward multiple of 16.21 while expected to grow earnings at the rate of 14%/yr for the next 5 years. That gives the stock an attractive Price-Earnings/Growth [PEG] ratio of 1.15.

- As a comparison, Visa Inc. ( V ) is trading at a forward multiple of 27 while Mastercard Incorporated ( MA ) is trading at a forward multiple of 35.

- At $182, the stock is trading nearly 10% below its median price target of $200. The 1.30% yield, while low, is extremely well-covered with a payout ratio of 21% and adds a bit of a cushion for investors.

Interestingly, Seeking Alpha's quant ratings give AXP stock a "D-", which I believe is due to the comparatively low valuation that bank stocks get in the financial sector. The more accurate comparison for AXP is with the likes of V and MA and on that front, AXP looks undervalued.

AXP Valuation Grade (Seekingalpha.com)

Technical Indicators

From a technical perspective, American Express stock is heading into the Q4 report and the new year with a strong base. The stock's Relative Strength Index [RSI] is in my preferred sweet spot, in the 60s, as it shows accumulation as well as provides further upside room before getting overbought. In addition, the stock is comfortably trading above both the 100- and 200-day moving averages. Q4 report will be critical though, as a disappointing report or outlook may push the stock lower and the next long-term support (100-day moving average) is a good 10% away.

AXP Moving Avgs (Barchart.com) AXP RSI (stockrsi.com)

Conclusion

If you feel like you are having a hard time decoding the strengths (or weaknesses) of the consumer, you are not alone. American Express stock has two downgrades ( here and here ) and one upgrade in the new year already, and we are in week three. While I expect Amex to report a good Q4, I have a much stronger conviction about the long-term potential of the company, especially as it continues its international expansion. At the same time, I'd like to note that the stock has gone up nearly 30% since October 2023, and would recommend waiting for a pullback before buying. I rate the stock a strong hold and continue reinvesting my dividends to accelerate my share count.

For further details see:

American Express Q4: Expect Decent Report But Stock Is A Hold